|

市场调查报告书

商品编码

1846217

无线对讲机:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Wireless Intercoms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

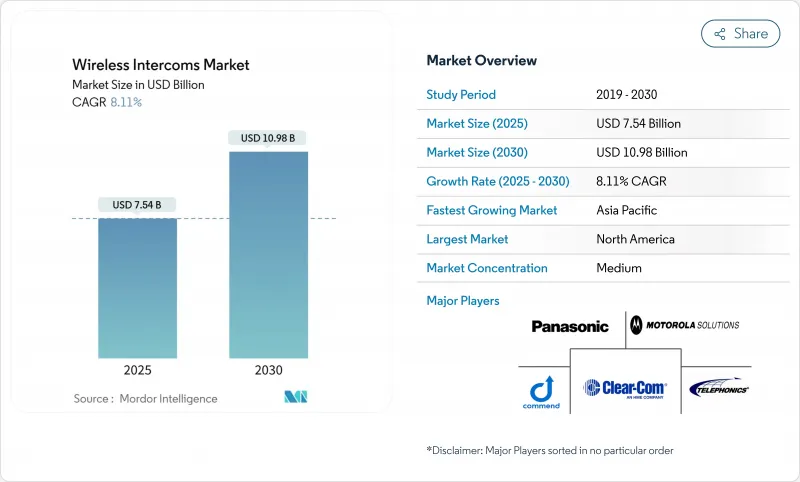

2025 年无线对讲机市场规模估计为 75.4 亿美元,预计到 2030 年将达到 109.8 亿美元,在预测期(2025-2030 年)内复合年增长率为 8.11%。

需求成长主要源自于有线音讯面板向支援IP的多模态系统的稳定过渡,这些系统能够透过同一网路骨干网路融合语音、影像和资料。关键成长要素包括楼宇基础设施的广泛数位化、Wi-Fi 6E和专用5G无线网路价格的下降,以及职业安全法规对免持通讯的标准化。随着云端原生参与企业将设备管理和分析功能与硬体捆绑在一起,提供具有终身价值的提案,市场竞争日益激烈,这尤其吸引那些没有内部IT资源的设施业主。此外,射频认证技术人员短缺的环境也倾向于选择可扩展的架构,以减少工具停机时间和安装工作。

全球无线对讲机市场趋势与洞察

对安全性和监控解决方案的需求日益增长

整合式对讲平台现在可将音讯串流直接传输到视讯分析主机,使控制室操作员能够将语音命令与视觉警报关联起来。在医院,Zenitel 的系统透过其内建语音引擎侦测到特定关键字,自动将紧急呼叫升级为保全人员呼叫,并锁定指定门禁,从而展现了这种融合。在大型机场,爱立信的专用 LTE 骨干网支援停机坪工作人员和塔台控制人员之间关键任务的对讲功能,从而减少滑行时间偏差并提高事件可追溯性。 2024 年高纯度石英短缺凸显了供应链的脆弱性,促使设施所有者倾向于使用模组化设备,因为无需重新认证整个阵列即可更换。语音、视讯和分析的紧密整合缩短了取证调查週期。其结果是,以安全为中心的资本投资与无线对讲系统的应用之间存在着密切联繫。

Wi-Fi/IP智慧家庭对讲机的兴起

房屋建筑商正越来越多地将音讯面板和门禁摄影机捆绑在同一Wi-Fi 6E网路上,从而简化低电压布线方案并缩短试运行时间。 CableLabs的一项研究证实,6 GHz频段缓解了以往高密度多用户住宅中因网路拥塞而导致的语音品质下降问题。 AiphoneCloud允许安装人员远端排除装置故障,从而降低上门服务成本,并使订阅模式对物业管理人员更具吸引力。 Stryker的Vocera徽章可与物业管理后端集成,使员工能够透过安全的语音提示接收清洁任务,而无需透过需要萤幕互动的行动应用程式通知。这些措施的累积效应是加快了传统模拟门禁系统的更新週期,从而增强了无线对讲机市场的需求。

射频干扰与频率拥塞

CableLabs 的多层模拟揭示了低延迟流量(例如对讲语音)的队头阻塞现象。共用频谱策略虽然能部分缓解问题,但会增加协调开销。日本的技术标准符合性认证要求每个无线电设备都必须通过 315 MHz、400 MHz、920 MHz 和 2.4 GHz频宽的单独测试,导致核准週期过长。美国国家频谱研发计画强调动态感知是解决之道,但大规模部署仍需数年时间。同时,供应商正在整合抗干扰天线,从而推高了组件成本。

细分市场分析

到2024年,安防监控将占无线对讲市场38%的份额,凸显了该技术在分层防御架构中的核心作用。机场、医院和资料中心强制升级门禁系统,使得语音认证成为生物识别扫描的有效补充,从而推动了该领域的发展。供应商透过整合降噪和人工智慧关键字辨识功能来提升产品差异化,这些功能无需人工干预即可发出警报。虽然活动管理绝对市场规模较小,但预计将以9.5%的复合年增长率成长,这主要得益于全双工网状无线技术的普及,该技术使演出总监能够即时调整灯光、烟火和广播链路。医疗保健产业也持续采用基于对讲的工作流程自动化。 Zenitel的涡轮单元与护理人员呼叫中间件集成,使医护人员能够在病患进入隔离病房前进行分诊,从而减少个人防护工具的使用。物流公司正在部署卡车称重对讲系统,并将其与称重软体配合使用,以减少车辆閒置时间并最大限度地减少司机与装卸平台的互动。

无线通讯在活动製作中的应用显而易见,许多多场馆合约都明确规定了在礼堂、体育场和临时场馆之间漫游的功能。饭店连锁企业倾向于使用隐藏的徽章式设备,这些设备可与物业管理软体对接,方便住宿无需使用会打扰客人的双向无线对讲机即可向工程部门发出信号。重工业场所需要本质安全型外壳和连接到同一通话路径的广域警报器,INDUSTRONIC 公司提案了「一个网路覆盖所有警报」的方案。教育机构则选择整合群发通知功能,以便透过单一的图形使用者介面同时发布封锁公告和对讲机控制指令。鑑于应用场景的多样性,多重通讯协定相容性已成为无线对讲机市场的必备功能。

无线对讲机市场报告按应用(安防监控、活动管理、酒店、交通物流、医疗保健等)、技术(Wi-Fi/IP、DECT 6.0、数位 UHF/VHF [MURS、FRS 等]、LTE/5G 蜂窝网路、Zigbee/蓝牙)、最终用户领域(住宅、商业、企业/公司园区、政府和公共地区进行细分和地区政府和地区进行细分。

区域分析

北美地区占2024年收入的36.2%,在严格的美国职业安全与健康管理局(OSHA)法规和成熟的室内覆盖基础设施的支持下,该地区有望率先采用私有5G对讲系统。主要係统整合商已签署长期维护合同,确保系统持续升级。在2025财年的采购中,机场优先考虑冗余呼叫路径,此前美国联邦航空管理局(FAA)的一次地面停飞事件凸显了语音可靠性方面的不足。国家频谱研发计画为动态共享实验提供了政策确定性,并鼓励供应商加强研发投入。

亚太地区将以10.9%的复合年增长率实现最快成长。中国的「讯号升级」计画将投入国家和私人资本,在12万个场所升级室内行动网路覆盖,并建造无线对讲机部署平台。印度通讯业在2024财年的市场规模达2.4兆印度卢比(约290亿美元),受益于监管品质评估工具,鼓励家庭用户安装高可用性连接,并提升对讲机的安装率。日本的合规性测试确保了低辐射设备,促使国内供应商采用干扰抑制滤波器,这将有利于出口。

节能型智慧建筑维修在欧洲将迎来强劲成长。 2030年实现碳中和的主导目标要求采用融合网络,以减少电缆重复建设。欧盟职业安全法规将全双工音讯列为高噪音区域的关键控制方法,从而刺激了对ATEX认证对讲机的需求。在南美洲以及中东和非洲地区,对讲机正被应用于交通设施升级改造,例如圣保罗和利雅得地铁在站台边缘和与旅游走廊相连的酒店扩建项目中都采用了IP音频系统。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对安全性和监控解决方案的需求日益增长

- 基于Wi-Fi/IP的智慧家庭对讲机的普及

- 智慧建筑与基础设施现代化浪潮

- 现场活动中全双工网状对讲系统的转变

- 工作场所安全法规要求使用免持通话

- 适用于临时工地的LTE/5G站点式系统

- 市场限制

- 射频干扰与频谱拥塞

- IP设备中的网路安全漏洞

- 熟练的射频-IT安装人员短缺

- 全球频谱许可证碎片化

- 价值/供应链分析

- 监管状况

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章 市场规模与成长预测

- 透过使用

- 安全与监控

- 活动管理

- 饭店业

- 运输/物流

- 卫生保健

- 工业和製造业

- 教育

- 其他的

- 按技术(连接性)

- Wi-Fi/IP

- DECT 6.0

- 数位超高频/甚高频(MURS、FRS 等)

- LTE/5G蜂窝网络

- Zigbee/Bluetooth

- 按最终用途面积

- 住房

- 商业设施

- 企业/企业园区

- 政府/公共

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 阿根廷

- 巴西

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 其他非洲国家

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Aiphone Co. Ltd

- Panasonic Corp.

- Clear-Com(HME)

- Motorola Solutions

- Zenitel NV

- Commend International GmbH

- RTS Intercom Systems(Bosch)

- Riedel Communications

- Sena Technologies

- Telephonics Corp.

- Axis Communications

- Dahua Technology

- Godrej Security Solutions

- Honeywell International

- Hytera Communications

- JVCKenwood Corp.

- 2N Telekomunikace(Axis)

- ButterflyMX

- DoorBird(Bird Home Automation)

- Alpha Communications

- Siedle and Sohne

- Akuvox

第七章 市场机会与未来展望

The Wireless Intercoms Market size is estimated at USD 7.54 billion in 2025, and is expected to reach USD 10.98 billion by 2030, at a CAGR of 8.11% during the forecast period (2025-2030).

Demand follows the steady shift from hard-wired voice panels to IP-enabled, multi-modal systems that blend audio, video, and data across the same network backbone. Widespread digitization of building infrastructure, improved affordability of Wi-Fi 6E and private 5G radios, and occupational-safety rules that formalize hands-free communication are the primary growth levers. Competitive intensity is rising as cloud-native entrants bundle device management and analytics with hardware, creating lifetime value propositions that appeal to facility owners who lack in-house IT resources. Procurement patterns also favor scalable architectures that limit tooling downtime, trimming installation labor in an environment where RF-certified technicians remain scarce.

Global Wireless Intercoms Market Trends and Insights

Expanding demand for security and surveillance solutions

Integrated intercom platforms now feed audio streams directly into video analytics consoles so control-room operators can correlate spoken commands with visual alerts. Hospitals illustrate this convergence as Zenitel systems automatically escalate a distress call to security staff and lock designated access doors when embedded speech engines detect specific keywords. At major airports, Ericsson's private LTE backbone supports mission-critical push-to-talk between tarmac crews and tower staff, reducing taxi-time deviations and improving incident traceability. High-purity quartz shortages during 2024 highlighted supply-chain fragility, prompting facility owners to favor modular devices that can be swapped without re-certifying the entire array. Tight pairing of voice, video, and analytics shortens forensic investigation cycles, a decisive benefit for operators facing budget scrutiny. The result is a firm linkage between security-centric capital expenditure and wireless intercom adoption.

Proliferation of Wi-Fi/IP-based smart-home intercoms

Residential builders increasingly bundle voice panels with door cameras on the same Wi-Fi 6E network, simplifying low-voltage wiring plans and cutting commissioning time. CableLabs research confirms that the 6 GHz band alleviates earlier congestion that degraded voice quality in dense apartment blocks. AiphoneCloud lets installers troubleshoot devices remotely, lowering truck-roll costs and making subscription models more attractive to property managers. Hotels echo this IP trend; Stryker's Vocera badge integrates with property-management back-ends, allowing staff to receive housekeeping tasks as secure voice prompts rather than mobile app notifications that require screen interaction. The cumulative effect is faster refresh cycles for legacy analog door stations, reinforcing demand nodes for the wireless intercoms market.

RF interference and spectrum congestion

Six-gigahertz Wi-Fi channels are nearing saturation in high-rise dwellings, a problem visualized in CableLabs multi-floor simulations that reveal head-of-line blocking for low-latency traffic such as intercom voice. Shared-spectrum policies offer partial relief but add coordination overhead. Japan's Technical Regulations Conformity Certification requires each wireless appliance to pass separate band tests at 315 MHz, 400 MHz, 920 MHz, and 2.4 GHz, lengthening approval cycles. The US National Spectrum R&D Plan stresses dynamic sensing as a remedy, but large-scale deployment remains years away. In the interim, vendors integrate interference-rejection antennas that raise the bill of materials.

Other drivers and restraints analyzed in the detailed report include:

- Smart-building and infrastructure modernization wave

- Shift to full-duplex mesh intercoms in live events

- Cyber-security vulnerabilities in IP devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security and surveillance accounted for 38% of the wireless intercoms market in 2024, underscoring the modality's central role in layered defense architectures. The segment benefits from mandatory access-control upgrades in airports, hospitals, and data centers, where voice verification now complements biometric scans. Suppliers differentiate by embedding noise cancellation and AI keyword spotting that escalate alerts without operator input. Event management, while smaller in absolute revenue, is forecast to post a 9.5% CAGR, propelled by full-duplex mesh radios that let show directors coordinate light cues, pyrotechnics, and broadcast links in real time. Healthcare keeps adopting intercom-driven workflow automation; Zenitel's turbine units integrate with nurse-call middleware so staff can triage before entering isolation wards, cutting personal-protective gear use. Logistics firms deploy truck-scale intercoms that pair with weigh-bridge software, slashing idle time and minimizing driver-dock interactions, a feature validated in Zenitel-B-TEK pilots.

Event production's embrace of wireless comms is visible in multi-venue contracts that specify roaming capability across auditoriums, stadiums, and temporary marquees. Hospitality chains gravitate toward discreet badge-style devices that mesh with property-management software, ensuring housekeeping can signal engineering without two-way radios that may disturb guests. Heavy-industry sites demand intrinsically safe housings and wide-area horns linked to the same talk paths, an offering INDUSTRONIC couches as a "one network, all alarms" proposition. Education campuses opt for mass-notification integration, enabling simultaneous lockdown announcements and intercom overrides from a single GUI. Collectively, application diversity cements multiprotocol compatibility as a must-have feature across the wireless intercoms market.

The Wireless Intercoms Market Report is Segmented by Application (Security and Surveillance, Event Management, Hospitality, Transportation and Logistics, Healthcare, and More), Technology (Wi-Fi/IP, DECT 6. 0, Digital UHF/VHF [MURS, FRS, Etc. ], LTE/5G Cellular, and Zigbee/Bluetooth), End-Use Sector (Residential, Commercial, Enterprise/Corporate Campuses, Government and Public Safety, and Others), and Geography.

Geography Analysis

North America generated 36.2% of 2024 revenue, buoyed by stringent OSHA mandates and mature indoor-coverage infrastructure that favors early adoption of private 5G intercoms. Large system integrators lock in long-term maintenance contracts, enabling sustained upgrade cycles. Fiscal 2025 procurement sees airports prioritizing redundant talk paths after FAA ground-stop incidents underscored voice resiliency gaps. The National Spectrum R&D Plan's backing for dynamic sharing experiments adds policy certainty that encourages vendor R&D spend.

Asia Pacific posts the fastest 10.9% CAGR. China's "Signal Upgrade" mission funnels state and private capital into indoor mobile coverage across 120,000 venues, creating a platform for wireless intercom rollouts. India's telecom sector, worth INR 2.4 trillion (USD 29.0 billion) in FY24, benefits from a regulatory quality-rating tool that prods landlords to install high-availability connectivity, lifting intercom attach rates. Japanese compliance testing ensures low emissions gear, spurring domestic suppliers to embed interference-mitigation filters that later become export advantages.

Europe registers steady growth on the back of energy-efficient smart-building retrofits. Directive-led targets for carbon neutrality by 2030 require converged networks that reduce cabling duplication. EU Worker Safety regulations classify full-duplex voice as a critical control measure in high-noise zones, energizing demand for ATEX-rated intercoms. South America and the Middle East & Africa see intercom adoption ride on transportation upgrades, metros in Sao Paulo and Riyadh specify IP voice along platform edges, and hospitality expansions linked to tourism corridors.

- Aiphone Co. Ltd

- Panasonic Corp.

- Clear-Com (HME)

- Motorola Solutions

- Zenitel NV

- Commend International GmbH

- RTS Intercom Systems (Bosch)

- Riedel Communications

- Sena Technologies

- Telephonics Corp.

- Axis Communications

- Dahua Technology

- Godrej Security Solutions

- Honeywell International

- Hytera Communications

- JVCKenwood Corp.

- 2N Telekomunikace (Axis)

- ButterflyMX

- DoorBird (Bird Home Automation)

- Alpha Communications

- Siedle and Sohne

- Akuvox

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding demand for security and surveillance solutions

- 4.2.2 Proliferation of Wi-Fi/IP-based smart-home intercoms

- 4.2.3 Smart-building and infrastructure modernization wave

- 4.2.4 Shift to full-duplex mesh intercoms in live events

- 4.2.5 Occupational-safety rules mandating hands-free comms

- 4.2.6 LTE/5G site-based systems for temporary job sites

- 4.3 Market Restraints

- 4.3.1 RF interference and spectrum congestion

- 4.3.2 Cyber-security vulnerabilities in IP devices

- 4.3.3 Shortage of RF-IT skilled installers

- 4.3.4 Global spectrum-licence fragmentation

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Security and Surveillance

- 5.1.2 Event Management

- 5.1.3 Hospitality

- 5.1.4 Transportation and Logistics

- 5.1.5 Healthcare

- 5.1.6 Industrial and Manufacturing

- 5.1.7 Education

- 5.1.8 Others

- 5.2 By Technology (Connectivity)

- 5.2.1 Wi-Fi/IP

- 5.2.2 DECT 6.0

- 5.2.3 Digital UHF/VHF (MURS, FRS, etc.)

- 5.2.4 LTE/5G Cellular

- 5.2.5 Zigbee/Bluetooth

- 5.3 By End-use Sector

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Enterprise/Corporate Campuses

- 5.3.4 Government and Public Safety

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Argentina

- 5.4.2.2 Brazil

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aiphone Co. Ltd

- 6.4.2 Panasonic Corp.

- 6.4.3 Clear-Com (HME)

- 6.4.4 Motorola Solutions

- 6.4.5 Zenitel NV

- 6.4.6 Commend International GmbH

- 6.4.7 RTS Intercom Systems (Bosch)

- 6.4.8 Riedel Communications

- 6.4.9 Sena Technologies

- 6.4.10 Telephonics Corp.

- 6.4.11 Axis Communications

- 6.4.12 Dahua Technology

- 6.4.13 Godrej Security Solutions

- 6.4.14 Honeywell International

- 6.4.15 Hytera Communications

- 6.4.16 JVCKenwood Corp.

- 6.4.17 2N Telekomunikace (Axis)

- 6.4.18 ButterflyMX

- 6.4.19 DoorBird (Bird Home Automation)

- 6.4.20 Alpha Communications

- 6.4.21 Siedle and Sohne

- 6.4.22 Akuvox

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment