|

市场调查报告书

商品编码

1846156

天门冬胺酸:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)Aspartic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

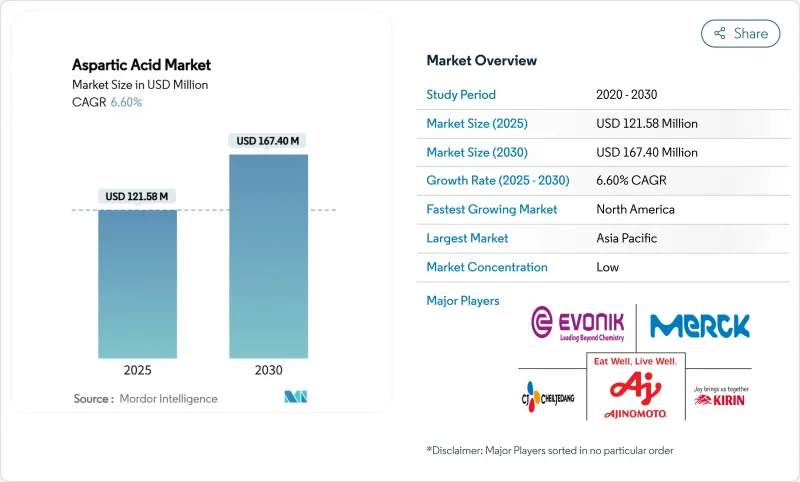

预计 2025 年天门冬胺酸市场价值将达到 1.2158 亿美元,到 2030 年将达到 1.674 亿美元,复合年增长率为 6.60%。

由于天门冬胺酸在多个产业中的重要应用,市场呈现持续成长。天门冬胺酸是食品和饮料製造中的关键成分,特别是在阿斯巴甜等人造甜味剂的生产中,它能够开发出符合消费者偏好的无糖和低热量产品。在製药领域,天门冬胺酸在药物和补充剂的配方中起着关键作用,支持治疗和营养需求。市场成长也受到其在永续工业过程中的应用的推动,例如可生物降解的聚合物和无磷清洁剂,符合当前的环境法规。对性能营养和膳食补充剂的不断增长的需求正在加强天冬胺酸在运动和健康产品中的使用。再加上生物发酵生产技术的改进,天门冬胺酸的应用范围正在扩大,使天门冬胺酸成为以健康为重点的永续解决方案中必不可少的成分。

全球天冬胺酸市场趋势与见解

亚洲清洁剂添加剂中天门冬胺酸的需求不断增长

天门冬胺酸市场正在经历显着成长,主要原因是亚洲越来越多地将天门冬胺酸加入清洁剂添加剂中。这种扩张从根本上是由不断变化的消费者偏好、严格的法律规范和整个全部区域持续的产品创新所决定的。在亚太地区,日益增强的环保意识极大地影响了消费者对环保洗衣精的购买模式。内务部的数据显示了这一趋势,该数据报告称,到 2023 年,日本家庭在洗衣精上的平均支出将达到 4,500 日圆。为了应对这一市场变化,清洁剂製造商正在策略性地重组产品系列,以包括可生物降解和无毒成分。天门冬胺酸衍生的聚合物已成为此类配方中的关键成分,具有环境永续性和作为水垢和岩盐抑制剂的优异性能的双重优势。亚洲市场向永续清洁剂添加剂的转变继续加强全球对天冬胺酸的需求,为市场建立了强劲的成长轨迹。

男性不孕症和运动营养领域对 D-天冬胺酸的需求不断增长

在人口趋势和市场创新的双重推动下,男性不孕症治疗和运动营养领域对 D-天冬胺酸 (DAA) 的需求不断增长,成为天门冬胺酸市场的主要成长要素。根据美国中央情报局 (CIA) 2024 年的数据,台湾和韩国的人均生育率分别为 1.11 和 1.12,为世界最低,凸显了东亚地区面临的巨大生育挑战。这种人口状况正在推动消费者和政府对生殖健康解决方案的兴趣日益浓厚。 D-天门冬胺酸在增强精子生成和活力方面的作用已得到科学检验,因此生育补充剂的使用率不断提高。各公司正在推出将 D-天门冬胺酸与辅助生育成分结合的新产品,以满足男性的生殖健康需求。这些补充剂的目标客户既有註重生育的消费者,也有运动营养用户,旨在提高精子品质、调节荷尔蒙和增强运动表现。人们对生育治疗和运动营养需求的兴趣的融合继续加强了 D-天冬胺酸的市场地位,显示天门冬胺酸市场具有持续成长的潜力。

长期服用D-天门冬胺酸补充剂的标籤规定更加严格

D-天门冬胺酸 (DAA) 补充剂标籤的监管要求影响产品配方、行销和消费者接受度,从而限制了天门冬胺酸市场。加拿大卫生署和食品药物管理局( FDA) 已对膳食补充剂实施了全面的标籤要求,包括警告、剂量限制和健康声明限制。 FDA 于 2025 年 2 月对阿斯巴甜的审查表明,对氨基酸补充剂及其健康声明的审查将更加严格。虽然这些法规保护了消费者,但它们也给高剂量或长期 D-天冬胺酸补充剂的製造商带来了挑战,因为合规成本增加并降低了市场潜力。像 D-天冬胺酸这样的新膳食成分需要对安全性和有效性进行科学检验,这进一步使产品核可复杂化和延迟。这些监管要求为产品开发、行销和消费者对 D-天门冬胺酸补充剂的信任设置了障碍,限制了市场扩张。

細項分析

到2024年,L-天门冬胺酸将以71.16%的市占率占据市场主导地位。这一重要的市场地位归功于其在多个行业中的关键作用。在食品领域,L-天门冬胺酸是合成阿斯巴甜(食品和饮料製造中常见的人工甜味剂)的关键原料,可满足人们对低热量、无糖产品日益增长的需求。该化合物也是药物配方中必不可少的成分,可作为药物和补充剂的成分,并可作为螯合剂用于生产工业清洁剂,以提高清洁性能。 L-天冬胺酸完善的生产基础设施和广泛的工业应用巩固了其市场地位。

D-天门冬胺酸是市场中成长最快的细分市场,预计2025年至2030年的复合年增长率为7.93%。这一增长得益于其在运动营养和生殖健康补充剂中的日益广泛的应用。该化合物因其有助于维持荷尔蒙平衡(尤其是睪固酮水平)而广受认可,使其成为运动员和健身爱好者运动营养产品的热门选择。其在男性生殖健康方面的作用也提升了其在生育补充剂中的份额。消费者对健身、运动表现和生殖健康日益增长的兴趣,以及支持D-天冬胺酸有效性的研究,正在推动特种健康和营养产品市场的扩张。

生物发酵已成为天门冬胺酸的主要生产方法,到 2024 年将占据 59.36% 的市场份额,并显示出巨大的成长潜力,到 2030 年的复合年增长率将达到 8.32%。这种市场主导地位归因于其营运成本效益、生产扩充性和环境永续性,使其特别有利于大规模工业应用。该方法使用特定的微生物将原材料转化为天冬胺酸,满足了市场对永续生产通讯协定日益增长的需求,同时最大限度地减少了对环境的影响。生物发酵过程在食品和饮料行业中获得了显着的关注,它是天冬氨酸大规模生产的重要组成部分,特别是对于阿斯巴甜等甜味剂应用而言,产量和品质稳定性至关重要。

化学合成在天门冬胺酸产业占有重要的市场影响,尤其是在需要快速生产、精确控制产量和稳定产品规格的应用中。该方法透过氨解和还原胺化等成熟製程将顺丁烯二酸酐或富马酸转化为产品,为製造商提供了可预测的成本结构和成熟的工业供应链网络。这种生产方法在石化基础设施发达或发酵原料取得受限的地区尤其有利。此外,化学合成有助于生产多种天冬胺酸变体,包括L-和D-天冬胺酸,从而满足日益增长的药品和营养保健品製造应用需求。

区域分析

亚太地区占天门冬胺酸市场的 43.76%,得益于製造业基础设施、原料供应以及终端使用领域不断增长的国内需求。中国透过政府和私营部门对氨基酸生产设施的投资,在生产能力方面处于该地区领先地位。根据美国农业部 (USDA) 谷物和饲料更新数据,中国玉米产量将在 2024/25 年度达到 2.949 亿吨,比上年度增加 2%。玉米产量的增加将增加发酵原料的供应,包括葡萄糖和淀粉衍生物,这些原料对于 L- 和 D-天冬胺酸的生物发酵生产至关重要。该地区透过由都市化、收入增加和健康偏好变化推动的综合生产到消费系统来保持其市场主导。

预计北美将见证最高的区域成长率,2025年至2030年的复合年增长率为8.91%。这一增长主要源于製药和营养保健品行业日益增长的需求,而天冬氨酸在这些领域对于氨基酸疗法、膳食补充剂和激素调节化合物至关重要。美国和加拿大在功能性成分的商业化方面表现出色,这得益于其强大的研发基础设施和支持创新的规范市场环境。该地区对运动营养、临床营养和洁净标示配方的关注,正在推动天门冬胺酸及其衍生物的先进应用。契约製造和生物技术公司的成长,正在推动产量的快速扩张,以应对新兴的健康趋势。

欧洲透过监管要求和永续性措施维持其市场地位。欧盟(EU)的磷酸盐禁令导致天门冬胺酸衍生物在清洁剂和水处理应用中的使用增加,作为磷酸盐螯合剂的替代品。该地区对可生物降解解决方案的推动,使得天门冬胺酸基聚合物在农业保水和养分输送系统中的应用增加。由于消费者偏好无糖替代品以及政府对环保材料的支持,英国市场具有成长潜力。欧洲製药业在药物配方中使用天门冬胺酸,这有助于该地区应用的多样化和市场稳定。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场驱动因素

- 亚洲清洁剂添加剂对天门冬胺酸的需求不断增加

- 男性不孕症运动营养对D-天门冬胺酸的需求不断增加

- 加大绿色氨基酸生产的补贴

- 可生物降解的聚天冬胺酸基高吸附剂在农业的应用日益广泛

- 欧盟磷酸盐禁令增加对天门冬胺酸螯合剂的需求

- 新兴国家的工业化和可支配所得的增加

- 市场限制

- 长期服用D-天门冬胺酸补充剂的标籤规定更加严格

- 高 pH 系统中天门冬胺酸基螯合剂的保存期限不稳定性。

- 在各种应用中与替代氨基酸和甜味剂的竞争

- 主要原物料价格波动影响生产成本与市场稳定

- 供应链分析

- 监理展望

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 依产品类型

- L-天门冬胺酸

- D-天门冬胺酸

- 依製造方法

- 生物发酵

- 化学合成

- 按纯度等级

- 食品级

- 医药级

- 工业级

- 按用途

- 饮食

- 营养补充品

- 製药

- 化妆品和个人护理

- 其他的

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 其他北美地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市场排名分析

- 公司简介

- Ajinomoto Co. Inc.

- Evonik Industries AG

- Kirin Holdings Company

- CJ CheilJedang Corp.

- Merck KGaA

- DIC Corporation

- Alpspure Lifesciences Private Limited

- Iris Biotech GmbH

- Fengchen Group Co.,Ltd

- AnaSpec Inc.

- Simson Pharma Limited

- Bio-Techne Corporation

- Alpha Chemika

- Zhangjiagang Huachang Pharmaceutical Co.,Ltd.

- CDH Fine Chemical

- Kishida Chemical Co.,Ltd. Manufacturer

- Tokyo Chemical Industry Co.

- Anmol Chemicals Pvt.Ltd

- Aditya Chemicals Limited

- AvansChem Speciality Chemicals

第七章 市场机会与未来展望

The Aspartic Acid market is valued at USD 121.58 million in 2025 and is expected to reach USD 167.40 million by 2030, registering a CAGR of 6.60%.

The market demonstrates consistent growth due to its essential applications across multiple industries. Aspartic Acid serves as a key component in food and beverage manufacturing, particularly in the production of artificial sweeteners like aspartame, which enables the development of sugar-free and low-calorie products aligned with consumer preferences. In pharmaceuticals, aspartic acid plays a vital role in medication and supplement formulations, supporting both therapeutic and nutritional needs. The market growth is also driven by its applications in sustainable industrial processes, including biodegradable polymers and phosphate-free detergents, which align with current environmental regulations. The increasing demand for performance nutrition and dietary supplements has enhanced aspartic acid usage in sports and wellness products. The expanding application range, coupled with improvements in bio-fermentation production techniques, establishes aspartic acid as an essential component in health-focused and sustainable solutions.

Global Aspartic Acid Market Trends and Insights

Increasing demand for Aspartic acid in Asian Detergent Additives

The aspartic acid market is experiencing substantial growth, primarily driven by its increasing incorporation in Asian detergent additives. This expansion is fundamentally shaped by evolving consumer preferences, stringent regulatory frameworks, and continuous product innovations across the region. In the Asia-Pacific region, heightened environmental awareness has significantly influenced consumer purchasing patterns toward eco-friendly laundry detergents. This trend is evidenced by data from the Ministry of Internal Affairs and Communications, which reported that Japanese households allocated an average of 4.5 thousand yen to laundry detergents in 2023 . In response to this market evolution, detergent manufacturers have strategically reformulated their product portfolios to include biodegradable and non-toxic components. Aspartic acid-derived polymers have emerged as a crucial ingredient in these formulations, offering dual benefits of environmental sustainability and superior performance as scale and halite inhibitors. This shift toward sustainable detergent additives in the Asian market continues to strengthen the global demand for aspartic acid, establishing a robust growth trajectory for the market.

Growing Demand for D-Aspartic Acid in Male-Fertility Sports Nutrition

The escalating demand for D-aspartic acid (DAA) in male fertility and sports nutrition is a key growth driver for the aspartic acid market, strongly supported by both demographic trends and market innovation. According to the Central Intelligence Agency (CIA) data for 2024, Taiwan and South Korea reported fertility rates of 1.11 and 1.12 children per woman, respectively, the lowest worldwide, highlighting a significant fertility challenge in East Asia. This demographic situation has intensified consumer and government attention on reproductive health solutions. The scientific validation of D-aspartic acid's role in enhancing sperm production and motility has increased its adoption in fertility supplements. Companies are introducing new products incorporating D-Aspartic Acid with complementary fertility-enhancing ingredients to address male reproductive health needs. These supplements target both fertility-focused consumers and sports nutrition users, marketed for their benefits in sperm quality improvement, hormonal regulation, and athletic performance enhancement. The convergence of fertility concerns and sports nutrition requirements continues to strengthen the market position of D-Aspartic Acid, indicating sustained growth potential in the aspartic acid market.

Stringent Labeling Rules on Long-Term D-Aspartate Supplementation

Regulatory requirements for D-aspartic acid (DAA) supplementation labeling constrain the aspartic acid market by affecting product formulation, marketing, and consumer acceptance. Health Canada and the Food and Drug Administration (FDA) enforce comprehensive labeling requirements for dietary supplements, including cautionary statements, dosage limits, and health claim restrictions. The Food and Drug Administration (FDA)'s February 2025 aspartame review indicates increased scrutiny of amino acid supplements and their health claims. While these regulations protect consumers, they create challenges for manufacturers of high-dose or long-term D-aspartic acid supplements through compliance costs and reduced market potential. The requirement for scientific validation of safety and efficacy for new dietary ingredients like D-aspartic acid further complicates and delays product approvals. These regulatory requirements limit market expansion by creating obstacles for product development, marketing, and consumer confidence in D-aspartic acid supplements.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Subsidies for Green Amino-Acid Manufacturing

- Increase in the Adoption of Biodegradable Polyaspartic Super-Absorbents in Agriculture

- Shelf-Life Instability of Aspartic-Based Chelators in High-pH Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

L-Aspartic Acid dominates the market with a 71.16% share in 2024. This significant market position stems from its essential role across multiple industries. In the food sector, L-Aspartic Acid is essential for aspartame synthesis, a common artificial sweetener in food and beverage manufacturing, meeting the increasing demand for low-calorie and sugar-free products. The compound is also vital in pharmaceutical formulations as a component for drugs and supplements, and in industrial detergent manufacturing as a chelating agent that improves cleaning performance. The established production infrastructure and broad industrial applications of L-Aspartic Acid strengthen its market position.

D-Aspartic Acid represents the market's fastest-growing segment, with a projected CAGR of 7.93% from 2025 to 2030. This growth results from its increased use in performance nutrition and reproductive health supplements. The compound has gained recognition for supporting hormonal balance, particularly testosterone levels, making it valuable in sports nutrition products for athletes and fitness enthusiasts. Its role in male reproductive health has also increased its presence in fertility supplements. The combination of growing consumer interest in fitness, athletic performance, and reproductive health, along with research supporting D-Aspartic Acid's effectiveness, drives its market expansion in specialized health and nutrition products.

Bio-fermentation has established itself as the predominant production methodology for aspartic acid, commanding 59.36% of the market share in 2024 and exhibiting substantial growth potential with an 8.32% CAGR through 2030. This market dominance is attributed to its operational cost-effectiveness, production scalability, and environmental sustainability characteristics, rendering it particularly advantageous for large-scale industrial applications. The methodology employs specific microorganisms for the conversion of raw materials into aspartic acid, consequently minimizing environmental impact while addressing increasing market requirements for sustainable manufacturing protocols. The bio-fermentation process has gained significant traction in the food and beverage industry, where it serves as an essential component in the large-scale production of aspartic acid, particularly for sweetener applications such as aspartame, where production volume and quality consistency are paramount considerations.

Chemical synthesis methodologies maintain a substantial market presence in the aspartic acid industry, particularly in applications necessitating expedited processing capabilities, precise yield control, and consistent product specifications. The methodology encompasses the transformation of maleic anhydride or fumaric acid through established processes of ammonolysis or reductive amination, providing manufacturers with predictable cost structures and well-established industrial supply chain networks. This production approach remains particularly viable in geographical regions characterized by developed petrochemical infrastructure or areas experiencing limitations in fermentation feedstock availability. Furthermore, chemical synthesis facilitates the production of multiple aspartic acid variants, including L-aspartic acid and D-aspartic acid, thereby addressing increasing demand requirements within pharmaceutical and nutraceutical manufacturing applications.

The Aspartic Acid Market is Segmented by Product Type (L-Aspartic Acid, and D-Aspartic Acid), by Production Method (Bio-Fermentation, and More), by Purity Grade (Food Grade, Pharmaceutical Grade, and More), by Application (Food and Beverages, Nutraceuticals and Dietary Supplements, and More), and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands 43.76% of the aspartic acid market, supported by its manufacturing infrastructure, feedstock availability, and increasing domestic demand across end-use sectors. China leads the regional production capacity through government and private sector investments in amino acid manufacturing facilities. The country's agricultural strength provides a significant advantage; the United States Department of Agriculture (USDA)'s Grain and Feed Update reports China's corn production reached 294.9 million metric tons in MY 2024/25, a 2% increase from the previous year . This corn production growth increases the availability of fermentation feedstocks, including glucose and starch derivatives, essential for L- and D-aspartic acid production through bio-fermentation. The region maintains its market leadership through an integrated production-to-consumption system, driven by urbanization, increasing incomes, and changing health preferences.

North America demonstrates the highest regional growth rate, with a projected CAGR of 8.91% from 2025 to 2030. This growth stems from increased demand in pharmaceutical and nutraceutical sectors, where aspartic acid is essential for amino acid therapies, dietary supplements, and hormone-regulating compounds. The United States and Canada excel in commercializing functional ingredients, backed by robust research and development infrastructure and a regulated market environment that supports innovation. The region's focus on sports nutrition, clinical nutrition, and clean-label formulations drives advanced applications of aspartic acid and its derivatives. The growth of contract manufacturers and biotechnology companies enables rapid production scaling to meet emerging health trends.

Europe maintains its market position through regulatory requirements and sustainability initiatives. The European Union's phosphate ban has increased the use of aspartic acid derivatives in detergents and water treatment applications as alternatives to phosphate-based chelating agents. The region's commitment to biodegradable solutions has increased the adoption of aspartic acid-based polymers in agricultural applications for water retention and nutrient delivery systems. The United Kingdom market demonstrates growth potential due to consumer preference for sugar-free alternatives and government support for environmentally friendly materials. Europe's pharmaceutical industry utilizes aspartic acid in drug formulations, contributing to the region's diverse application range and market stability.

- Ajinomoto Co. Inc.

- Evonik Industries AG

- Kirin Holdings Company

- CJ CheilJedang Corp.

- Merck KGaA

- DIC Corporation

- Alpspure Lifesciences Private Limited

- Iris Biotech GmbH

- Fengchen Group Co.,Ltd

- AnaSpec Inc.

- Simson Pharma Limited

- Bio-Techne Corporation

- Alpha Chemika

- Zhangjiagang Huachang Pharmaceutical Co.,Ltd.

- CDH Fine Chemical

- Kishida Chemical Co.,Ltd. Manufacturer

- Tokyo Chemical Industry Co.

- Anmol Chemicals Pvt.Ltd

- Aditya Chemicals Limited

- AvansChem Speciality Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Increasing demand for Aspartic acid in Asian Detergent Additives

- 4.1.2 Growing Demand for D-Aspartic Acid in Male-Fertility Sports Nutrition

- 4.1.3 Rise in Subsidies for Green Amino-Acid Manufacturing

- 4.1.4 Increase in the Adoption of Biodegradable Polyaspartic Super-Absorbents in Agriculture

- 4.1.5 Growing Demand for Aspartic-Based Chelating Agents owing to Phosphate Ban in EU

- 4.1.6 Increasing industrialization and disposable income in developing countries

- 4.2 Market Restraints

- 4.2.1 Stringent Labeling Rules on Long-Term D-Aspartate Supplementation

- 4.2.2 Shelf-Life Instability of Aspartic-Based Chelators in High-pH Systems

- 4.2.3 Competition from alternative amino acids and sweeteners in various applications

- 4.2.4 Price volatility of key raw materials impacts manufacturing costs and market stability

- 4.3 Supply-Chain Analysis

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 L-Aspartic Acid

- 5.1.2 D-Aspartic Acid

- 5.2 By Production Method

- 5.2.1 Bio-fermentation

- 5.2.2 Chemical Synthesis

- 5.3 By Purity Grade

- 5.3.1 Food Grade

- 5.3.2 Pharmaceutical Grade

- 5.3.3 Industrial Grade

- 5.4 By Application

- 5.4.1 Food and Beverages

- 5.4.2 Nutraceuticals and Dietary Supplements

- 5.4.3 Pharmaceuticals

- 5.4.4 Cosmetics and Personal Care

- 5.4.5 Others

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ajinomoto Co. Inc.

- 6.4.2 Evonik Industries AG

- 6.4.3 Kirin Holdings Company

- 6.4.4 CJ CheilJedang Corp.

- 6.4.5 Merck KGaA

- 6.4.6 DIC Corporation

- 6.4.7 Alpspure Lifesciences Private Limited

- 6.4.8 Iris Biotech GmbH

- 6.4.9 Fengchen Group Co.,Ltd

- 6.4.10 AnaSpec Inc.

- 6.4.11 Simson Pharma Limited

- 6.4.12 Bio-Techne Corporation

- 6.4.13 Alpha Chemika

- 6.4.14 Zhangjiagang Huachang Pharmaceutical Co.,Ltd.

- 6.4.15 CDH Fine Chemical

- 6.4.16 Kishida Chemical Co.,Ltd. Manufacturer

- 6.4.17 Tokyo Chemical Industry Co.

- 6.4.18 Anmol Chemicals Pvt.Ltd

- 6.4.19 Aditya Chemicals Limited

- 6.4.20 AvansChem Speciality Chemicals