|

市场调查报告书

商品编码

1848301

工业和商用清洁化学品:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Industrial And Institutional Cleaning Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

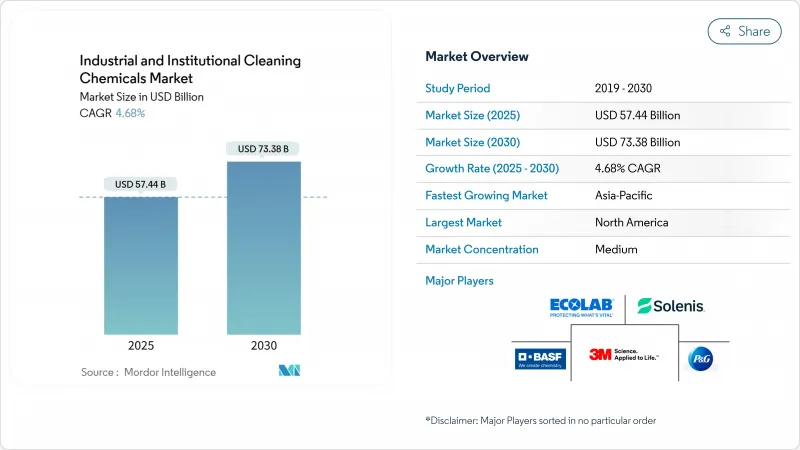

工业和商用清洁化学品市场规模预计在 2025 年为 574.4 亿美元,预计到 2030 年将达到 733.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.68%。

医疗保健、食品加工、快餐店和酒店业的结构性转变解释了市场的稳定趋势,而非週期性上涨。急性照护和长期照护中更严格的感染控制通讯协定推动了低接触式优质消毒剂的普及,而亚太地区快速工业化的经济体则推动了生物基製剂的超平均成长。儘管北美凭藉严格的法律规范保持了规模主导,但供应商正越来越多地针对新兴市场进行在地化创新,以应对波动性石化产品投入带来的利润压力。数位化计量、物联网远端监控和基于酵素的清洁化学品如今已成为核心竞争优势,这表明解决方案生态系统而非单一产品将决定未来的差异化。

全球工业和商用清洁化学品市场趋势和洞察

急性和长期照护机构中 COVID-19 后感染控制通讯协定

2024年,美国疾病管制与预防中心(CDC)加强了指引的製定,要求使用经美国环保署(EPA)註册且经证实可有效对抗多重抗药性细菌的消毒剂。该指南鼓励医院统一使用优质擦拭巾、喷雾剂和浓缩液,以减少接触时间,同时不牺牲频谱。联合委员会现在要求在医疗机构政策中明确提及这些联邦惯例,从而有效地实现采购专业化,并惩罚缺乏监管文件的供应商。领先的供应商正在捆绑支援物联网的分配器,以监控现场员工培训的合规性,从而最大限度地减少床栏和护理站等高接触区域的失误。人们对抗菌素抗药性的日益担忧进一步推动了对在表面上保持长时间活性的频谱化学品的需求,例如过氧乙酸混合物。

亚洲肉类和水产品加工企业采用 HACCP主导的消毒剂

亚洲各设施强制实施危害分析和关键控制点 (HACCP) 系统,迫使加工商采用消毒剂来应对地方性疾病和水硬度变化。哈萨克 2024 年的研究证实,实施 HACCP 可减少肉类中的铅和砷残留,从而定量提高安全性。越南虾类领导者 Minh Phu 现在将酵素清洁剂与不含过氧化物的消毒剂混合,以在保持出口残留基准值的情况下将整体清洁成本降低 30-50%。提供审核文件和快速现场技术建议的供应商具有优势,尤其是当产品符合清真和出口法规时。随着加工商扩大自动化程度,需求正转向可减少过量化学品使用和污水COD 负荷的控制剂量系统。

原物料价格波动

自2024年年中以来,石脑油相关界面活性剂原料价格上涨了12-15%,挤压了配方商的毛利率,迫使北美和欧洲的市场出现选择性溢价。为了应对市场波动,大型供应商正在对冲高达40%的环氧乙烷(EO)敞口,并加速用椰子衍生醇乙氧基化物或槐醣脂生物界面活性剂,这些表面活性剂追踪的是农业指数而非石化指数。配方改良专案也推动了活性剂浓度的提高,从而降低了包装重量和运输成本。然而,购买力有限的中小型调配商正面临营运资金压力,并推迟了区域扩张计画。

細項分析

2024年,界面活性剂将占据工业和商用清洁化学品市场份额的32.1%,是脱脂清洁剂、消毒湿纸巾和洗碗机清洁剂中不可或缺的一部分。其双亲性结构使其能够乳化油脂和颗粒污垢,使其成为获得HACCP认证的肉类加工厂和符合CDC标准的医院清洁剂功效声明的核心。然而,对石化产品的依赖使其面临价格波动和碳足迹审查的风险,这促使人们投资于槐醣脂和鼠李醣脂,它们具有类似的润湿性能,同时可将温室气体排放减少50%。联合利华的2024年采购政策要求供应商评估可追溯、无森林砍伐的成分,加速整个供应链的永续采购。

相较之下,溶剂是成长最快的原料类别,预计复合年增长率为6.3%。成长主要由水溶性乙二醇醚、生物基乳酸酯以及符合加州2025年0.5% VOC基准值的低VOC d-柠檬烯混合物所推动。墨西哥和美国的汽车OEM工厂越来越多地指定使用不易燃的水性零件清洁溶剂,这推动了对高闪点二元酸酯的需求。 N-N-甲基吡咯烷酮(NMP)和其他生殖毒性溶剂的监管压力也加速了金属清洁应用领域的替代,为那些能够不依赖危险分类而定制溶剂强度的供应商创造了市场空间。

一般清洁剂因其广泛适用于地板、墙壁和硬表面,预计到2024年将占销售额的35%。浓缩型稀释袋装清洁剂适用于客房清洁、卫浴清洁和玻璃清洁,塑胶重量减少80%,符合连锁饭店的ESG审核。产品管理也促进了防腐剂的再生产,以避免MIT和CMIT,确保符合欧洲2025年《除生物剂修正案》。

随着医疗保健、餐饮服务和交通枢纽加强卫生警戒,消毒剂和杀菌剂的复合年增长率达到 6.7%,超过所有其他类型。区域製剂製造商正在推出利用过氧化氢和柠檬酸的无季铵盐产品,以解决消费者的敏感问题并满足当地的排放限制。洗衣和汽车护理细分市场正在稳步增长,利用感测器驱动的剂量控制和水资源再利用系统,同时节省水电费和化学品用量。

区域分析

受美国疾病管制与预防中心 (CDC)、美国环保署 (EPA) 和美国食品药物管理局 (FDA) 等法规对备案优质解决方案的青睐推动,北美将在2024年引领工业和商用清洁化学品市场,收入份额达33%。医院采用符合CDC 2024年环境清洁程序的杀孢子擦拭巾,将支撑稳定的消毒剂需求。

亚太地区是成长引擎,2025年至2030年的复合年增长率为7.8%,这得益于卫生标准的提高、製造业的扩张以及政府对食源性疾病的打击。中国正在加紧修订消毒剂国家标准,鼓励国际供应商实现生产和文件的本地化。越南、泰国和印尼正在引入类似REACH的化学品管理法规,这提高了对成分透明度的需求,并加强了对生物基产品的采用。

欧洲是一个成熟而又创新的市场,欧盟绿色新政和不断发展的除生物剂指令推动配方师向植物来源活性剂和封闭式包装方向发展。德国正在试行商用清洁容器押金计划,而斯堪地那维亚的市政当局则强制要求碳中和采购,间接支持富含酵素的清洁剂。

中东和非洲将受益于海湾合作委员会、埃及和肯亚蓬勃发展的酒店计划和医疗保健投资,以及与美国和欧洲品牌签订的特许经营协议下的大量 QSR 部署。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 包含 3 个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 急性和长期照护机构中 COVID-19 后感染控制通讯协定

- 亚洲肉类和水产品加工中采用 HACCP主导的消毒剂

- 海湾合作委员会国家和埃及的快餐店蓬勃发展,需要自动洗碗机装载

- 全球旅游业和酒店业的復苏

- 东亚半导体无尘室扩建推动超低残留混合物

- 市场限制

- 原物料价格波动

- 环氧乙烷原料的波动性导致界面活性剂成本上升

- 严格的环境和健康法规

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 按原料

- 氯化碱

- 苛性钠

- 碱灰

- 氯

- 界面活性剂

- 非离子

- 阴离子

- 阳离子

- 男女

- 溶剂

- 酒精

- 碳氢化合物

- 氯化

- 醚

- 磷酸盐

- 酸

- 除生物剂

- 其他成分(螯合剂、流变改质剂、遮光剂、分散剂、酮、酯)

- 氯化碱

- 依产品类型

- 一般清洁剂

- 消毒剂和消毒剂

- 衣物洗护产品

- 车辆清洁产品

- 按原料产地

- 生物基/绿色

- 常规/石化

- 依市场类型

- 商业的

- 食品服务

- 零售

- 洗衣和干洗

- 卫生保健

- 洗车

- 办公室、饭店、住宿设施

- 製造业

- 食品/饮料加工

- 金属加工产品

- 电子元件

- 其他製造业(纺织、纸浆及造纸、石化)

- 商业的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- 3M

- Akzo Nobel NV

- Albemarle Corporation

- BASF

- Betco

- CLARIANT

- Croda International Plc

- Ecolab

- Henkel AG & Co. KGaA

- Huntsman International LLC

- KERSIA GROUP

- LANXESS

- National Chemical Laboratories, Inc.

- Nouryon

- Procter & Gamble

- Reckitt

- Solenis

- Solvay

- Spartan Chemical Company, Inc.

- Stepan Company

- Westlake Corporation

- WM Barr

第七章 市场机会与未来展望

The Industrial And Institutional Cleaning Chemicals Market size is estimated at USD 57.44 billion in 2025, and is expected to reach USD 73.38 billion by 2030, at a CAGR of 4.68% during the forecast period (2025-2030).

Structural shifts in healthcare, food processing, quick-service restaurants, and hospitality, rather than cyclical upswings, explain the market's steady trajectory. Premium disinfectants with rapid contact times are gaining traction as infection-control protocols tighten in acute and long-term care, while Asia-Pacific's fast-industrializing economies stimulate above-average growth for bio-based formulations. North America retains scale leadership through stringent regulatory oversight, but suppliers increasingly localize innovation for emerging markets to counter margin pressure from volatile petrochemical inputs. Digital dosing, IoT remote monitoring, and enzyme-enabled cleaning chemistries are now core competitive levers, signaling that solution ecosystems, not standalone products, will define future differentiation.

Global Industrial And Institutional Cleaning Chemicals Market Trends and Insights

Infection-Control Protocols Post-COVID-19 in Acute and Long-Term Care Facilities

Tighter guidelines from the CDC in 2024 require EPA-registered disinfectants with demonstrated efficacy against multidrug-resistant organisms, prompting hospitals to standardize on premium wipes, sprays and concentrates that shorten contact time without sacrificing spectrum. The Joint Commission now mandates explicit reference to these federal practices within facility policies, effectively professionalizing procurement and disadvantaging suppliers lacking regulatory dossiers. Leading vendors bundle on-site staff training with IoT-enabled dispensers that monitor compliance, minimizing error in high-touch zones such as bed rails and nurse stations. Elevated antimicrobial resistance concerns further spur demand for broad-spectrum chemistries like peracetic acid blends that remain active on surfaces for extended periods.

HACCP-Driven Sanitizer Adoption in Asian Meat and Seafood Processing

Mandatory hazard analysis and critical control point (HACCP) systems across Asian facilities compel processors to adopt sanitizers targeted to endemic pathogens and variable water hardness. A Kazakh study published in 2024 showed HACCP deployment cut lead and arsenic residues in meat, underscoring quantifiable safety gains. Vietnamese shrimp leader Minh Phu now blends enzyme-based cleaners with peroxide-free sanitizers, reducing overall cleaning costs 30-50% while staying within export residue limits. Suppliers that deliver both documentation for audits and rapid on-site technical advice have the inside track, particularly when products align with halal and export regulations. As processors scale automation, demand is shifting toward controlled-dosing systems that cut chemical overuse and wastewater COD loads.

Fluctuating Raw Material Prices

Surges of 12-15% in naphtha-linked surfactant feedstocks since mid-2024 squeezed formulators' gross margins and forced selective price surcharges in North America and Europe. To buffer volatility, large suppliers hedge up to 40% of EO exposure and accelerate substitution with coconut-derived alcohol ethoxylates or sophorolipid biosurfactants that track agricultural rather than petrochemical indices. Reformulation programs also push higher actives concentrations, cutting package weight and shipping costs. Still, small and mid-size blenders with limited purchasing leverage face working-capital stress, delaying regional expansion plans.

Other drivers and restraints analyzed in the detailed report include:

- QSR Boom in GCC and Egypt Requiring Automated Warewash Dosing

- Global Tourism and Hospitality Recovery

- Ethylene-Oxide Feedstock Volatility Elevating Surfactant Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surfactants retained 32.1% of industrial and institutional cleaning chemicals market share in 2024, anchored by indispensability across degreasers, disinfectant wipes and ware-wash detergents. Their amphiphilic structure enables emulsification of fats, oils and particulate soils, making them central to efficacy claims in HACCP-certified meat plants and CDC-compliant hospital cleaners. Yet petrochemical dependency exposes formulators to both price swings and carbon footprint scrutiny, pushing investment toward sophorolipids and rhamnolipids that deliver comparable wetting with 50% lower GHG emissions. Unilever's 2024 procurement policy now scores suppliers on traceable, deforestation-free feedstocks, accelerating sustainable sourcing across the chain.

Solvents, by contrast, represent the fastest-growing raw material category with a 6.3% forecast CAGR. Growth leans on water-miscible green glycol ethers, bio-derived lactate esters and low-VOC d-limonene blends that comply with California's 2025 0.5% VOC threshold for general cleaners. Auto OEM plants in Mexico and the United States increasingly specify non-flammable aqueous parts-wash solvents, fuelling demand for high-flashpoint dibasic esters. Regulatory pressure on N-methyl-2-pyrrolidone (NMP) and other reproductive-toxicity solvents accelerates substitution even in metal cleaning applications, opening market room for suppliers able to tailor solvency strength without hazardous classifications.

General-purpose cleaners represented 35% of 2024 revenue due to universal applicability on floors, walls and hard surfaces. Concentrated pouches that dilute in proportioned bottles now cover housekeeping, restroom and glass cleaning tasks with 80% lower plastic weight, answering chain-hotel ESG audits. Product stewardship also drives preservatives reformulation to avoid MIT and CMIT, ensuring compliance with Europe's 2025 biocide revisions.

Disinfectants and sanitizers outpace all other types at 6.7% CAGR because healthcare, foodservice and transit hubs maintain an elevated baseline of hygiene vigilance. Regional formulators introduce quaternary-ammonium-free options that leverage hydrogen peroxide and citric acid to meet consumer sensitivities and local discharge limits. Laundry and vehicle care subsegments grow steadily, tapping sensor-driven dosage control and water-re-use systems to conserve utilities and chemicals simultaneously.

The Industrial and Institutional Cleaning Chemicals Market Report Segments the Industry by Raw Material (Chlor-Alkali, Surfactants, Solvents, and More), Product Type (General-Purpose Cleaners, Disinfectants and Sanitizers, and More), Ingredient Origin (Bio-based/Green and Conventional/Petrochemical), Market Type (Commercial and Manufacturing), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

North America led the industrial and institutional cleaning chemicals market with 33% revenue share in 2024, buoyed by CDC, EPA and FDA regulations that favor premium, fully documented solutions. Hospitals adopt sporicidal wipes that comply with the CDC's 2024 environmental-cleaning procedures, underpinning steady disinfectant demand.

Asia-Pacific is the growth engine, registering a 7.8% CAGR over 2025-2030 on the back of rising hygiene standards, manufacturing expansion and government crackdowns on food-borne illness. China tightens GB standard revisions on disinfectants, nudging international suppliers to localize production and documentation. Vietnam, Thailand and Indonesia roll out REACH-style chemical control laws, heightening the need for ingredient transparency and bolstering bio-based adoption.

Europe remains a mature yet innovative market where the EU Green Deal and evolving biocide directives drive formulators toward plant-derived surfactants and closed-loop packaging. Germany pilots deposit systems for commercial cleaning canisters, while Scandinavian municipalities specify carbon-neutral procurement, indirectly favoring enzyme-rich cleaners.

The Middle East and Africa benefit from burgeoning hospitality projects and health-care investment across GCC, Egypt and Kenya, augmented by ample QSR rollout under franchise agreements with US and European brands.

- 3M

- Akzo Nobel N.V.

- Albemarle Corporation

- BASF

- Betco

- CLARIANT

- Croda International Plc

- Ecolab

- Henkel AG & Co. KGaA

- Huntsman International LLC

- KERSIA GROUP

- LANXESS

- National Chemical Laboratories, Inc.

- Nouryon

- Procter & Gamble

- Reckitt

- Solenis

- Solvay

- Spartan Chemical Company, Inc.

- Stepan Company

- Westlake Corporation

- WM Barr

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infection-Control Protocols Post-COVID-19 in Acute and Long-Term Care Facilities

- 4.2.2 HACCP-Driven Sanitizer Adoption in Asian Meat and Seafood Processing

- 4.2.3 Quick-Service Restaurant Boom in GCC and Egypt Requiring Automated Warewash Dosing

- 4.2.4 Global Tourism and Hospitality Recovery

- 4.2.5 Semiconductor Cleanroom Expansion Driving Ultra-Low-Residue Blends in East Asia

- 4.3 Market Restraints

- 4.3.1 Fluctuating Raw Material Prices

- 4.3.2 Ethylene-Oxide Feedstock Volatility Elevating Surfactant Costs

- 4.3.3 Stringent Environmental and Health Regulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Chlor-alkali

- 5.1.1.1 Caustic Soda

- 5.1.1.2 Soda Ash

- 5.1.1.3 Chlorine

- 5.1.2 Surfactants

- 5.1.2.1 Non-ionic

- 5.1.2.2 Anionic

- 5.1.2.3 Cationic

- 5.1.2.4 Amphoteric

- 5.1.3 Solvents

- 5.1.3.1 Alcohols

- 5.1.3.2 Hydrocarbons

- 5.1.3.3 Chlorinated

- 5.1.3.4 Ethers

- 5.1.4 Phosphates

- 5.1.5 Acids

- 5.1.6 Biocides

- 5.1.7 Other Raw Materials (Chelants, Rheology Modifiers, Opacifiers, Dispersants, Ketones, Esters)

- 5.1.1 Chlor-alkali

- 5.2 By Product Type

- 5.2.1 General-Purpose Cleaners

- 5.2.2 Disinfectants and Sanitizers

- 5.2.3 Laundry Care Products

- 5.2.4 Vehicle Wash Products

- 5.3 By Ingredient Origin

- 5.3.1 Bio-based / Green

- 5.3.2 Conventional / Petrochemical

- 5.4 By Market Type

- 5.4.1 Commercial

- 5.4.1.1 Foodservice

- 5.4.1.2 Retail

- 5.4.1.3 Laundry and Dry-Cleaning

- 5.4.1.4 Healthcare

- 5.4.1.5 Car Washes

- 5.4.1.6 Offices, Hotels and Lodging

- 5.4.2 Manufacturing

- 5.4.2.1 Food and Beverage Processing

- 5.4.2.2 Fabricated Metal Products

- 5.4.2.3 Electronic Components

- 5.4.2.4 Other Manufacturing (Textile, Pulp and Paper, Petrochemical)

- 5.4.1 Commercial

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Malaysia

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Turkey

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Nigeria

- 5.5.5.7 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Albemarle Corporation

- 6.4.4 BASF

- 6.4.5 Betco

- 6.4.6 CLARIANT

- 6.4.7 Croda International Plc

- 6.4.8 Ecolab

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International LLC

- 6.4.11 KERSIA GROUP

- 6.4.12 LANXESS

- 6.4.13 National Chemical Laboratories, Inc.

- 6.4.14 Nouryon

- 6.4.15 Procter & Gamble

- 6.4.16 Reckitt

- 6.4.17 Solenis

- 6.4.18 Solvay

- 6.4.19 Spartan Chemical Company, Inc.

- 6.4.20 Stepan Company

- 6.4.21 Westlake Corporation

- 6.4.22 WM Barr

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Emerging Use of Bio-based Cleaning Chemicals

工业和机构清洁化学品市场分析及预测(至2035年):按类型、产品、服务、技术、应用、剂型、材料类型、最终用户和功能划分

工业和机构清洁化学品市场分析及预测(至2035年):按类型、产品、服务、技术、应用、剂型、材料类型、最终用户和功能划分 2026年全球工业和机构清洁化学品市场报告

2026年全球工业和机构清洁化学品市场报告 工业和机构清洁化学品市场规模、份额和成长分析(按原料、产品、应用、产业和地区划分)-2026-2033年产业预测

工业和机构清洁化学品市场规模、份额和成长分析(按原料、产品、应用、产业和地区划分)-2026-2033年产业预测 工业和机构清洁化学品市场规模、份额和趋势分析报告:按原材料、产品、最终用途、地区和细分市场预测(2026-2033 年)

工业和机构清洁化学品市场规模、份额和趋势分析报告:按原材料、产品、最终用途、地区和细分市场预测(2026-2033 年) 工业和机构清洁化学品市场预测至2032年:按产品类型、来源、原材料、应用、最终用户和地区分類的全球分析

工业和机构清洁化学品市场预测至2032年:按产品类型、来源、原材料、应用、最终用户和地区分類的全球分析 全球工业和机构清洁化学品市场(2024-2028)

全球工业和机构清洁化学品市场(2024-2028)