|

市场调查报告书

商品编码

1848335

木醋液:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Wood Vinegar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

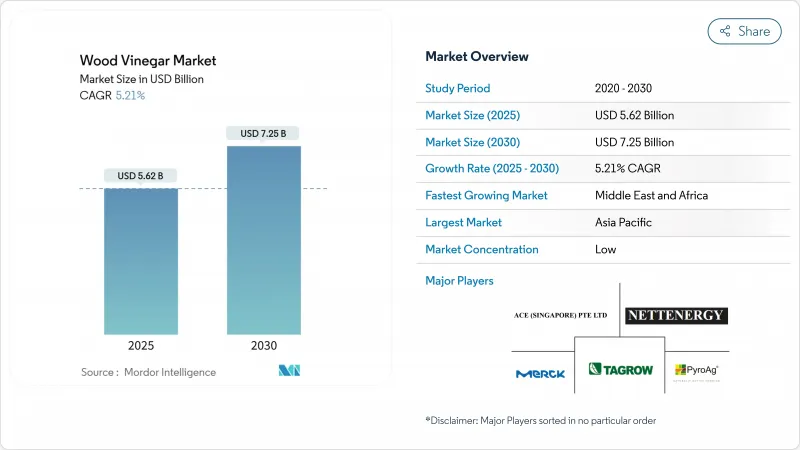

预计木醋市场规模到 2025 年将达到 56.2 亿美元,到 2030 年将达到 72.5 亿美元,复合年增长率为 5.21%。

农业、食品加工和特种化学品领域对生物基投入品的需求不断增长,是关键的催化剂,而日益严格的环境法规限制了合成化学品的使用,也进一步加剧了这一需求。政策对循环经济经营模式的大力支持、热解系统的快速技术改进以及水产养殖和化妆品领域终端应用的不断拓展,进一步拓宽了生物基材料的商业性前景。亚太地区凭藉中国、日本和东南亚成熟的生产群集,仍然是全球收益的主要驱动力;而中东和非洲则因永续农业倡议和有针对性的捐助项目而实现了最快的增长。关键的竞争态势包括持续的市场碎片化、充足的垂直整合空间以及高温热解反应器和连续蒸馏系统领域的专利活动活性化。

全球焦木酸市场趋势与洞察

对天然食品防腐剂和增味剂的需求不断增长

随着美国食品药物管理局(FDA)的GRAS框架明确了食品应用法规,食品和饮料产业向天然防腐剂的转变正在重塑木醋液的需求动态。木醋液的抗菌特性主要源自于其所含的乙酸和酚类化合物,为食品製造商提供了一种天然的替代品,可取代罐头食品、酱料和乳製品中合成的防腐剂。最近的研究表明,源自灵芝的木醋液具有与维生素C相当的广泛抗菌活性,并具有重要的抗氧化特性,可在延长保质期的同时保持食品安全标准。该化合物的天然来源符合消费者对洁净标示产品的偏好,使其采用率高于传统的防腐剂替代品。这一趋势在高端食品领域尤其明显,天然成分具有更高的价格溢价,为木醋液生产商创造了永续的收益来源。中国批准竹醋液用于化妆品,显示木醋液衍生物将在消费品中得到广泛认可,并有可能拓展传统食品应用以外的市场机会。

政府支持政策和环境法规

法律规范越来越倾向于生物基替代品而非合成化学品,这在多个国家和地区形成了对木醋液的结构性需求驱动力。欧盟在西班牙卡斯蒂利亚-拉曼恰地区推广木醋液作为天然生物除草剂的倡议表明了政府对永续农业实践的支持,在各种试验中喷洒了超过 3,000 公升木醋液,证明了其在有效除草的同时确保了对人类健康的安全。旨在减少合成农药的环境法规正在加速木醋液的采用,特别是在对食品中化学残留限制较严格的地区。政府对循环经济实践的奖励进一步支持了利用农业废弃物生产木醋液,解决了废弃物管理和永续农业目标。此类政策框架创造了长期的市场稳定性并鼓励对产能扩张的投资。

来自合成替代品的竞争

成熟的合成化学产业凭藉着成熟的供应链、标准化的产品和经过验证的功效,对木醋液的市场渗透构成了强大的竞争。合成杀虫剂和防腐剂得益于数十年的研发投入,其配方高度优化,性能特征可预测,许多最终用户比天然替代品更青睐这些配方。合成化学产业的规模经济使其具有竞争力的价格,这对合成化学品製造商构成了挑战,尤其是在永续性往往高于永续性的大宗农业应用领域。木醋液的应用通常需要新的监管途径,这会带来不确定性并延迟市场准入。合成替代品的性能一致性降低了那些无法容忍作物歉收或未经验证的天然替代品带来的产品品质问题的商业用户的风险。

細項分析

凭藉其成熟的基础设施和卓越的木醋酸产量,慢速热解将在2024年占据木醋酸市场58.45%的主导份额。由于能够最大限度地回收液体产品,同时最大限度地降低能耗,慢速热解法传统上一直占据市场主导地位。慢速热解尤其受到大规模商业营运的青睐,因为它能够确保稳定的产量和成本效益。其与现有系统的兼容性进一步支援了其广泛应用,使其成为希望在不进行大规模营运改造的情况下满足不断增长的需求的生产商的可靠选择。

相反,快速热解在木醋液市场正经历快速成长,预计在预测期(2025-2030年)的复合年增长率将达到7.34%。这一增长得益于技术进步,这些进步提高了生产效率并改善了产品品质。反应器设计和製程优化的创新是推动快速热解应用的关键因素,因为它们在维持高品质标准的同时显着缩短了加工时间。这些进步使快速热解成为越来越有吸引力的选择,适合那些希望扩大业务规模并有效满足不断变化的市场需求的生产商。

区域分析

到2024年,亚太地区将占据40.15%的主导市场。这得益于其悠久的农业应用以及已从传统木炭生产转型为一体化生物炼製厂运营的生产基础设施。政府对有机农业和生物基农药的大力支持进一步推动了这一成长。日本凭藉其先进的热解技术和严格的品管体系,为焦木酸生产树立了全球标准。同时,东南亚国家正在利用其丰富的棕榈壳和竹子蕴藏量,建构高效、经济的生产体系。此外,该地区的水产养殖业正在成为重要的成长引擎,研究强调了焦木酸在改善水质和鱼类健康方面的作用,尤其是在对虾养殖中。

中东和非洲将以最高的成长率领先,2025 年至 2030 年的复合年增长率将达到 7.95%。这种快速增长主要是因为该地区越来越认识到木醋酸在应对农业挑战方面的有效性,例如增强抗旱能力和防止土壤劣化。此外,该地区丰富的椰枣残渣可作为木醋酸的永续原料。该研究强调了将农业废弃物转化为有价值的生物产品、改善土壤特性和支持循环经济原则的成功。在政府倡导永续和有机农业的政策推动下,该地区为采用木醋酸创造了良好的环境。此外,国际发展项目正在推动这一势头,提供技术援助和资金以加强生产能力。

北美和欧洲的成熟市场面临严格的监管环境。这些地区优先考虑木醋液的高端用途,尤其是在食品、药品和高价值农业领域。在美国,FDA 的 GRAS 框架为木醋液进入食品应用领域提供了明确的路径。在大西洋彼岸的欧洲,法规越来越倾向生物基替代品,而远离合成化学品。同时,南美洲的农业充满了成长潜力。该地区的国家不仅支持有机农业,而且还在寻求合成农药的永续替代品。凭藉丰富的生物质资源和完善的农业框架,南美洲有望实现强劲的市场扩张。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 对天然食品防腐剂和增味剂的需求不断增加

- 政府支持政策和环境法规

- 向有机和永续农业转型

- 生物基农药需求不断成长

- 木醋液生产技术进展

- 扩大在水产养殖的应用

- 市场限制

- 生产成本高

- 来自合成替代品的竞争

- 缺乏科学检验和研究

- 分销和扩大规模的挑战

- 供应链分析

- 监理展望

- 波特五力模型

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 依製造方法

- 缓慢热解

- 中间热解

- 快速热解

- 按原料

- 竹子

- 硬木

- 针叶树

- 农业残留物

- 椰子壳

- 其他的

- 按用途

- 农业

- 作物营养

- 作物保护

- 食品/饮料

- 罐头

- 酱

- 乳製品

- 其他食品和饮料应用

- 动物饲料

- 製药

- 其他用途

- 农业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 其他北美地区

- 欧洲

- 英国

- 德国

- 西班牙

- 法国

- 义大利

- 荷兰

- 瑞典

- 波兰

- 比利时

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 印尼

- 泰国

- 新加坡

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥伦比亚

- 秘鲁

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 埃及

- 摩洛哥

- 奈及利亚

- 土耳其

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市场排名分析

- 公司简介

- Ace(Singapore)Pte Ltd

- Nettenergy BV

- Tagrow Co. Ltd

- Merck KGaA

- PyroAg Pty Ltd(PyroAg)

- Byron Biochar

- Earth Systems(Green Man Char)

- NewCarbon

- Shijiazhuang Hongsen Activated Carbon Co., Ltd.

- VerdiLife Inc.

- Nara Tanka Industries Co., Ltd.

- New Life Agro

- Tex Cycle

- Xi'An Hj Herb Biotechnology Co., Ltd.

- The Green Side of the Fence Ltd

- Haiqi Environmental Protection Technology Co.,ltd.

- Sane Shell Carbon

- Aspire Renoil Associates Co

- Qingdao Re-green Biological Technology Co.,Ltd.

- Penta Fine Ingredients, Inc.

第七章 市场机会与未来展望

The wood vinegar market size is valued at USD 5.62 billion in 2025 and is forecast to reach USD 7.25 billion by 2030, advancing at a 5.21% CAGR.

Rising demand for bio-based inputs in agriculture, food processing, and specialty chemicals is the primary catalyst, reinforced by tightening environmental regulations that discourage synthetic chemical use. Strong policy support for circular-economy business models, rapid technology upgrades in pyrolysis systems, and expanding end-use cases in aquaculture and cosmetics further broaden commercial prospects. Asia-Pacific continues to anchor global revenues through well-established production clusters in China, Japan, and Southeast Asia, while Middle East and Africa registers the quickest uptake due to sustainable-farming initiatives and targeted donor programs. Key competitive dynamics include persistent fragmentation, ample room for vertical integration, and escalating patent activity in high-temperature pyrolysis reactors and sequential distillation systems.

Global Wood Vinegar Market Trends and Insights

Increasing demand for natural food preservatives and flavor enhancers

The food and beverage industry's pivot toward natural preservatives is reshaping wood vinegar demand dynamics, with the FDA's GRAS framework providing regulatory clarity for food applications. Wood vinegar's antimicrobial properties, primarily attributed to its acetic acid content and phenolic compounds, offer food manufacturers a natural alternative to synthetic preservatives in canned foods, sauces, and dairy products. Recent research demonstrates that wood vinegar from Litchi chinensis exhibits broad-spectrum antibacterial activity comparable to vitamin C, with significant antioxidant properties that extend shelf life while maintaining food safety standards. The compound's natural origin aligns with consumer preferences for clean-label products, driving adoption rates that exceed traditional preservative alternatives. This trend is particularly pronounced in premium food segments where natural ingredients command price premiums, creating sustainable revenue streams for wood vinegar producers. The regulatory approval of bamboo vinegar for cosmetic applications in China signals broader acceptance of wood vinegar derivatives in consumer products, potentially expanding market opportunities beyond traditional food applications.

Supportive government policies and environmental regulations

Regulatory frameworks increasingly favor bio-based alternatives over synthetic chemicals, creating structural demand drivers for wood vinegar across multiple jurisdictions. The European Union's initiative promoting wood vinegar as a natural bio-herbicide in Castilla-La Mancha, Spain, demonstrates government support for sustainable agricultural practices, with over 3,000 liters applied in various trials showing effectiveness against weeds while maintaining safety for human health . Environmental regulations targeting synthetic pesticide reduction are accelerating wood vinegar adoption, particularly in regions implementing stringent chemical residue limits in food products. Government incentives for circular economy practices further support wood vinegar production from agricultural waste, addressing both waste management and sustainable agriculture objectives. These policy frameworks create long-term market stability and encourage investment in production capacity expansion.

Competition from synthetic alternatives

Established synthetic chemical industries present formidable competition through mature supply chains, standardized products, and proven efficacy profiles that challenge wood vinegar market penetration. Synthetic pesticides and preservatives benefit from decades of research and development investment, resulting in highly optimized formulations with predictable performance characteristics that many end-users prefer over natural alternatives. The synthetic chemical industry's economies of scale enable competitive pricing that wood vinegar producers struggle to match, particularly in commodity agricultural applications where cost considerations often outweigh sustainability benefits. Regulatory approval processes for synthetic chemicals are well-established and understood by industry participants, while wood vinegar applications often require novel regulatory pathways that create uncertainty and delay market entry. The performance consistency of synthetic alternatives provides risk mitigation for commercial users who cannot afford crop failures or product quality issues associated with unproven natural alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Rising demand for bio-based pesticides

- Expanding use in aquaculture

- High production costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, slow pyrolysis holds a commanding 58.45% share of the wood vinegar market, leveraging its established infrastructure and superior yields of wood vinegar. This method has traditionally dominated the market due to its ability to maximize liquid product recovery while minimizing energy consumption. Slow pyrolysis is particularly favored for large-scale commercial operations, as it ensures consistent output and cost efficiency. Its widespread adoption is further supported by its compatibility with existing systems, making it a reliable choice for producers aiming to meet growing demand without significant operational overhauls.

Conversely, fast pyrolysis is experiencing rapid growth in the wood vinegar market, with a projected CAGR of 7.34% during the forecast period of 2025-2030. This growth is driven by technological advancements that enhance production efficiency and improve product quality. Innovations in reactor design and process optimization are key factors propelling the adoption of fast pyrolysis, as they significantly reduce processing time while maintaining high-quality standards. These advancements make fast pyrolysis an increasingly attractive option for producers seeking to scale operations and meet evolving market demands efficiently.

The Wood Vinegar Market Report is Segmented by Production Method (Slow Pyrolysis, Intermediate Pyrolysis, and Fast Pyrolysis), Feed Stock (Bamboo, Hardwood, Softwood, and More), Application (Agriculture, Food and Beverage, Animal Feed, Pharmaceuticals, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2024, the Asia-Pacific region commands a dominant 40.15% market share, bolstered by its long-standing agricultural applications and a production infrastructure that has transitioned from traditional charcoal manufacturing to integrated biorefinery operations. This growth is further fueled by robust government backing for organic farming and bio-based pesticides. Japan sets global standards in wood vinegar production with its cutting-edge pyrolysis technologies and stringent quality control systems. Meanwhile, Southeast Asian nations capitalize on their rich reserves of coconut shells and bamboo, crafting efficient and cost-effective production systems. Additionally, the region's aquaculture sector is emerging as a pivotal growth engine, with studies highlighting wood vinegar's role in enhancing water quality and fish health, particularly in shrimp farming.

The Middle East and Africa lead the pack with the highest growth rate, achieving a notable 7.95% CAGR from 2025 to 2030. This surge is largely attributed to the region's growing acknowledgment of wood vinegar's efficacy in tackling agricultural hurdles, such as bolstering drought resilience and combating soil degradation. Furthermore, the region's plentiful date palm residues serve as a sustainable feedstock for wood vinegar. Research underscores the successful transformation of agricultural waste into valuable bio-products, enhancing soil properties and championing circular economy principles. Bolstered by government policies that advocate for sustainable agriculture and organic farming, the region fosters a conducive environment for wood vinegar adoption. Additionally, international development programs bolster this momentum, offering both technical assistance and funding to enhance production capacities.

North America and Europe, with their mature markets, grapple with stringent regulatory landscapes. These regions prioritize premium applications of wood vinegar, especially in food, pharmaceuticals, and high-value agriculture. In the U.S., the FDA's GRAS framework delineates a clear path for wood vinegar's entry into food applications. Across the Atlantic, European regulations are increasingly leaning towards bio-based alternatives, sidelining synthetic chemicals. Meanwhile, South America's agricultural landscape is ripe with growth potential. Countries in the region are not only championing organic farming but are also on the lookout for sustainable substitutes to synthetic pesticides, especially as these face mounting regulatory scrutiny. With its rich biomass resources and a well-established agricultural framework, South America is poised for a robust market expansion.

- Ace (Singapore) Pte Ltd

- Nettenergy B.V.

- Tagrow Co. Ltd

- Merck KGaA

- PyroAg Pty Ltd (PyroAg)

- Byron Biochar

- Earth Systems (Green Man Char )

- NewCarbon

- Shijiazhuang Hongsen Activated Carbon Co., Ltd.

- VerdiLife Inc.

- Nara Tanka Industries Co., Ltd.

- New Life Agro

- Tex Cycle

- Xi'An Hj Herb Biotechnology Co., Ltd.

- The Green Side of the Fence Ltd

- Haiqi Environmental Protection Technology Co.,ltd.

- Sane Shell Carbon

- Aspire Renoil Associates Co

- Qingdao Re-green Biological Technology Co.,Ltd.

- Penta Fine Ingredients, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for natural food preservatives and flavor enhancers

- 4.2.2 Supportive government policies and environmental regulations

- 4.2.3 Shift toward organic and sustainable agriculture

- 4.2.4 Rising demand for bio-based pesticides

- 4.2.5 Advancements in wood vinegar production technology

- 4.2.6 Expanding use in aquaculture

- 4.3 Market Restraints

- 4.3.1 High production costs

- 4.3.2 Competition from synthetic alternatives

- 4.3.3 Low scientific validation and research

- 4.3.4 Distribution and scale-up challenges

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Production Method

- 5.1.1 Slow Pyrolysis

- 5.1.2 Intermediate Pyrolysis

- 5.1.3 Fast Pyrolysis

- 5.2 By Feedstock

- 5.2.1 Bamboo

- 5.2.2 Hardwood

- 5.2.3 Softwood

- 5.2.4 Agricultural Residues

- 5.2.5 Coconut Shells

- 5.2.6 Others

- 5.3 By Application

- 5.3.1 Agriculture

- 5.3.1.1 Crop Nutrition

- 5.3.1.2 Crop Protection

- 5.3.2 Food and Beverage

- 5.3.2.1 Canned Food

- 5.3.2.2 Sauces

- 5.3.2.3 Dairy Products

- 5.3.2.4 Other Food and Beverage Applications

- 5.3.3 Animal Feed

- 5.3.4 Pharmaceuticals

- 5.3.5 Other Applications

- 5.3.1 Agriculture

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Spain

- 5.4.2.4 France

- 5.4.2.5 Italy

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Indonesia

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Columbia

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Egypt

- 5.4.5.5 Morocco

- 5.4.5.6 Nigeria

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ace (Singapore) Pte Ltd

- 6.4.2 Nettenergy B.V.

- 6.4.3 Tagrow Co. Ltd

- 6.4.4 Merck KGaA

- 6.4.5 PyroAg Pty Ltd (PyroAg)

- 6.4.6 Byron Biochar

- 6.4.7 Earth Systems (Green Man Char )

- 6.4.8 NewCarbon

- 6.4.9 Shijiazhuang Hongsen Activated Carbon Co., Ltd.

- 6.4.10 VerdiLife Inc.

- 6.4.11 Nara Tanka Industries Co., Ltd.

- 6.4.12 New Life Agro

- 6.4.13 Tex Cycle

- 6.4.14 Xi'An Hj Herb Biotechnology Co., Ltd.

- 6.4.15 The Green Side of the Fence Ltd

- 6.4.16 Haiqi Environmental Protection Technology Co.,ltd.

- 6.4.17 Sane Shell Carbon

- 6.4.18 Aspire Renoil Associates Co

- 6.4.19 Qingdao Re-green Biological Technology Co.,Ltd.

- 6.4.20 Penta Fine Ingredients, Inc.