|

市场调查报告书

商品编码

1846144

片状成型和块状成型模塑胶:市场份额分析、行业趋势、统计数据和成长预测(2025-2030)Sheet Molding And Bulk Molding Compounds - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

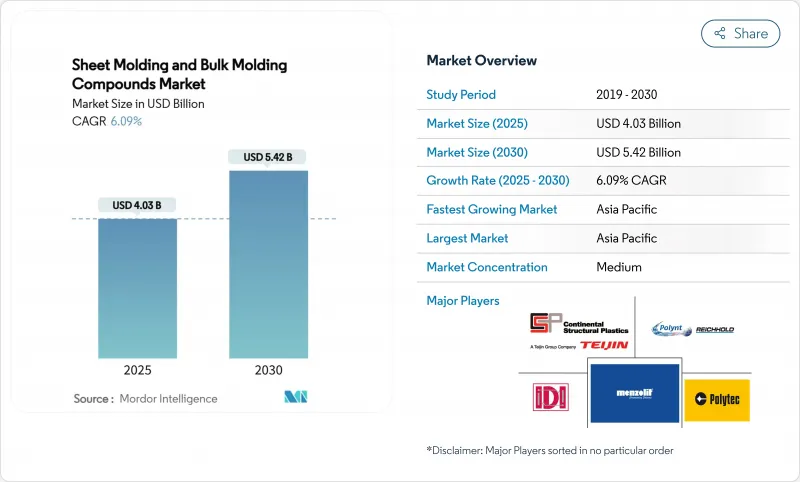

片状成型和块状成型模塑胶市场规模预计在 2025 年为 40.3 亿美元,预计到 2030 年将达到 54.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.09%。

电动车轻量化结构部件的持续需求、模压成型的低废品率以及树脂化学性能的改进,持续推动资本流入新的产能。单一零件成本的降低,尤其是对于先前依赖多级冲压的复杂形状零件,正在加速汽车和家电应用中用模压成型复合复合材料取代金属衝压。目标商标产品製造商现在指定使用具有A级表面处理的先进片状成型材料,这些材料可直接用于外部,并省去了曾经限制其应用的二次喷漆步骤。亚太地区在高流动性、低密度片状成型化合物方面保持着成本领先地位,但欧洲关于苯乙烯排放的法规正在推动环氧基替代品的快速发展。

全球片状成型和块状成型塑胶市场趋势和洞察

电动和混合动力汽车原始设备製造商推动轻量化

电动车拥有大型电池组,因此每减轻一公斤重量都意味着续航里程的增加。因此,汽车製造商正在重新设计车门盖、车身面板和电池外壳,使用先进的片状模塑胶。与同类铝製设计相比,这些材料可减轻高达 40% 的零件重量,同时满足碰撞负载路径和隔热要求。特斯拉、通用汽车和知名品牌已公开推出采用单次压缩成型的多部件整合策略,从而减少焊接操作和生产线节拍时间。随着这些计画从试点规模扩大到全面生产,片状成型和块状模塑胶的市场参与企业正从中受益。

电子电气元件成型中心产能快速扩张

亚太地区中国、越南和马来西亚的电子产业丛集持续安装配备自动进料和红外线固化控制的高吨位压机。将改质商、注塑商和终端设备组装商集中位置,缩短了供应链,使製造商能够满足连接器外壳和马达绝缘系统所需的严格尺寸公差。中国政府旨在实现高性能聚合物自给自足的计划正在推动这一扩张,使该地区能够满足不断增长的全球需求。

苯乙烯和玻璃纤维价格波动

苯乙烯单体的交易週期紧凑,受苯原料波动和运输限制的影响。苯乙烯价格每吨100美元的波动会直接影响树脂价格,挤压那些没有长期供应合约的小型片状成型塑胶生产商的利润空间。同时,由于许多结构级产品的玻纤含量接近65%(重量百分比),玻璃纤维额外费用也进一步影响了价格的稳定性。

細項分析

2024年,聚酯树脂占据了片状成型和块状成型塑胶市场份额的55.19%,这得益于低成本、广泛的供应商基础以及与传统压缩生产线一致的固化速度。该细分市场将继续受益于对汽车引擎盖下盖和结构内部支架的需求。同时,到2030年,环氧树脂牌号的复合年增长率将达到6.92%,这得益于挥发性有机化合物含量的降低和耐热性的提高,这对电力传动系统设计师很有吸引力。赢创主导的玻璃纤维增强环氧树脂电池外壳专案检验,其重量减轻了近10%,同时保持了车辆认证所需的关键压溃力阈值。随着环氧树脂体系的成熟,可能会出现将聚酯表皮与环氧树脂芯材混合的混合积层法,以平衡经济性和强度。

玻璃纤维凭藉其良好的性价比和优异的电气元件介电强度,预计到2024年将保持其销售额的80.22%。主要玻璃纤维製造商持续扩建熔炉,稳定了供应,并支持亚太和北美地区汽车玻璃纤维的大量生产。碳纤维片状成型塑胶的复合年增长率预计将达到7.06%,在航太二级结构和高端跑车领域发展势头强劲。用于绘製纤维取向的製程模拟工具可缩短开发週期,提供可预测的机械性能,并降低废品率。混合纤维毡采用交替的玻璃层和碳纤维层,有助于在不牺牲刚度的情况下实现中等成本目标。

片状成型和块状成型模塑胶市场报告按树脂类型(环氧树脂、聚酯)、纤维类型(玻璃纤维、碳纤维)、製造工艺(压缩成型、转注成型、其他)、最终用户行业(汽车和运输、电气和电子、其他)和地区(亚太地区、北美、欧洲、南美、中东和非洲)细分。

区域分析

亚太地区将维持其成本优势,到2024年将占48.54%的市占率。受国内电动车产量成长、中阶消费性电子产品消费成长以及政府鼓励国内复合材料零件生产的激励措施的活性化,压平机产能已接近满载运作。预计该地区需求复合年增长率为6.45%,片状成型和块状成型塑胶市场将继续转移到亚洲价值链。

北美是销量第二大的地区。早期推出的电动皮卡需要大型结构盖,而航太计画则使用高模量碳片状成型塑胶作为二次结构。联邦政府为陆上电池工厂提供资金的政策正在鼓励新的复合材料电池盒生产线,并促进当地复合材料的消费。

欧洲持续推行严格的环保法规,推动了低苯乙烯片状成型系统和环氧树脂创新技术的采用。汽车製造商蓝图在2030年至2035年之间逐步淘汰内燃机,这将推动对轻质复合材料的需求。同时,强大的化学基础设施为专用树脂添加剂提供了支持,这些添加剂可增强机械性能并延长模具寿命。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 电动和混合动力汽车原始设备製造商推动轻量化

- 电子电气元件成型中心产能快速扩张

- 与金属衝压相比,批量压缩成型更具成本效益

- 高流动性、低密度片状成型零件 (SMC) 辅助打造 A-Class 车身面板

- 智慧面板的套模电子 (IME) 集成

- 市场限制

- 苯乙烯和玻璃纤维价格波动

- 工程热塑性塑胶取代电池盒中的片状成型组件(SMC)

- 回收消费后热固性树脂的障碍

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 依树脂类型

- 聚酯纤维

- 环氧树脂

- 依纤维类型

- 玻璃纤维

- 碳纤维

- 按製造工艺

- 压缩成型

- 注塑/转注成型

- 树脂转注成形(RTM)

- 拉挤成型

- 按最终用户产业

- 汽车和运输

- 电气和电子

- 建筑/施工

- 航太

- 电器产品

- 其他终端用户产业(能源等)

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- AOC

- Ashland Container Corporation

- Astar SA

- Continental Structural Plastics(Teijin)

- Core Molding Technologies

- CSP

- DIC Corporation

- IDI Composites International

- Kingfa Sci.&Tech. Co.,Ltd.

- LyondellBasell Industries Holdings BV

- Menzolit

- National Manufacturing Group

- OPmobility SE

- POLYNT SPA

- Polynt-Reichhold

- Polytec Group

- Polytec Masterbatch LLC

- TORAY INDUSTRIES, INC.

第七章 市场机会与未来展望

The Sheet Molding & Bulk Molding Compounds Market size is estimated at USD 4.03 billion in 2025, and is expected to reach USD 5.42 billion by 2030, at a CAGR of 6.09% during the forecast period (2025-2030).

Sustained demand for lightweight structural parts in electric vehicles, low scrap rates from compression molding, and improved resin chemistries keep capital flowing into new capacity. Cost reductions per part, especially in complex geometries that previously relied on multi-stage stamping, accelerate the replacement of metal stampings with compression-molded composites across automotive and electrical applications. Original equipment manufacturers now specify advanced sheet molding materials with Class-A finishes, allowing direct exterior use and eliminating secondary paint steps that once limited adoption. Asia-Pacific retains cost-leadership in high-flow, low-density sheet molding compounds, while European regulations on styrene emissions fast-track epoxy-based alternatives.

Global Sheet Molding And Bulk Molding Compounds Market Trends and Insights

Light-weighting Push from Electric Vehicles and Hybrid Vehicle OEMs

Electric models move large battery packs, so every kilogram saved extends range. Automakers therefore redesign closures, body panels, and battery housings with advanced sheet molding compounds that cut part weight by up to 40% versus comparable aluminum designs while satisfying crash-load pathways and thermal shielding demands. Tesla, General Motors, and leading Chinese brands have publicly outlined multi-part consolidation strategies that favor single-shot compression molding, reducing weld operations and line takt time. Sheet molding and bulk molding compounds market participants benefit as these programs scale from pilot to full volume production.

Rapid Capacity Additions in Electrical and Electronics Components Molding Hubs

APAC electronics clusters in China, Vietnam, and Malaysia continue installing high-tonnage compression presses equipped with automated material dosing and infrared curing control. Co-location of compounders, molders, and end-device assemblers shortens supply chains and helps manufacturers meet stringent dimensional tolerances required for connector housings and motor insulation systems. Government programs in China that target self-sufficiency in high-performance polymers reinforce this build-out, positioning the region to support global demand spikes.

Styrene and Fiberglass Price Volatility

Styrene monomer trades in tight cycles, reacting to benzene feedstock swings and shipping constraints. Each USD 100 per ton change in styrene cascades into resin pricing, squeezing margins for small sheet molding compounders that lack long-term supply contracts. Simultaneous fiberglass surcharges further hinder price stability because glass fiber content approaches 65 wt % in many structural grades.

Other drivers and restraints analyzed in the detailed report include:

- Cost-effective High-volume Compression Molding versus Metal Stamping

- High-flow, Low-density Sheet Molding Components Enabling Class-A Body Panels

- Engineering Thermoplastics Replacing SMC in Battery Boxes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester resin accounted for 55.19% sheet molding and bulk molding compounds market share in 2024 thanks to low cost, broad supplier base, and cure kinetics tailored to legacy compression lines. The segment continues to profit from automotive demand for under-hood covers and structural interior brackets. At the same time epoxy grades post a 6.92% CAGR toward 2030, driven by reduced volatile organic compound content and elevated heat resistance that appeals to electric drivetrain designers. The Evonik-led program for glass-fiber-reinforced epoxy battery housings validated weight reductions approaching 10% while maintaining crush-force thresholds critical to vehicle homologation. As epoxy systems mature, hybrid lay-ups that blend polyester skins with epoxy cores may emerge to balance economics and strength.

Glass fiber kept 80.22% of 2024 revenue due to favorable cost-to-performance and excellent dielectric strength for electrical parts. Continuous furnace expansions at major glass fiber producers stabilize supply, supporting high-volume automotive launches in Asia-Pacific and North America. Carbon fiber sheet molding compounds, posting a 7.06% CAGR, gain momentum in aerospace secondary structures and premium sports cars where curb-weight targets override raw-material premiums. Process simulation tools mapping fiber orientation now shorten development cycles, delivering predictable mechanical performance and cutting scrap rates. Hybridized fiber mats that alternate glass and carbon layers help designers hit mid-tier cost targets without compromising stiffness.

The Sheet Molding & Bulk Molding Compounds Market Report is Segmented by Resin Type (Epoxy and Polyester), Fiber Type (Glass Fiber and Carbon Fiber), Manufacturing Process (Compression Molding, Transfer Molding, and More), End-User Industry (Automotive and Transportation, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific retains the cost advantage that underpins its 48.54% share in 2024. Intensifying domestic EV production, rising middle-class appliance consumption, and government incentives for composite part localization keep presses running near capacity. With estimated demand growth translating to a 6.45% regional CAGR, the sheet molding and bulk molding compounds market continues to shift toward Asian value chains.

North America sits second in regional revenue. Early electric-pickup launches require large structural covers, and aerospace programs consume high-modulus carbon sheet molding compounds for secondary structures. Federal policy that funds onshore battery factories encourages new composite battery-box lines, lifting local compound consumption.

Europe upholds strict environmental rules that spur adoption of low-styrene sheet molding systems and epoxy innovations. Automaker roadmaps that phase out internal combustion between 2030 and 2035 expand demand for lightweight composites. Meanwhile, robust chemical-industry infrastructure supports specialized resin additives that raise mechanical performance and prolong mold life.

- AOC

- Ashland Container Corporation

- Astar S.A.

- Continental Structural Plastics (Teijin)

- Core Molding Technologies

- CSP

- DIC Corporation

- IDI Composites International

- Kingfa Sci.&Tech. Co.,Ltd.

- LyondellBasell Industries Holdings B.V.

- Menzolit

- National Manufacturing Group

- OPmobility SE

- POLYNT SPA

- Polynt-Reichhold

- Polytec Group

- Polytec Masterbatch LLC

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Light-weighting Push from Electric Vehicles and Hybrid Vehicle OEMs

- 4.2.2 Rapid Capacity Additions in Electrical and Electronics Components Molding Hubs

- 4.2.3 Cost-effective High-volume Compression Molding versus Metal Stamping

- 4.2.4 High-flow, Low-density Sheet Molding Components (SMC) enabling Class-A body Panels

- 4.2.5 Integration of In-mold Electronics (IME) for Smart Panels

- 4.3 Market Restraints

- 4.3.1 Styrene and Fiberglass Price Volatility

- 4.3.2 Engineering Thermoplastics Replacing Sheet Molding Components (SMC) in Battery Boxes

- 4.3.3 End-of-life Recycling Hurdles for Thermosets

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Polyester

- 5.1.2 Epoxy

- 5.2 By Fiber Type

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.3 By Manufacturing Process

- 5.3.1 Compression Molding

- 5.3.2 Injection / Transfer Molding

- 5.3.3 Resin Transfer Molding (RTM)

- 5.3.4 Pultrusion

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Electrical and Electronics

- 5.4.3 Building and Construction

- 5.4.4 Aerospace

- 5.4.5 Domestic Appliances

- 5.4.6 Other End-user Industries (Energy, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AOC

- 6.4.2 Ashland Container Corporation

- 6.4.3 Astar S.A.

- 6.4.4 Continental Structural Plastics (Teijin)

- 6.4.5 Core Molding Technologies

- 6.4.6 CSP

- 6.4.7 DIC Corporation

- 6.4.8 IDI Composites International

- 6.4.9 Kingfa Sci.&Tech. Co.,Ltd.

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 Menzolit

- 6.4.12 National Manufacturing Group

- 6.4.13 OPmobility SE

- 6.4.14 POLYNT SPA

- 6.4.15 Polynt-Reichhold

- 6.4.16 Polytec Group

- 6.4.17 Polytec Masterbatch LLC

- 6.4.18 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

片状成型市场规模、份额和成长分析(按纤维、类型、树脂类型、最终用户和地区划分)—2026-2033年产业预测

片状成型市场规模、份额和成长分析(按纤维、类型、树脂类型、最终用户和地区划分)—2026-2033年产业预测 BMC韧体市场(按平台、应用程式、部署模式、用途和最终用户)- 全球预测,2025 年至 2030 年

BMC韧体市场(按平台、应用程式、部署模式、用途和最终用户)- 全球预测,2025 年至 2030 年 片状模塑胶和块状模料市场规模、份额、趋势分析报告:按树脂类型、纤维类型、应用、地区、细分市场预测,2024-2030年

片状模塑胶和块状模料市场规模、份额、趋势分析报告:按树脂类型、纤维类型、应用、地区、细分市场预测,2024-2030年![片状模塑胶(SMC) 市场:趋势、机会与竞争分析 [2024-2030]](/sample/img/cover/42/default_cover_5.png) 片状模塑胶(SMC) 市场:趋势、机会与竞争分析 [2024-2030]

片状模塑胶(SMC) 市场:趋势、机会与竞争分析 [2024-2030] 亚太地区碳纤维 SMC BMC 市场预测至 2030 年 - 区域分析 - 按树脂类型和最终用途产业

亚太地区碳纤维 SMC BMC 市场预测至 2030 年 - 区域分析 - 按树脂类型和最终用途产业 北美碳纤维基 SMC BMC 市场预测至 2030 年 - 区域分析 - 按树脂类型和最终用途行业

北美碳纤维基 SMC BMC 市场预测至 2030 年 - 区域分析 - 按树脂类型和最终用途行业 欧洲碳纤维基 SMC BMC 市场预测至 2030 年 - 区域分析 - 按树脂类型(聚酯、乙烯基酯、环氧树脂等)和最终用途行业(汽车、航太、电气和电子、建筑和其他)

欧洲碳纤维基 SMC BMC 市场预测至 2030 年 - 区域分析 - 按树脂类型(聚酯、乙烯基酯、环氧树脂等)和最终用途行业(汽车、航太、电气和电子、建筑和其他) 全球片状模塑胶市场 - 全球产业分析、规模、份额、成长、趋势、预测 (2031) - 按产品、按技术、按等级、按应用、按最终用户、按地区

全球片状模塑胶市场 - 全球产业分析、规模、份额、成长、趋势、预测 (2031) - 按产品、按技术、按等级、按应用、按最终用户、按地区