|

市场调查报告书

商品编码

1849827

汽车防锁死煞车系统和电子稳定控制:市场份额分析、产业趋势、统计数据和成长预测(2025-2030 年)Automotive Anti Lock Braking System And Electronic Stability Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

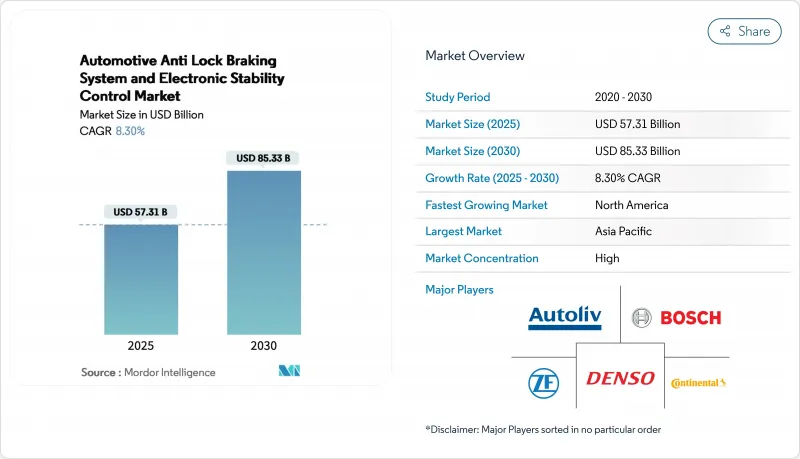

汽车防锁死系统和电子稳定控制市场规模预计在 2025 年达到 573.1 亿美元,到 2030 年达到 853.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.30%。

强制性安全法规、青睐线控刹车设计的电动平台以及全球汽车产量的稳定復苏推动了成长。欧盟 (EU)、美国、印度和中国的监管机构如今将 ABS 视为更广泛主动安全套件的基石,鼓励原始设备製造商 (OEM) 将 ABS 纳入几乎所有新车型领域。先进封装製造商正利用这些强制规定,将 ABS 与高级驾驶辅助控制器捆绑销售。随着单通道 ABS 和电动 ABS 架构的普及以及产量的不断增长,电动摩托车和纯电动车的需求成长最为迅速。

全球汽车防锁死煞车系统和电子稳定控制系统市场趋势与洞察

强制性安全法规推动全球采用ABS

诸如针对摩托车的联合国 R78 法规、美国的 FMVSS-122 法规以及印度的 AIS-150 法规等严格政策,正在推动新车 ABS 安装率达到 100%。美国国家公路交通安全管理局 (NHTSA) 已颁布法规,要求到 2029 年必须配备自动紧急煞车系统,而 ABS 是遵守的关键。欧洲已强制要求 125cc 及以上的Scooter安装 ABS,这将对高度依赖摩托车的东南亚国协产生影响。印度也正在效仿这一趋势,敦促供应商推出成本优化的单通道解决方案。联合国亚太经社会 (UN-ESCAP) 估计,摩托车 ABS 可将致命事故减少 31%,这增强了监管机构的信心。

由于全球汽车产量增加,ABS 市场正在扩大

疫情后的生产復苏在亚太地区最为明显,中国已恢復满载生产,印度摩托车产量在2024年创下历史新高。产量的成长将直接转化为对ABS的需求成长,尤其是在其从选配变为标配的背景下。博世指出,先进的ABS可以预防40%的摩托车事故,这项数据引起了消费者和政策制定者的共鸣。

成本障碍阻碍了价格敏感市场的采用

在印度、印尼和巴西,对于经济型两轮车和入门级汽车来说,ABS 的价格溢价仍然很高。由于原始设备製造商的平均利润率为 7.2%,而供应商的利润率仍接近 5.5%,因此吸收 ABS 成本的空间有限。因此,一级供应商正在重新设计液压单元以消除阀门的复杂性,采用共用ECU,并进行在地化生产,以实现可行的价格分布。

細項分析

汽车防锁死系统市场将以乘用车为主,在欧洲、中国和北美,乘用车强制安装防锁死煞车系统,到2024年将占到总销售额的47.15%。稳定的汽车需求,加上日益完善的驾驶辅助系统,确保了稳定的收益基础。预计该细分市场将随着ADAS的普及而同步成长,儘管成长速度低于摩托车市场。乘用车防锁死煞车系统市场规模预计将以8.10%的复合年增长率成长,这得益于主机厂将煞车控制与车道维持和自我调整巡航功能整合。

电动两轮车市场发展势头强劲,复合年增长率高达15.40%。在印度和欧洲,125cc以上的摩托车必须配备ABS防锁死煞车系统,这推动了比汽车解决方案更轻、更便宜的单通道架构的发展。在中国和东南亚地区流行的电动Scooter更青睐再生製动,这迫使供应商将ABS演算法与能量再生逻辑相结合。博斯预测,到2026年,骑乘援助将大规模应用于市场,这凸显了该地区对两轮车主动安全系统的需求。

到2024年,电控系统仍将是最大的零件细分市场,占总收入的33.55%,其份额受不断增长的计算需求驱动。人工智慧韧体现在可以即时解读车轮转速数据、道路摩擦係数和车辆负载,从而实现预测性煞车。此功能将推动电子控制单元(ECU)的复合年增长率预测达到12.10%,远远领先其他零件。由于能够承受摩托车和重型卡车振动的固态设计,车轮转速感测器的价值正在不断提升。

针对纯电动车,液压控制单元正面临重量和效率的重新设计,因为每公斤重量都会影响续航里程。阀门和致动器采用轻质铝外壳,并利用先进的机电一体化技术来缩短反应时间。随着人工智慧 (AI) 逐渐进入中央网域控制器,ECU 供应商纷纷提供无线更新功能以维持网路合规性,从而缓解了软体定义煞车的关键限制之一。

汽车防锁死系统市场按车辆类型(两轮车、其他)、组件(电控系统(ECU)、其他)、ABS 类型(四通道、其他)、技术(液压 ABS、其他)、最终用户(OEM 安装、其他)和地区细分。市场预测以金额(美元)和数量(单位)提供。

区域分析

受中国生产规模和印度日益严格的法规影响,亚太地区以36.55%的市占率领先汽车防锁死煞车系统市场。印度已强制要求摩托车安装ABS,这促使供应商在当地设立ECU工厂以避免进口关税。中国已强制要求乘用车安装ABS和电子稳定控制系统,促使国内一级供应商与跨国竞争对手保持同步。日本和韩国的原始设备製造商正在将ABS整合到其专有的混合动力系统中,以巩固其在该地区的技术领先地位。

到2030年,北美的复合年增长率将达到13.60%,其中美国的需求将受到即将到来的AEB法规和加拿大FMVSS标准的推动。保险公司提供的多险种折扣将推动商用车队的改装。服务出口市场的墨西哥组装厂正在预先安装ABS系统,以满足美国和欧盟的认证要求。中东/非洲和南美洲存在着规模较小但正在成长的市场,例如巴西强制所有新摩托车都安装ABS系统,沙乌地阿拉伯则为配备先进安全套件的车辆提供奖励。

欧洲受欧盟通用安全法规的驱动,该法规强制所有新车配备ABS,并将ABS纳入更广泛的AEB检验范围。德国仍然是该地区的创新中心,供应商正在试行使用基于ABS的紧急煞车数据来改善道路摩擦力测绘。 Gapwaves指出,AEB所需的附加雷达感测器可补充ABS讯号,实现冗余。东欧的组装厂正在将AEB的采用范围扩大到入门级车辆,以确保统一的安全标准。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 强制性安全法规(UN R78、FMVSS-122、AIS-150)

- 新冠疫情过后,全球乘用车和摩托车产量呈上升趋势

- 扩大配备主动安全功能的车辆的保险奖励

- 需要整合线传煞车的电动平台

- 二手车队转换为基于远端资讯处理的UBI的需求激增

- 捆绑 ABS 和 ADAS 网域控制站的一级供应商

- 市场限制

- 新兴市场的价格分布摩托车和汽车的 BOM 成本较高

- 与传统液压架构整合的复杂性

- 2023年以后半导体供应链的限制

- 软体定义煞车的网路安全认证延迟

- 价值链/供应链分析

- 监管格局

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模和成长预测(价值(美元)和数量(单位))

- 按车辆类型

- 摩托车

- 搭乘用车

- 轻型商用车

- 中型和重型商用车

- 按组件

- 电控系统(ECU)

- 液压控制单元

- 车轮转速感知器

- 阀门和致动器

- 按ABS类型

- 4通道

- 3个通道

- 单通道(摩托车)

- 依技术

- 液压ABS

- 电动ABS

- 气动ABS

- 按最终用户

- OEM相容

- 售后改装

- 按地区

- 北美洲

- 美国

- 加拿大

- 其他北美地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 中东和非洲

- 土耳其

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- DENSO Corporation

- Mando Corporation

- Hyundai Mobis Co., Ltd.

- Hitachi Astemo, Ltd.

- Brembo SpA

- Knorr-Bremse AG

- WABCO(ZF CVCS)

- Haldex AB

- Nissin Kogyo Co., Ltd.

- ADVICS Co., Ltd.

- Aptiv PLC

- Delphi Technologies(BorgWarner)

- Veoneer Holding LLC

- Autoliv Inc.

- BWI Group

- Maruichi Machine

- Federal-Mogul Motorparts

第七章 市场机会与未来展望

The Automotive Anti Lock Braking System And Electronic Stability Control Market size is estimated at USD 57.31 billion in 2025, and is expected to reach USD 85.33 billion by 2030, at a CAGR of 8.30% during the forecast period (2025-2030).

Growth is anchored in mandatory safety regulations, electrified platforms that favor brake-by-wire designs, and the steady rebound of global vehicle production. Regulators in the European Union, the United States, India, and China now regard ABS as foundational to wider active-safety suites, prompting OEMs to embed ABS into virtually every new vehicle segment. Suppliers are capitalizing on these mandates by bundling ABS with advanced driver assistance controllers, while insurers reward fleets and consumers that opt for active-safety packages. Alongside rising production volumes, electric two-wheelers and battery electric cars are creating the fastest incremental demand as single-channel and electric ABS architectures gain popularity.

Global Automotive Anti Lock Braking System And Electronic Stability Control Market Trends and Insights

Mandatory Safety Regulations Driving Global ABS Adoption

Stringent policies such as UN R78 for motorcycles, FMVSS-122 in the United States, and AIS-150 in India are pushing ABS fitment toward 100% in new vehicles. The U.S. National Highway Traffic Safety Administration's rule requiring automatic emergency braking by 2029 makes ABS core to achieving compliance. Europe already enforces motorcycle ABS on scooters above 125 cc, influencing ASEAN nations that rely heavily on two-wheelers. India mirrored this trend, compelling suppliers to release cost-optimized single-channel solutions. UN ESCAP estimates that motorcycle ABS can cut fatalities by 31% unescap.org, reinforcing regulators' confidence.

Rising Global Vehicle Production Expanding ABS Market Footprint

Post-pandemic manufacturing recovery is most pronounced in Asia Pacific, where China returned to full-scale capacity and India's two-wheeler output set new highs in 2024. Increased unit volumes translate directly into greater ABS demand, especially as ABS migrates from optional to standard equipment. Bosch notes that advanced ABS can prevent 40% of two-wheeler crashes, a statistic resonating with consumers and policymakers.

Cost Barriers Limiting Penetration in Price-Sensitive Markets

ABS price premiums remain challenging for low-cost motorcycles and entry-level cars in India, Indonesia, and Brazil, where a few USD can sway purchase decisions. OEM margins average 7.2%, while suppliers hover near 5.5%, limiting room to absorb ABS costs. Tier-1 vendors therefore re-engineer hydraulic units to remove valving complexity, adopt shared ECUs, and localize production to achieve viable price points.

Other drivers and restraints analyzed in the detailed report include:

- Growing Insurance Incentives for Active-Safety Equipped Vehicles

- Electrification Platforms Transforming ABS Architecture

- Semiconductor Supply Constraints Impacting Production Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars anchored the automotive anti-lock braking system market in 2024, delivering 47.15% revenue thanks to mandatory fitment in Europe, China, and North America. Stable car demand, paired with increasingly sophisticated driver assistance packages, ensures a consistent revenue base. The segment will grow in tandem with ADAS penetration, though at a slower pace than two-wheelers. The automotive anti-lock braking system market size for passenger cars is projected to expand at 8.10% CAGR, supported by OEM integration of brake control with lane-keeping and adaptive cruise functions.

Electric two-wheelers inject faster momentum at 15.40% CAGR. Mandates in India and Europe require ABS on motorcycles above 125 cc, propelling single-channel architectures that weigh and cost less than four-wheel solutions. Electric scooters popular in China and Southeast Asia favor regenerative braking, forcing suppliers to fuse ABS algorithms with energy-recovery logic. Bosch forecasts mass-market rider assistance deployment by 2026, underscoring regional appetite for active safety on two-wheelers.

Electronic control units remained the largest component segment in 2024 at 33.55% revenue, a share lifted by rising computational needs. AI firmware now interprets wheel-speed data, road friction coefficients, and vehicle load in real time, enabling predictive braking. This functionality drives a 12.10% CAGR outlook for ECUs, well ahead of other components. Wheel-speed sensors follow in value, benefiting from solid-state designs that withstand vibration on two-wheelers and heavy trucks.

Hydraulic control units face weight and efficiency redesigns for battery electric vehicles, where every kilogram impacts range. Valves and actuators exploit lightweight aluminum housings and advances in mechatronics to cut response times. As AI moves onto central domain controllers, ECU suppliers adapt by offering over-the-air update capabilities to maintain cyber compliance, mitigating one of the key restraints on software-defined braking.

The Automotive Anti-Lock Braking System Market is Segmented by Vehicle Type (Two-Wheelers, and More), Component (Electronic Control Unit (ECU), and More), ABS Type (4-Channel, and More), Technology (Hydraulic ABS, and More), End User (OEM-Fitment, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific leads the automotive anti-lock braking system market with 36.55% market share, propelled by China's production scale and India's regulatory surge. India's ABS mandate on motorcycles is growing significantly, with suppliers establishing local ECU plants to avoid import tariffs. China pairs ABS with compulsory electronic stability control on passenger cars, keeping domestic tier-1 suppliers in lockstep with multinational competitors. Japanese and South Korean OEMs integrate ABS with proprietary hybrid systems, sharpening regional technology leadership.

North America expands at highest CAGR at 13.60% by 2030, with U.S. demand buoyed by upcoming AEB rules and Canada aligning with FMVSS standards. Commercial fleet retrofits gain traction where insurers offer multiline discounts. Mexico's assembly plants, serving export markets, pre-install ABS to satisfy both U.S. and EU homologation. Smaller yet growing markets in the Middle East, Africa, and South America witness Brazil mandating ABS on all new motorcycles, and Saudi Arabia incentivizing fleets that adopt advanced safety packages.

Europe follows, underpinned by the EU General Safety Regulation that obliges ABS on all new vehicles and positions it within broader AEB validation. Germany remains the region's innovation hub, with suppliers piloting ABS-based harsh-brake data to improve road-friction mapping. Gapwaves notes that extra radar sensors required for AEB complement ABS signals for redundancy. Eastern European assembly plants extend adoption to entry-level cars, ensuring uniform safety standards.

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- DENSO Corporation

- Mando Corporation

- Hyundai Mobis Co., Ltd.

- Hitachi Astemo, Ltd.

- Brembo S.p.A.

- Knorr-Bremse AG

- WABCO (ZF CVCS)

- Haldex AB

- Nissin Kogyo Co., Ltd.

- ADVICS Co., Ltd.

- Aptiv PLC

- Delphi Technologies (BorgWarner)

- Veoneer Holding LLC

- Autoliv Inc.

- BWI Group

- Maruichi Machine

- Federal-Mogul Motorparts

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory safety regulations (UN R78, FMVSS-122, AIS-150)

- 4.2.2 Rising global passenger-car & 2-wheeler production rebounding post-COVID

- 4.2.3 Growing insurance incentives for active-safety equipped vehicles

- 4.2.4 Electrification platforms requiring brake-by-wire integration

- 4.2.5 Rapid retrofit demand in used-vehicle fleets for telematics-based UBI

- 4.2.6 Tier-1 suppliers bundling ABS with ADAS domain controllers

- 4.3 Market Restraints

- 4.3.1 High BOM cost for low-end 2-wheelers & emerging-market cars

- 4.3.2 Integration complexity with legacy hydraulic architectures

- 4.3.3 Semiconductor supply-chain constraints post-2023

- 4.3.4 Cyber-security certification delays for software-defined braking

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Two-Wheelers

- 5.1.2 Passenger Cars

- 5.1.3 Light Commercial Vehicles

- 5.1.4 Medium and Heavy Commercial Vehicles

- 5.2 By Component

- 5.2.1 Electronic Control Unit (ECU)

- 5.2.2 Hydraulic Control Unit

- 5.2.3 Wheel Speed Sensors

- 5.2.4 Valves & Actuators

- 5.3 By ABS Type

- 5.3.1 4-Channel

- 5.3.2 3-Channel

- 5.3.3 Single-Channel (Motorcycle)

- 5.4 By Technology

- 5.4.1 Hydraulic ABS

- 5.4.2 Electric ABS

- 5.4.3 Pneumatic ABS

- 5.5 By End User

- 5.5.1 OEM-Fitment

- 5.5.2 Aftermarket Retrofit

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Turkey

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 DENSO Corporation

- 6.4.5 Mando Corporation

- 6.4.6 Hyundai Mobis Co., Ltd.

- 6.4.7 Hitachi Astemo, Ltd.

- 6.4.8 Brembo S.p.A.

- 6.4.9 Knorr-Bremse AG

- 6.4.10 WABCO (ZF CVCS)

- 6.4.11 Haldex AB

- 6.4.12 Nissin Kogyo Co., Ltd.

- 6.4.13 ADVICS Co., Ltd.

- 6.4.14 Aptiv PLC

- 6.4.15 Delphi Technologies (BorgWarner)

- 6.4.16 Veoneer Holding LLC

- 6.4.17 Autoliv Inc.

- 6.4.18 BWI Group

- 6.4.19 Maruichi Machine

- 6.4.20 Federal-Mogul Motorparts

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

汽车防锁死煞车系统市场(按组件、车辆类型、类型和分销管道)—全球预测 2025-2032防锁死煞车系统 (ABS) 市场按车辆类型、系统、感测器、技术和分销管道划分 - 全球预测 2025-2032 年防锁死煞车系统和电子稳定控制系统市场按销售管道、车辆类型、系统类型、驱动方式和通道数量划分-全球预测,2025-2032年

汽车防锁死煞车系统市场(按组件、车辆类型、类型和分销管道)—全球预测 2025-2032防锁死煞车系统 (ABS) 市场按车辆类型、系统、感测器、技术和分销管道划分 - 全球预测 2025-2032 年防锁死煞车系统和电子稳定控制系统市场按销售管道、车辆类型、系统类型、驱动方式和通道数量划分-全球预测,2025-2032年 全球乘用车ABS马达电路市场

全球乘用车ABS马达电路市场 防锁死煞车系统 (ABS) 市场报告,按组件类型(速度感知器、电子控制单元 (ECU)、液压单元)、车辆类型(两轮车、乘用车、商用车)、最终用途(OEM、更换需求)和地区划分,2025 年至 2033 年

防锁死煞车系统 (ABS) 市场报告,按组件类型(速度感知器、电子控制单元 (ECU)、液压单元)、车辆类型(两轮车、乘用车、商用车)、最终用途(OEM、更换需求)和地区划分,2025 年至 2033 年 2025年全球汽车防锁死煞车系统与电子稳定控制系统市场报告汽车速度编码器市场:按产品类型、材料、技术、输出讯号、应用、车辆类型、销售管道- 2025-2030 年全球预测防锁死剂市场:按产品类型、ABS 零件、最终用户、汽车类型、技术类型、应用、分销管道、销售管道- 2025-2030 年全球预测

2025年全球汽车防锁死煞车系统与电子稳定控制系统市场报告汽车速度编码器市场:按产品类型、材料、技术、输出讯号、应用、车辆类型、销售管道- 2025-2030 年全球预测防锁死剂市场:按产品类型、ABS 零件、最终用户、汽车类型、技术类型、应用、分销管道、销售管道- 2025-2030 年全球预测 汽车用ABS零件的全球市场规模:各产品,各用途,各地区,范围及预测防锁死煞车系统 (ABS) 市场、机会、成长动力、产业趋势分析与预测,2024-2032 年

汽车用ABS零件的全球市场规模:各产品,各用途,各地区,范围及预测防锁死煞车系统 (ABS) 市场、机会、成长动力、产业趋势分析与预测,2024-2032 年