|

市场调查报告书

商品编码

1848293

聚酰亚胺薄膜:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Polyimide Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

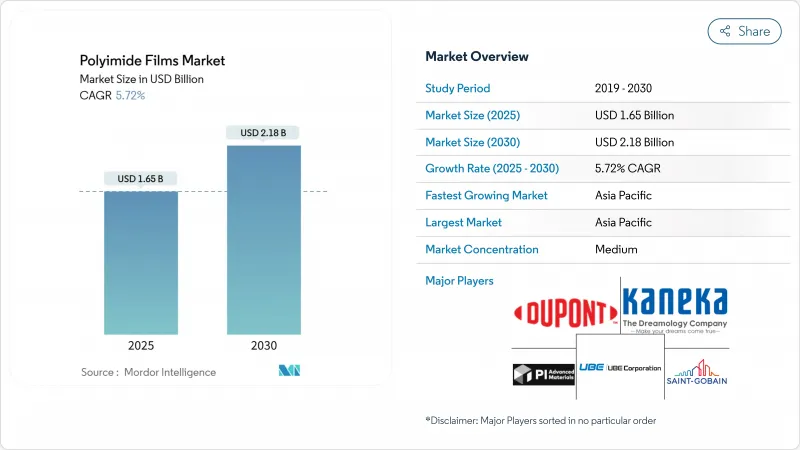

预计2025年全球聚酰亚胺薄膜市场规模将达到16.5亿美元,到2030年将达到21.8亿美元,2025年至2030年的复合年增长率为5.72%。

微型消费性电子产品、电气化交通和高温航太电子产品是需求的主要驱动力。 5G基础设施的持续投资以及向SiC/GaN功率元件的转型将增强高可靠性薄膜的长期消费。此外,与PFAS相关的监管压力可能会重塑树脂化学和采购模式。

全球聚酰亚胺薄膜市场趋势与洞察

折迭式和可捲曲显示器将加速无色聚酰亚胺薄膜的采用

随着智慧型手机製造商将第二代折迭式设备商业化,可折迭半径不超过3毫米的透明基板的需求日益增长。无色基板在450奈米波长下的透光率超过85%,并在超过10万次折迭循环中保持机械完整性,使原始设备製造商(OEM)能够采用超薄玻璃替代品并减轻铰链重量。一家韩国供应商推出了一种星形紫外线吸收剂,可抑制光劣化并延长汽车仪錶板的户外使用寿命。中国和韩国对面板的持续投资支持了稳定的供应。此外,旋转性电视的投产拓宽了应用基础,聚酰亚胺薄膜市场也持续向高阶显示器领域拓展。

导热聚酰亚胺薄膜可实现高密度电动车电池组

随着汽车平台向800V架构过渡,产生的热负荷也随之增加,因此,具有增强平面热导率的薄型电隔离器至关重要。含石墨的聚酰亚胺层压板如今的热传导率接近0.5 W/m*K,同时维持超过200 kV/mm的介电击穿强度,满足严格的安全裕度。受北极熊启发,中空二氧化硅结构的研究已达到0.041 W/m*K,降低了寒冷气候的失控风险。这些进展支持了中国、美国和德国积极的电池组緻密化计划,使聚酰亚胺薄膜市场在动力传动系统链中站稳了脚跟。

低成本替代品的可用性

琥珀色聚酰亚胺的价格溢价是同类PEN薄膜的两倍以上。 Kaladex PEN的机械RTI为160°C,适用于家用电器和标准汽车线束。对于电容器和中阶柔性电路而言,由于买家会权衡热裕度和元件成本,PEN的经济性正成为采购的驱动因素。在下一代显示器和功率元件的性能再次提升之前,成本敏感地区(尤其是东南亚和拉丁美洲)加强对高温聚酯的研发力度,可能会减少聚酰亚胺薄膜市场的销售量。

細項分析

传统琥珀色产品凭藉其在传统电线绝缘和柔性电路领域的优势,将在2024年占据聚酰亚胺薄膜市场份额的45%。儘管这一细分市场占据了聚酰亚胺薄膜市场的最大份额,但随着新化学技术的兴起,其成长率低于市场平均值。无色PI泡棉的复合年增长率将达到6.14%,这得益于折迭式行动电话、可捲曲电视和透明触控介面的普及。聚酰亚胺薄膜产业正在见证混合紫外线阻隔添加剂的研发,这些添加剂旨在保护主干免受太阳光劣化的影响,并填补曾经支撑玻璃盖板主导地位的性能缺口。

导热等级为电动车电池提供平面绝缘,分散局部热点,石墨或陶瓷微填料支援平面路径。氟涂层等级继续用于对酸稳定性至关重要的利基化学加工设备。双向拉伸薄膜的分子排列使其尺寸重复性在0.1%以内,仍然是柔性航太感测器的首选。虽然双向拉伸薄膜在聚酰亚胺薄膜市场中仅占一小部分,但其超高利润率正奖励日本和比利时的产能扩张。所有产品类型的技术创新正在支撑聚酰亚胺薄膜市场的韧性。

区域分析

预计到2024年,亚太地区将占聚酰亚胺薄膜市场收入的44%,到2030年,复合年增长率将达到6.00%。中国当地面板製造商将在2025年至2026年期间扩大其柔性OLED产能,以支援区域消费。国内树脂製造商曾经一度仅限于琥珀色电气级产品,如今正瞄准电子级聚酰亚胺,以减少对进口的依赖并提高成本竞争力。日本和韩国凭藉超净反应器和多级溶剂回收系统保持领先地位,从而能够满足高阶智慧型手机OEM厂商所需的一致光学透明度。印度作为专业电子代工中心的崛起正在吸引外国直接投资,扩大当地对软式电路板的需求。

北美在航太、国防和先进半导体应用领域占据着巨大的份额。杜邦公司斥资2.2亿美元在俄亥俄州瑟克尔维尔的扩建项目将增强高端Kapton和Pyralux的国内供应,缓解地缘政治供应担忧,并缩短国防部项目的前置作业时间。新兴企业,利用聚酰亚胺与MEMS感测器阵列和microLED背板的兼容性,扩大聚酰亚胺薄膜市场的区域覆盖范围。

欧洲正在推动稳定的工业需求,这得益于欧洲大陆的汽车和可再生能源设备的结构性支撑。围绕PFAS的监管势头正在加速配方的重新设计,并鼓励当地供应商投资绿色溶剂系统和无氟单体。这种适应性保护了该地区的聚酰亚胺薄膜市场免受整体萎缩的影响,同时向采用类似法规的其他司法管辖区输出环保解决方案。南美、中东和非洲仍然是规模较小的终端市场,但巴西蓬勃发展的电子产业丛集和海湾地区的国防卫星计画将推动需求成长。虽然这些地区普遍存在依赖进口的供应模式,但合资企业的洽谈表明,它们正逐渐转向本地化加工业务。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 折迭式和可捲曲显示器加速无色聚酰亚胺薄膜的采用

- 用于高密度电动车电池组的导热聚酰亚胺薄膜

- 卫星「新太空」电子设备需要耐辐射聚酰亚胺绝缘体

- 扩展5G基础设施

- 航太领域向高温 SiC/GaN 电力电子技术的过渡

- 市场限制

- 低成本替代品的可用性

- 酰亚胺化和溶剂回收生产线的资本投资较高

- 影响聚酰亚胺等级的PFAS逐步淘汰法规

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 依产品类型

- 常规(琥珀色)PI薄膜

- 无色PI膜

- 氟涂层PI薄膜

- 导热/石墨填充PI薄膜

- 双向拉伸PI薄膜

- 按用途

- 软性印刷电路板(FPCB)

- 特殊加工产品

- 感压胶带

- 电线电缆

- 电动机/发电机

- 按最终用途行业

- 电子产品

- 车

- 航太

- 标籤

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略性倡议(併购、合资、产能扩张)

- 市占率分析

- 公司简介

- 3M

- AGC Inc.

- Arakawa Chemical Industries,Ltd.

- DuPont

- IST Corporation

- KANEKA CORPORATION

- Kolon Industries, Inc.

- Mitsui Chemicals, Inc.

- PI Advanced Materials Co., Ltd.

- Saint-Gobain

- Taimide Tech. Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

- Von Roll

- Wuhan Imide New Materials Technology Co.,LTD

- Zhejiang Hecheng Smart Electric Co., Ltd.

第七章 市场机会与未来展望

The global polyimide films market reached USD 1.65 billion in 2025 and is projected to advance to USD 2.18 billion by 2030, reflecting a 5.72% CAGR over 2025-2030.

Miniaturized consumer electronics, electrified transportation, and high-temperature aerospace electronics are the principal engines of demand, while colorless formulations unlock opportunities in foldable displays. Persistent investment in 5G infrastructure and the transition toward SiC/GaN power devices reinforce long-term consumption of high-reliability films. Supply security remains a strategic issue because capacity additions lag the speed at which downstream sectors scale, and PFAS-related regulatory pressures could realign resin chemistry and sourcing patterns.

Global Polyimide Films Market Trends and Insights

Foldable and rollable displays accelerating colorless polyimide film uptake

Demand for transparent substrates that can fold below a 3 mm radius has intensified as smartphone makers commercialize second-generation foldable devices. Colorless substrates deliver more than 85% transmittance at 450 nm and retain mechanical integrity for more than 100,000 folding cycles, allowing original-equipment makers to integrate ultra-thin glass alternatives while achieving lighter hinges. Korean suppliers have introduced star-shaped UV absorbers that inhibit photodegradation and extend outdoor service life in automotive dashboards. Ongoing panel investments across China and South Korea underpin steady offtake, and the pipeline for rollable televisions is widening the application base, ensuring the polyimide films market continues to expand into premium display niches.

Thermally-conductive polyimide films enabling high-density EV battery packs

Vehicle platforms transitioning to 800 V architectures generate higher heat loads, making thin electrical isolators with enhanced in-plane thermal conductivity indispensable. Graphite-laden polyimide laminates now offer thermal conductivities approaching 0.5 W/m*K while sustaining dielectric breakdown strengths above 200 kV/mm, satisfying stringent safety margins. Research into polar-bear-inspired hollow SiO2 constructs achieved 0.041 W/m*K to mitigate cold-climate runaway risk. These advances support aggressive battery-pack densification programs in China, the United States, and Germany, giving the polyimide films market a solid foothold in power-train value chains.

Availability of low-cost substitutes

Amber polyimide commands a price premium that can exceed 2X comparable PEN films. Kaladex PEN delivers a mechanical RTI of 160 °C, adequate for consumer appliances and standard automotive harnesses. In capacitors and mid-range flex circuits, buyers weigh thermal margins against component cost, and PEN's economics increasingly sway procurement. Intensified research and development into higher-temperature polyester variants could peel volume away from the polyimide films market in cost-sensitive regions, particularly Southeast Asia and Latin America, until next-generation displays and power devices lift performance thresholds again.

Other drivers and restraints analyzed in the detailed report include:

- Satellite New-Space electronics requiring radiation-hard polyimide insulators

- Expansion of 5G infrastructure

- PFAS-phase-out regulations affecting polyimide grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional amber products generated 45% of polyimide films market share in 2024 on the strength of legacy wire insulation and flex circuitry. The segment constitutes the largest slice of polyimide films market size, yet its growth rate stays below the market average as newer chemistries capture attention. Colorless PI Form are on track for a 6.14% CAGR, riding the adoption curve in folding phones, rollable televisions, and transparent touch interfaces. The polyimide films industry witnesses a pipeline of hybrid UV-blocking additives that protect the backbone against solar aging, closing performance gaps that once anchored glass cover-window dominance.

Thermally-conductive grades supply electric-vehicle batteries with planar insulation that distributes localized hotspots, supported by graphite or ceramic micro-fillers for in-plane pathways. Fluorine-coated variants continue to serve niche chemical-processing equipment where acid stability is decisive. Biaxially stretched films, whose molecular alignment delivers dimensional repeatability within 0.1%, remain favored for aerospace sensor flexes. Although they hold a smaller slice of polyimide films market size, their ultra-high margins incentivize capacity additions in Japan and Belgium. Collective innovation across all product types sustains the resilience of the broader polyimide films market.

The Polyimide Film Market Report Segments the Industry by Product Type (Conventional PI Film, Colorless PI Film, and More), Application (Flexible Printed Circuit Boards, Specialty Fabricated Products, and More), End-Use Industry (Electronics, Automotive, Aerospace, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 44% of 2024 revenue for the polyimide films market and is projected to deliver a 6.00% CAGR through 2030. Mainland Chinese panel makers expand flexible OLED capacity during 2025-2026, underpinning regional consumption. Domestic resin suppliers, once confined to amber electrical grades, now target electronic-grade polyimide, narrowing import reliance and improving cost competitiveness. Japan and South Korea maintain a lead in ultra-clean reactors and multi-stage solvent-recovery systems, enabling consistent optical clarity demanded by premium smartphone OEMs. India emerges as a focal point for contract electronics manufacturing, drawing foreign direct investment that enlarges local pull for flexible substrates.

North America holds a prominent share attributable to aerospace, defense, and advanced semiconductor applications. DuPont's USD 220 million expansion in Circleville, Ohio deepens domestic supply of high-end Kapton and Pyralux variants, mitigating geopolitical supply concerns and shortening lead times for Department of Defense programs. Start-ups clustered around Silicon Valley exploit polyimide's compatibility with MEMS sensor arrays and micro-LED backplanes, injecting innovation that broadens the regional application canvas within the polyimide films market.

Europe commands stable industrial demand, structurally underpinned by continental automotive and renewable-energy equipment. Regulatory momentum around PFAS accelerates formulation redesign, prompting local suppliers to invest in green solvent systems and fluorine-free monomers. This adaptive capacity shields the regional polyimide films market from outright contraction while exporting environmental solutions to other jurisdictions adopting similar restrictions. South America and the Middle East and Africa remain smaller end-markets, yet Brazil's budding electronics clusters and Gulf defense satellite programs seed incremental demand. Import-reliant supply models dominate these regions, though joint-venture talks indicate gradual movement toward local converting operations.

- 3M

- AGC Inc.

- Arakawa Chemical Industries,Ltd.

- DuPont

- I.S.T Corporation

- KANEKA CORPORATION

- Kolon Industries, Inc.

- Mitsui Chemicals, Inc.

- PI Advanced Materials Co., Ltd.

- Saint-Gobain

- Taimide Tech. Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

- Von Roll

- Wuhan Imide New Materials Technology Co.,LTD

- Zhejiang Hecheng Smart Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Foldable and Rollable Displays Accelerating Colorless PolyImide Film Uptake

- 4.2.2 Thermally-Conductive Poly Imide Films Enabling High-Density EV Battery Packs

- 4.2.3 Satellite "New-Space" Electronics Requiring Radiation-Hard Poly Imide Insulators

- 4.2.4 Expansion of 5G infrastructure

- 4.2.5 Shift to High-Temperature SiC/GaN Power Electronics in Aerospace

- 4.3 Market Restraints

- 4.3.1 Availability of low-cost substitutes

- 4.3.2 High CapEx for Imidisation and Solvent-Recovery Lines

- 4.3.3 PFAS-Phase-out Regulations Affecting Poly Imide Grades

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Conventional (Amber) PI Film

- 5.1.2 Colorless PI Film

- 5.1.3 Fluorine-Coated PI Film

- 5.1.4 Thermally-Conductive/Graphite-Filled PI Film

- 5.1.5 Biaxially-Stretched PI Film

- 5.2 By Application

- 5.2.1 Flexible Printed Circuit Boards (FPCB)

- 5.2.2 Specialty Fabricated Products

- 5.2.3 Pressure Sensitive Tapes

- 5.2.4 Wire and Cable

- 5.2.5 Motor/Generator

- 5.3 By End-use Industry

- 5.3.1 Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace

- 5.3.4 Labelling

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JVs, Capacity Adds)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arakawa Chemical Industries,Ltd.

- 6.4.4 DuPont

- 6.4.5 I.S.T Corporation

- 6.4.6 KANEKA CORPORATION

- 6.4.7 Kolon Industries, Inc.

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 PI Advanced Materials Co., Ltd.

- 6.4.10 Saint-Gobain

- 6.4.11 Taimide Tech. Inc.

- 6.4.12 TORAY INDUSTRIES, INC.

- 6.4.13 UBE Corporation

- 6.4.14 Von Roll

- 6.4.15 Wuhan Imide New Materials Technology Co.,LTD

- 6.4.16 Zhejiang Hecheng Smart Electric Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Increased Research and Development in aerospace and space tech

聚酰亚胺薄膜市场:2026-2032年全球预测(依产品类型、薄膜厚度、应用和最终用途划分)

聚酰亚胺薄膜市场:2026-2032年全球预测(依产品类型、薄膜厚度、应用和最终用途划分) 2026年全球聚酰亚胺薄膜和胶带市场报告

2026年全球聚酰亚胺薄膜和胶带市场报告 聚酰亚胺薄膜市场-2026-2031年预测

聚酰亚胺薄膜市场-2026-2031年预测 日本聚酰亚胺薄膜市场报告(按应用、配销通路、最终用途和地区划分,2026-2034年)全球聚酰亚胺薄膜市场:市场规模、占有率、成长率、产业分析、按类型、应用和地区划分的考量因素及未来预测(2026-2034)

日本聚酰亚胺薄膜市场报告(按应用、配销通路、最终用途和地区划分,2026-2034年)全球聚酰亚胺薄膜市场:市场规模、占有率、成长率、产业分析、按类型、应用和地区划分的考量因素及未来预测(2026-2034) 聚酰亚胺薄膜市场规模、份额及成长分析(按类型、应用、终端用户产业及地区划分)-2026-2033年产业预测

聚酰亚胺薄膜市场规模、份额及成长分析(按类型、应用、终端用户产业及地区划分)-2026-2033年产业预测 全球聚酰亚胺薄膜和胶带市场评估:依应用、终端产业、地区、机会和预测(2018-2032 年)

全球聚酰亚胺薄膜和胶带市场评估:依应用、终端产业、地区、机会和预测(2018-2032 年) 高温聚酰亚胺薄膜市场规模、份额和趋势分析报告:按厚度、应用、地区和细分市场预测(2025-2033 年)聚酰亚胺薄膜市场规模、份额和趋势分析报告:按应用、最终用途、地区和细分市场预测(2025-2033 年)

高温聚酰亚胺薄膜市场规模、份额和趋势分析报告:按厚度、应用、地区和细分市场预测(2025-2033 年)聚酰亚胺薄膜市场规模、份额和趋势分析报告:按应用、最终用途、地区和细分市场预测(2025-2033 年) 电子产业聚酰亚胺薄膜市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

电子产业聚酰亚胺薄膜市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)