|

市场调查报告书

商品编码

1910571

陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Ceramic Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

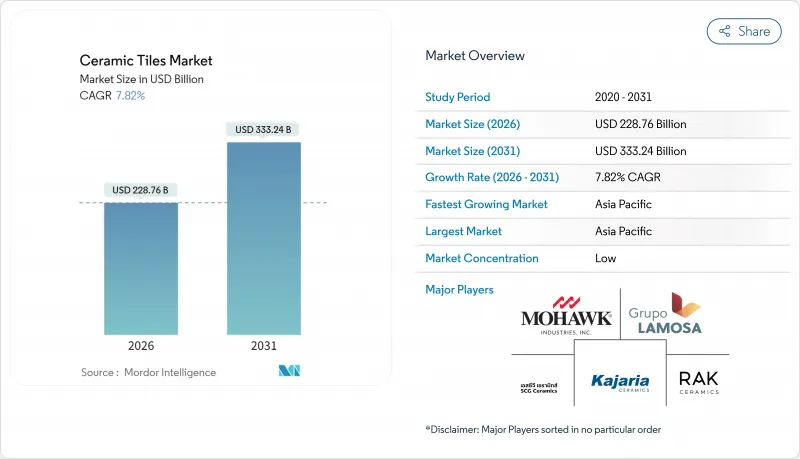

2025年陶瓷砖市场价值为2,121.7亿美元,预计从2026年的2,287.6亿美元成长到2031年的3,332.4亿美元,在预测期(2026-2031年)内复合年增长率为7.82%。

公共部门基础设施建设的持续投入、亚太地区快速的都市区化进程以及消费者对耐用、易清洁表面的偏好,都推动了这个市场的成长。美国新的政府支出计画以及印度和东南亚大都会区、机场和智慧城市的持续发展,扩大了地板材料和覆材产品的潜在需求基础。此外,将超逼真的石材、木材和金属效果印製到瓷体上的技术也推动了需求成长,使产品能够在不承受天然材料价格波动的情况下实现高端化。欧洲的环境法规正在加速低碳窑炉和废弃物材料混合物的应用,而线上零售通路则提高了全球产品的供应量和价格透明度。

全球陶瓷砖市场趋势与洞察

建筑和基础设施扩建

全球对交通走廊、能源工厂和综合用途设施的资本支出正推动陶瓷砖市场订单激增。在美国,联邦政府多年计画已拨款1.2兆美元用于道路、桥樑、半导体製造厂和清洁能源设施建设,从而持续刺激工厂和资料中心对高强度陶瓷瓷砖的需求。中国的「一带一路」倡议正在推动经济合作区内大量使用瓷砖的火车站和住宅,东南亚国协政府也在增加土木工程预算,优先考虑使用寿命长达30年的地板材料产品。骨材和水泥供应商的收入实现了两位数成长,显示陶瓷表面材料的下游消费强劲。

对美观耐用表面的需求

设计师们越来越追求视觉衝击力和性能之间的平衡,这推动了大尺寸瓷砖和仿大理石瓷砖的普及。喷墨印表机能够再现天然石材的纹理和金属光泽,同时减轻重量并实现色彩保真度。尺寸可达 1.8 公尺 x 3.6 公尺的大尺寸瓷砖减少了接缝,打造出无缝衔接的效果,这在开放式办公室和豪华住宅中备受青睐。快速釉面釉药缩短了生产週期,使得能够频繁推出反映时尚潮流的新款式。在厨房和地下室等对防潮性能要求极高的场所,瓷砖的市场份额正在超过实木地板。建筑师正在为电子组装车间指定防静电饰面,使功能性不仅限于装饰性。

高昂的建设和维修成本

许多已开发市场都面临着熟练瓷砖工短缺的问题,这推高了人事费用并延长了计划。大尺寸磁砖需要专用起重设备和环氧树脂接缝剂,与标准的60公分磁砖相比,安装预算会增加15%至25%。虽然住宅可以在週末自行安装浮动乙烯基复合地板,但瓷砖翻新则需要专业的防水和表面处理。儘管行业协会正在加强认证项目,但合格工人的供应量仍无法满足需求,这限制了近期的产量成长,尤其是在维修项目中。

细分市场分析

吸水率低于0.5%、耐冻、适用于户外广场和交通枢纽的陶瓷瓷砖,预计到2025年将占据陶瓷砖市场50.78%的份额。采用喷墨装饰技术的釉药瓷砖,预计到2031年将以8.34%的复合年增长率增长,超过釉药陶瓷和马赛克瓷砖。消费者认为其天然的色彩和耐磨等级(PEI IV级及以上)是其耐用性的有力证明,因此瓷砖在酒店大堂和机场等场所被广泛用作大理石的替代品。

该细分市场的强劲成长动能正推动着整个陶瓷砖市场的发展,製造商利用连续窑炉大规模生产大型建筑幕墙墙砖,在降低结构荷载的同时,维持了抗衝击性。马赛克瓷砖虽然仍属于小众市场,但在高端水疗中心等注重工艺美感的场所,其市场份额正在不断扩大,价格也相应上涨。抗菌铜釉药的创新应用正在拓展其在食品加工区和医院等领域的应用,这很好地诠释了产品多元化如何促进持续的收入成长。

到2025年,地板材料铺装将占陶瓷砖市场规模的48.10%,这主要得益于潮湿区域和人流量大的区域的强制性规范要求。防滑瓷质砖和工业用石板砖将主导商业厨房、仓库和交通枢纽等场所,从而确保稳定的市场销售。

到2031年,墙面应用将以8.17%的复合年增长率增长,这主要得益于建筑师对纹理和3D表面在特色墙、酒店接待区和零售背景墙等领域的应用。不断丰富的设计选择将推高平均售价,而易于清洁的釉药则符合酒店业的卫生标准。屋顶和外墙应用将集中在地中海和安第斯地区,这些地区重视陶瓷的保温性和抗冰雹性能;而檯面、泳池和一些小众应用领域也将推动整体需求成长。

陶瓷砖市场按产品类型(例如,陶瓷瓷砖、釉药)、应用领域(例如,地板材料、墙壁材料)、最终用户(住宅、商业、工业)、施工阶段(新建、维修/改造)、分销渠道(例如,独立零售商、大型五金建材超市)和地区进行细分。市场预测以以金额为准。

区域分析

预计到2025年,亚太地区将占全球营收的47.35%,并在2031年之前维持8.31%的年均成长率。这主要得益于大规模的城市住宅建设、都会区扩张以及出口导向生产群集的形成。中国内陆省份正在扩大靠近粘土矿床地区的产能,而印度则在推动智慧城市和经济适用住宅计划,并推荐使用地板材料。越南北部地区拥有100多家生产商,该国已从依赖进口釉药化学品转型,并计划在2024年实现釉药占80%、陶瓷瓷砖20%的生产结构。东协贸易协定促进了免税分销,并推动了区域整合供应链的发展。

北美是一个成熟但具有重要战略意义的地区,其本土製造商正在为未来的反倾销关税做好准备。儘管房屋抵押贷款利率上升导緻美国瓷砖消费量在2024年降至2.645亿平方公尺,但联邦政府对半导体和电池工厂的投入支撑了长期需求。莫霍克工业公司(Mohawk Industries)正利用其在田纳西州和德克萨斯州的垂直整合窑炉来缩短前置作业时间并确保公共计划符合规范。在加拿大,大量资金正投入医院和交通设施的维修中,并日益强制要求使用低碳材料。同时,墨西哥的拉莫萨集团(Grupo Lamosa)正在拉丁美洲各地扩建工厂,以分散其货币风险。儘管受能源价格上涨的影响,欧洲瓷砖机械出口量在2023年下降了18%,但仍占全球瓷砖机械出口量的50%(assopiastrelle.it)。义大利的闭合迴路工厂可100%回收烧製前的废料,展现了其在环保领域的领先地位。西班牙正推进氢窑试点项目,以实现欧盟的净零排放目标;同时,波兰的黏土短缺导致进口量增加,现货价格波动。在中东和非洲地区,埃及正利用低成本的页岩资源,每年生产2亿平方公尺。阿联酋的拉斯海马地区拥有4万家註册工业企业,推动了相关表面处理流程的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩大建筑和基础设施开发

- 市场对美观耐用的地板材料解决方案的需求日益增长

- 消费者越来越偏好环保和永续产品。

- 製造技术的进步

- 可支配所得增加和生活方式改变

- 日益老化的建筑基础设施和不断增长的维修需求

- 市场限制

- 安装和维护成本高昂

- 脆性和开裂风险

- 原物料价格波动

- 製造业的环境问题

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 陶瓷瓷砖

- 釉药磁砖

- 无釉瓷砖

- 马赛克瓷砖

- 其他的

- 透过使用

- 地面

- 墙

- 屋顶工程

- 其他的

- 最终用户

- 住宅

- 商业的

- 产业

- 依建筑类型

- 新房产

- 维修和更换

- 透过分销管道

- 独立零售商

- 大型家居建材商店

- 线上零售

- 直接向承包商销售

- 按地区

- 北美洲

- 加拿大

- 美国

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 其他南美洲

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚(新加坡、马来西亚、泰国、印尼、越南、菲律宾)

- 亚太其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mohawk Industries

- Grupo Lamosa

- SCG Ceramics Public Co. Ltd.

- Kajaria Ceramics Ltd.

- RAK Ceramics

- Pamesa Grupo Empresarial

- Guangdong Newpearl Ceramics

- Johnson Tiles

- Ceramic Industries Ltd.

- Porcelanosa Grupo

- Centura Tile

- Interceramic

- Florida Tile

- Villeroy & Boch

- Crossville Inc.

- Marazzi Group

- Iris Ceramica Group

- Noritake Co., Inc.

- Somany Ceramics

- Emser Tile*

第七章 市场机会与未来展望

The ceramic tiles market was valued at USD 212.17 billion in 2025 and estimated to grow from USD 228.76 billion in 2026 to reach USD 333.24 billion by 2031, at a CAGR of 7.82% during the forecast period (2026-2031).

Steady public-sector infrastructure outlays, rapid urban migration in Asia-Pacific, and consumers' preference for durable, easy-to-clean surfaces anchor this expansion. New government spending packages in the United States and ongoing metro, airport, and smart-city developments in India and Southeast Asia are enlarging the addressable base for flooring and cladding products. Demand also benefits from technology that prints hyper-realistic stone, wood, and metallic effects on porcelain bodies, enabling premiumization without the price volatility of natural materials. Environmental regulations in Europe accelerate the rollout of low-carbon kilns and waste-based raw mixes, while online retail channels broaden product availability and price transparency worldwide.

Global Ceramic Tiles Market Trends and Insights

Construction and infrastructure expansion

Global capital spending on transport corridors, energy plants, and mixed-use complexes is stimulating large-volume orders for the ceramic tiles market. In the United States, multiyear federal programmed collectively allocate USD 1.2 trillion to roads, bridges, semiconductor fabs, and clean-energy facilities, generating sustained demand for heavy-duty porcelain specified in factories and data centers. China's Belt and Road Initiative drives tile-intensive rail stations and housing in partner economies, while ASEAN governments raise civil works budgets that favor flooring products with 30-year service lives. Suppliers of aggregates and cement report double-digit revenue growth, signaling robust downstream consumption of ceramic surfacing.

Demand for aesthetic, durable surfaces

Designers increasingly combine visual impact with performance, fuelling the uptake of large-format planks and marble-look slabs. Inkjet printers replicate veining and metallic highlights that rival quarried stone, but at lower weight and in repeatable colourways. Format growth-porcelain boards up to 1.8 m by 3.6 m-reduces grout lines and conveys seamless continuity valued in open-plan offices and luxury residences. Quick-fire glazes cut production cycles, enabling frequent style introductions that mirror fashion trends. The ceramic tiles market also gains share versus hardwood in kitchens and basements where moisture resistance is critical. Architects specify anti-static finishes for electronics assembly floors, widening functional appeal beyond decor.

High installation and maintenance costs

Skilled tile setters remain scarce in many developed markets, lifting labour rates and extending project timelines. Large-format porcelain slabs need specialised lifting rigs and epoxy grouts, adding 15-25% to installation budgets versus standard 60 cm products. Where homeowners can install floating vinyl planks themselves over a weekend, ceramic renovations require professional waterproofing and sub-floor preparation. Industry associations have stepped up certification schemes, yet supply of certified crews lags demand, tempering short-run volume growth, especially in refurbishments.

Other drivers and restraints analyzed in the detailed report include:

- Preference for eco-friendly products

- Manufacturing technology advances

- Raw material price volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Porcelain tiles secured 50.78% of the ceramic tiles market share in 2025 owing to water-absorption rates below 0.5% and frost resistance that suits outdoor plazas and transit hubs. Glazed porcelain, aided by inkjet decoration, is projected to register an 8.34% CAGR through 2031, outpacing glazed ceramic and mosaic formats. Consumers perceive its colour-through body and abrasion class >= PEI IV as proof of longevity, encouraging substitution for marble in hotel lobbies and airports.

The segment's momentum lifts the overall ceramic tiles market as manufacturers leverage continuous kilns to mass-produce large thin slabs for facades, reducing structural load yet retaining impact strength. Mosaic tiles, though niche, capture share in luxury spas were artisanal aesthetics command price premiums. Copper-glaze innovations offering antimicrobial action broaden use in food-handling zones and hospitals, illustrating how product diversification underpins sustained revenue growth.

Floor installations represented 48.10% of the ceramic tiles market size in 2025 driven by mandatory specification in wet areas and heavy-traffic corridors. Slip-resistant porcelain and industrial-grade quarry tiles dominate commercial kitchens, warehouses, and transit stations, ensuring baseline volume stability.

Wall applications, posting an 8.17% CAGR to 2031, flourish as architects deploy textured and 3D surfaces for feature walls, hotel receptions, and retail backdrops. Expanded design palettes increase average selling prices, and easy-clean glazes meet hospitality hygiene codes. Roof and facade uses remain concentrated in Mediterranean and Andean regions where ceramic's thermal mass and hail resistance are valued, while countertop, pool, and niche applications collectively extend total addressable demand.

The Ceramic Tiles Market Segments Into by Product Type (Porcelain Tiles, Glazed Ceramic Tiles, and More), by Application (Floor, Wall, and More), by End-User (Residential, Commercial, Industrial), by Construction (New Construction, Replacement and Renovation), by Distribution Channel (Independent Retailers, Large Home Centers and More), by Geography. The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

Asia-Pacific accounted for 47.35% of global revenue in 2025 and is forecast to compound to 8.31% annually through 2031, anchored by mass urban housing, metro extensions, and export-oriented production clusters. China's inland provinces add capacity close to clay deposits, while India scales smart-city and affordable-housing schemes that stipulate vitrified flooring. Vietnam's 100-plus manufacturers, concentrated in the north, rely on imported chemicals for glazes but still achieved a combined output mix of 80% glazed and 20% porcelain tiles in 2024. ASEAN trade agreements allow duty-free flows, favouring regionally integrated supply chains.

North America presents a mature but strategically important arena where domestic producers hedge against future antidumping duties. US tile consumption eased to 264.5 million m2 in 2024 amid high mortgage rates, yet federal outlays on semiconductor and battery plants underpin long-term volume. Mohawk Industries leverages vertically integrated Tennessee and Texas kilns to shorten lead times and secure public-project specifications. Canada funds hospital and transit refurbishments that increasingly stipulate low-carbon materials, while Mexico's Grupo Lamosa operates plants across Latin America to diversify currency exposure. Europe, while posting an 18% output drop in 2023 due to energy spikes, still accounts for 50% of global tile-machinery exports assopiastrelle.it. Italy's closed-loop plants recycle 100% of unfired scrap, showcasing environmental leadership. Spain advances hydrogen-kiln pilots to meet EU Net-Zero targets, while Poland's clay shortages force higher imports and spot-price volatility. In the Middle East and Africa, Egypt produces 200 million m2 annually using low-cost shale resources, and the UAE's Ras Al Khaimah cluster hosts 40,000 industrial registrants, fuelling related surface-finishing demand.

- Mohawk Industries

- Grupo Lamosa

- SCG Ceramics Public Co. Ltd.

- Kajaria Ceramics Ltd.

- RAK Ceramics

- Pamesa Grupo Empresarial

- Guangdong Newpearl Ceramics

- Johnson Tiles

- Ceramic Industries Ltd.

- Porcelanosa Grupo

- Centura Tile

- Interceramic

- Florida Tile

- Villeroy & Boch

- Crossville Inc.

- Marazzi Group

- Iris Ceramica Group

- Noritake Co., Inc.

- Somany Ceramics

- Emser Tile*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Construction and Infrastructure Development

- 4.2.2 Increasing Demand for Aesthetic and Durable Flooring Solutions

- 4.2.3 Growing Preference for Eco-Friendly and Sustainable Products

- 4.2.4 Advancements in Manufacturing Technology

- 4.2.5 Rising Disposable Income and Changing Lifestyle

- 4.2.6 Increasing Ageing Building Infrastructure and Demand for Renovation Activities

- 4.3 Market Restraints

- 4.3.1 High Installation and Maintenance Costs

- 4.3.2 Fragility and Risk of Cracking

- 4.3.3 Raw Material Price Volatility

- 4.3.4 Environmental Concerns in Manufacturing

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Porcelain Tiles

- 5.1.2 Glazed Ceramic Tiles

- 5.1.3 Unglazed Ceramic Tiles

- 5.1.4 Mosaic Tiles

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Floor

- 5.2.2 Wall

- 5.2.3 Roofing

- 5.2.4 Others

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Renovation and Replacement

- 5.5 By Distribution Channel

- 5.5.1 Independent Retailers

- 5.5.2 Large Home Centers

- 5.5.3 Online Retail

- 5.5.4 Direct Sales to Contractors

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 India

- 5.6.3.2 China

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.6.3.7 Rest of Asia Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Grupo Lamosa

- 6.4.3 SCG Ceramics Public Co. Ltd.

- 6.4.4 Kajaria Ceramics Ltd.

- 6.4.5 RAK Ceramics

- 6.4.6 Pamesa Grupo Empresarial

- 6.4.7 Guangdong Newpearl Ceramics

- 6.4.8 Johnson Tiles

- 6.4.9 Ceramic Industries Ltd.

- 6.4.10 Porcelanosa Grupo

- 6.4.11 Centura Tile

- 6.4.12 Interceramic

- 6.4.13 Florida Tile

- 6.4.14 Villeroy & Boch

- 6.4.15 Crossville Inc.

- 6.4.16 Marazzi Group

- 6.4.17 Iris Ceramica Group

- 6.4.18 Noritake Co., Inc.

- 6.4.19 Somany Ceramics

- 6.4.20 Emser Tile*

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球陶瓷砖市场:机会与策略展望(至2034年)

全球陶瓷砖市场:机会与策略展望(至2034年) 陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分

陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分 美国陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031)

美国陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031) 日本水泥瓦市场:规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年印尼陶瓷砖市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲瓷砖市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)菲律宾瓷砖市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚瓷砖:市场份额分析、行业趋势与统计、成长预测(2026-2031)

日本水泥瓦市场:规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年印尼陶瓷砖市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲瓷砖市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)菲律宾瓷砖市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚瓷砖:市场份额分析、行业趋势与统计、成长预测(2026-2031) 陶瓷砖市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测(2026-2033 年)

陶瓷砖市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测(2026-2033 年)