|

市场调查报告书

商品编码

1849884

BPaaS(业务流程即服务):市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Business-Process-as-a-Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

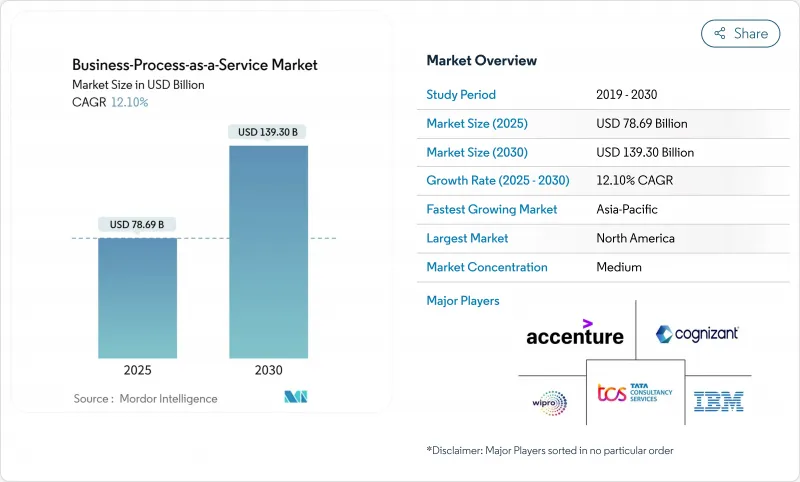

预计到 2025 年,业务流程即服务 (BPaaS) 市场规模将达到 786.9 亿美元,到 2030 年将达到 1,393 亿美元,预测期(2025-2030 年)的复合年增长率为 12.10%。

云端原生交付模式的加速普及、人工智慧的快速发展以及监管机构对弹性营运日益增长的压力,正在重塑企业策略。企业正在将固定成本转化为可变成本,同时即时获取先进的自动化、分析和特定产业最佳实践——这些能力过去需要数年的资本投入才能实现。在近期供应链中断事件后,企业对营运弹性的关注度显着提升,这进一步巩固了业务流程即服务 (BPaaS) 作为实现本地合规、标准化流程并同时实现全球扩展的首选途径的地位。供应商正透过基于结果的商业模式、自主云端选项和符合 ESG 标准的流程包来应对这一趋势,所有这些都在深化业务流程即服务 (BPaaS) 市场在数位转型专案中的策略角色。

全球业务流程即服务 (BPaaS) 市场趋势与洞察

对云端服务和标准化流程的需求不断增长

向云端平台的普遍转型支援大规模流程标准化。目前,94% 的企业利用云端解决方案来简化工作流程、缩短部署週期并实现一致的管治。弹性资源分配支援快速因应需求变化,而无需进行新的资本决策。 IBM 指出,77% 的企业已经运行混合架构,这使它们能够在多个云端平台上统一核心流程,同时将策略性工作负载保留在首选的司法管辖区。标准化的云端原生模组加速了银行和保险业的合规运营,在这些行业中,统一的审核追踪至关重要。因此,业务流程即服务 (BPaaS) 市场在各个寻求速度、弹性和全球覆盖的行业中继续保持着多年的成长动能。

降低营运成本和提高生产力的必要性

经济逆风加剧了以基于消费的模式取代固定成本的压力。业务流程即服务 (BPaaS) 将多年期授权合约、资料中心折旧免税额和人事费用成本转化为与实际使用量挂钩的变动成本。 DXC Technology 的报告显示,企业从传统外包模式转向 BPaaS 框架后,可节省 20% 至 30% 的成本。这些服务内建的流程自动化功能进一步提高了生产力,一些公司报告称,其财务后勤部门营运效率提高了 40%。这些财务和营运方面的综合优势,使业务流程即服务 (BPaaS) 市场成为提升短期盈利和长期竞争力的实用工具。

人们越来越关注资料安全和隐私问题

业务流程即服务 (BPaaS) 的部署涉及分散式基础设施,这可能会扩大威胁面。南非储备银行警告称,如果控制措施薄弱,云端处理会加剧营运风险和系统性风险。欧洲的 GDPR 和加州的 CCPA 法规对违规行为处以严厉的处罚,迫使服务提供者实施进阶加密、身分管理和区域资料居住架构。即使更安全的平台不断涌现,人们对业务流程即服务 (BPaaS) 市场的信心也在逐渐恢復,但日益严格的审查仍将暂时减缓决策週期,并限制敏感领域在短期内采用 BPaaS。

细分市场分析

到2024年,大型企业将占据业务流程即服务 (BPaaS) 市场64.3%的份额,它们利用标准化的全球工作流程来简化审核并减少平台重迭。这些企业通常会先外包财务和人力资源等非核心职能,然后在管治结构稳健后,扩展到客户体验和供应链分析领域。许多公司正在实施中间件层,将本地部署的ERP系统与公共云端微服务结合,充分利用供应商的创新,同时保持策略资料控制。同时,新成立的企业级管治委员会根据基于结果的合约监控供应商的绩效,以确保其与策略目标持续保持一致。

中小企业(SMB)历来在市场中占比偏低,如今却成为成长最快的细分市场,预计复合年增长率(CAGR)将达到13.3%。云端优先解决方案消除了资本支出、专业人才短缺和基础设施维护等传统障碍。总部位于日本的Kubel Co., Ltd.报告称,其Chatwork平台到2024年9月将服务60.5万家中小企业客户,这印证了该细分市场的巨大需求。中小企业通常从单一流程模组入手,例如薪资核算、发票处理或服务台自动化,并在可靠性得到验证后扩展到端到端套件。弹性定价模式在成长和景气衰退时期都能提供重要的现金流弹性。因此,随着供应商发布针对特定产业规性客製化的预先配置软体包,预计到2030年,中小企业相关的业务流程即服务(BPaaS)市场规模将显着成长。

人力资源管理在2024年占总收入的24.1%,反映出全球普遍体认到,标准化招募、薪资核算和人才招聘流程能够降低合规风险并提升员工体验。许多供应商现在将人力资源模组与预测分析结合,用于预测离职率、识别技能差距并推荐学习内容。核算和财务流程也可以透过机器人发票核对、自动核对和人工智慧驱动的诈欺检查来提高准确性并缩短週期时间。供应链和采购解决方案则能够改善供应商协作并提升库存可见度。

客户服务与支援预计将以每年 14.6% 的速度成长,推动品牌向全通路互动转型。人工智慧主导的聊天机器人和语音分析能够以远低于传统客服中心的成本提供即时、个人化的回应。 Sutherland Global 的客户案例提高了首次呼叫解决率,提升了净推荐值 (NPS),减少了升级次数,同时缩短了平均回应时间。销售和行销业务流程即服务 (BPaaS) 对这些进步起到了补充作用,它将宣传活动数据与前台分析同步,从而提高销售线索品质。营运模组将工作流程引擎应用于现场服务调度、工厂维护计划和品质保证。这些创新将支持 BPaaS(业务流程即服务)市场的持续扩张。

业务流程即服务 (BPaaS) 市场按组织规模(大型企业、中小企业)、流程类型(人力资源管理、核算与财务、其他)、部署模式(公共云端BPaaS、私有云端BPaaS、混合/多重云端BPaaS)、最终用户行业(银行、金融服务和保险 (BFSI)、IT 和通讯、其他)以及地区进行细分。市场预测以美元计价。

区域分析

北美地区预计在2024年将占全球收入的41.2%,这主要得益于早期云端采用率高以及强大的供应商生态系统。金融机构正在利用业务流程即服务 (BPaaS) 来整合跨司法管辖区的合规文檔,而零售集团则在积极推动人工智慧驱动的客户服务自动化。云端基础设施集中度显着,英国竞争与市场管理局 (CMA) 估计,AWS 和微软分别占据北美基础设施40-50%和30-40%的份额。这种主导地位促使 BPaaS 供应商与超大规模资料中心业者建立策略联盟,以优化延迟并推动联合市场推广计画。

预计亚太地区将在2025年至2030年间以12.8%的复合年增长率实现最快成长。印度、菲律宾和印尼等国政府正在推行「云端优先」政策,以降低营运成本并改善公共服务。印度资料安全委员会预测,到2022年,该国的云端市场规模将达到77亿美元,凸显了其基础设施的成熟度。本地供应商正与全球企业合作,以满足区域资料在地化的需求。面临人手不足的挑战,日本企业正在利用业务流程即服务(BPaaS)来实现日常任务的自动化,从而刺激製造业和零售业的需求。

在欧洲,严格的资料隐私规则正在引导企业选择云端服务方案,并推动其谨慎成长。 GDPR合规性正在影响合约条款、资料居住条款和责任共担框架。预计2029年,德国的业务流程外包(BPO)市场规模将达213.2亿美元,目前云端服务采用率已达81%。金融机构倾向于混合模式,将本地主权云与可扩展的公共资源结合,以满足欧洲金融监管局(Eurofi)的监管指南。该地区强劲的ESG(环境、社会和治理)议程正在推动以永续发展为中心的业务流程即服务(BPaaS)解决方案的需求,这些解决方案能够自动进行碳核算和社会影响报告。

其他好处

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对云端服务和标准化流程的需求不断增长

- 需要降低营运成本并提高生产效率

- 业务流程即服务 (BPaaS) 中人工智慧/超自动化技术的快速应用

- 基于结果的业务流程即服务 (BPaaS)定价模式的扩展

- ESG相关报告要求推动永续性BPaaS

- 对产业专用的BPaaS解决方案的需求

- 市场限制

- 人们越来越关注资料安全和隐私问题

- 与原有核心系统整合的复杂性

- 供应商锁定和有限的互通性

- 主权云端要求限制了跨国业务流程即服务 (BPaaS)。

- 产业价值链分析

- 监管环境

- 技术展望

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 影响市场的宏观经济因素

第五章 市场规模与成长预测

- 按组织规模

- 大公司

- 小型企业

- 透过流程

- 人力资源管理(HRM)

- 会计与财务

- 客户服务与支援

- 销售与行销

- 供应链与采购

- 营运和其他横向流程

- 按部署模式

- 公共云端BPaaS

- 私有云端BPaaS

- 混合/多重云端BPaaS

- 按最终用户行业划分

- BFSI

- 资讯科技和通讯

- 医疗保健和生命科学

- 零售与电子商务

- 製造业

- 政府和公共部门

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 新加坡

- 马来西亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Accenture plc

- IBM Corporation

- Tata Consultancy Services(TCS)

- Cognizant Technology Solutions

- Wipro Limited

- HCL Technologies

- Capgemini SE

- Infosys Limited

- Genpact Ltd.

- Fujitsu Ltd.

- Oracle Corporation

- SAP SE

- Deloitte Touche Tohmatsu Limited

- NTT DATA

- CGI Inc.

- DXC Technology

- Tech Mahindra

- EXL Service Holdings

- ADP Inc.

- Alight Solutions

- Paychex Inc.

- UKG(Ultimate Kronos Group)

- TriNet Group

- Ceridian HCM

- WNS Global Services

- Sutherland Global Services

第七章 市场机会与未来趋势

The Business-Process-as-a-Service Market size is estimated at USD 78.69 billion in 2025, and is expected to reach USD 139.30 billion by 2030, at a CAGR of 12.10% during the forecast period (2025-2030).

Accelerating adoption of cloud-native delivery models, rapid progress in artificial intelligence, and stronger regulatory pressure for resilient operations are reshaping organizational strategies. Enterprises are converting fixed costs into variable outlays while gaining immediate access to advanced automation, analytics, and industry-specific best practices-capabilities that once required years of capital investment. Intensifying focus on operational resilience after recent supply-chain disruptions has further positioned BPaaS as a preferred route for standardized processes that scale globally yet remain locally compliant. Vendors are responding through outcome-based commercial models, sovereign-cloud options, and ESG-linked process bundles, all of which deepen the strategic role of the Business-Process-as-a-Service market in digital transformation programs.

Global Business-Process-as-a-Service Market Trends and Insights

Growing Demand for Cloud Services and Standardized Processes

Universal migration toward cloud platforms underpins large-scale process standardization. Ninety-four percent of enterprises now leverage cloud solutions to streamline workflows, shorten deployment cycles, and ensure consistent governance. Elastic resource allocation supports rapid pivots in demand without forcing new capital decisions. IBM notes that 77% of firms already run hybrid architectures, enabling them to unify core processes over multiple clouds while keeping strategic workloads in preferred jurisdictions. Standardized, cloud-native modules accelerate compliance tasks in banking and insurance, where uniform audit trails are essential. As a result, the Business-Process-as-a-Service market experiences sustained multi-year momentum across sectors that demand speed, resilience, and global reach.

Need to Reduce Operational Cost and Boost Productivity

Economic headwinds intensify pressure to replace fixed costs with consumption-based models. BPaaS converts multi-year license contracts, data-center depreciation, and labor overhead into variable fees that align with actual usage. DXC Technology reports savings of 20-30% when organizations shift from traditional outsourcing to BPaaS frameworks. Process automation embedded in these services delivers additional productivity gains, with some enterprises citing 40% efficiency improvements in finance back-office tasks. These combined financial and operational benefits reinforce the Business-Process-as-a-Service market as a pragmatic lever for near-term profitability and long-term competitiveness.

Heightened Data-Security and Privacy Concerns

BPaaS deployments involve a distributed infrastructure that can enlarge the threat surface. The South African Reserve Bank cautions that cloud computing amplifies operational and systemic risks when controls are weak. European GDPR and California CCPA regulations impose severe penalties for non-compliance, compelling providers to implement sophisticated encryption, identity management, and regional data-residency architectures. Heightened scrutiny temporarily slows decision cycles, limiting short-term adoption in sensitive verticals even as security-enhanced platforms emerge to rebuild trust in the Business-Process-as-a-Service market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of AI / Hyper-automation in BPaaS

- Expansion of Outcome-based (Gain-share) BPaaS Pricing Models

- Integration Complexity with Legacy Core Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large Enterprises dominated 2024 with 64.3% of the Business-Process-as-a-Service market share, leveraging standardized global workflows to simplify audits and cut duplicative platforms. They often start by outsourcing non-core finance and HR tasks, then extend coverage to customer experience and supply-chain analytics once governance structures prove resilient. Integration remains a priority; many deploy middleware layers that blend on-premise ERPs with public-cloud microservices, preserving strategic data control while maximizing vendor innovation. In parallel, fresh enterprise-wide governance councils monitor vendor performance under outcome-based contracts, ensuring continuous alignment with strategic objectives.

SMEs, though historically under-represented, now display the strongest momentum with a forecast 13.3% CAGR. Cloud-first solutions remove traditional barriers such as capital outlay, specialist talent shortages, and infrastructure maintenance. Japan's Kubell Co. reports that its Chatwork platform served 605,000 SME clients by September 2024, underscoring the segment's pent-up demand. SMEs typically begin with single-process modules-payroll, invoicing, or help-desk automation-before scaling to end-to-end suites as reliability is proven. The elastic fee model offers crucial cash-flow flexibility during growth spurts or economic contractions. Consequently, the Business-Process-as-a-Service market size attributable to SMEs is projected to widen substantially through 2030 as providers release pre-configured bundles tailored for industry-specific compliance.

Human Resource Management retained 24.1% of 2024 revenue, reflecting global recognition that standardized recruitment, payroll, and talent-engagement workflows lower compliance risk and enhance employee experience. Many providers now pair HR modules with predictive analytics that forecast attrition, identify skill gaps, and recommend learning content. Accounting and Finance processes also gain traction as robotic invoice matching, automated reconciliations, and AI-driven fraud checks boost accuracy while shrinking cycle times. Supply Chain and Procurement solutions improve vendor collaboration and inventory visibility, critical in volatile logistics environments.

Customer Service and Support, forecast to rise 14.6% annually, leads growth as brands pivot to omnichannel engagement. AI-driven chatbots and voice analytics deliver instant, personalized responses at far lower cost than traditional call centers. Sutherland Global's deployments cut average response time while raising first-contact resolution, enhancing NPS scores, and reducing escalations. Sales and Marketing BPaaS complements these advances, synchronizing campaign data with front-office analytics to sharpen lead quality. Operations modules apply workflow engines to field-service dispatch, plant-maintenance scheduling, and quality assurance. Together, these innovations anchor sustained expansion of the Business-Process-as-a-Service market.

Business Process As A Service Market is Segmented by Organization Size (Large Enterprises and Small and Medium Enterprises), Process (Human Resource Management, Accounting and Finance, and More), Deployment Model (Public Cloud BPaaS, Private Cloud BPaaS, and Hybrid/Multi-Cloud BPaaS), End-User Industry (BFSI, IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 41.2% of 2024 revenue for the Business-Process-as-a-Service market, buoyed by early cloud uptake and deep provider ecosystems. Financial institutions use BPaaS to consolidate compliance documentation across jurisdictions, while retail groups pursue AI-led customer-service automation. Cloud infrastructure concentration is notable; the UK Competition and Markets Authority estimates AWS and Microsoft hold 40-50% and 30-40% of North American infrastructure, respectively. This dominance encourages BPaaS vendors to forge strategic alliances with hyperscalers for latency optimization and joint go-to-market programs.

Asia-Pacific is projected to record the fastest 12.8% CAGR between 2025 and 2030. Governments in India, the Philippines, and Indonesia promote "cloud first" mandates to reduce operating costs and improve citizen services. The Data Security Council of India notes that the national cloud market reached USD 7.70 billion by 2022, underscoring the readiness of foundational infrastructure. Indigenous providers partner with global players to address regional data-localization requirements. Japanese enterprises, challenged by labor shortages, lean on BPaaS to automate routine functions, stimulating demand across manufacturing and retail sectors.

Europe exhibits measured growth as stringent privacy rules guide deployment choices. GDPR compliance shapes contract terms, data-residency clauses, and shared-responsibility frameworks. Germany's BPO market, forecast to hit USD 21.32 billion by 2029, already registers 81% cloud adoption among firms. Financial institutions prefer hybrid models, pairing local sovereign clouds with scalable public resources to satisfy supervisory guidance outlined by Eurofi. The region's strong ESG agenda fuels demand for sustainability-centric BPaaS solutions that automate carbon accounting and social-impact reporting.

- Accenture plc

- IBM Corporation

- Tata Consultancy Services (TCS)

- Cognizant Technology Solutions

- Wipro Limited

- HCL Technologies

- Capgemini SE

- Infosys Limited

- Genpact Ltd.

- Fujitsu Ltd.

- Oracle Corporation

- SAP SE

- Deloitte Touche Tohmatsu Limited

- NTT DATA

- CGI Inc.

- DXC Technology

- Tech Mahindra

- EXL Service Holdings

- ADP Inc.

- Alight Solutions

- Paychex Inc.

- UKG (Ultimate Kronos Group)

- TriNet Group

- Ceridian HCM

- WNS Global Services

- Sutherland Global Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for cloud services and standardized processes

- 4.2.2 Need to reduce operational cost and boost productivity

- 4.2.3 Rapid adoption of AI/hyper-automation in BPaaS

- 4.2.4 Expansion of outcome-based BPaaS pricing models

- 4.2.5 ESG-linked reporting mandates driving sustainability BPaaS

- 4.2.6 Demand for industry-specific BPaaS solutions

- 4.3 Market Restraints

- 4.3.1 Heightened data-security and privacy concerns

- 4.3.2 Integration complexity with legacy core systems

- 4.3.3 Vendor lock-in and interoperability limitations

- 4.3.4 Sovereign-cloud requirements restricting cross-border BPaaS

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Organization Size

- 5.1.1 Large Enterprises

- 5.1.2 Small and Medium Enterprises (SMEs)

- 5.2 By Process

- 5.2.1 Human Resource Management (HRM)

- 5.2.2 Accounting and Finance

- 5.2.3 Customer Service and Support

- 5.2.4 Sales and Marketing

- 5.2.5 Supply Chain and Procurement

- 5.2.6 Operations and Other Horizontal Processes

- 5.3 By Deployment Model

- 5.3.1 Public Cloud BPaaS

- 5.3.2 Private Cloud BPaaS

- 5.3.3 Hybrid/Multi-Cloud BPaaS

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecommunications

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 IBM Corporation

- 6.4.3 Tata Consultancy Services (TCS)

- 6.4.4 Cognizant Technology Solutions

- 6.4.5 Wipro Limited

- 6.4.6 HCL Technologies

- 6.4.7 Capgemini SE

- 6.4.8 Infosys Limited

- 6.4.9 Genpact Ltd.

- 6.4.10 Fujitsu Ltd.

- 6.4.11 Oracle Corporation

- 6.4.12 SAP SE

- 6.4.13 Deloitte Touche Tohmatsu Limited

- 6.4.14 NTT DATA

- 6.4.15 CGI Inc.

- 6.4.16 DXC Technology

- 6.4.17 Tech Mahindra

- 6.4.18 EXL Service Holdings

- 6.4.19 ADP Inc.

- 6.4.20 Alight Solutions

- 6.4.21 Paychex Inc.

- 6.4.22 UKG (Ultimate Kronos Group)

- 6.4.23 TriNet Group

- 6.4.24 Ceridian HCM

- 6.4.25 WNS Global Services

- 6.4.26 Sutherland Global Services

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

2026年全球业务流程管理(BPM)解决方案市场报告

2026年全球业务流程管理(BPM)解决方案市场报告 业务流程即服务 (BPaaS) 市场报告:按流程、部署类型、企业规模、产业和地区划分 (2026–2034)2026年全球业务流程即服务(BPaaS)市场报告

业务流程即服务 (BPaaS) 市场报告:按流程、部署类型、企业规模、产业和地区划分 (2026–2034)2026年全球业务流程即服务(BPaaS)市场报告 业务流程即服务市场分析及至2035年预测:依类型、产品类型、服务、技术、组件、应用、流程、部署类型、最终用户及功能划分

业务流程即服务市场分析及至2035年预测:依类型、产品类型、服务、技术、组件、应用、流程、部署类型、最终用户及功能划分 业务流程即服务 (BPaaS) 市场 - 全球产业规模、份额、趋势、机会与预测:按应用、部署模式、公司规模、垂直产业、地区和竞争格局预测,2021-2031 年

业务流程即服务 (BPaaS) 市场 - 全球产业规模、份额、趋势、机会与预测:按应用、部署模式、公司规模、垂直产业、地区和竞争格局预测,2021-2031 年 BPaaS(业务流程即服务)市场-2025-2030 年预测

BPaaS(业务流程即服务)市场-2025-2030 年预测 商业营运服务市场报告:2031 年趋势、预测与竞争分析

商业营运服务市场报告:2031 年趋势、预测与竞争分析 全球业务流程即服务市场规模研究(按业务流程、部署模型和区域预测)2022-2032

全球业务流程即服务市场规模研究(按业务流程、部署模型和区域预测)2022-2032 BPaaS(业务流程即服务)的全球市场规模、份额和趋势分析:按业务流程、组织规模、行业、地区、前景和预测,2024-2031 年

BPaaS(业务流程即服务)的全球市场规模、份额和趋势分析:按业务流程、组织规模、行业、地区、前景和预测,2024-2031 年 BPaaS(业务流程即服务)市场规模、份额和趋势分析报告:按业务流程、组织规模、行业、地区和细分市场进行预测,2025-2030 年

BPaaS(业务流程即服务)市场规模、份额和趋势分析报告:按业务流程、组织规模、行业、地区和细分市场进行预测,2025-2030 年