|

市场调查报告书

商品编码

1846160

行动生物识别:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Mobile Biometrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

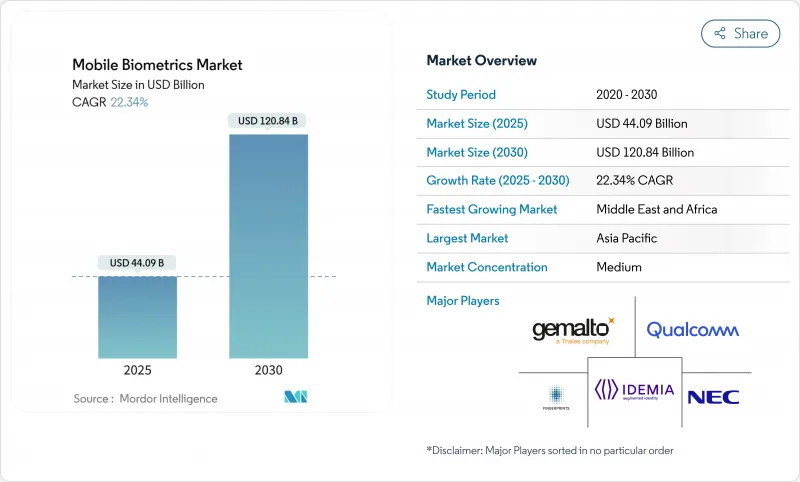

预计到 2025 年,行动生物识别市场规模将达到 440.9 亿美元,到 2030 年将扩大到 1,208.4 亿美元,复合年增长率高达 22.34%。

5G 连接、设备端人工智慧处理以及新兴经济体日益增长的数位身分要求共同推动了这一趋势。针对入门级安卓行动电话的攻击日益增多,使得持续的行为监控比静态检查更为重要。随着企业转向基于云端基础的生物辨识平台,组件发展趋势正朝着演进型服务方向转变。指纹感应器代表着日益成熟的核心技术,也是新型技术创新的前沿领域。儘管智慧型手机仍占据装置需求的主导地位,但智慧型穿戴装置正在引领潮流,预示着未来将转向环境、始终在线的身份验证环境。

全球移动生物识别市场趋势与洞察

印度UPI生态系中双模认证激增

印度的统一支付介面(UPI)允许使用指纹或脸部认证代替密码,从而减少诈欺并加快小额交易。这种模式已经影响东南亚各地的银行帐户供应商,并可能推动行动生物辨识技术在无银行帐户消费者中的普及。银行可以从降低扣回争议帐款成本中获益,但隐私监管机构仍在密切关注与Aadhaar(印度居民生物识别)关联的储存方式。

支援5G的终端AI提升了中国OEM智慧型手机的欺骗侦测能力

鑑于2024年生物辨识诈骗预计将激增40%,中国行动电话製造商已将本土人工智慧模型应用于手机,以侦测身分冒用。这种软硬体结合的策略提升了手机在全球竞争中的竞争力,巩固了其高端市场地位,同时也兼顾了电池续航力。

低成本安卓设备上的高演示攻击率

低价安卓设备通常缺乏有效的身份验证机制,导致伪造的声音和麵具在六次试验内就能有99%的机率绕过感应器。这个缺陷削弱了用户信任,迫使非洲银行增加实体身分证件审核,从而降低了它们在价格敏感型市场的规模。

细分市场分析

预计到2024年,硬体生物识别市场规模将达到265.3亿美元,占收益份额的60.2%。在产品日益同质化的背景下,感测器製造商已投资研发屏下超音波模组以维持利润率。人工智慧优化晶片可降低延迟,并确保在照度和手指潮湿等环境下的可用性。服务虽然规模较小,但正以23.3%的复合年增长率成长,这主要得益于银行和医院购买的识别服务订阅。服务提供者正在将编配仪錶板、诈欺风险分析和合规性报告等功能捆绑在一起,从而将资本支出转向营运支出。

託管服务的需求在医疗保健领域最为明显,医院纷纷将生物识别患者註册外包,以避免资料中心运作。主要的基础设施即服务 (IaaS) 供应商正在联合销售生物辨识 API 以扩大其业务范围,而整合指纹、语音和行为讯号的软体平台作为多重云端部署的指定整合商,正逐渐占据战略地位。这些因素共同作用,增强了服务飞轮效应,推动了整个行动生物识别市场年度经常性收益的成长。

单因子认证技术预计在2024年将创造314.7亿美元的收益,凸显了用户对iOS和Android原生内建的一键解锁流程的偏好。然而,监管机构和保险公司目前正敦促银行减少剩余的诈骗,并将新的预算项目用于部署多因素认证方案,该方案将生物识别与基于设备的加密金钥相结合。

透过将FIDO凭证快取在硬体隔离区中,Google可以允许使用人脸或指纹作为使用者不可见的第二重身份验证。企业无需放弃行动支付流程即可获得纵深防御。我们预计董事会层级的风险委员会将优先考虑分层控制措施,例如针对由生成式人工智慧技术武装的网路钓鱼套件包的防御措施。

区域分析

预计亚太地区2024年的营收将达到197.9亿美元,占全球收益的44.8%。智慧型手机的快速普及、金融科技应用的激增以及政府支持的数位身分识别项目将助力该地区继续保持领先地位。中国原始设备製造商(OEM)采用超音波屏下感测器已带动整个供应链,降低了零件成本,并推动了该技术的普及应用。印度的Aadhaar(印度居民身分识别系统)连动铁路计画正在稳步推进,而使用统一支付介面(UPI)的双模式交易正在将商家的服务范围扩展到大都会区以外的地区。

中东将成为成长最快的地区,到2024年市场规模将达到28.5亿美元,复合年增长率高达24.2%。阿联酋以行动认证取代实体身分证,是自上而下政策加速国家间互通性的例证。科威特的「2035愿景」将生物辨识註册与电子政府服务结合,推动了对多模态套件的需求。杜拜的基础设施建设热潮,包括计划交通项目,正促使承包商采用生物辨识门禁系统,进一步推动了该地区的支出成长。

北美保持稳定成长,但成长放缓,这主要得益于企业对其身分和存取管理 (IAM) 系统进行现代化改造,以及消费者银行业务转向无密码登入。摩根大通的生物辨识结帐试点计画预示着无卡零售支付即将迎来变革。欧洲在结构上仍然具有吸引力,但正努力应对 GDPR 和人工智慧法律的严格要求。欧盟数位身分钱包协调了 10 个国家的标准,加快了供应商认证流程。撒哈拉以南非洲地区的携带式选民登记套件销量虽小以金额为准呈成长趋势,凸显了对携带式登记硬体的潜在需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 印度统一支付介面(UPI)生态系中双模身份验证的激增

- 支援5G的终端AI提升了中国OEM智慧型手机的欺骗侦测能力

- 尼日利亚、巴西和印尼强制要求手机银行进行电子身份验证 (e-KYC)。

- 在撒哈拉以南非洲部署行动生物识别选民登记套件

- 欧洲的数位身分钱包法规加速了行动电话上生物识别护照的使用。

- 高阶市场OEM厂商转向采用屏下超音波感测器

- 市场限制

- 低成本安卓设备上的高演示攻击率

- 欧盟严格的数据主权法律限制了云端基础的语音生物辨识技术

- 持续行为认证带来的电池消耗问题

- 缺乏通用的行动生物识别性能基准

- 价值/供应链分析

- 监理展望

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场规模与成长预测

- 按组件

- 硬体

- 软体平台

- 透过服务

- 透过身份验证模式

- 单因素身份验证

- 多因素身份验证

- 按技术/模式

- 指纹认证

- 脸部认证

- 语音辨识

- 虹膜辨识

- 静脉和血管模式识别

- 行为生物特征(步态、击键)

- 其他方式

- 依设备类型

- 智慧型手机

- 药片

- 智慧型穿戴装置

- 物联网/边缘设备

- 坚固耐用的手持式扫描仪

- 按行业

- BFSI

- 政府机构

- 卫生保健

- 零售与电子商务

- 资讯科技/通讯

- 国防和安全

- 教育

- 其他行业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧的

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 纽西兰

- 其他亚太地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲国家

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Apple Inc.

- Samsung Electronics Co. Ltd.

- Qualcomm Technologies Inc.

- IDEMIA(Safran Identity and Security)

- NEC Corporation

- Thales Group(Gemalto)

- Fingerprint Cards AB

- Goodix Technology Co. Ltd.

- Synaptics Incorporated

- Precise Biometrics AB

- Nuance Communications Inc.

- Aware Inc.

- Daon Inc.

- M2SYS Technology

- Veridium Ltd.

- FaceTec Inc.

- Mobbeel Solutions SLL

- VoiceVault Inc.

- ValidSoft Ltd.

- Tech5 SA

- HYPR Corp.

- Suprema Inc.

- ID RandD Inc.

- ImageWare Systems Inc.

第七章 市场机会与未来展望

The mobile biometric market size is valued at USD 44.09 billion in 2025 and is forecast to expand to USD 120.84 billion by 2030, translating into a robust 22.34% CAGR.

Momentum stems from the convergence of 5G connectivity, on-device AI processing, and tighter digital-identity mandates across emerging economies. Continuous behavioral monitoring is gaining favor over static checks as presentation-attack attempts on entry-level Android phones escalate. Component trends is giving way to services that are advancing as organizations migrate toward cloud-based biometric platforms. Fingerprint sensors illustrating a maturing core and an innovation frontier in new modalities. Device demand is dominated by smartphones, but smart wearables are setting the pace, signaling a pivot toward ambient, always-on authentication environments.

Global Mobile Biometrics Market Trends and Insights

Bi-modal authentication surge in India's UPI ecosystem

India's Unified Payments Interface is enabling fingerprint or facial recognition in lieu of PINs, cutting fraud and speeding micro-transactions. The model is already influencing wallet providers across Southeast Asia and could lift mobile biometric market adoption among unbanked consumers. Banks benefit from reduced chargeback costs, yet privacy regulators continue to scrutinize Aadhaar-linked storage practices.

5G-enabled on-device AI improving spoof detection in Chinese OEM smartphones

Chinese handset makers have embedded AI models that detect deep-fake attempts locally, a timely response after a 40% jump in biometric fraud in 2024. The hardware-software bundle raises the bar for global competitors and underpins premium positioning while preserving battery life.

High presentation-attack rates on low-cost Android devices

Budget phones often lack robust liveness checks, allowing deep-fake audio or masks to bypass sensors 99% of the time in six attempts. The gap erodes user trust and forces banks in Africa to add physical ID reviews, dampening scale in price-sensitive segments.

Other drivers and restraints analyzed in the detailed report include:

- e-KYC mandates for mobile banking in Nigeria and Brazil

- European Digital Identity Wallet regulation accelerating biometric passports on phones

- Restrictive data-sovereignty laws limiting cloud voice biometrics in the EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The mobile biometric market size for hardware stood at USD 26.53 billion in 2024, equal to 60.2% revenue share. Sensor makers invested in under-display ultrasonic modules to defend margins as commoditization sets. AI-optimized chips compress latency, ensuring usability in low-light and wet-finger scenarios. Services, though smaller, are compounding at 23.3% CAGR on the back of identity-as-a-service subscriptions purchased by banks and hospitals. Providers bundle orchestration dashboards, fraud-risk analytics, and compliance reporting, shifting capital expense to operating outlays.

Demand for managed services is most pronounced in healthcare, where hospitals outsource biometric patient enrollment to avoid running data centers. Leading IaaS players co-market biometric APIs, broadening reach. Meanwhile, software platforms that unify fingerprint, voice, and behavioral signals hold strategic ground as integrators of record for multicloud deployments. Collectively, these forces reinforce a services flywheel that drives stickier annual recurring revenue across the mobile biometric market.

Single-factor techniques generated USD 31.47 billion in 2024, underscoring user preference for one-touch unlock flows embedded natively in iOS and Android. However, regulators and insurers now pressure banks to shrink residual fraud, steering new budget line items toward multi-factor deployments that mix biometrics with device-based cryptographic keys.

Android 15's passkey integration proves critical; by caching FIDO credentials in the hardware enclave, Google enables face or fingerprint to act as a second factor invisibly to users. Enterprises gain defense-in-depth without abandonment mobile checkout flows. Expect board-level risk committees to prioritize such layered controls as phishing kits that weaponize generative AI.

The Mobile Biometric Market Report is Segmented by Component (Hardware, Software Platforms, Services), Authentication Mode (Single-Factor Authentication, and More), Technology/Modality (Fingerprint Recognition, Facial Recognition, and More), Device Type (Smartphones, Tablets, and More), Industry Vertical (BFSI, Government and Public Sector, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated USD 19.79 billion in 2024, equating to 44.8% of global revenue. Rapid smartphone penetration, proliferating fintech apps, and government-backed digital ID programs sustain region-leading scale. Chinese OEMs' embrace of ultrasonic in-display sensors has rippled across supply chains, lowering BOM costs and seeding mass adoption. India continues to iterate on Aadhaar-linked rails, with bi-modal UPI transactions expanding merchant acceptance beyond metro centers.

The Middle East, at USD 2.85 billion in 2024, is the fastest-growing pocket with a 24.2% CAGR. UAE's replacement of physical Emirates IDs with mobile credentials exemplifies a top-down policy play that accelerates nationwide interoperability. Kuwait's Vision 2035 ties biometric enrollment to e-government service access, lifting demand for multimodal kits. Dubai's infrastructure boom, including transit megaprojects, compels contractors to adopt biometric access control, further lifting regional outlays.

North America maintains steady but slower growth as enterprises modernize IAM stacks and consumer banking shifts toward password-free sign-in. JPMorgan Chase's biometric checkout pilots hint at a coming inflection in card-less retail payments. Europe remains structurally attractive but navigates stringent GDPR and AI Act requirements. The EU Digital Identity Wallet harmonizes standards across 10 nations, catalyzing vendor certification pipelines. Sub-Saharan Africa, while smaller in dollar terms, drives volume in mobile voter-registration kits, underscoring latent demand for portable enrollment hardware.

- Apple Inc.

- Samsung Electronics Co. Ltd.

- Qualcomm Technologies Inc.

- IDEMIA (Safran Identity and Security)

- NEC Corporation

- Thales Group (Gemalto)

- Fingerprint Cards AB

- Goodix Technology Co. Ltd.

- Synaptics Incorporated

- Precise Biometrics AB

- Nuance Communications Inc.

- Aware Inc.

- Daon Inc.

- M2SYS Technology

- Veridium Ltd.

- FaceTec Inc.

- Mobbeel Solutions SLL

- VoiceVault Inc.

- ValidSoft Ltd.

- Tech5 SA

- HYPR Corp.

- Suprema Inc.

- ID RandD Inc.

- ImageWare Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Bi-modal authentication surge in India's Unified Payments Interface (UPI) ecosystem

- 4.2.2 5G-enabled on-device AI improving spoof detection in Chinese OEM smartphones

- 4.2.3 e-KYC mandates for mobile banking in Nigeria, Brazil and Indonesia

- 4.2.4 Deployment of mobile biometric voter enrolment kits across Sub-Saharan Africa

- 4.2.5 European Digital Identity Wallet regulation accelerating biometric passport use on phones

- 4.2.6 OEM shift toward under-display ultrasonic sensors in premium segment

- 4.3 Market Restraints

- 4.3.1 High presentation-attack rates on low-cost Android devices

- 4.3.2 Restrictive data-sovereignty laws limiting cloud-based voice biometrics in EU

- 4.3.3 Battery-drain concerns for continuous behavioral authentication

- 4.3.4 Absence of universal mobile biometric performance benchmarks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software Platforms

- 5.1.3 Services

- 5.2 By Authentication Mode

- 5.2.1 Single-Factor Authentication

- 5.2.2 Multi-Factor Authentication

- 5.3 By Technology / Modality

- 5.3.1 Fingerprint Recognition

- 5.3.2 Facial Recognition

- 5.3.3 Voice Recognition

- 5.3.4 Iris Recognition

- 5.3.5 Vein and Vascular Pattern Recognition

- 5.3.6 Behavioral Biometrics (Gait, Keystroke)

- 5.3.7 Other Modalities

- 5.4 By Device Type

- 5.4.1 Smartphones

- 5.4.2 Tablets

- 5.4.3 Smart Wearables

- 5.4.4 IoT / Edge Devices

- 5.4.5 Rugged Handhelds and Scanners

- 5.5 By Industry Vertical

- 5.5.1 BFSI

- 5.5.2 Government and Public Sector

- 5.5.3 Healthcare

- 5.5.4 Retail and E-commerce

- 5.5.5 IT and Telecom

- 5.5.6 Defense and Security

- 5.5.7 Education

- 5.5.8 Other Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co. Ltd.

- 6.4.3 Qualcomm Technologies Inc.

- 6.4.4 IDEMIA (Safran Identity and Security)

- 6.4.5 NEC Corporation

- 6.4.6 Thales Group (Gemalto)

- 6.4.7 Fingerprint Cards AB

- 6.4.8 Goodix Technology Co. Ltd.

- 6.4.9 Synaptics Incorporated

- 6.4.10 Precise Biometrics AB

- 6.4.11 Nuance Communications Inc.

- 6.4.12 Aware Inc.

- 6.4.13 Daon Inc.

- 6.4.14 M2SYS Technology

- 6.4.15 Veridium Ltd.

- 6.4.16 FaceTec Inc.

- 6.4.17 Mobbeel Solutions SLL

- 6.4.18 VoiceVault Inc.

- 6.4.19 ValidSoft Ltd.

- 6.4.20 Tech5 SA

- 6.4.21 HYPR Corp.

- 6.4.22 Suprema Inc.

- 6.4.23 ID RandD Inc.

- 6.4.24 ImageWare Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球行动生物辨识市场报告

2026年全球行动生物辨识市场报告 全球行动生物识别市场规模、份额、趋势和成长分析报告(2026-2034年)行动生物辨识市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)行动生物识别市场:未来预测(2025-2030)

全球行动生物识别市场规模、份额、趋势和成长分析报告(2026-2034年)行动生物辨识市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)行动生物识别市场:未来预测(2025-2030)