|

市场调查报告书

商品编码

1848059

联网汽车设备:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Connected Car Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

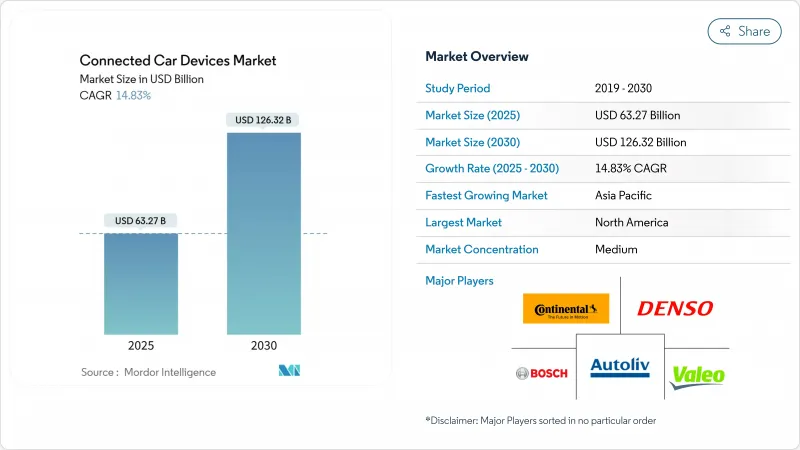

预计到 2025 年,联网汽车设备市场规模将达到 632.7 亿美元,到 2030 年将达到 1,263.2 亿美元,预测期(2025-2030 年)复合年增长率为 14.83%。

需求成长主要受5G快速部署、新的紧急呼叫(e-Call)和高级驾驶辅助系统(ADAS)强制要求以及向依赖无缝连接的软体定义车辆转型所驱动。原始设备製造商(OEM)将嵌入式模组视为订阅服务和数据货币化的基石,预计连网服务带来的单车收入将达到1,600美元。蜂窝车联网(C-V2X)标准的广泛应用以及能够降低安全关键功能延迟的边缘人工智慧晶片组也推动了市场成长。

全球联网汽车设备市场趋势与洞察

快速部署 5G 和通讯业者-OEM 合作伙伴关係

预计到2027年,5G汽车连接将推动相关业务收入呈指数级成长。思科和TELUS已为超过150万辆5G汽车提供自动化平台,将延迟降低至接近即时水平,这对于自动驾驶功能至关重要。伙伴关係将连接、边缘运算和开发者工具整合到整合产品中,使OEM厂商能够更快地推出新服务。这些联盟对供应商而言意义重大,因为通讯业者正在从频宽远距离诊断和高清地图,从而提高每位用户平均收入。

E-Call 和 ADAS 法规成为强制规定

美国国家公路交通安全管理局(NHTSA)强制要求所有轻型车辆在2029年9月前配备行人侦测的自动紧急煞车系统,预计每年遵循成本将达3.54亿美元,终身收益将达58.2亿美元。欧洲正在根据通用安全法规实施e-Call紧急呼叫系统和一系列驾驶辅助功能,而中国则在北京部署了超过7000个5G-A基地台,扩大车路云试点计画。这些强制性规定消除了时间表的不确定性,并鼓励汽车製造商将连网感测器作为标准配置。供应商受益于可预测的产量,而消费者则获得了有助于降低事故率的通用安全功能。

网路安全漏洞与召回

Pwn2Own Automotive 2024 竞赛揭露了 Alpine Halo9 资讯娱乐系统中一个零点漏洞,成功率高达 96%,凸显了远端入侵的便利性。 2023 年,软体相关的召回事件将影响超过 3000 万辆汽车,而 NIST 列出的漏洞 CVE-2023-6248 允许攻击者完全控制一个常见的车载资讯服务闸道。随着汽车逐渐成为行动资料中心,其攻击面不断扩大,售后修补程式的成本和声誉损失也随之增加。监管机构要求从设计之初就注重安全性,促使供应商采用硬体信任根、安全无线电框架和持续渗透测试等措施。

细分市场分析

到2024年,随着工厂硬体与车辆诊断、电源管理和保固系统的深度集成,OEM集成将占据联网汽车设备市场63.27%的份额。汽车製造商在组装过程中整合模组,以确保符合e-Call和ADAS的要求,简化空中升级流程,并增强品牌对资料的控制。对软体定义架构的日益依赖正在巩固OEM在该管道的领先地位,因为他们将互联功能与远端功能启动和预测性维护等创收服务联繫起来。

然而,随着保险公司和车队管理公司对老旧车辆维修,售后市场供应商正以15.74%的复合年增长率快速扩张。即插即用的加密狗和硬布线黑盒子可提供即时使用数据,从而支援行为模式的保险费率和资产追踪。哈曼的Ready Upgrade 套件就是一个专为混合车队量身定制的解决方案,它兼具快速安装和跨品牌兼容性。儘管原始设备製造商(OEM)仍然占据主导地位,但注重价格的车主和商业营运商也在共同推动售后市场的发展,确保了联网汽车设备市场的竞争多样性。

车对车(V2V)互联技术无需路边装置即可提供碰撞预警,预计2024年将占据联网汽车设备市场39.62%的收入份额。成熟的标准和已被证实的安全性提升促使汽车製造商优先采用V2V技术,尤其是在旨在获得五星级安全评级的量产车型中。此外,商用车也越来越倾向于加装V2V技术,因为前向碰撞预警可以减少停机时间和保险成本。

预计到2030年,随着能源公司与汽车製造商合作以稳定以可再生的电网,车网互动(V2G)能力将以15.12%的复合年增长率成长。双向充电器结合互联功能,使电动车能够将储存的能量输回电网,从而为车主和电网营运商开闢新的收入来源。车路互动(V2I)和车行互动(V2P)领域的成长与智慧城市建设的投入密切相关,但依赖更广泛的公共投资。整合式V2X系统最终将融合所有模式,但随着生态系统的成熟,V2V仍将是基石。

区域分析

2024年,北美占据了联网汽车设备市场38.73%的份额。联邦政府根据《基础设施投资与就业法案》提供的资金支持,以及消费者对配备高级驾驶辅助系统(ADAS)、高清资讯娱乐系统和5G热点的豪华SUV的偏好,正在推动连网汽车的普及。美国运输部与5G汽车协会正在进行的试验增强了人们对车联网(C-V2X)技术的信心,而严格的网路安全和隐私法规正在影响采购规范。加拿大和墨西哥受益于一体化的供应链,使得区域内的原始设备製造商(OEM)工厂能够对联网模组和售后服务堆迭进行标准化。这些因素维持了北美地区健康的更换週期和售后服务合约。

亚太地区预计在2030年前以15.37%的复合年增长率实现最快成长。中国的车路云一体化发展蓝图正在推动公共和私人领域的投资,仅在北京就已部署超过7000个5G-A基地台,用于智慧出行。国内品牌正透过嵌入互联功能在竞争激烈的电动车市场中脱颖而出,而区域供应商则为摩托车和微型车提供成本优化的车载资讯服务。日本和韩国正利用其晶片製造能力和早期5G部署,测试下一代C-V2X侧链功能。在印度,日益严格的安全标准和智慧型手机普及率高、对全天候资讯娱乐系统需求旺盛的人群,将创造大规模生产的机会。

欧洲在强制性紧急呼叫系统(e-Call)和通用安全法规等统一法规的推动下,保持着稳定发展的势头。德国、英国和法国引领这一趋势,豪华品牌纷纷将互联功能整合到高阶车型中,中阶品牌也紧跟着。能源效率和碳减排目标推动了Vehicle-to-Grid)试点计画的发展,该计画将电动车充电与可再生能源发电相结合。严格的资料主权法律正在影响云端託管的选择,使欧洲供应商更具优势。一项泛欧盟网路安全认证标准正在製定中,预计将简化跨境认证流程,并进一步刺激连网汽车设备市场的发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 5G的快速普及以及营运商与OEM厂商之间的伙伴关係

- 美国、欧盟和中国强制执行紧急呼叫和高阶驾驶辅助系统(ADAS)法规

- OEM厂商基于订阅的收入目标

- 边缘人工智慧晶片支援车载推理

- 基于使用量的保险线索售后市场远端资讯处理

- 跨产业应用商店生态系统

- 市场限制

- 网路安全漏洞与召回

- 多频段V2X模组的物料清单成本较高

- 资料云退出费用会降低OEM服务利润率

- 半导体供应链中的脆弱性

- 价值/供应链分析

- 监管状态

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争的激烈程度

第五章 市场规模与成长预测

- 最终用户

- OEM

- 售后市场

- 依通讯类型

- V2V

- V2I

- V2P

- V2N

- V2G

- 依产品类型

- 驾驶辅助系统(ADAS)

- 车载资讯系统

- 车载资讯娱乐系统

- 网路安全硬体

- 透过连接技术

- 嵌入式

- 融合的

- 繫绳

- DSRC

- C-V2X(4G/5G)

- 按车辆推进类型

- 内燃机车辆

- 电动车

- 电池电动车

- 油电混合车

- 燃料电池电动车

- 插电式混合动力电动车

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- ZF Friedrichshafen AG

- Harman International

- Valeo SA

- Magna International

- Panasonic Corp.

- Visteon Corp.

- Autoliv Inc.

- Infineon Technologies AG

- Autotalks Ltd.

- Qualcomm Inc.

- NXP Semiconductors

- NVIDIA Corp.

- Sierra Wireless

- Cisco Systems

- Huawei Technologies

- AT&T

- Verizon

- Vodafone Group

- Ericsson

- LG Electronics

- Telit

第七章 市场机会与未来展望

The Connected Car Devices Market size is estimated at USD 63.27 billion in 2025, and is expected to reach USD 126.32 billion by 2030, at a CAGR of 14.83% during the forecast period (2025-2030).

Demand stems from rapid 5G roll-outs, new e-Call and ADAS mandates, and the shift toward software-defined vehicles that rely on seamless connectivity. OEMs view embedded modules as the backbone for subscription services and data monetization, with potential revenue of USD 1,600 per vehicle from connected offerings. Growth is bolstered by the spread of cellular vehicle-to-everything (C-V2X) standards and edge AI chipsets that lower latency for safety-critical functions.

Global Connected Car Devices Market Trends and Insights

Rapid 5G Roll-Out and Carrier-OEM Partnerships

Automotive 5G connections are forecast to grow exponentially in enablement revenues by 2027. Cisco and TELUS already provision more than 1.5 million 5G vehicles on automated platforms, cutting latency to near-real-time levels critical for autonomous features. Partnerships now bundle connectivity, edge computing, and developer tools into unified offerings that let OEMs launch new services faster. These alliances change the supplier landscape because carriers shift from bandwidth providers to strategic technology partners. The resulting service platforms underpin premium infotainment, remote diagnostics, and high-definition maps, supporting higher average revenue per user.

Mandatory E-Call and ADAS Regulations

The National Highway Traffic Safety Administration requires automatic emergency braking with pedestrian detection on all light vehicles by September 2029, carrying USD 354 million in annual compliance costs and lifetime benefits topping USD 5.82 billion. Europe enforces e-Call and a suite of driver-assistance functions under the General Safety Regulation, while China scales vehicle-road-cloud pilots with more than 7,000 5G-A base stations in Beijing. These mandates remove uncertainty around timelines, prompting OEMs to integrate connected sensors as standard equipment. Suppliers benefit from predictable volumes, and consumers gain universal safety features that lower accident rates.

Cyber-Security Vulnerabilities and Recalls

The Pwn2Own Automotive 2024 contest exposed a zero-click exploit in Alpine's Halo9 infotainment unit with a 96% success rate, highlighting the ease of remote compromise. Software-related recalls affected over 30 million vehicles in 2023, and the NIST-listed CVE-2023-6248 flaw enables full device takeover of popular telematics gateways. As vehicles become rolling data centres, their attack surface expands, raising the cost of post-sale patches and reputational damage. Regulators demand security-by-design, pushing suppliers to embed hardware root-of-trust, secure over-the-air frameworks, and continuous penetration testing.

Other drivers and restraints analyzed in the detailed report include:

- Subscription-Based Revenue Targets

- Edge AI Chips for In-Vehicle Inferencing

- High BOM Cost of Multi-Band V2X Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OEM installations captured 63.27% of the connected car devices market share in 2024 because factory-fitted hardware integrates deeply with vehicle diagnostics, power management, and warranty frameworks. Automakers embed modules during assembly to ensure compliance with e-Call and ADAS mandates, streamline over-the-air upgrades, and bolster brand control over data. Growing reliance on software-defined architectures cements this channel's leadership as OEMs link connectivity to revenue-generating services such as remote feature activation and predictive maintenance.

However, aftermarket providers are expanding quickly, with a 15.74% CAGR, as insurers and fleet managers retrofit legacy assets. Plug-and-play dongles and hardwired black boxes supply real-time usage data that underpins behaviour-based premiums and asset tracking. HARMAN's ready-upgrade kits exemplify solutions tailored for mixed fleets needing installation speed and cross-brand compatibility. While OEM control remains strong, price-sensitive owners and commercial operators continue to drive a parallel aftermarket, ensuring competitive variety within the connected car devices market.

Vehicle-to-vehicle links represented 39.62% of the connected car devices market revenue share in 2024 because they deliver collision warnings without requiring roadside units. Mature standards and demonstrated safety gains encourage OEMs to adopt V2V first, particularly in high-volume models aiming for five-star safety ratings. Retrofits also proliferate in commercial fleets where forward-collision alerts cut downtime and insurance costs.

Vehicle-to-grid capability is projected to post a 15.12% CAGR to 2030 as energy utilities partner with automakers to stabilise renewable-heavy grids. Bidirectional chargers paired with connectivity let electric cars feed stored power back to the network, creating new revenue for owners and grid operators. Growth in vehicle-to-infrastructure and vehicle-to-pedestrian segments follows smart-city spending, yet these depend on broader public investment. Over time, integrated V2X suites will blend all modes, but V2V will remain the cornerstone while ecosystems mature around it.

The Connected Car Devices Market Report is Segmented by End-User Type (OEM and Aftermarket), Communication Type (V2V, V2I, and More), Product Type (Driver Assistance System (DAS), Telematics, and More), Connectivity Technology (Embedded, Integrated, and More), Vehicle Propulsion Type (IC Engine and Electric), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 38.73% of the connected car devices market share in 2024. Uptake is driven by federal funding under the Infrastructure Investment and Jobs Act and consumer appetite for premium SUVs brimming with ADAS, high-definition infotainment, and 5G hotspots. Ongoing pilots with the U.S. Department of Transportation and the 5G Automotive Association boost confidence in C-V2X, while tight cybersecurity and privacy rules shape procurement specifications. Canada and Mexico benefit from integrated supply chains, enabling regional OEM plants to standardise connected modules and software stacks. These factors sustain healthy replacement cycles and after-sales subscriptions across North America.

Asia-Pacific is on track for the fastest 15.37% CAGR to 2030. China's vehicle-road-cloud blueprint anchors public and private spending, with Beijing alone hosting more than 7,000 5G-A base stations for intelligent mobility. Domestic brands embed connectivity to differentiate in a crowded electric-vehicle arena, while regional suppliers deliver cost-optimised telematics for two-wheelers and microcars. Japan and South Korea leverage chip-making prowess and early 5G roll-outs to test next-generation C-V2X sidelink features. India emerges as a high-volume opportunity as safety norms tighten and smartphone-savvy buyers demand always-on infotainment, though price sensitivity keeps tethered solutions relevant.

Europe maintains steady momentum under harmonised regulations such as mandatory e-Call and the General Safety Regulation. Germany, the United Kingdom, and France lead adoption as luxury marques bundle connectivity into premium trim lines, and mid-range brands follow suit. Energy-efficiency and carbon-reduction goals drive interest in vehicle-to-grid pilots that align EV charging with renewable output. Strict data sovereignty laws influence cloud-hosting choices, giving European-based providers an edge. Pan-EU standards for cybersecurity certification are under development, promising to streamline cross-border homologation and further stimulate the connected car devices market.

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- ZF Friedrichshafen AG

- Harman International

- Valeo SA

- Magna International

- Panasonic Corp.

- Visteon Corp.

- Autoliv Inc.

- Infineon Technologies AG

- Autotalks Ltd.

- Qualcomm Inc.

- NXP Semiconductors

- NVIDIA Corp.

- Sierra Wireless

- Cisco Systems

- Huawei Technologies

- AT&T

- Verizon

- Vodafone Group

- Ericsson

- LG Electronics

- Telit

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G Roll-Out and Carrier-OEM Partnerships

- 4.2.2 Mandatory E-Call and ADAS Regulations in US, EU, CN

- 4.2.3 Subscription-Based Revenue Targets by OEMs

- 4.2.4 Edge AI Chips Enabling In-Vehicle Inferencing

- 4.2.5 Usage-Based-Insurance Driving Aftermarket Telematics

- 4.2.6 Cross-Industry App-Store Ecosystems

- 4.3 Market Restraints

- 4.3.1 Cyber-Security Vulnerabilities and Recalls

- 4.3.2 High BOM Cost of Multi-Band V2X Modules

- 4.3.3 Data-Cloud Egress Fees Eroding OEM Service Margins

- 4.3.4 Semiconductor Supply-Chain Fragility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By End-User Type

- 5.1.1 OEM

- 5.1.2 Aftermarket

- 5.2 By Communication Type

- 5.2.1 V2V

- 5.2.2 V2I

- 5.2.3 V2P

- 5.2.4 V2N

- 5.2.5 V2G

- 5.3 By Product Type

- 5.3.1 Driver Assistance System (ADAS)

- 5.3.2 Telematics

- 5.3.3 In-Car Infotainment

- 5.3.4 Cyber-security Hardware

- 5.4 By Connectivity Technology

- 5.4.1 Embedded

- 5.4.2 Integrated

- 5.4.3 Tethered

- 5.4.4 DSRC

- 5.4.5 C-V2X (4G/5G)

- 5.5 By Vehicle Propulsion Type

- 5.5.1 Internal-Combustion Engine Vehicles

- 5.5.2 Electric Vehicles

- 5.5.2.1 Battery Electric Vehicle

- 5.5.2.2 Hybrid Electric Vehicle

- 5.5.2.3 Fuel-cell Electric Vehicle

- 5.5.2.4 Plug-in Hybrid Electric Vehicle

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Denso Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Harman International

- 6.4.6 Valeo SA

- 6.4.7 Magna International

- 6.4.8 Panasonic Corp.

- 6.4.9 Visteon Corp.

- 6.4.10 Autoliv Inc.

- 6.4.11 Infineon Technologies AG

- 6.4.12 Autotalks Ltd.

- 6.4.13 Qualcomm Inc.

- 6.4.14 NXP Semiconductors

- 6.4.15 NVIDIA Corp.

- 6.4.16 Sierra Wireless

- 6.4.17 Cisco Systems

- 6.4.18 Huawei Technologies

- 6.4.19 AT&T

- 6.4.20 Verizon

- 6.4.21 Vodafone Group

- 6.4.22 Ericsson

- 6.4.23 LG Electronics

- 6.4.24 Telit

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment