|

市场调查报告书

商品编码

1850004

硬焊焊合金:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Braze Alloys - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

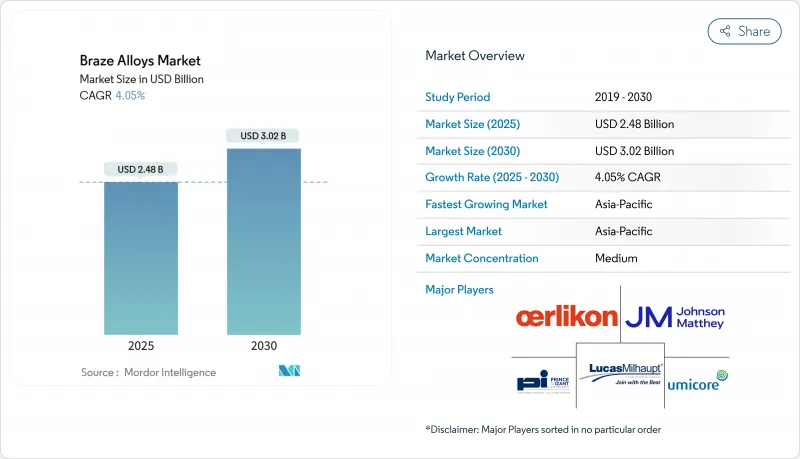

预计到 2025 年,硬焊合金市场规模将达到 24.8 亿美元,到 2030 年将达到 30.2 亿美元,年复合成长率为 4.05%。

汽车热交换器、电动车电力电子设备和先进航太结构对精密金属连接的需求不断增长,推动了市场发展。在中温作业中,硬焊逐渐取代焊接,维持了市场高销售量;同时,新型非晶质箔合金的出现,也拓展了异种金属连接的应用范围。亚太地区在销售和成长方面占据主导地位,这主要得益于中国铝二次加工的蓬勃发展以及该地区电子产品产能的扩张。供应链参与企业越来越倾向于选择高性能配方而非价格敏感型产品,这预示着硬焊焊合金市场正在转向品质驱动型采购模式。

全球硬焊市场趋势与洞察

硬焊而非焊接或锡焊

硬焊因其能在低温下连接材料,从而保持基材性能(这对于航太和电子应用中高精度装配至关重要)而备受製造商青睐。炉内硬焊可在单次循环中完成多个接头的连接,省去了焊接工序,减少了人工成本,并最大限度地减少了变形。改良的焊丝化学成分使其强度可与焊接接头媲美,同时又具备高抗疲劳性,这使得硬焊成为复杂薄壁结构的首选工艺。汽车供应商表示,将手工硬焊修復改为批量焊焊,铝製散热器生产线的生产週期显着缩短。随着原始设备製造商 (OEM) 推行精实生产,这一趋势正在推动中温硬焊合金市场的发展。

汽车热交换器中对铝焊焊的需求迅速成长

电动车和涡轮增压内燃机都需要小型温度控管系统。铝硅焊料可在不影响轻量化目标的前提下形成密封接头,这对于提高续航里程和燃油经济性至关重要。 A2L冷媒的引入提高了接头完整性的要求,进一步增加了焊料用量。 NOCOLOK等助焊剂技术可在可控气氛炉中均匀润湿,从而满足一级热交换器工厂每年数百万台设备的产能需求。这些因素将在短期内导致对铝焊焊焊料的高需求,从而推动亚太地区、北美自由贸易组织(NAFTA)和欧洲汽车丛集的硬焊合金市场成长。

基底金属价格波动

由于供应瓶颈和基础设施需求,铜和银的价格将出现剧烈波动。成本上升将挤压对冲金属或将成本转嫁给客户的焊料生产商的利润净利率,这可能导致对价格敏感的暖通空调和白色家电行业的订单延迟。这种波动将迫使一些加工商考虑机械紧固,在短期内对硬焊焊合金市场构成下行压力。均衡的筹资策略和改进低贵金属含量的合金将部分抵消这种抑製作用,但无法完全消除风险。

细分市场分析

预计到2024年,铜基焊料的销售额将占总销售额的35.86%,显示其在汽车、暖通空调和一般工业应用等领域具有广泛的应用潜力。客户青睐铜的导热性、适中的熔点以及与助焊剂的兼容性,这确保了硬焊焊料市场稳定。含银焊料用于对接头耐腐蚀性要求极高的高阶电子产品,而金合金则符合严苛环境下的微腐蚀防护需求。

其他基底金属,主要是镍和钴,由于其高温稳定性,将以4.71%的复合年增长率快速增长至2030年,这使得它们非常适合用于电动车电池模组和涡轮机部件。亚利桑那州立大学的研究表明,铜-钽-锂合金在800 ℃下保持1120 MPa的屈服强度长达10000小时,这预示着先进铜合金的发展方向。此类发展将扩大特种耐高温合金的市场规模,但不会撼动铜的市场主导地位。

至2024年,棒材和线材产品将占硬焊合金市场30.94%的份额。 MRO(维修、维修和大修)技术人员依赖这种常见的焊焊形式进行焊炬操作,而小批量製造商则看重其低廉的入门成本。粉末、膏状和箔状焊料则适用于电子和航太航天等特殊领域的连接,可在需要特定几何形状时实现合金的精确定位。

受汽车散热器生产线(该行业对重复性要求极高)的推动,预成型环和预製件正以 4.97% 的复合年增长率快速增长。预成型环可将循环时间缩短高达 30%,并提供一致的焊角尺寸,从而减少检验后的返工。机器人技术的整合应用有利于可自动拾取和放置的预製件,这将推动硬焊合金市场在 2030 年前保持高于平均水平的成长。

区域分析

预计到2024年,亚太地区将贡献全球46.28%的收入,年复合成长率达5.03%,成为规模最大且成长最快的地区。受新能源汽车和基础建设的推动,中国再生铝产品市场正以每年13%的速度成长,从而提振了对铝基焊料的需求。日本精密製造商和韩国电子组装正在安装先进的炉线,进一步巩固其在亚太地区的专业技术。儘管薪资上涨和环境、社会及公司治理(ESG)法规的实施正促使部分产能转移至越南和泰国,但强大的供应链仍使亚太地区在硬焊合金市场占据核心地位。

北美保持第二的位置,这主要得益于航太发动机和国防电子项目对高性能镍钴焊料的需求。美国的回流政策和通膨抑制法案正推动资本流入现代化熔炉升级改造,而墨西哥的汽车出口则刺激了铝製散热器的消费。儘管技术纯熟劳工短缺和铜价间歇性上涨抑制了绝对增长,但硬焊合金市场仍然强劲。

欧洲成熟的工业基础为汽车、暖通空调和通用工程领域提供了稳定的需求。严格的RoHS和REACH法规要求正在推动无镉无铅产品的快速普及。德国电动车平台的推广应用刺激了铝硅合金焊料的生产,而英国航太复合材料丛集则转向使用非晶质箔材进行金属-陶瓷连接。循环经济指令为再生焊料开闢了新的市场空间,预示着该地区硬焊合金市场将呈现一条微妙的成长路径。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 硬焊而非焊接或锡焊

- 汽车热交换器中对铝基焊硬焊的需求激增

- 非晶质箔合金的兴起使得低温异质接面的实现成为可能

- 电动车电力电子领域采用镍基介电浆料

- 暖通空调和冷冻产业成长

- 市场限制

- 基底金属价格波动

- 禁止对有害金属(镉、铅)进行监管

- 积层製造替代方案

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按基底金属

- 铜

- 银

- 金子

- 铝

- 其他基底金属(镍、钴等)

- 透过填写表格

- 粉末

- 贴上

- 箔纸/丝带

- 棒材/线材

- 环和预成型件

- 按温度范围

- 低温(低于 450°C)

- 中温(450-800℃)

- 高温(超过 800°C)

- 按最终用户行业划分

- 车

- 航太与国防

- 电机与电子工程

- 建造

- 其他终端用户产业(医疗设备、能源/电力等)

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Aimtek, Inc.

- Cupro Alloys Corporation

- Fusion, Inc.

- Indian Solder and Braze Alloys Pvt. Ltd.

- Johnson Matthey

- Lucas-Milhaupt Inc.

- Materion Corporation

- Morgan Advanced Materials plc

- Nihon Superior Co., Ltd.

- OC Oerlikon Management AG

- Prince & Izant Company

- Saru Silver Alloy Private Limited

- Sulzer Ltd

- The Lincoln Electric Company

- Umicore

- VBC Group

- Wieland Group

第七章 市场机会与未来展望

The braze alloys market size stands at USD 2.48 billion in 2025 and is on track to reach USD 3.02 billion by 2030, reflecting a 4.05% CAGR.

The market gains strength from growing demand for precision metal joining in automotive heat exchangers, EV power electronics, and advanced aerospace structures. Steady substitution of welding by brazing in medium-temperature operations keeps volumes high, while new amorphous foil alloys widen the application window into dissimilar metal assemblies. Asia-Pacific dominates volume and growth, supported by China's secondary aluminum boom and regional electronics capacity expansions. Supply chain participants now favor high-performance formulations over price-driven grades, indicating a shift toward quality-led purchasing across the braze alloys market.

Global Braze Alloys Market Trends and Insights

Adoption of Brazing Over Welding & Soldering

Manufacturers favor brazing because it joins materials at lower temperatures, which preserves base metal properties critical for tight-tolerance assemblies in aerospace and electronics applications. Furnace brazing consolidates multiple joints in a single cycle, eliminating sequential welding steps, cutting labor, and minimizing distortion. Improved filler chemistries now match welded joint strength while offering higher fatigue resistance, making brazing the process of choice for complex thin-wall structures. Automotive suppliers report shorter takt times in aluminum radiator lines after switching from manual weld repair to batch brazing. As OEMs push lean manufacturing, this driver strengthens the braze alloys market across medium-temperature ranges.

Surging Demand for Aluminum Brazes in Automotive Heat Exchangers

Electric vehicles and turbocharged combustion engines both require compact heat management systems. Aluminum-silicon fillers form leak-tight joints without compromising lightweight targets vital for range and fuel economy. Implementing A2L refrigerants has tightened joint integrity requirements, further boosting filler volumes. Flux technologies such as NOCOLOK deliver uniform wetting in controlled-atmosphere furnaces, supporting annual throughput in the millions of units at Tier-1 heat-exchanger plants. These factors translate into high short-term pull for aluminum brazes, lifting the braze alloys market in automotive clusters across APAC, NAFTA, and Europe.

Base-Metal Price Volatility

Copper and silver exhibit sharp price swings due to supply bottlenecks and infrastructure demand. Cost spikes compress margins for filler producers, who hedge metals or pass costs to customers, risking order deferrals in price-sensitive HVAC and white-goods sectors. The volatility prompts some fabricators to consider mechanical fastening, placing downward pressure on the braze alloys market during short-term cycles. Balanced sourcing strategies and alloy reformulations with lower noble-metal content partially offset the restraint, yet cannot fully neutralize exposure.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Amorphous-Foil Alloys Enabling Low-Temperature Dissimilar Joins

- EV Power-Electronics Uptake of Nickel-Based Induction Pastes

- Toxic-Metal Regulatory Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Copper-based fillers generated 35.86% of revenue in 2024, underscoring their broad applicability in automotive, HVAC, and general industrial lines. Users value copper's thermal conductivity, moderate melting point, and compatibility with fluxes, which keep the braze alloys market anchored in this metal class. Silver-bearing grades serve premium electronics where joint resistivity matters, and gold alloys fill micro-corrosion niches in harsh environments.

Other base metals, chiefly nickel and cobalt, will expand briskly at a 4.71% CAGR to 2030 as their high-temperature stability suits EV battery modules and turbine components. Arizona State University demonstrated a copper-tantalum-lithium alloy sustaining 1120 MPa yield strength after 10,000 hours at 800 °C, validating the trajectory toward advanced copper variants. These developments enlarge the braze alloys market size for specialty high-heat grades without eclipsing copper's volume leadership.

Rod and wire products accounted for 30.94% of the braze alloys market in 2024. MRO technicians rely on these familiar forms for torch work, and small batch fabricators appreciate their low entry cost. Powder, paste, and foil formats address niche electronics and aerospace joints, offering precise alloy placement when geometry demands.

Rings and preforms are advancing at a 4.97% CAGR, propelled by automotive radiator lines that value repeatability. Pre-shaped rings cut cycle time by up to 30% and deliver consistent fillet size, which reduces post-inspection rework. Robotics integration favors preforms that can be picked and placed automatically, sustaining above-average growth in the braze alloys market through 2030.

The Braze Alloys Market Report Segments the Industry by Base Metal (Copper, Silver, and More), Filler Form (Powder, Paste, and More), Temperature Range (Low-Temperature, Medium-Temperature, and More), End-User Industry (Automotive, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 46.28% of global revenue in 2024 and is forecast to grow at 5.03% CAGR, making it the largest and fastest region simultaneously. China's secondary aluminum segment is expanding 13% per year, driven by new energy vehicles and infrastructure, which elevates demand for aluminum-based fillers. Japanese precision manufacturers and Korean electronics assemblers install advanced furnace lines, deepening regional expertise. Rising wages and ESG regulations are starting to nudge some capacity toward Vietnam and Thailand, but entrenched supply chains keep APAC at the center of the braze alloys market.

North America holds a solid second tier, propelled by aerospace engine and defense electronics programs that specify high-performance nickel and cobalt fillers. US reshoring policies and the Inflation Reduction Act funnel capital into modern furnace upgrades, while Mexico's auto exports accelerate aluminum radiator consumption. Skilled labor shortages and intermittent copper price spikes temper absolute growth but do not derail the braze alloys market momentum.

Europe's mature industrial base delivers steady demand across automotive, HVAC, and general engineering. Strict RoHS and REACH requirements push quick adoption of cadmium-free and lead-free variants. Germany's EV platform rollout stimulates aluminum-silicon filler volumes, and the UK's aerospace composites cluster turns to amorphous foils for metal-ceramic joints. Circular-economy directives open niches for recycled filler metals, signaling a nuanced growth path for the braze alloys market in the region.

- Aimtek, Inc.

- Cupro Alloys Corporation

- Fusion, Inc.

- Indian Solder and Braze Alloys Pvt. Ltd.

- Johnson Matthey

- Lucas-Milhaupt Inc.

- Materion Corporation

- Morgan Advanced Materials plc

- Nihon Superior Co., Ltd.

- OC Oerlikon Management AG

- Prince & Izant Company

- Saru Silver Alloy Private Limited

- Sulzer Ltd

- The Lincoln Electric Company

- Umicore

- VBC Group

- Wieland Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of brazing over welding & soldering

- 4.2.2 Surging demand for aluminum based brazes in automotive heat-exchangers

- 4.2.3 Rise of amorphous-foil alloys enabling low-temp dissimilar joins

- 4.2.4 EV power-electronics uptake of Ni-based induction pastes

- 4.2.5 Growth of the HVAC and refrigeration industry

- 4.3 Market Restraints

- 4.3.1 Base-metal price volatility

- 4.3.2 Toxic-metal (Cd, Pb) regulatory bans

- 4.3.3 Substitution by additive-manufacturing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Base Metal

- 5.1.1 Copper

- 5.1.2 Silver

- 5.1.3 Gold

- 5.1.4 Aluminum

- 5.1.5 Other Base Metals (Nickel,Cobalt, etc.)

- 5.2 By Filler Form

- 5.2.1 Powder

- 5.2.2 Paste

- 5.2.3 Foil / Ribbon

- 5.2.4 Rod / Wire

- 5.2.5 Rings & Preforms

- 5.3 By Temperature Range

- 5.3.1 Low-Temperature (Less than 450 °C)

- 5.3.2 Medium-Temperature (450-800 °C)

- 5.3.3 High-Temperature (Greater than 800 °C)

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Electrical and Electronics

- 5.4.4 Construction

- 5.4.5 Other End-User Industries(Medical Devices, Energy and Power, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aimtek, Inc.

- 6.4.2 Cupro Alloys Corporation

- 6.4.3 Fusion, Inc.

- 6.4.4 Indian Solder and Braze Alloys Pvt. Ltd.

- 6.4.5 Johnson Matthey

- 6.4.6 Lucas-Milhaupt Inc.

- 6.4.7 Materion Corporation

- 6.4.8 Morgan Advanced Materials plc

- 6.4.9 Nihon Superior Co., Ltd.

- 6.4.10 OC Oerlikon Management AG

- 6.4.11 Prince & Izant Company

- 6.4.12 Saru Silver Alloy Private Limited

- 6.4.13 Sulzer Ltd

- 6.4.14 The Lincoln Electric Company

- 6.4.15 Umicore

- 6.4.16 VBC Group

- 6.4.17 Wieland Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Development of Vacuum Brazing Technology

铝硬焊助焊剂市场规模、份额和成长分析:按产品类型、应用、最终用户、分销管道和地区划分 - 2026-2033 年行业预测

铝硬焊助焊剂市场规模、份额和成长分析:按产品类型、应用、最终用户、分销管道和地区划分 - 2026-2033 年行业预测 硬焊焊丝市场按产品类型、材料类型、包装、厚度、分销管道和应用划分-全球预测,2026-2032年铜硬焊料市场按产品类型、成分、通路、应用和最终用途行业划分-2026年至2032年全球预测

硬焊焊丝市场按产品类型、材料类型、包装、厚度、分销管道和应用划分-全球预测,2026-2032年铜硬焊料市场按产品类型、成分、通路、应用和最终用途行业划分-2026年至2032年全球预测 硬焊合金市场规模、份额及成长分析(依製程、基材、应用、最终用户及地区划分)-2026-2033年产业预测

硬焊合金市场规模、份额及成长分析(依製程、基材、应用、最终用户及地区划分)-2026-2033年产业预测 巴西:全球市场份额和排名、总收入和需求预测(2025-2031年)

巴西:全球市场份额和排名、总收入和需求预测(2025-2031年) 全球铝焊硬焊市场按产品类型、最终用途产业和地区划分-预测至2032年铜焊焊合金:全球市占率排名、总销售额和需求预测(2025-2031年)

全球铝焊硬焊市场按产品类型、最终用途产业和地区划分-预测至2032年铜焊焊合金:全球市占率排名、总销售额和需求预测(2025-2031年) 银基和金基焊焊材料市场按产品类型(银基焊焊材料、金基焊焊材料)、应用(暖通空调和冷冻、汽车、航太、医疗、电气和电子等)和地区划分,2025 年至 2033 年

银基和金基焊焊材料市场按产品类型(银基焊焊材料、金基焊焊材料)、应用(暖通空调和冷冻、汽车、航太、医疗、电气和电子等)和地区划分,2025 年至 2033 年