|

市场调查报告书

商品编码

1849854

动物生长促进剂:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Animal Growth Promoters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

预计到 2025 年,动物生长促进剂市场规模将达到 194 亿美元,到 2030 年将达到 265 亿美元,预测期内复合年增长率为 6.40%。

这一强劲的发展趋势反映了畜牧业向功能性营养的转变,这种转变既能维护动物健康,又能减少生产对环境的影响。消费者对无抗生素肉类的需求不断增长,主要出口中心的监管日益严格,以及亚太地区持续的蛋白质需求,都为生产商创造了更大的商业性。传统蛋白质饲料价格压力不断加大,促使人们关注酵素製剂和益生菌,因为它们能从每公斤饲料中提取更多营养。工厂内部数位化,特别是人工智慧驱动的微量添加技术,能够消除浪费,并使添加剂用量与动物的即时需求相匹配,即使原材料成本飙升,也能保障净利率。向碳中和农业转型的势头进一步提升了生物解决方案(例如基于芽孢桿菌的益生菌)的价值,这些解决方案兼具性能优势和永续性。

全球动物生长促进剂市场趋势及洞察

全球对不含抗生素肉类的需求激增

零售商和快餐店越来越倾向于使用无抗生素供应链,这促使全球生产商投资研发能够维持动物生长性能的天然替代品。这一趋势在禽肉和猪肉产业尤其明显,无抗生素标籤能够提升产品的市场竞争力。欧盟对抗菌生长促进剂的禁令已树立了明确的标桿,北美杂货商对认证产品提供15%至25%的溢价。因此,在监管和消费者支付意愿的双重推动下,动物生长促进剂市场的需求底线稳定。

大规模畜牧养殖及提高产量,重点提升饲料效率

亚太和南美洲的大型畜牧生产商正致力于降低饲料转换率,以抵消谷物价格波动的影响。目前,生产商的目标是将肉鸡的饲料转换率控制在2.0以下,猪的饲料转换率控制在2.5以下,他们透过使用能将营养物质消化率提高3-5%的酵素製剂以及能将饲料需求降低2-4%的益生菌菌株来实现这一以金额为准。

饲料用有机酸的价格波动

受天然气价格上涨和少数大型工厂计画外停产的影响,甲酸成本在2024年之前波动了40%至60%。丙酸基准价格飙升至多年来的最高点,导致饲料厂利润率下降,迫使饲料厂减少发行或转向更便宜的替代品。对于没有长期合约的小型饲料厂而言,这种价格波动将降低其对优质添加剂的需求,暂时抑制动物生长促进剂市场的扩张。

细分市场分析

益生菌产品,尤其是芽孢桿菌和乳酸桿菌,因其能持续提高饲料转换率和肠道健康而得到广泛检验,预计到2024年将占全球销售额的34.5%。这一领先地位巩固了动物生长促进剂市场的整体格局,因为一体化生产商已将多菌株菌群应用于饲料的各个阶段,以弥补动物生长促进剂退出市场的影响。庞大的用户群推动了能够耐受製粒温度的产孢菌株的研发,进一步拓展了益生菌的应用范围。植物性添加剂市场规模已达5亿美元,预计其复合年增长率将达到9.4%,超过其他所有类别,主要得益于天然色素、抗氧化剂和抗菌剂的功效符合洁净标示的要求。酵素製剂因其耐热设计(能够承受製粒高温)而持续吸引投资,这些酵素製剂能够释放低等级谷物中经常流失的营养成分。同时,酸味剂依然强劲,尤其是在饲料腐败风险较高的热带地区。

植物源性增效剂的发展动能也正扩展到复方产品领域,这些产品利用精油和有机酸的协同作用,提供比单独使用任何一种化合物都更强的病原体抑制效果。这种趋势在猪和家禽养殖业中最为显着,因为这些领域疾病压力和抗生素抑製作用相互交织。益生元作为辅助成分,能够滋养肠道菌群并促进益生菌定植,其应用也日益广泛。抗生素和离子载体的使用量正在下降,但在监管不严格的地区仍然具有一定的意义。动物生长促进剂市场正持续转型为生物或植物来源产品。随着数据的积累,即使是较保守的反刍动物养殖场也开始采用植物来源混合物,以减少甲烷排放,满足即将到来的碳排放审核要求。商业公司正在积极回应,推广无溶剂萃取方法,以确保活性成分含量的稳定性,同时满足环保要求。

到2024年,鸡肉销售额将占总销售额的37.5%,这反映了该品类在全球范围内的受欢迎程度及其对营养成分微调的应对力。由于抗生素使用受限,养殖企业正在投资动物生长促进剂以维持动物生长,而先进的配方已被证实能够使大规模商业养殖场的鸡群死亡率降低4-6%。随着人工智慧驱动的肉鸡管理平台能够根据感测器数据设定添加剂用量,预计其使用量将进一步成长。水产养殖业将以8.6%的复合年增长率快速成长,这主要得益于鱼粉成本的上涨以及对永续水产饲料的需求。东南亚的虾农在引入益生菌和酵素製剂混合饲料后,饲料转换率提高了6-8%,显示该领域取得了商业性成功。

养猪户在动物生长促进剂市场占据重要份额,他们采用分阶段饲餵方案,利用酸化剂减少断奶后腹泻,并利用酵素从高纤维饲粮中提取能量。反刍动物对甲烷减量化合物(例如博沃)的需求稳定,博沃于2024年12月获得英国新批准。马、宠物和特种动物等特殊领域虽然消费量较低,但利润率较高,因为养殖户追求功能性强、符合人类食用标准的原料。各物种的养殖整合商都在寻求投资回报率的证明,这促使供应商创建田间数据仪錶盘,将添加剂的制度与动物的生长和健康状况联繫起来。

区域分析

预计到2024年,亚太地区将占全球销售额的41.6%,复合年增长率接近8%,巩固其作为动物生长促进剂市场中心的地位。中国领先的一体化企业正积极响应其出口目标,承诺不使用抗生素,从而推动益生菌和酵素製剂的快速普及。光是北京赛拓生技有限公司预计到2024年益生菌收入就将累计3.0279亿元人民币(约4,213万美元),凸显了中国的生产能力。印度不断壮大的中产阶级推动了对鸡肉和鸡蛋的需求,同时政府推广计划鼓励农民减少抗生素的使用,这为植物性和有机酸类产品提供了天然的利好因素。东南亚水产养殖业正在释放新的生产潜力,泰国和越南正在迅速部署池塘感测器,透过讯号进行自适应给药,以提高鱼类存活率并影响全球水产品供应。

北美仍然是技术的试验场,因为严格的客户规格贯穿整个肉类价值链。美国的人工授精加工厂会根据玉米的进料品质和肉鸡的增重预测,逐班调整添加剂的使用方案。加拿大育肥场经营者正在采用减少甲烷排放的添加剂,以应对日益严格的碳排放法规,从而保持出口竞争力。儘管畜群成长缓慢,但每头动物的添加剂支出却在增加,这推动了动物生长促进剂市场在北美地区的价值成长。

成熟但监管严格的欧洲继续禁止使用抗菌生长促进剂,同时鼓励使用天然解决方案。德国率先使用农场感测器,将饲料转换率的提高与酵素混合物直接关联起来,提供细緻的证据,从而促进重复购买。法国和西班牙支持有机农业,推动了对不使用化学溶剂的标准化植物油的需求。东欧正在迅速追赶,对其饲料基础设施进行现代化改造,并将添加剂的使用纳入欧盟可追溯性要求,作为合规通讯协定的一部分。儘管牲畜数量趋于稳定,但这些因素的汇聚正在稳步推动整个动物生长促进剂市场的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场驱动因素

- 全球对不含抗生素肉类的需求激增

- 更重视大规模畜牧生产和饲料效率

- 益生菌的生产成本与离子载体相当。

- 后生元肠道微生物群突破改善生长性能

- 碳中和生物反应器技术显着降低了芽孢桿菌的生产成本。

- 人工智慧驱动的饲料厂精准微量投药

- 市场限制

- 饲料用有机酸价格波动

- 全球AGP法规正在迅速演变

- 益生菌发酵级糖供应瓶颈

- 霉菌毒素交互作用导致添加剂功效降低

- 监管环境

- 技术展望

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 益生菌

- 益生元

- 植物来源成分

- 氧化剂

- 酵素

- 抗生素

- 其他类型(离子载体、荷尔蒙)

- 依动物类型

- 家禽

- 猪

- 反刍动物

- 水产养殖

- 其他动物(马、宠物)

- 按形式

- 干燥

- 液体

- 按原料

- 细菌

- 酵母菌

- 真菌

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 亚太其他地区

- 中东

- 土耳其

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- DSM-Firmenich

- Cargill, Inc.

- Vetoquinol

- Alltech

- Kemin Industries

- Huvepharma

- Novonesis

- BASF SE

- ADM

- Evonik Industries

- Adisseo

- Phibro Animal Health

- Virbac

- Nutreco

第七章 市场机会与未来展望

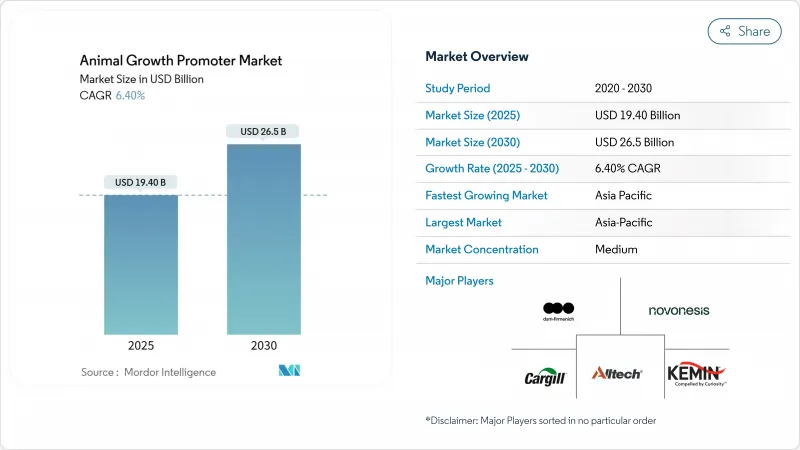

The Animal Growth Promoter Market size is estimated at USD 19.40 billion in 2025 and is anticipated to reach USD 26.5 billion by 2030, at a CAGR of 6.40% during the forecast period.

This solid trajectory mirrors the livestock sector's transition toward functional nutrition that keeps animals healthy while trimming the environmental impact of production. Rising consumer insistence on antibiotic-free meat, stricter regulations across major export hubs, and sustained protein demand in Asia-Pacific collectively widen commercial headroom for manufacturers. Intensifying price pressure on traditional protein meals amplifies interest in enzymes and probiotics that unlock more nutrients from every kilogram of feed. Digitalization inside mills, especially AI-enabled micro-dosing, reduces waste and aligns additive inclusion rates with real-time animal needs, preserving margins even when raw-material costs swing sharply. Momentum toward carbon-neutral farming further elevates biological solutions such as Bacillus-based probiotics that deliver both performance and sustainability benefits.

Global Animal Growth Promoters Market Trends and Insights

Global Antibiotic-Free Meat Demand Boom

Retailers and quick-service restaurants now stipulate antibiotic-free supply chains, prompting producers worldwide to invest in natural alternatives that preserve growth performance. This trend is especially strong in the poultry and swine sectors, where antibiotic-free labeling boosts marketability. EU prohibitions on antimicrobial growth promoters have already shown a clear template, and North American grocers offer premiums of 15-25% for certified products. The animal growth promoters market, therefore, gains a steady demand floor from both regulation and consumer willingness to pay.

Intensifying Large-Scale Livestock Production and Feed Efficiency Focus

Mega farms in Asia-Pacific and South America aim for ever-lower feed conversion ratios to offset volatile grain prices. Producers now target sub-2.0 FCR in broilers and sub-2.5 in swine by leveraging enzymes that lift nutrient digestibility by 3-5% and targeted probiotic strains that shave 2-4% off feed needs. With global feed output dipping 0.2% to 1.29 billion metric tons in 2024, efficiency gains, not tonnage, will fuel growth. These imperatives reinforce premium demand for advanced solutions and expand the animal growth promoters market in value terms.

Feed-Grade Organic-Acid Price Volatility

Formic-acid costs swung 40-60% in 2024, influenced by natural gas price spikes and unplanned shutdowns at a handful of large plants. Propionic-acid benchmarks climbed to multi-year highs, eroding feed-mill margins and prompting ration cuts or cheaper substitutes. For small mills without long-term contracts, this instability dampens the appetite for premium inclusions and temporarily tempers the animal growth promoters' market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Probiotic Manufacturing Cost-Parity with Ionophores

- Postbiotic Gut-Microbiome Breakthroughs Boosting Growth Performance

- Rapidly Evolving Global AGP Regulatory Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Probiotics generated 34.5% of global revenue in 2024, supported by robust validation of Bacillus and Lactobacillus strains that consistently enhance feed efficiency and gut health. This leadership bolsters the overall animal growth promoters market, as integrated producers increasingly blend multi-strain consortia into every diet phase to offset AGP withdrawal. The sizable installed base encourages Research and Development into spore-forming variants that can withstand pelleting temperatures, further widening use cases. The phytogenic niche, already a USD 500 million category, advances at a forecast 9.4% CAGR, outpacing all other groups thanks to natural coloration, antioxidative, and antimicrobial benefits that dovetail with clean-label demands. Enzymes continue to draw investment because thermostable designs survive high-temperature pelleting, unlocking otherwise lost nutrients in lower-grade grains. Meanwhile, acidifiers hold steady, especially in tropical climates where feed spoilage risk is acute.

Momentum in phytogenics spills into combinatory products that tap the synergistic effects of essential oils plus organic acids, delivering stronger pathogen suppression than either class alone. Adoption is strongest in swine and poultry, where disease pressure and antibiotic curbs converge. Prebiotics gain traction as companion ingredients that nourish resident microbiota and reinforce probiotic colonization. Antibiotics and ionophores retreat but remain present in regions lacking strict rules. The animal growth promoters market continues its pivot toward biological or plant-derived variants. As data accumulate, even conservative ruminant operations adopt phytogenic blends seeking methane mitigation to meet upcoming carbon audits. Commercial players respond by scaling solvent-free extraction methods, ensuring consistent active compound loads while meeting environmental expectations.

Poultry captured 37.5% of 2024 revenue, reflecting the category's global popularity and responsiveness to nutritional fine-tuning. Integrators invest in animal growth promoters to maintain growth despite antibiotic limits, and advanced formulations are credited with lowering flock mortality by 4-6% in large commercial setups. Usage intensity is poised to deepen as AI-assisted broiler management platforms prescribe additive inclusion rates based on sensor data. Aquaculture expands fastest at an 8.6% CAGR, driven by escalating fishmeal costs and the push for sustainable aquatic diets. As shrimp farmers in Southeast Asia integrate probiotic and enzyme blends, they report feed conversion improvements of 6-8%, underlining the segment's commercial payoff.

Swine producers adopt phase-feeding programs where acidifiers curb post-weaning diarrhea, and enzymes unlock energy from high-fiber rations, sustaining a solid share of the animal growth promoters market. Ruminants contribute a stable demand for methane-reducing compounds such as Bovaer, newly cleared for UK use in December 2024. Specialty segments, horses, pets, and niche exotics-consume small volumes yet deliver premium margins because owners seek functional, human-grade ingredients. Across species, integrators demand proof of ROI, spurring suppliers to produce field-data dashboards that link additive regimes to growth and health outcomes.

The Animal Growth Promoters Market Report is Segmented by Type (Probiotics, Prebiotics, Phytogenics, Acidifiers, and More), by Animal Type (Poultry, Swine, Ruminants, Aquaculture, and Others), by Form (Dry and Liquid), by Source (Bacterial, Yeast, and Fungal), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 41.6% of global revenue in 2024 and is projected to grow near 8% CAGR, securing its role as the epicenter of the animal growth promoters market. China's large integrators commit to antibiotic-free pledges aligned with export ambitions, driving steep adoption of probiotics and enzymes. Beijing Scitop Bio-tech alone posted CNY 302.79 million (USD 42.13 million) in probiotic revenue during 2024, underscoring domestic capacity. India's rising middle class promotes chicken and egg demand, while government extension programs teach farmers to curb antibiotic use, creating natural tailwinds for phytogenic and organic-acid categories. Southeast Asian aquaculture unlocks new volumes, with Thailand and Vietnam rapidly installing in-pond sensors that cue adaptive additive dosing, boosting fish survival rates and shading global seafood supplies.

North America remains a technology testbed as stringent customer specifications filter through the meat value chain. AI-linked mills in the United States adjust additive regimens every shift based on incoming corn quality and broiler weight-gain forecasts. Feedlot operators in Canada adopt methane-reduction additives in anticipation of stricter carbon rules, preserving export competitiveness. Although livestock headcounts grow slowly, per-animal additive spending trends upward, reinforcing regional value growth inside the animal growth promoters market.

Europe, a mature but highly regulated arena, continues to ban antimicrobial growth promoters while incentivizing natural solutions. Germany spearheads on-farm sensor usage that links feed conversion gains directly to enzyme cocktails, providing granular proof that fuels repeat purchases. France and Spain champion organic rearing, pushing demand for standardized phytogenic oils free from chemical solvents. Eastern Europe catches up quickly, modernizing feed infrastructure and integrating EU traceability mandates, which embed additive usage as part of compliance protocols. These converging forces keep Europe a steady contributor to the overall animal growth promoters market expansion despite flat livestock numbers.

- DSM-Firmenich

- Cargill, Inc.

- Vetoquinol

- Alltech

- Kemin Industries

- Huvepharma

- Novonesis

- BASF SE

- ADM

- Evonik Industries

- Adisseo

- Phibro Animal Health

- Virbac

- Nutreco

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Global antibiotic-free meat demand boom

- 4.1.2 Intensifying large-scale livestock production and feed efficiency focus

- 4.1.3 Probiotic manufacturing cost-parity with ionophores

- 4.1.4 Postbiotic gut-microbiome breakthroughs boosting growth performance

- 4.1.5 Carbon-neutral bioreactor technologies slashing Bacillus costs

- 4.1.6 AI-driven precision micro-dosing in feed mills

- 4.2 Market Restraints

- 4.2.1 Feed-grade organic-acid price volatility

- 4.2.2 Rapidly evolving global AGP regulatory restrictions

- 4.2.3 Fermentation-grade sugar supply bottlenecks for probiotics

- 4.2.4 Mycotoxin interactions reducing additive efficacy

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Porters Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Type (Value)

- 5.1.1 Probiotics

- 5.1.2 Prebiotics

- 5.1.3 Phytogenics

- 5.1.4 Acidifiers

- 5.1.5 Enzymes

- 5.1.6 Antibiotics

- 5.1.7 Other Types (Ionophores, Hormones)

- 5.2 By Animal Type (Value)

- 5.2.1 Poultry

- 5.2.2 Swine

- 5.2.3 Ruminants

- 5.2.4 Aquaculture

- 5.2.5 Other Animals (Equine, Pets)

- 5.3 By Form (Value)

- 5.3.1 Dry

- 5.3.2 Liquid

- 5.4 By Source (Value)

- 5.4.1 Bacterial

- 5.4.2 Yeast

- 5.4.3 Fungal

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 DSM-Firmenich

- 6.4.2 Cargill, Inc.

- 6.4.3 Vetoquinol

- 6.4.4 Alltech

- 6.4.5 Kemin Industries

- 6.4.6 Huvepharma

- 6.4.7 Novonesis

- 6.4.8 BASF SE

- 6.4.9 ADM

- 6.4.10 Evonik Industries

- 6.4.11 Adisseo

- 6.4.12 Phibro Animal Health

- 6.4.13 Virbac

- 6.4.14 Nutreco