|

市场调查报告书

商品编码

1910628

汽车软体:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

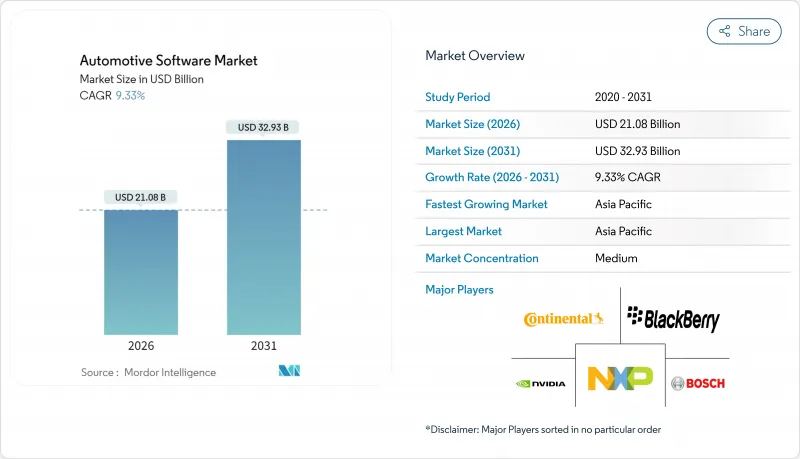

预计到 2025 年,汽车软体市场规模将达到 192.8 亿美元,到 2026 年将达到 210.8 亿美元,到 2031 年将达到 329.3 亿美元,预测期(2026-2031 年)的复合年增长率为 9.33%。

这种成长反映了汽车产业正从以硬体为中心的模式稳步向软体定义平台转变,其中从电池优化到自动驾驶等关键功能都嵌入在程式码中,而非机械部件中。分区电子/电气架构的日益普及,使线束重量减轻了高达30%,从而释放了运算能力用于开发新功能。全球汽车製造商正在快速部署空中下载(OTA)功能,以符合欧盟WP.29网路安全和软体更新法规。同时,基于订阅的「按需功能」服务正开始带来丰厚的售后收入。半导体供应商、超大规模资料中心业者和一级软体公司日益增长的兴趣加剧了竞争,导致收购活动激增,以确保作业系统、中介软体和安全堆迭资产的安全。这些趋势,加上政府对电气化的奖励,正在推动资金持续流入电池管理软体、边缘云端连接和人工智慧驱动的程式码产生工具领域。

全球汽车软体市场趋势与洞察

中国汽车製造商推出L2+级自动驾驶功能,推动亚洲ADAS代码量成长。

比亚迪、小鹏和捷克等品牌正在采用敏捷开发框架,将功能发布週期缩短高达 60%,导致 ADAS 代码量激增,并加速了西方竞争对手的竞争优势。感知处理、感测器融合和路径规划演算法的快速迭代开发,推动了对冗余运算的需求,促使主要晶片製造商设计嵌入国产集中式 ECU 中的特定领域加速器。业内相关人员指出,符合规范的 OTA 升级流程对于维持车队更新至关重要,而安全的 DevOps 是维持市场领先地位的先决条件。

OEM厂商转向集中式分区电子电气架构将增加全球中介软体支出

以特斯拉 Model 3 等车款为例,以四到六个区域控制器取代数十个域 ECU,可显着简化布线,减轻重量并降低功率损耗。然而,分散式布局将复杂性转移到了软体层,例如抽象异质感测器、管理确定性通讯以及实施功能安全分区。由于 OEM 厂商正在快速整合 AUTOSAR Classic 和 Adaptive 协定堆迭、即时 POSIX 核心以及云端 API,中间件供应商报告称,整合计划积压严重。恩智浦以 6.25 亿美元收购 TTTech Auto,凸显了可跨车型系列扩展的认证中间件的价值。

中介软体标准碎片化阻碍了OEM厂商之间的重复使用。

由于缺乏统一的API,一级供应商不得不将相同的功能移植到多个专有协议堆迭中,这增加了检验成本并扼杀了创新。 AUTOSAR和SOAFEE等联盟提案了协调一致的以服务为导向的框架,但品牌策略的差异,尤其是在坚持使用专有层的欧洲OEM厂商之间,阻碍了融合。因此,中介软体供应商开发出可配置的适配器,以牺牲效能为代价换取可移植性,这种折衷方案增加了运行时开销并使安全认证更加复杂。

细分市场分析

应用软体仍将是最大的收入驱动力,预计到2025年将占汽车软体市场48.02%的份额,这反映了客户对高级驾驶辅助系统(ADAS)、资讯娱乐系统和个人化空中下载(OTA)更新的需求。作业系统平台是成长最快的细分市场,随着原始设备製造商(OEM)采用针对功能安全进行强化的基于Linux的发行版,其复合年增长率(CAGR)将达到9.62%。随着统一运算加速功能部署,应用层程式码的市场规模预计将稳定成长。中间件的战略价值也在不断提升,它充当POSIX核心和更高级别应用程式之间经过安全认证的桥樑,Aptiv将其称为区域间流量的「协调器」。

对开放原始码元件日益增长的依赖正在重塑供应商之间的谈判格局。半导体供应商捆绑参考镜像以加速客户采用,而软体整合商则寻求从长期维护、网路安全加固和版本控制中获利。随着汽车软体市场向共用程式码库演进,相关人员在合规性、整合工具和即时确定性方面展开竞争。以恩智浦收购中间件为例的产业整合表明,平台覆盖范围将决定即将推出的电动车和自动驾驶汽车的合约归属。

预计到2025年,ADAS(高级驾驶辅助系统)和安全系统将占汽车软体市场收入的33.25%,这主要得益于欧盟通用安全法规强制要求配备智慧速度辅助、车道维持和自动紧急煞车等功能。该细分市场受益于高搭载率和频繁的功能升级,而ADAS软体仍是5G数据管道的核心。动力传动系统和电池管理应用预计将超越其他细分市场,以13.08%的复合年增长率增长,因为汽车製造商竞相延长纯电动车的续航里程、保护锂离子电池并协调双向充电。

资讯娱乐和远端资讯处理平台将利用 5G频宽、整合串流媒体合作伙伴以及收集车辆使用数据以进行预测性维护,从而支持持续的收入成长目标。车身控制模组将迁移到中央运算节点,共用晶片将降低物料清单成本,但同时也增加了对强大隔离性的需求。跨领域协作的加强将模糊传统的边界,而监管压力将促使安全逻辑固定在确定性核心中,并将非关键软体迁移到容器化的微服务中。

区域分析

预计2025年,亚洲将占据汽车软体市场最大份额,达38.62%,年复合成长率(CAGR)为11.48%。这主要得益于中国对软体定义汽车的快速普及以及政府对自动驾驶导航模组的激励措施。敏捷的发布週期使中国汽车製造商能够比传统製造商快60%整合L2及以上级别的功能,从而重振了中国的中间件和感知堆迭生态系统。韩国透过早期采用5G-V2X技术推动边缘云端分析,而日本则透过其人工智慧模型检验实验室专注于功能安全领域的领先地位。区域电池供应链正在加速软体增强型能源管理系统的发展,确保亚洲在汽车软体市场保持其核心地位。

北美排名第二,这得益于《通货膨胀与復苏法案》(IRA)的税额扣抵,该政策推动了对电池管理软体和家用充电优化设备的需求。订阅式功能的普及使得汽车製造商能够在车辆售出后很长一段时间内,透过驾驶辅助升级和资讯娱乐应用程式来实现盈利。硅谷的新兴企业提供人工智慧工具,可以缩短程式码发布週期;而底特律的老牌企业则实施DevOps流程,以达到消费性电子产品的开发速度。这些因素共同作用,使得每辆车的软体负载保持在高位,巩固了该地区作为汽车软体市场产生收入模式试验场的地位。

欧洲凭藉联合国WP.29框架下严格的网路安全和空中下载(OTA)法规,保持强大的市场地位,并积极推广经认证的软体更新管理系统。北欧国家(以瑞典主导)预计将以10.85%的复合年增长率成长,这主要得益于电动车的普及和数位服务应对力的提升。然而,开发人员,尤其是具备AUTOSAR认证的开发人员的短缺,正带来薪资上涨和专案延期的风险。对专业培训机构的投资标誌着欧洲正朝着培养本土能力的方向进行策略转型,也体现了欧洲在扩大软体生产规模的同时,致力于保障软体品质的决心。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 中国汽车製造商引入L2+级自动驾驶功能,正在推动亚洲ADAS代码量的成长。

- OEM厂商向集中式、分区式电气和电子架构的转型正在推动全球中介软体支出成长。

- 欧盟WP.29 OTA更新指令:加速欧洲安全软体堆迭的部署

- 北美地区基于订阅的「按需功能」模式推动售后软体收入成长

- 美国IRA电动车奖励推动电池管理软体的需求

- 韩国部署5G-V2X网路以支援边缘云汽车软体服务

- 市场限制

- 中介软体标准碎片化阻碍了OEM厂商之间的重复使用。

- 欧洲AUTOSAR Classic和Adaptive开发人员短缺,导致成本上升。

- R155/R156 网路安全认证考试费用 缓慢的课程进度

- 传统CAN架构限制了SDV在新兴市场的普及

- 价值/供应链分析

- 监管趋势(联合国欧洲经济委员会R155/R156号条例、美国OTA法规、欧盟网路弹性法案)

- 技术展望(区域架构、人工智慧工具链、空中升级管道)

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 软体层

- 应用软体

- 中介软体

- 作业系统

- 韧体/基本输入/输出软体

- 透过使用

- ADAS和安全系统

- 资讯娱乐和车载资讯系统

- 动力传动系统和电池管理

- 身体控制和舒适度

- 联网汽车服务

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 大型商用车辆

- 透过推进力

- 内燃机车辆

- 电池式电动车(BEV)

- 混合动力电动车(HEV/PHEV)

- 透过部署

- 车载(嵌入式)

- 云/边缘环境

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Robert Bosch GmbH

- Continental AG

- Elektrobit

- BlackBerry Limited(QNX)

- Google LLC(Alphabet Inc.)

- Microsoft Corporation

- Wind River Systems

- NXP Semiconductors NV

- NVIDIA Corporation

- Aptiv PLC

- TTTech Auto AG

- Vector Informatik GmbH

- Infineon Technologies AG

- Intel Corporation

- LG Electronics Vehicle Solutions

- DENSO Corporation

- Panasonic Automotive Systems

- KPIT Technologies Ltd.

- Intellias Ltd.

- Tata Elxsi Ltd.

- Airbiquity Inc.

- MontaVista Software LLC

- Renesas Electronics Corporation

- HARMAN International

- GlobalLogic Inc.

第七章 市场机会与未来展望

The automotive software market was valued at USD 19.28 billion in 2025 and estimated to grow from USD 21.08 billion in 2026 to reach USD 32.93 billion by 2031, at a CAGR of 9.33% during the forecast period (2026-2031).

Growth reflects the steady shift from hardware-centric vehicles to software-defined platforms where key functions, ranging from battery optimisation to automated driving, reside in code rather than mechanical parts. The rising adoption of zonal electronic/electrical architectures is trimming harness weight by up to 30% and freeing computing power for new features. Global automakers are fast-tracking over-the-air (OTA) update capabilities to comply with EU WP.29 cybersecurity and software-update rules, while subscription-based "functions-on-demand" services are starting to unlock high-margin, post-sale revenue streams. Heightened interest from semiconductor suppliers, hyperscalers, and Tier-1 software firms is intensifying competition, prompting a surge of acquisitions to secure operating-system, middleware, and safety-stack assets. These moves and government incentives for electrification keep capital flowing into battery-management software, edge-cloud connectivity, and AI-driven code-generation tools.

Global Automotive Software Market Trends and Insights

Level-2+ Autonomous Launches by Chinese OEMs Boosting ADAS Code Volume in Asia

Agile development frameworks allow brands such as BYD, Xpeng, and Zeekr to trim feature-release cycles by up to 60%, driving an explosion in ADAS code lines and accelerating competitive catch-up by Western rivals. Rapid iteration on perception, sensor fusion, and path-planning algorithms fuels demand for redundant compute, leading chipmakers to design domain-specific accelerators packaged within Chinese-built centralized ECUs. Industry observers note that compliant OTA pipelines are mandatory to keep those fleets current, making secure DevOps a prerequisite for sustained market leadership.

OEM Shift to Centralized Zonal E/E Architectures Raising Middleware Spend Globally

Replacing dozens of domain ECUs with four to six zone controllers simplifies wiring significantly, as exemplified in models such as Tesla Model 3, cuts weight, and reduces power loss. Yet decentralised layout shifts complexity toward software layers that must abstract heterogeneous sensors, manage deterministic communication, and enforce functional-safety partitions. Middleware vendors report a backlog of integration projects as OEMs race to harmonise AUTOSAR Classic and Adaptive stacks, real-time POSIX kernels, and cloud APIs. NXP's USD 625 million purchase of TTTech Auto highlighted the premium on certified middleware that can scale across vehicle families.

Fragmented Middleware Standards Hindering Cross-OEM Re-use

Lack of unified APIs forces Tier-1s to port identical functions to multiple proprietary stacks, elevating validation expense and slowing innovation. Consortia such as AUTOSAR and SOAFEE have proposed harmonised service-oriented frameworks, yet diverging brand strategies stall convergence, particularly among European OEMs with entrenched bespoke layers. Middleware houses thus build configurable adapters that sacrifice performance for portability, a compromise that adds runtime overhead and complicates safety certification.

Other drivers and restraints analyzed in the detailed report include:

- EU WP.29 OTA-Update Mandate Accelerating Secure Software Stacks in Europe

- Subscription-Based 'Functions-on-Demand' Models Expanding Post-Sale Software Revenues in North America

- Shortage of AUTOSAR Classic and Adaptive Developers in Europe Inflating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Application software still delivers the highest revenue at 48.02% of the automotive software market in 2025, mirroring customer appetite for ADAS, infotainment, and personalised over-the-air upgrades. Operating-system platforms are the fastest-growing slice, advancing at 9.62% CAGR as OEMs embrace Linux-based distributions hardened for functional safety. The market size for application-layer code is projected to climb steadily as consolidated compute unlocks faster feature roll-outs. Middleware's strategic value climbs in step, acting as a safety-certified bridge between POSIX kernels and high-level apps; Aptiv calls it the "orchestrator" of zonal traffic.

Growing reliance on open-source components reshapes vendor bargaining power. Silicon suppliers bundle reference images to accelerate customer entry, while software integrators monetise long-term maintenance, cyber-hardening, and variant management. As the automotive software market evolves toward shared code bases, stakeholders differentiate via compliance, integration tooling, and real-time determinism. Consolidation, exemplified by NXP's middleware acquisition, signals that platform breadth will determine contract wins for forthcoming electric and autonomous vehicle launches.

ADAS and safety systems delivered 33.25% revenue of the automotive software market in 2025, thanks to mandatory intelligent-speed assist, lane-keeping, and AEB under the EU General Safety Regulation. The cluster benefits from high attach rates and frequent feature upgrades, keeping ADAS software at the heart of 5 G-enabled data pipelines. Powertrain and battery-management applications are forecasted to outpace all others at 13.08% CAGR as OEMs race to extend BEV range, safeguard lithium-ion cells, and orchestrate bidirectional charging.

Infotainment and telematics platforms absorb 5G bandwidth, integrate streaming partners, and harvest vehicle-usage data for predictive maintenance, fuelling recurring revenue ambitions. Body-control modules migrate to central compute nodes, where shared silicon slashes bill-of-materials cost yet magnifies the need for robust isolation. Increasing cross-domain orchestration blurs historical boundaries, but regulatory pressure keeps safety logic anchored in deterministic cores while non-critical software shifts toward containerised microservices.

The Automotive Software Market Report is Segmented by Software Layer (Application Software, Middleware, and More), Application (ADAS and Safety Systems and More), Vehicle Type (Passenger Cars and More), Propulsion (Internal Combustion Engine Vehicles (ICE) and More), Deployment (On-Board (Embedded) and Off-Board (Cloud / Edge)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia commanded the largest regional share at 38.62% of the automotive software market in 2025, and is projected to grow at an 11.48% CAGR, propelled by China's fast-track deployment of software-defined vehicles and government incentives for autonomous navigation modules. Agile release cycles let Chinese OEMs integrate Level-2+ functions at a pace 60% quicker than traditional counterparts, catalysing domestic middleware and perception-stack ecosystems. South Korea's early roll-out of 5 G-V2X enables edge-cloud analytics, while Japan focuses on functional-safety leadership through AI-model verification labs. Regional battery supply chains accelerate software-enhanced energy-management systems, ensuring that Asia remains the gravitational centre of the automotive software market.

North America sits second, leveraging the Inflation Reduction Act credits to swell demand for battery-management software and home-charging optimisers. Subscription-driven features have proliferated, allowing automakers to monetise driver-assistance upgrades and infotainment apps long after the point of sale. Silicon Valley start-ups inject AI tooling that shortens code-release cycles, and Detroit incumbents adopt DevOps pipelines mirroring consumer-electronics cadence. Together, these factors sustain high per-vehicle software content, cementing the region as a testbed for revenue-generation models in the automotive software market.

Europe maintains a formidable position anchored by stringent cybersecurity and OTA mandates under UN WP.29, driving uptake of certified software-update management systems. The Nordics, spearheaded by Sweden, are pegged for a 10.85% CAGR on the back of EV prevalence and digital-service readiness. Nonetheless, developer shortages, particularly AUTOSAR-certified talent, impose wage inflation and risk schedule slippage. Investment in dedicated training academies reflects a strategic pivot to home-grown capability, underscoring Europe's resolve to safeguard quality while scaling software output.

- Robert Bosch GmbH

- Continental AG

- Elektrobit

- BlackBerry Limited (QNX)

- Google LLC (Alphabet Inc.)

- Microsoft Corporation

- Wind River Systems

- NXP Semiconductors N.V.

- NVIDIA Corporation

- Aptiv PLC

- TTTech Auto AG

- Vector Informatik GmbH

- Infineon Technologies AG

- Intel Corporation

- LG Electronics Vehicle Solutions

- DENSO Corporation

- Panasonic Automotive Systems

- KPIT Technologies Ltd.

- Intellias Ltd.

- Tata Elxsi Ltd.

- Airbiquity Inc.

- MontaVista Software LLC

- Renesas Electronics Corporation

- HARMAN International

- GlobalLogic Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Level-2+ Autonomous Launches by Chinese OEMs Boosting ADAS Code Volume in Asia

- 4.2.2 OEM Shift to Centralized Zonal E/E Architectures Raising Middleware Spend Globally

- 4.2.3 EU WP.29 OTA-Update Mandate Accelerating Secure Software Stacks in Europe

- 4.2.4 Subscription-Based 'Functions-on-Demand' Models Expanding Post-Sale Software Revenues in North America

- 4.2.5 U.S. IRA EV Incentives Driving Battery-Management Software Demand

- 4.2.6 Roll-out of 5G-V2X Networks Enabling Edge-Cloud Automotive Software Services in South Korea

- 4.3 Market Restraints

- 4.3.1 Fragmented Middleware Standards Hindering Cross-OEM Re-use

- 4.3.2 Shortage of AUTOSAR Classic & Adaptive Developers in Europe Inflating Costs

- 4.3.3 R155/R156 Cyber-Homologation Testing Costs Delaying Program Timelines

- 4.3.4 Legacy CAN Architectures in Emerging Markets Limiting SDV Adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (UNECE R155/R156, U.S. OTA Rules, EU Cyber Resilience Act)

- 4.6 Technological Outlook (Zonal Architecture, AI Tool-chains, Over-the-Air Pipelines)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Software Layer

- 5.1.1 Application Software

- 5.1.2 Middleware

- 5.1.3 Operating System

- 5.1.4 Firmware / Basic Input-Output Software

- 5.2 By Application

- 5.2.1 ADAS and Safety Systems

- 5.2.2 Infotainment and Telematics

- 5.2.3 Powertrain and Battery-Management

- 5.2.4 Body Control and Comfort

- 5.2.5 Connected Vehicle Services

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.4 By Propulsion

- 5.4.1 Internal Combustion Engine Vehicles (ICE)

- 5.4.2 Battery Electric Vehicles (BEV)

- 5.4.3 Hybrid Electric Vehicles (HEV/PHEV)

- 5.5 By Deployment

- 5.5.1 On-Board (Embedded)

- 5.5.2 Off-Board (Cloud / Edge)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of the Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Elektrobit

- 6.4.4 BlackBerry Limited (QNX)

- 6.4.5 Google LLC (Alphabet Inc.)

- 6.4.6 Microsoft Corporation

- 6.4.7 Wind River Systems

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 NVIDIA Corporation

- 6.4.10 Aptiv PLC

- 6.4.11 TTTech Auto AG

- 6.4.12 Vector Informatik GmbH

- 6.4.13 Infineon Technologies AG

- 6.4.14 Intel Corporation

- 6.4.15 LG Electronics Vehicle Solutions

- 6.4.16 DENSO Corporation

- 6.4.17 Panasonic Automotive Systems

- 6.4.18 KPIT Technologies Ltd.

- 6.4.19 Intellias Ltd.

- 6.4.20 Tata Elxsi Ltd.

- 6.4.21 Airbiquity Inc.

- 6.4.22 MontaVista Software LLC

- 6.4.23 Renesas Electronics Corporation

- 6.4.24 HARMAN International

- 6.4.25 GlobalLogic Inc.

7 Market Opportunities and Future Outlook

电池管理系统硬体在环测试市场(按最终用途、车辆类型、组件类型、测试模式、应用和BMS类型划分),全球预测,2026-2032年

电池管理系统硬体在环测试市场(按最终用途、车辆类型、组件类型、测试模式、应用和BMS类型划分),全球预测,2026-2032年 汽车保固管理软体市场规模、份额和成长分析(按产品类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测

汽车保固管理软体市场规模、份额和成长分析(按产品类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测 全球汽车终端认证市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车终端认证市场规模、份额、趋势和成长分析报告(2026-2034) 汽车软体市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、应用、软体层级、地区及竞争格局划分,2021-2031年)高阶驾驶辅助系统的硬体在环测试市场,按测试类型、测试阶段、车辆类型和应用划分,全球预测(2026-2032年)

汽车软体市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、应用、软体层级、地区及竞争格局划分,2021-2031年)高阶驾驶辅助系统的硬体在环测试市场,按测试类型、测试阶段、车辆类型和应用划分,全球预测(2026-2032年) 汽车软体市场机会、成长要素、产业趋势分析及2026年至2035年预测

汽车软体市场机会、成长要素、产业趋势分析及2026年至2035年预测 日本汽车软体市场按产品类型、车辆类型、应用和地区划分,2026-2034年

日本汽车软体市场按产品类型、车辆类型、应用和地区划分,2026-2034年 汽车软体市场规模、份额和成长分析(按软体类型、应用、最终用途、部署类型和地区划分)-2026-2033年产业预测

汽车软体市场规模、份额和成长分析(按软体类型、应用、最终用途、部署类型和地区划分)-2026-2033年产业预测 车载娱乐系统市场预测至2032年:按系统类型、组件、车辆类型、通路和地区分類的全球分析车辆即平台硬体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

车载娱乐系统市场预测至2032年:按系统类型、组件、车辆类型、通路和地区分類的全球分析车辆即平台硬体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)