|

市场调查报告书

商品编码

1849964

甲苯:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)Toluene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

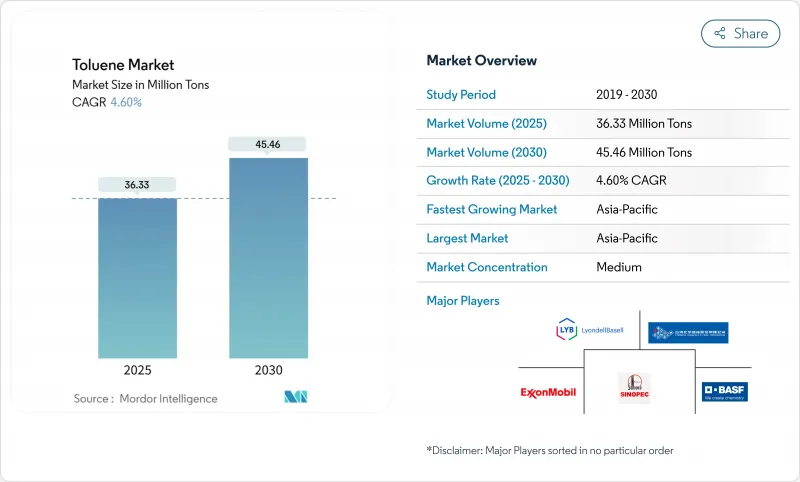

预计到 2025 年,甲苯市场规模将达到 3,633 万吨,预计到 2030 年将达到 4,546 万吨,在预测期(2025-2030 年)内复合年增长率为 4.60%。

需求成长反映了该化学品作为芳香烃的多功能性,它可用于生产苯、二甲苯和二异氰酸酯(TDI)等下游产品,为从建筑到电子等众多行业提供原料。旨在减少排放的监管倡议正在加速製程升级,从而提高能源效率并减少挥发性有机化合物(VOC)的排放,进而增强企业的长期竞争力。这些趋势凸显了供应链向一体化、永续性驱动型供应链的转变,有利于那些能够在成本领先和清洁製程技术投资之间取得平衡的生产商。

全球甲苯市场趋势与洞察

东协地区聚氨酯泡棉产量强劲,推动了TDI消费。

马来西亚、越南和泰国家具、床上用品和汽车座椅用软泡沫生产的快速扩张,推动了TDI需求的成长。诸如马来西亚国家石油公司(Petronas)的RAPID综合体等区域性投资,提高了当地获取甲苯基中间体的管道,并减少了对进口的依赖。生产商正在提高原油与化学品的产量比率,以扩大芳烃产能,使甲苯成为该地区聚氨酯供应的核心。

印度和中国的辛烷值提升强制令将增加重整甲苯的摄取量。

印度的第六阶段排放标准(Bharat Stage VI)和中国六号排放标准(China 6)要求更高的抗爆剂含量,促使炼油厂增加富含甲苯的重整油的用量。努马利加尔炼油厂产能升级至900万吨/年将提振本地供应,而中国的综合炼油厂将为汽油调合池提供更多芳烃。这些倡议将吸收潜在的甲苯过剩,从而为炼油厂利润率提供缓衝,并推高亚太地区溶剂的价格。

欧盟REACH法规收紧对芳烃挥发性有机化合物的限制

欧盟正在收紧挥发性有机化合物(VOC)法规,促使油漆、被覆剂和黏合剂製造商放弃使用芳香族溶剂。由于需要投资于衰减设备以及使用更昂贵的低VOC载体进行替代,因此合规成本将会增加。随着跨国配方商为了遵守欧盟和英国的限製而调整产品线,市场分散化将更加明显,这将抑制消费者应用领域对甲苯的区域需求。

细分市场分析

到2024年,苯和二甲苯将占衍生性商品消费量的38%,显示它们在聚酯、尼龙和特种化学品产业链中占据重要地位。这种领先地位确保了重整装置和芳烃萃取装置的产能稳定,即使利润率有所波动。同时,与TDI相关的甲苯市场预计将在2025年至2030年间以5.45%的复合年增长率成长,这反映了新兴国家对家具和床上用品的强劲需求。

苯甲醛、苯甲酸、TNT及其衍生性商品已发展出一些专门的销售管道,但总体而言,它们在甲苯市场中所占份额较小。一体化生产商透过平衡产品组合併利用规模经济,同时向大宗商品客户和特殊客户供货。

甲苯市场报告按衍生物(苯和二甲苯、汽油添加剂、甲苯二异氰酸酯 (TDI) 及其他)、应用领域(油漆和涂料、粘合剂和油墨、化工工业及其他)、终端用户行业(汽车、建筑、石油和天然气及其他)以及地区(亚太地区、北美地区、欧洲及其他)对行业进行细分。市场预测以吨为单位。

区域分析

预计到2024年,亚太地区将占全球销售量的55%,巩固其作为甲苯市场主要成长引擎的地位,年复合成长率将达到5.61%。都市化、建筑业蓬勃发展以及汽车普及率的提高,正在支撑东协和南亚地区对甲苯衍生物的需求。

北美是一个成熟且充满创新活力的地区,其监管决策具有全球影响力。美国在逐步淘汰剧毒溶剂方面处于领先地位,但却无意中在某些改质剂中偏爱了甲苯。欧洲正在製定最严格的VOC法规,在降低溶剂需求的同时,促进低排放製程化学领域的研究和开发。

中东地区正透过沙乌地阿拉伯和阿联酋的世界级混合二甲苯生产设施增加产量,使其成为亚洲的重要供应地。南美洲的份额较小,但巴西工业的復苏正在提振该地区的需求,尤其是在与重大活动和基础设施建设相关的施工窗口期。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 东协的硬质聚氨酯泡棉生产推动了TDI消费

- 印度和中国的辛烷值提升强制令将推动改良汽油的消费。

- 台湾和韩国对电子级溶剂的需求

- 甲苯取代二氯甲烷用于美国黏合剂领域

- 海湾合作委员会地区芳烃装置产能快速扩张

- 市场限制

- 加强欧盟REACH法规对芳香族化合物的VOC限制

- 石脑油与原油价差的波动对利润率带来压力。

- 北美生物基溶剂的应用日益普及

- 价值链分析

- 原料分析

- 技术概览

- 监管分析

- 贸易分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 价格指数

第五章 市场规模与成长预测

- 导数

- 苯和二甲苯

- 汽油添加剂

- 甲苯二异氰酸酯(TDI)

- 其他衍生物(苯甲酸、三硝基甲苯(TNT)、苯甲醛)

- 透过使用

- 油漆和涂料

- 黏合剂和油墨

- 化工

- 霹雳

- 其他用途(药品、溶剂和脱脂剂、染料和颜料)

- 按最终用户行业划分

- 车

- 建造

- 石油和天然气

- 军事与国防

- 其他终端用户产业(电子产品、消费品)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- BASF

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- CPC Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- Indian Oil Corporation Ltd

- INEOS

- LyondellBasell Industries Holdings BV

- Mangalore Refinery and Petrochemicals Limited

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals, Inc.

- Reliance Industries Limited

- SABIC

- Shell plc

- SK innovation Co., Ltd

- TotalEnergies

- Valero

第七章 市场机会与未来展望

The Toluene Market size is estimated at 36.33 Million Tons in 2025, and is expected to reach 45.46 Million Tons by 2030, at a CAGR of 4.60% during the forecast period (2025-2030).

Demand growth reflects the chemical's versatility as an aromatic hydrocarbon used in downstream products such as benzene, xylene, and toluene diisocyanate (TDI), which feed diverse sectors from construction to electronics. Regulatory initiatives to reduce emissions accelerate process upgrades that improve energy efficiency and cut volatile organic compound (VOC) releases, supporting long-term competitiveness. Together, these trends underscore a shift toward integrated, sustainability-oriented supply chains that favor producers able to balance cost leadership with technology investments in cleaner processes.

Global Toluene Market Trends and Insights

Robust Polyurethane Foam Build-out in ASEAN Elevates TDI Consumption

Surging output of flexible foam for furniture, bedding, and vehicle seats is driving incremental TDI demand in Malaysia, Vietnam, and Thailand. Regional investments, such as Petronas' RAPID complex, increase local access to toluene-based intermediates, limiting import reliance. Producers are elevating crude-to-chemicals yields to expand aromatics output, placing toluene at the heart of regional polyurethane supply.

Octane-Boost Mandates in India and China Boost Reformate Toluene Intake

India's Bharat Stage VI and China 6 fuel norms demand higher anti-knock components, prompting refiners to raise reformate volumes enriched with toluene. Numaligarh Refinery's upgrade to 9 MTPA consolidates local supply, while Chinese integrated complexes channel more aromatics into gasoline blending pools. These moves absorb incremental toluene streams that might otherwise face oversupply, creating a cushion for refinery margins and lifting solvent-grade prices across Asia Pacific.

Tightening EU REACH VOC Restrictions on Aromatics

The European Union has intensified VOC thresholds, prompting paint, coating, and adhesive producers to reformulate away from aromatic solvents. Compliance costs rise through investment in abatement equipment and substitution with higher-priced low-VOC carriers. Market fragmentation emerges as multinational formulators rationalize product lines to accommodate EU and the United Kingdom limits, dampening regional toluene demand in consumer-facing applications

Other drivers and restraints analyzed in the detailed report include:

- Electronics-Grade Solvents Demand in Taiwan and South Korea

- Substitution of Methylene Chloride by Toluene in US Adhesives

- Volatility in Naphtha and Crude Spreads Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Benzene and xylene retained a 38% share of derivative consumption in 2024, underscoring their entrenched role in polyester, nylon, and specialty chemical chains. That leadership secures steady throughput for reformers and aromatics extractors even as margins fluctuate. Meanwhile, the toluene market size tied to TDI is projected to expand at a 5.45% CAGR from 2025-2030, reflecting robust furniture and bedding demand across emerging economies.

Benzaldehyde, benzoic acid, TNT, and niche derivatives carve specialized outlets, but collectively they account for a modest share of the toluene market volumes. Integrated producers balance this portfolio, leveraging economies of scale to supply both commodity and specialty customers.

The Toluene Market Report Segments the Industry by Derivative (Benzene and Xylene, Gasoline Additives, Toluene Diisocyanates (TDI), and Others), Application (Paints and Coatings, Adhesives and Inks, Chemical Industry, and Others), End-User Industry (Automotive, Construction, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons)

Geography Analysis

Asia Pacific controlled 55% of global volumes in 2024, and the region's 5.61% CAGR cements its status as the primary growth engine for the toluene market. Urbanization, construction booms, and rising vehicle penetration sustain derivative demand throughout ASEAN and South Asia.

North America is a mature yet innovative arena where regulatory decisions ripple globally. The United States is spearheading the phaseout of high-toxicity solvents, inadvertently favoring toluene in specific reformulations. Europe grapples with the strictest VOC rules, trimming solvent demand but stimulating research and development toward low-emission process chemistry.

The Middle East adds new barrels through world-scale mixed-xylene facilities in Saudi Arabia and the United Arab Emirates, positioning the region as a swing supplier for Asia. South America accounts for a smaller slice, yet Brazil's industrial recovery lifts regional appetite, especially for construction windows tied to major events and infrastructure drives.

- BASF

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- CPC Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- Indian Oil Corporation Ltd

- INEOS

- LyondellBasell Industries Holdings B.V.

- Mangalore Refinery and Petrochemicals Limited

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals, Inc.

- Reliance Industries Limited

- SABIC

- Shell plc

- SK innovation Co., Ltd

- TotalEnergies

- Valero

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust Polyurethane Foam Build-out in ASEAN Elevates TDI Consumption

- 4.2.2 Octane-Boost Mandates in India and China Boost Reformate Toluene Intake

- 4.2.3 Electronics-Grade Solvents Demand in Taiwan and South Korea

- 4.2.4 Substitution of Methylene Chloride by Toluene in US Adhesives

- 4.2.5 Rapid Capacity Addition of Aromatics Units in GCC Region

- 4.3 Market Restraints

- 4.3.1 Tightening EU REACH VOC Restrictions on Aromatics

- 4.3.2 Volatility in Naphtha and Crude Spreads Compressing Margins

- 4.3.3 Growing Bio-Based Solvent Adoption in North America

- 4.4 Value Chain Analysis

- 4.5 Feedstock Analysis

- 4.6 Technological Snapshot

- 4.7 Regulatory Analysis

- 4.8 Trade Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Degree of Competition

- 4.10 Price Index

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Derivative

- 5.1.1 Benzene and Xylene

- 5.1.2 Gasoline Additives

- 5.1.3 Toluene Diisocyanates (TDI)

- 5.1.4 Other Derivatives (Benzoic Acid, Trinitrotoluene (TNT), Benzaldehyde)

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Inks

- 5.2.3 Chemical Industry

- 5.2.4 Explosives

- 5.2.5 Other Applications (Pharmaceuticals, Solvents and Degreasers, Dyes and Pigments)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Oil and Gas

- 5.3.4 Military and Defense

- 5.3.5 Other End-user Industries (Electronics, Consumer Products)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Braskem

- 6.4.3 Chevron Phillips Chemical Company LLC

- 6.4.4 China Petrochemical Corporation

- 6.4.5 CNPC

- 6.4.6 CPC Corporation

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Formosa Chemicals & Fibre Corp

- 6.4.9 Indian Oil Corporation Ltd

- 6.4.10 INEOS

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 Mangalore Refinery and Petrochemicals Limited

- 6.4.13 Mitsubishi Chemical Group Corporation

- 6.4.14 Mitsui Chemicals, Inc.

- 6.4.15 Reliance Industries Limited

- 6.4.16 SABIC

- 6.4.17 Shell plc

- 6.4.18 SK innovation Co., Ltd

- 6.4.19 TotalEnergies

- 6.4.20 Valero

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

甲苯市场分析及预测(至2035年):类型、产品、应用、技术、终端用户、组件、製程、功能、材料类型及导入形式

甲苯市场分析及预测(至2035年):类型、产品、应用、技术、终端用户、组件、製程、功能、材料类型及导入形式 全球甲苯衍生物市场规模、份额、趋势和成长分析报告(2026-2034年)

全球甲苯衍生物市场规模、份额、趋势和成长分析报告(2026-2034年) 日本甲苯市场规模、份额、趋势和预测:按技术、应用和地区划分,2026-2034年

日本甲苯市场规模、份额、趋势和预测:按技术、应用和地区划分,2026-2034年 2026年全球甲苯市场报告2026年全球甲苯衍生物市场报告

2026年全球甲苯市场报告2026年全球甲苯衍生物市场报告 氯甲苯市场规模、份额和成长分析(依产品类型、形态、应用、最终用途产业、纯度、销售管道和地区划分)-2026-2033年产业预测

氯甲苯市场规模、份额和成长分析(依产品类型、形态、应用、最终用途产业、纯度、销售管道和地区划分)-2026-2033年产业预测 甲苯市场规模、份额及成长分析(按形态、应用和地区划分)-产业预测,2026-2033年

甲苯市场规模、份额及成长分析(按形态、应用和地区划分)-产业预测,2026-2033年 甲苯市场依纯度等级、衍生物、形态、生产流程、应用及分销通路划分-2025-2032年全球预测

甲苯市场依纯度等级、衍生物、形态、生产流程、应用及分销通路划分-2025-2032年全球预测 全球乙烯基甲苯(VT)市场-市场份额和排名、总收入、需求预测(2025-2031)

全球乙烯基甲苯(VT)市场-市场份额和排名、总收入、需求预测(2025-2031) 甲苯二异氰酸酯市场预测(至2032年):全球形态、应用、最终用户和地区分析

甲苯二异氰酸酯市场预测(至2032年):全球形态、应用、最终用户和地区分析