|

市场调查报告书

商品编码

1849861

WiGig:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)WiGig - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

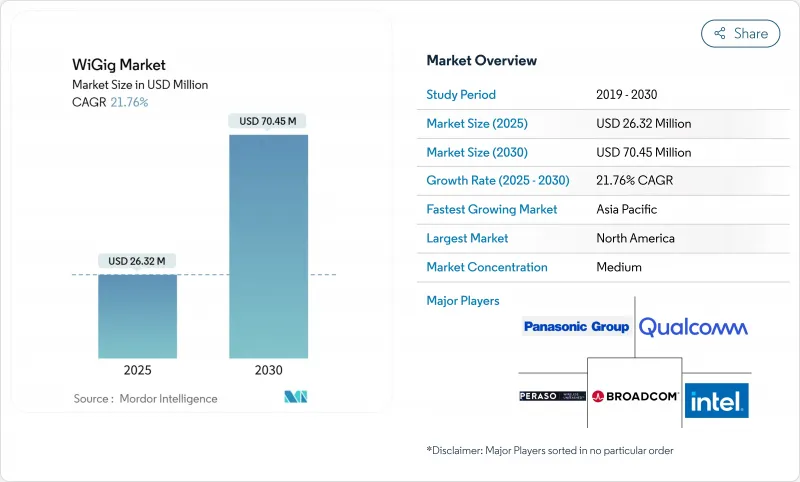

预计到 2025 年,WiGig 市场规模将达到 263.2 亿美元,到 2030 年将达到 704.5 亿美元,在此期间的复合年增长率为 21.76%。

商业性动能正从小众无线扩充座转向广泛整合到Wi-Fi 7三频存取点、高阶笔记型电脑和早期6G回程传输试验。对4K/8K视讯、AR/VR工作负载和边缘AI流量的需求正在使2.4 GHz和5/6 GHz频段的容量捉襟见肘,因此60 GHz吞吐量对于对延迟敏感的应用至关重要。同时,半导体供应商正透过系统晶片)解决方案简化设计週期,这些方案在降低功耗的同时缩小了尺寸——这是智慧型手机和超薄笔记型电脑的先决条件。最后,政策和技术都将影响WiGig市场的发展轨迹,因为围绕镓供应的地缘政治压力和不同的区域功率上限规则正在促使原始设备製造商(OEM)认证第二供应商,并促使监管机构协调60 GHz框架。

全球WiGig市场趋势与洞察

4K/8K 和 XR 串流媒体的需求激增

超高清内容需要持续的 25–100 Mbps 单流频宽,而现今家庭用户往往同时运行 4K、8K 和 AR 应用。 60 GHz 频段提供了余量,弥补了 2.4 GHz 和 5/6 GHz 频段在流量干扰和通道频宽限制方面的不足。在北美和日本,付费电视业者已经开始捆绑 8K 体育赛事直播,这进一步挑战了传统 Wi-Fi 的效能极限。因此,设备 OEM 厂商正在整合多Gigabit无线电模组,以使高阶电视、主机和耳机能够在无需有线连接的情况下保持低于 10 毫秒的延迟。随着 XR 耳机在企业培训和消费级游戏中的普及,可靠的无线吞吐量成为一项重要的购买标准,直接扩大了 WiGig 的潜在市场。

将60GHz三频无线电整合到Wi-Fi 7 AP中

网路基地台供应商正在推出将 2.4 GHz、5/6 GHz 和 60 GHz 频段整合到单一平台的 Wi-Fi 7 晶片组。多链路操作可即时遍历会话,使近距离装置能够跃升至 60 GHz 频段,而远距离用户端则保持在较低频宽。这种架构降低了密集园区内的布线成本,并透过优化频宽管理的网路分析工具提高了软体收入。一家部署了 10 Gbps 光纤上行链路的欧洲云端办公室正在使用三频 Wi-Gig 来应对尖峰时段拥塞,这凸显了基础设施融合如何将 Wi-Gig 从一项豪华附加元件转变为基本配置。

射程有限且视线不佳

在 60 GHz 频段,氧气吸收和墙壁衰减会将链路距离限制在约 10 米,这意味着需要在每个会议室和工厂单元安装接入点。即使是玻璃隔间也会使吞吐量减半,而人员移动会引入衰落,需要波束追踪演算法。自动驾驶车辆的现场测试表明,当小型障碍物破坏菲涅尔区时,封包遗失会急剧上升,这进一步凸显了 WiGig 部署需要进行精确的现场勘测。这些限制使得该技术只能应用于高密度场所和固定设置,从而限制了消费者的接受度,并削弱了 WiGig 在大众市场家用路由器领域的市场潜力。

细分市场分析

到2024年,显示设备将占WiGig市场份额的46.0%,这意味着在可预见的未来,无线显示器、扩充座和AR/ VR头戴装置仍将是主要的收入来源。这个细分市场受益于家庭用户对整洁游戏角落的需求以及办公室向共享办公室布局的转型。配备双4K萤幕和SSD级週边周边设备的无线集线器已出现在高阶企业套装中,这体现了WiGig在新建专案中相对于USB-C线缆的优势,因为它具有一次设计、多次部署的高效性。 AR/ VR头戴装置製造商正在采用60GHz频段以避免令人不适的延迟,而即将到来的混合实境技术将进一步推动这一趋势。电视和投影机正在整合WiGig技术,以便在客厅内传输未压缩的8K视讯串流,但由于即使在隔着一堵墙的情况下也可能出现讯号接收损失,因此WiGig的普及速度较为缓慢。

网路基础设施设备是成长最快的细分市场,复合年增长率高达 28.40%,主要得益于 Wi-Fi 7 三频网路基地台货量与企业更新週期同步成长。工厂中的边缘运算节点现在利用 60GHz回程传输来避免光纤沟槽,从而将安装前置作业时间缩短高达 70%。市政资讯亭供应商正在尝试使用 60GHz 无线电模组,为人口密集的市中心走廊提供临时宽频服务,而光纤计划在这些区域需要数月的钻孔许可。早期指标显示,在视距范围内链路可用性超过 99%,这表明回程传输可以成为 WiGig 的一个利润丰厚的邻近市场。

到2024年,系统晶片)设计将占据WiGig市场58.0%的份额,预计到2030年将以23.0%的复合年增长率成长。整合晶粒整合了基频、射频前端和电源管理,可将基板面积减少高达30%,并延长智慧型手机电池续航力。随着代工厂不断完善3奈米製程及其子节点,添加60GHz模组的增量成本将会降低,进而加快中阶设备的整合速度。高通最新的平台将WiGig、6GHz Wi-Fi、蓝牙低功耗音讯和5G无线电整合在单一基板上,将供应商认证週期从季度缩短至几週。

当传统基板需要即插即用的模组,或工业设备需要坚固耐用的封装时,分离式积体电路方案仍然适用。例如,无需重新设计整个主机板,即可为医疗成像推车加装 60 GHz 的网卡。英特尔的 18A蓝图同时涵盖单片式和基于模组的架构,使 OEM 厂商能够将高效能 CPU 核心与专用无线模组结合。 SoC 的便利性和分离式装置的灵活性之间的平衡,应能平衡创新风险,并支持 WiGig 市场的持续扩张。

WiGig 市场报告按产品(显示设备、网路基础设施设备等)、技术(系统晶片(SoC)、集成电路 (IC))、频宽(57-66 GHz、66-71 GHz 等)、应用(游戏和多媒体、企业无线扩展等)、终端用户行业(消费电子、企业和数据中心、汽车和运输区域运输等地区。

区域分析

到2024年,北美将占据WiGig市场34.20%的份额,这主要得益于企业早期采用WiGig技术、《晶片法案》(CHIPS Act)推动的半导体投资,以及美国联邦通信委员会(FCC)允许高于其他地区的EIRP(等效全向辐射功率)的规定。纽约的金融服务公司正在部署无线对接设备以最大限度地提高办公空间利用率,而西海岸的高科技园区则利用60GHz链路建造灵活的工作舱。加拿大在银行业和媒体产业正效仿美国的模式,而墨西哥的加工出口走廊(Maquiladora Corridor)正在试行以WiGig技术为基础的AGV(自动导引车)车队,以提升出口製造业的竞争力。

亚太地区是成长引擎,预计到2030年将以23.50%的复合年增长率成长。日本网路设备製造商率先认证了整合WiGig无线电技术的三频Wi-Fi 7网路基地台。东京各市政府正计画在大型赛事举办前,在体育场大厅提前部署WiGig技术。韩国正利用其密集的5G骨干网络,将WiGig技术整合到高阶智慧型手机中,实现三频分流;新加坡则在其金融区的智慧路灯上试行60GHz链路,这些都凸显了全部区域数位转型的强劲势头。

欧洲在WiGig技术方面进展不一。德国和英国在维修依赖确定性无线网路的智慧工厂方面处于领先地位,但南欧地区缓慢的资本支出导致该地区的WiGig普及率低于全球平均水平。欧洲电信标准化协会(ETSI)的标准统一了技术参数,但欧盟各国在功率限制方面的差异造成了额外的认证工作,减缓了WiGig的普及速度。杜拜的金融科技中心正在评估WiGig在交易大厅的应用,南非的矿业公司正在测试用于即时钻井分析的60 GHz连结。然而,资本支出限制和地理挑战限制了WiGig的短期普及,随着该地区GDP和互联互通倡议的推进,WiGig市场仍有巨大的成长空间。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 4K/8K 和 XR 串流媒体的需求激增

- 将 WiGig 三频无线电整合到 Wi-Fi 7 AP 中

- 支援 WiGig 功能的笔记型电脑和智慧型手机正变得越来越普及。

- 企业对超高速无线扩充座的需求

- 边缘AI伺服器,附60GHz背板链路

- 60GHz频段机上互联试点

- 市场限制

- 范围有限,目光锐利

- Wi-Fi 6E/7 和 5G 毫米波替代的风险

- 手持式 60GHz 无线电的热设计限制。

- 分散的 60 GHz EIRP 调节

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章 市场规模与成长预测

- 副产品

- 显示装置

- 无线扩充座

- AR/ VR头戴装置

- 电视和投影仪

- 网路基础设施设备

- 网路基地台和路由器

- 回程传输

- 其他的

- 显示装置

- 透过技术

- 系统晶片(SoC)

- 积体电路(IC)

- 按频宽

- 57~66GHz(IEEE 802.11ad)

- 66~71GHz

- 71 至 86 GHz(IEEE 802.11ay 绑定)

- 透过使用

- 游戏和多媒体

- 企业级无线扩充座

- 网路和资料传输

- 车载资讯娱乐系统

- 智慧製造/工业物联网

- 按最终用户行业划分

- 消费性电子产品

- 企业和资料中心

- 汽车与运输

- 工业和製造业

- 航太与国防

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Qualcomm Technologies Inc.

- Intel Corporation

- Broadcom Inc.

- Cisco Systems Inc.

- Panasonic Holdings Corp.

- Peraso Technologies Inc.

- Blu Wireless Technology Ltd.

- Tensorcom Inc.

- Fujikura Ltd.

- Sivers Semiconductors AB

- Dell Technologies Inc.

- Lenovo Group Ltd.

- HP Development Company LP

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Marvell Technology Inc.

- NXP Semiconductors NV

- Analog Devices Inc.

- Keysight Technologies Inc.

- LitePoint(Teradyne Inc.)

- NEC Corporation

- Qualcomm Atheros(subsidiary)

第七章 市场机会与未来展望

The WiGig market size is valued at USD 26.32 billion in 2025 and is forecast to expand to USD 70.45 billion by 2030, translating into a 21.76% CAGR over the period.

Commercial momentum is shifting from niche wireless-docking hubs toward broad integration in Wi-Fi 7 tri-band access points, premium laptops, and early 6G backhaul trials. Demand for 4K/8K video, AR/VR workloads, and edge-AI traffic is stretching the capacity of the 2.4 GHz and 5/6 GHz bands, making 60 GHz throughput indispensable for latency-sensitive applications. At the same time, semiconductor vendors are simplifying design cycles through system-on-chip solutions that cut power draw while shrinking form factors, a prerequisite for smartphones and ultra-thin notebooks. Finally, geopolitical pressures around gallium supply and diverging regional power-limit rules are prompting OEMs to qualify second-source suppliers and lobby regulators for harmonized 60 GHz frameworks, indicating that policy as well as technology will shape the WiGig market trajectory.

Global WiGig Market Trends and Insights

Surge in 4K/8K and XR streaming demand

Ultra-high-definition content requires sustained 25-100 Mbps per stream, and households now run simultaneous 4K, 8K, and AR tasks. The 60 GHz layer supplies headroom where 2.4 GHz and 5/6 GHz traffic face interference and limited contiguous channel widths. In North America and Japan, pay-TV operators already bundle 8K sports feeds that push legacy Wi-Fi to its limits. Device OEMs therefore embed multi-gigabit radios so that premium televisions, consoles, and headsets can maintain sub-10 ms latencies without tethered links. As XR headsets scale in enterprise training and consumer gaming, dependable untethered throughput becomes a purchasing criterion, directly raising the addressable WiGig market.

Integration of 60 GHz tri-band radios in Wi-Fi 7 APs

Access-point vendors are shipping Wi-Fi 7 chipsets that aggregate 2.4 GHz, 5/6 GHz, and 60 GHz into a single platform. Multi-link operation hands sessions back and forth in real time, letting short-range devices jump to 60 GHz while distant clients remain on lower bands. This architecture reduces cabling costs for dense campuses and unlocks incremental software revenue from network-analytics tools that optimize band steering. European cloud offices deploying 10 Gbps fiber uplinks view tri-band Wi-Gig as a hedge against peak-hour congestion, underscoring how infrastructure integration converts WiGig from a luxury add-on into a baseline checklist item.

Limited range and strict line-of-sight

At 60 GHz, oxygen absorption and wall attenuation curb links to roughly 10 meters, so access points must be installed in every conference room or factory cell. Even glass partitions can halve throughput, and moving people create fading that requires beam-tracking algorithms. Field tests on autonomous vehicles show packet-loss spikes when small obstacles break Fresnel zones, reinforcing that WiGig rollouts need precise site surveys. Such constraints restrict the technology to high-density venues or fixed setups, limiting broader consumer adoption and trimming WiGig market expectations in mass-market home routers.

Other drivers and restraints analyzed in the detailed report include:

- Rising attach-rate of WiGig-enabled laptops and smartphones

- Enterprise need for ultra-fast wireless docking

- Substitution risk from Wi-Fi 6E/7 and 5G mmWave

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Display devices commanded 46.0% of the WiGig market in 2024, demonstrating how wireless monitors, docking stations, and AR/VR headsets still anchor near-term revenue. The sub-segment benefits from households seeking clutter-free gaming corners and offices migrating to hot-desking layouts. Wireless hubs that host dual 4K screens and SSD-grade peripherals already appear in premium enterprise bundles, showing that design-once, deploy-many efficiencies favor WiGig over USB-C cabling for new builds. AR/VR headset makers rely on 60 GHz to avoid nausea-inducing latency, and upcoming mixed-reality rollouts will further lift unit volumes. Televisions and projectors integrate WiGig for uncompressed 8K streams across a living room, but adoption lags because a single wall can impair reception.

Network infrastructure devices are the fastest-growing slice at 28.40% CAGR, a trajectory driven by Wi-Fi 7 tri-band access points shipping into corporate refresh cycles. Edge-compute nodes inside factories now leverage 60 GHz backhaul to sidestep fiber trenching, reducing installation lead-times by up to 70%. Municipal kiosk vendors experiment with 60 GHz radios for pop-up broadband in dense downtown corridors where digging permits add months to fiber projects. Early metrics show link availability above 99% when clear line-of-sight is maintained, validating that backhaul can be a high-margin adjacency for the WiGig market.

System-on-chip designs held 58.0% share of the WiGig market in 2024 and are projected to grow at 23.0% CAGR through 2030. Unified dies integrate baseband, RF front-end, and power management, cutting board space by up to 30% and extending smartphone battery life. As foundries perfect sub-3 nm nodes, the incremental cost of adding a 60 GHz block falls, accelerating attach rates in mid-tier devices. Qualcomm's latest platforms pack WiGig, 6 GHz Wi-Fi, Bluetooth LE Audio, and 5G radios into one substrate, reducing vendor qualification cycles from quarters to weeks.

Discrete integrated-circuit implementations remain relevant where legacy boards need drop-in modules or where industrial gear demands ruggedized packages. Medical imaging carts, for instance, retrofit 60 GHz cards without redesigning the entire motherboard. Intel's 18A roadmap targets both monolithic and tile-based architectures so that OEMs can mix high-performance CPU cores with specialized radio tiles, underscoring how manufacturing advances keep multiple bill-of-materials paths viable. The interplay between SoC convenience and discrete flexibility should balance innovation risk, supporting continued WiGig market expansion.

The WiGig Market Report is Segmented by Product (Display Devices, Network Infrastructure Devices, and More), Technology (System-On-Chip (SoC) and Integrated Circuit (IC)), Frequency Band (57-66 GHz, 66-71 GHz, and More), Application (Gaming and Multimedia, Enterprise Wireless Docking, and More), End-User Industry (Consumer Electronics, Enterprise and Datacenter, Automotive and Transportation, and More), and Geography.

Geography Analysis

North America accounted for 34.20% of the WiGig market in 2024, owing to early enterprise adoption, CHIPS-Act-funded semiconductor investments, and FCC rules that allow higher EIRP than most regions. Financial-services firms in New York deploy wireless docking to maximize real-estate density, and West-Coast tech campuses use 60 GHz links in agile work pods. Canada mirrors U.S. patterns in banking and media verticals, while Mexico's maquiladora corridor pilots WiGig-based AGV fleets to raise export manufacturing competitiveness.

Asia Pacific is the growth engine with a 23.50% CAGR to 2030. Japan's networking OEMs were the first to certify tri-band Wi-Fi 7 access points that embed WiGig radios; early municipal deployments in Tokyo target stadium concourses ahead of large-scale events.China's consumer-electronics giants build 60 GHz capability into televisions and laptops to differentiate in crowded domestic channels, although export clearance may face geopolitical headwinds tied to gallium supply chains. South Korea bundles WiGig in premium smartphones, leveraging its dense 5G backbone for tri-band offload, while Singapore pilots 60 GHz links in financial district smart lamp-posts, underscoring region-wide digital-transformation momentum.

Europe exhibits heterogeneous progress. Germany and the United Kingdom lead with smart-factory retrofits that rely on deterministic wireless, but Southern Europe's slower capital-spending pulls regional penetration below global averages. ETSI standards harmonize technical parameters, yet power-limit disparities across EU nations raise extra certification work that delays rollouts. The Middle East and Africa remain nascent; Dubai's fintech hubs evaluate WiGig for trading floors, and South-Africa mines test 60 GHz links for real-time drilling analytics. However, capex constraints and terrain challenges temper near-term uptake, leaving considerable headroom for the WiGig market as regional GDP and connectivity initiatives advance.

- Qualcomm Technologies Inc.

- Intel Corporation

- Broadcom Inc.

- Cisco Systems Inc.

- Panasonic Holdings Corp.

- Peraso Technologies Inc.

- Blu Wireless Technology Ltd.

- Tensorcom Inc.

- Fujikura Ltd.

- Sivers Semiconductors AB

- Dell Technologies Inc.

- Lenovo Group Ltd.

- HP Development Company LP

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Marvell Technology Inc.

- NXP Semiconductors N.V.

- Analog Devices Inc.

- Keysight Technologies Inc.

- LitePoint (Teradyne Inc.)

- NEC Corporation

- Qualcomm Atheros (subsidiary)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in 4K/8K and XR streaming demand

- 4.2.2 Integration of WiGig tri-band radios in Wi-Fi 7 APs

- 4.2.3 Rising attach-rate of WiGig-enabled laptops and smartphones

- 4.2.4 Enterprise need for ultra-fast wireless docking

- 4.2.5 Edge-AI servers adopting 60 GHz back-plane links

- 4.2.6 In-flight cabin connectivity pilots at 60 GHz

- 4.3 Market Restraints

- 4.3.1 Limited range and strict line-of-sight

- 4.3.2 Substitution risk from Wi-Fi 6E/7 and 5G mmWave

- 4.3.3 Thermal design limits in handheld 60 GHz radios

- 4.3.4 Fragmented 60 GHz EIRP regulations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Display Devices

- 5.1.1.1 Wireless Docking Stations

- 5.1.1.2 AR/VR Headsets

- 5.1.1.3 Televisions and Projectors

- 5.1.2 Network Infrastructure Devices

- 5.1.2.1 Access Points and Routers

- 5.1.2.2 Backhaul Radios

- 5.1.3 Others

- 5.1.1 Display Devices

- 5.2 By Technology

- 5.2.1 System-on-Chip (SoC)

- 5.2.2 Integrated Circuit (IC)

- 5.3 By Frequency Band

- 5.3.1 57-66 GHz (IEEE 802.11ad)

- 5.3.2 66-71 GHz

- 5.3.3 71-86 GHz (IEEE 802.11ay bonded)

- 5.4 By Application

- 5.4.1 Gaming and Multimedia

- 5.4.2 Enterprise Wireless Docking

- 5.4.3 Networking and Data Transfer

- 5.4.4 In-vehicle Infotainment

- 5.4.5 Smart Manufacturing / IIoT

- 5.5 By End-user Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Enterprise and Datacenter

- 5.5.3 Automotive and Transportation

- 5.5.4 Industrial and Manufacturing

- 5.5.5 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Qualcomm Technologies Inc.

- 6.4.2 Intel Corporation

- 6.4.3 Broadcom Inc.

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Panasonic Holdings Corp.

- 6.4.6 Peraso Technologies Inc.

- 6.4.7 Blu Wireless Technology Ltd.

- 6.4.8 Tensorcom Inc.

- 6.4.9 Fujikura Ltd.

- 6.4.10 Sivers Semiconductors AB

- 6.4.11 Dell Technologies Inc.

- 6.4.12 Lenovo Group Ltd.

- 6.4.13 HP Development Company LP

- 6.4.14 Samsung Electronics Co. Ltd.

- 6.4.15 MediaTek Inc.

- 6.4.16 Marvell Technology Inc.

- 6.4.17 NXP Semiconductors N.V.

- 6.4.18 Analog Devices Inc.

- 6.4.19 Keysight Technologies Inc.

- 6.4.20 LitePoint (Teradyne Inc.)

- 6.4.21 NEC Corporation

- 6.4.22 Qualcomm Atheros (subsidiary)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

无线Gigabit市场:2026年至2032年全球市场预测(依服务类型、频宽、网路架构及最终用户划分)

无线Gigabit市场:2026年至2032年全球市场预测(依服务类型、频宽、网路架构及最终用户划分) WiGig市场规模、份额、趋势和预测:按产品、通讯协定、技术类型、企业规模、最终用户行业和地区划分,2026-2034年

WiGig市场规模、份额、趋势和预测:按产品、通讯协定、技术类型、企业规模、最终用户行业和地区划分,2026-2034年 2026年全球无线Gigabit市场报告WiGig全球市场报告2026无线Gigabit市场规模、份额、趋势和预测:按产品、技术、最终用户产业和地区划分,2026-2034 年

2026年全球无线Gigabit市场报告WiGig全球市场报告2026无线Gigabit市场规模、份额、趋势和预测:按产品、技术、最终用户产业和地区划分,2026-2034 年 WiGig市场分析及至2035年预测:按类型、产品、服务、技术、组件、应用、设备、部署模式及最终用户划分

WiGig市场分析及至2035年预测:按类型、产品、服务、技术、组件、应用、设备、部署模式及最终用户划分 WiGig市场-全球产业规模、份额、趋势、机会、预测:按产品、类型、技术、最终用户、地区和竞争对手划分,2021-2031年无线Gigabit(Wigig)市场 - 全球产业规模、份额、趋势、机会及预测(依产品类型、技术、产业垂直领域、地区及竞争格局划分,2021-2031年)

WiGig市场-全球产业规模、份额、趋势、机会、预测:按产品、类型、技术、最终用户、地区和竞争对手划分,2021-2031年无线Gigabit(Wigig)市场 - 全球产业规模、份额、趋势、机会及预测(依产品类型、技术、产业垂直领域、地区及竞争格局划分,2021-2031年) WiGig市场规模、份额和成长分析(按产品、类型、最终用户和地区划分)-产业预测(2026-2033年)

WiGig市场规模、份额和成长分析(按产品、类型、最终用户和地区划分)-产业预测(2026-2033年) 无线Gigabit市场(按通路、通讯协定和地区)

无线Gigabit市场(按通路、通讯协定和地区)