|

市场调查报告书

商品编码

1850009

低温冷冻机:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Cryocooler - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

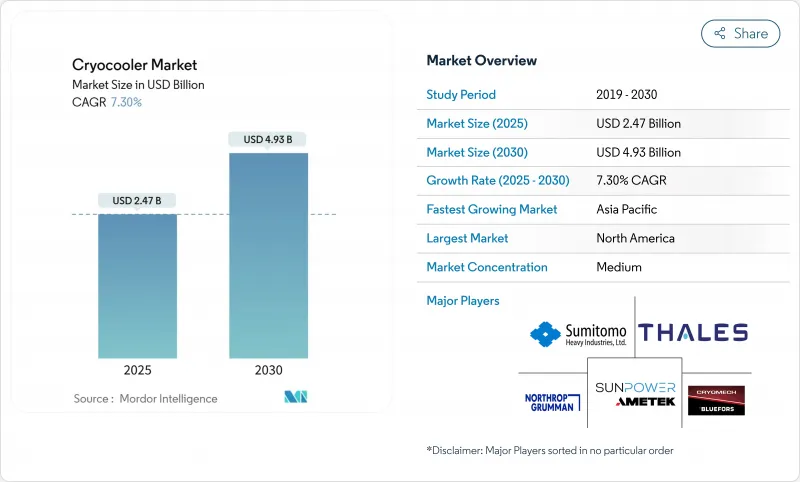

预计到 2025 年,低温冷冻机市场规模将达到 34.7 亿美元,到 2030 年将达到 49.3 亿美元,2025 年至 2030 年的复合年增长率为 7.30%。

太空探勘、量子运算和无氦磁振造影设备的需求不断增长,推动了这一发展趋势。长寿命空间低温冷冻机为不断扩展的小型卫星卫星群提供动力,而低于4K的稀释预冷器正成为量子处理器不可或缺的组件。在医疗保健领域,新兴经济体二线城市的医院正在部署氦光学磁振造影系统,该系统采用密封封闭回路型冷却,以避免供应链接触液态氦。在应用层级,军用红外线感测器和下一代光电检测器的普及,加速了对兼顾尺寸、重量和功耗(SWaP)限制的紧凑型斯特林冷却器的需求。

全球低温冷冻机市场趋势与洞察

对士兵佩戴式装备红外线感测器的紧凑型低温冷却装置的需求激增

军事现代化项目推动了对紧凑型低温冷却器的需求,以便在不增加士兵负担的情况下冷却红外线焦平面阵列。欧洲防务基金对先进光电检测器的需求凸显了对士兵可用系统的持续投资。像SOFRADIR这样的供应商正在改进能够承受超过100K高温的动作温度检测器架构,从而降低冷却器的功耗。对活塞密封涂层耐磨性的持续研究提高了线性压缩机的运作週期。最后,印度和阿联酋的国防抵销政策正在降低单位成本,并建立国内製造基地,这可能会改变传统的出口方向。

快速扩张的小型卫星星系需要长寿命的空间低温冷冻机。

为了支援高光谱遥测成像器和科学载荷,小型卫星越来越多地配备机械冷却器,这要求它们在多年任务期间保持焦平面温度恆定在 90 K 或更低。欧洲太空总署 (ESA) 的焦耳-汤姆森冷却器技术的进步实现了无振动运行,这对光学稳定性至关重要。诺斯罗普·格鲁曼公司已在轨道上部署了 12 台长寿命脉衝管和斯特林冷却器,证明了其使用寿命可超过 12 年。 《全球探索蓝图》强调了低温系统在维持月球住家周边设施和火星设施运作方面的重要作用。美国太空总署 (NASA) 2026 财年预算累计83 亿美元的探勘经费,其中一部分用于资助先进的低温推进剂管理系统,而这依赖于可靠的低温硬体。

重量低于 5 公斤的平台,其热升限值应为 10 瓦或更低。

由于扫掠体积减小,小型化冷却器在热升力方面面临物理限制,这给士兵便携式红外线瞄准器和立方卫星有效载荷的设计者带来了挑战。即使是微米级的密封磨损也会在现场部署数月内降低斯特林效率。对小型化自由活塞斯特林装置的研究表明其具有优势,但需要在振动和冷却功率之间进行权衡。 NASA 的评估也反映了在轨立方体立方卫星,它们必须在严格的质量-功率范围内运作。

细分市场分析

到2024年,线性斯特林製冷机将占据低温冷冻机市场63%的份额,这反映了其在国防感测器系统中的长期应用。脉衝管製冷机虽然体积较小,但预计到2030年将以9.4%的复合年增长率成长,因为无振动运作对于量子硬体至关重要。因此,低温冷冻机产业正在改进回收材料和惯性管设计,以提高脉衝管的效率并保持可靠性。同时,吉福德-麦克马洪製冷机和混合型GM-JT製冷机(例如住友的RJT-100)在液化天然气和超导性磁铁中承担着重要的热提升任务。总体而言,这种竞争表明低温冷冻机市场正在逐步向低振动技术转型,以适应对噪音敏感的有效载荷的出现。

虽然第二代布雷顿循环解决方案仍在满足航太子系统对特殊压力比的需求,但其成本和复杂性阻碍了其广泛应用。模组化设计理念允许製造商将斯特林或脉衝管核心部件替换到通用压缩机壳体中,从而缩短开发时间并满足多样化的专案需求。这种转变表明,随着低温冷冻机市场应用配置的不断演变,原始设备製造商 (OEM) 正在寻求与平台无关的策略,以保护其利润空间。

到2024年,5万至10万开尔文级的应用将占总收入的42%,这主要得益于磁振造影(MRI)、红外线感测和卫星设备等领域的应用。相反,随着毫开尔文级温度支援超导量子位元的运行,1至2万开尔文级应用市场将在2030年前以9.2%的复合年增长率成长。这项转变将推动针对高导电高导电性铅基再生基质的超导性,以维持毫开尔文级的温度梯度。液态氮级(77K)冷却仍是实验室低温恆温器的主流,但由于市场需求趋于成熟,其成长速度有所放缓。随着量子晶圆厂扩大其试验生产线,预计1至2万开尔文级应用的低温冷冻机市场规模将进一步扩大,也凸显了氦经济型架构的战略必要性。

相分离冷冻机等创新技术,仅需极少量的氦-3即可实现585 mK的基准温度,这为在不严重影响同位素需求的前提下实现商业性化生产提供了一条途径。同时,太空任务需要20-40 K范围内的长期稳定温度来冷却中红外线检测器。

低温冷冻机市场按低温冷冻机类型(斯特林式、吉福德-麦克马洪式、脉衝管式、焦耳-汤姆森、布雷顿式)、温度范围(1K-20K 及其他)、运行循环(闭合迴路、开放回路)、热交换器类型(再生式及其他)、终端用户行业(航太、医疗保健、军事及其他)和地区进行细分。所有细分市场的规模和预测均以美元计价。

区域分析

2024年,北美地区维持了38%的销售额,这主要得益于美国国防研发部门投入的44亿美元,用于研发需要嵌入式低温冷冻机冷却器的下一代感测器有效载荷。美国国家航空暨太空总署(NASA)83亿美元的探勘系统预算也为长寿命太空冷却器的研发提供了资金。加拿大魁北克的航太产业丛集供应压缩机子组件,而墨西哥的加工出口走廊则支援再生器外壳的精密加工。美国财政部于2024年禁止外国投资中国製造的量子冷却设备,这促使美国国内代工厂增加了相关投资并成立了更多合资企业。

亚太地区以9.5%的复合年增长率实现最快成长,主要得益于中国的液化天然气低温技术计画和2024年产业政策带来的动态进展。宁波低温发电厂展示了中国从进口液化天然气中回收低温牛酪油的能力。日本在半导体活化补贴的推动下,推动了产业技术综合研究所(AIST)与布鲁福德公司(Bluefords)的稀释冷冻机合作计画。印度的国防抵销规则要求外国主承包商在当地采购零件,从而加速了小型化斯特林瞄准军事光学器件新兴製造生态系统的发展。

由于欧洲太空总署 (ESA) 的任务以及由公共资金支持的 EuroQuIC 联盟的量子蓝图,欧洲保持着强大的市场份额。德国的精密工程部门正在研发再生设备,而法国泰雷兹公司则将脉衝管冷却器整合到太空相机中。欧洲防务基金 2025 年的征集主题确保了对士兵佩戴式热成像仪的持续需求,而高效冷却对于此类设备至关重要。英国与技术设施委员会 (STFC) 正在利用官民合作关係扩大氦气回收基础设施,以实现英国的净零排放目标。对俄罗斯航太进口的製裁正在促使零件采购转向欧盟供应商,从而略微推高了低温冷冻机市场的平均售价。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 士兵携带装备中红外线感测器的紧凑型低温冷却需求激增

- 快速扩张的小型卫星星座需要长寿命太空冰箱

- 新兴国家二线城市核磁共振成像系统安装量不断增加

- 北美和中国的液化抑低尖峰负载计划推动了大型通用汽车系统的建设。

- 量子技术的规模化应用需要低于 4K 的稀释和预冷却设备。

- 国防抵销计划促进国内生产(印度、阿联酋)

- 市场限制

- 重量低于 5 公斤的平台,其热升限值应小于 10 瓦。

- 氦-3供应瓶颈适用于低于1K的应用

- 机载光电有效载荷的振动声噪音不合规性

- 对于热提升超过 100 W 的脉衝管,其资本投资溢价高于通用汽车。

- 价值/供应链分析

- 监管环境

- 技术展望

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

第五章 市场规模与成长预测

- 按低温冷冻机类型

- 英镑

- 吉福德·麦克马洪

- 脉衝管

- 焦耳-汤姆森

- 布雷顿

- 按温度范围

- 1K~20K

- 20K~77K

- 77K~200K

- 超过20万

- 透过操作週期

- 闭合迴路

- 开放回路

- 按热交换器类型

- 再生型

- 恢復类型

- 最终用户

- 宇宙

- 卫生保健

- 军事与国防

- 商业和工业

- 能源与电力

- 运输

- 研究与学术

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 非洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Sumitomo Heavy Industries Ltd.

- Northrop Grumman Corporation

- Cryomech Inc.(Bluefors Oy)

- Thales Group

- Sunpower Inc.(AMETEK)

- Ricor Systems

- Stirling Cryogenics BV

- Chart Industries Inc.

- Creare LLC

- Air Liquide Advanced Technologies

- Janis ULT Cryogenics

- Advanced Research Systems Inc.

- Eaton Corp. PLC

- Cobham Ltd.

- Honeywell Aerospace

- Linde Cryogenics

- Lockheed Martin(SCD)

- Absolut System

- CryoSpectra GmbH

- DH Instruments(Addi-data)

第七章 市场机会与未来展望

The cryocooler market stood at USD 3.47 billion in 2025 and is forecast to reach USD 4.93 billion by 2030, advancing at a 7.30% CAGR during 2025-2030.

Rising demand from space exploration, quantum computing and helium-free MRI installations anchors the underlying growth trajectory . Long-life space cryocoolers enable expanding small-satellite constellations, while sub-4 K dilution pre-coolers are becoming indispensable for quantum processors . In healthcare, hospitals in tier-2 cities across emerging economies deploy helium-light MRI systems that rely on sealed, closed-loop cooling to sidestep supply-chain exposure to liquid helium . At an application level, the proliferation of soldier-borne infrared (IR) sensors and next-generation optronic detectors is accelerating demand for compact Stirling coolers that balance size, weight and power (SWaP) constraints.

Global Cryocooler Market Trends and Insights

Surge in demand for compact cryogenic cooling for IR sensors in soldier-borne devices

Military modernization programs are intensifying the need for miniaturized cryocoolers that cool IR focal-plane arrays without burdening soldiers with excess weight. European Defence Fund calls for advanced optronic detectors, underscoring enduring investment in soldier systems. Suppliers such as SOFRADIR are improving High-Operating-Temperature detector architectures that tolerate >100 K, thereby shrinking cooler power budgets. Ongoing wear-resistance research into piston-seal coatings enables longer duty cycles for linear compressors SPIE. Finally, defense offset rules in India and UAE are building domestic production bases that could lower unit costs and reshape traditional export flows.

Rapid expansion of small-satellite constellations requiring long-life space cryocoolers

SmallSats increasingly integrate mechanical coolers to support hyperspectral imagers and science payloads that demand consistent sub-90 K focal-plane temperatures throughout multiyear missions . ESA's Joule-Thomson cooler advances offer vibration-free operation essential for optical stability . Northrop Grumman has already fielded 12 long-life pulse-tube and Stirling units on orbit, proving lifetime goals beyond 12 years . The Global Exploration Roadmap highlights the role of cryogenic systems in sustaining lunar habitats and Mars assets. NASA's FY 2026 budget earmarks USD 8.3 billion for exploration, part of which funds advanced cryogenic propellant management that depends on reliable low-temperature hardware .

Heat-lift limitations below 10 W in <5 kg platforms

Miniaturized coolers face physical limits where decreasing swept volumes constrain heat-lift, challenging designers of soldier-portable IR sights and CubeSat payloads . Even micron-scale seal wear can degrade Stirling efficiency within months of field deployment. Research into miniature free-piston Stirling devices shows gains but still trades off between vibration and cooling power . NASA's assessments echo the same dilemma for on-orbit CubeSats that must operate within tight mass-power envelopes .

Other drivers and restraints analyzed in the detailed report include:

- Growing MRI system installations in emerging economies' tier-2 cities

- Quantum-tech scale-up needs sub-4 K dilution pre-coolers

- Helium-3 supply bottleneck for sub-1 K applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Linear Stirling units accounted for 63% of cryocooler market share in 2024, reflecting legacy adoption across defense sensor suites. Pulse-tube coolers, although representing a smaller slice, are projected to grow at 9.4% CAGR to 2030 as vibration-free operation becomes critical for quantum hardware. The cryocooler industry is therefore tuning regenerator materials and inertance tube designs that boost pulse-tube efficiency while retaining reliability. Meanwhile, Gifford-McMahon and hybrid GM-JT devices like Sumitomo's RJT-100 serve large heat-lift duties in LNG and superconducting magnets . Overall, this rivalry signals a gradual rebalancing of the cryocooler market toward low-vibration technologies that accommodate emerging noise-sensitive payloads.

Second-generation Brayton cycle solutions continue to address aerospace subsystems with unique pressure-ratio demands; however, cost and complexity cap broader uptake. Modular design philosophies increasingly allow manufacturers to swap Stirling or pulse-tube cores into common compressor housings, shortening development times and fulfilling diversified program needs. The shift illustrates how OEMs pursue platform-agnostic strategies that protect margins as application mix evolves within the cryocooler market.

Applications operating between 50 K and 100 K held 42% revenue in 2024, underpinned by MRI, IR sensing and satellite instruments. Conversely, the 1-20 K niche is expanding at a 9.2% CAGR through 2030 as millikelvin regimes underpin superconducting qubit operation. This shift propels targeted R&D into high-conductivity lead-based regenerator matrices that maintain temperature gradients at millikelvin levels. Liquid-nitrogen class (77 K) cooling still dominates laboratory cryostats, yet its growth lags due to maturing demand. The cryocooler market size for 1-20 K applications is forecast to widen as quantum fabs scale pilot lines, reinforcing the strategic imperative for helium-economizing architectures.

Innovations such as the phase-separation refrigerator achieving 585 mK base with tiny helium-3 inventory highlight a path to unlock commercial throughput without crippling isotope demand. Simultaneously, space missions require long-term stability in the 20-40 K range to cool mid-infrared detectors; pulse-tube coolers integrated with Stirling precoolers remain preferred solutions in those regimes.

The Cryocooler Market is Segmented by Cryocooler Type (Stirling, Gifford-McMahon, Pulse-Tube, Joule-Thomson, Brayton) Temperature Range (1 K - 20 K and More), Operating Cycle (Closed-Loop, Open-Loo), Heat-Exchanger Type (Regenerative and More), End-User Vertical (Space, Healthcare, Military, and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Segments.

Geography Analysis

North America retained 38% of 2024 revenue on the back of USD 4.4 billion in U.S. defense R&D that targets next-generation sensor payloads requiring embedded cryocoolers . NASA's USD 8.3 billion exploration systems budget also channels funds to long-life space coolers . Canada's aerospace cluster in Quebec supplies compressor sub-assemblies, while Mexico's maquiladora corridor supports precision machining for regenerator housings. The U.S. Treasury's 2024 rules barring outbound investment in Chinese quantum cooling triggered an uptick in domestic foundry commitments and joint ventures .

Asia-Pacific posts the fastest growth at 9.5% CAGR, led by China's LNG cold-energy initiatives and quantum drive under its 2024 industrial policy. Ningbo's cold-energy power plant demonstrates national capability to harvest cryogenic exergy from imported LNG. Japan pushes forward via AIST and Bluefors' dilution refrigerator partnership, bolstered by semiconductor revitalisation grants. India's defense-offset rules obligate foreign primes to source components locally, accelerating a nascent manufacturing ecosystem for miniature Stirlings targeting soldier optics.

Europe maintains robust share courtesy of ESA missions and the EuroQuIC consortium's public-funded quantum roadmap. Germany's precision engineering sector underwrites regenerator R&D, while France's Thales integrates pulse-tube coolers into space cameras. The European Defence Fund's 2025 call topics ensure recurring demand for soldier-borne thermal imagers that require efficient cooling. The UK's STFC campus leverages public-private partnerships to expand helium-recovery infrastructure, aligning with national net-zero targets. Sanctions on Russian aerospace imports reroute component sourcing towards intra-EU suppliers, subtly lifting average selling prices within the cryocooler market.

- Sumitomo Heavy Industries Ltd.

- Northrop Grumman Corporation

- Cryomech Inc. (Bluefors Oy)

- Thales Group

- Sunpower Inc. (AMETEK)

- Ricor Systems

- Stirling Cryogenics BV

- Chart Industries Inc.

- Creare LLC

- Air Liquide Advanced Technologies

- Janis ULT Cryogenics

- Advanced Research Systems Inc.

- Eaton Corp. PLC

- Cobham Ltd.

- Honeywell Aerospace

- Linde Cryogenics

- Lockheed Martin (SCD)

- Absolut System

- CryoSpectra GmbH

- DH Instruments (Addi-data)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for compact cryogenic cooling for IR sensors in soldier-borne devices

- 4.2.2 Rapid expansion of small-satellite constellations requiring long-life space cryocoolers

- 4.2.3 Growing MRI system installations in emerging economies tier-2 cities

- 4.2.4 LNG peak-shaving projects in North America & China driving large-capacity GM systems

- 4.2.5 Quantum-tech scale-up needs sub-4 K dilution-pre-coolers

- 4.2.6 Defense offset programs fostering domestic cryocooler production (India, UAE)

- 4.3 Market Restraints

- 4.3.1 Heat-lift limitations below 10 W in <5 kg platforms

- 4.3.2 Helium-3 supply bottleneck for sub-1 K applications

- 4.3.3 Vibro-acoustic noise non-compliance for airborne EO payloads

- 4.3.4 Capex premium of pulse-tube over GM for >100 W heat-lift

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Value Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cryocooler Type

- 5.1.1 Stirling

- 5.1.2 Gifford-McMahon

- 5.1.3 Pulse-Tube

- 5.1.4 Joule-Thomson

- 5.1.5 Brayton

- 5.2 By Temperature Range

- 5.2.1 1 K- 20 K

- 5.2.2 20 K - 77 K

- 5.2.3 77 K -200 K

- 5.2.4 > 200 K

- 5.3 By Operating Cycle

- 5.3.1 Closed-Loop

- 5.3.2 Open-Loop

- 5.4 By Heat-Exchanger Type

- 5.4.1 Regenerative

- 5.4.2 Recuperative

- 5.5 By End-user Vertical

- 5.5.1 Space

- 5.5.2 Healthcare

- 5.5.3 Military and Defense

- 5.5.4 Commercial and Industrial

- 5.5.5 Energy and Power

- 5.5.6 Transportation

- 5.5.7 Research and Academic

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Netherlands

- 5.6.3.7 Russia

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 ASEAN

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.2 Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Recent Developments)

- 6.4.1 Sumitomo Heavy Industries Ltd.

- 6.4.2 Northrop Grumman Corporation

- 6.4.3 Cryomech Inc. (Bluefors Oy)

- 6.4.4 Thales Group

- 6.4.5 Sunpower Inc. (AMETEK)

- 6.4.6 Ricor Systems

- 6.4.7 Stirling Cryogenics BV

- 6.4.8 Chart Industries Inc.

- 6.4.9 Creare LLC

- 6.4.10 Air Liquide Advanced Technologies

- 6.4.11 Janis ULT Cryogenics

- 6.4.12 Advanced Research Systems Inc.

- 6.4.13 Eaton Corp. PLC

- 6.4.14 Cobham Ltd.

- 6.4.15 Honeywell Aerospace

- 6.4.16 Linde Cryogenics

- 6.4.17 Lockheed Martin (SCD)

- 6.4.18 Absolut System

- 6.4.19 CryoSpectra GmbH

- 6.4.20 DH Instruments (Addi-data)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2025-2033 年低温冷却器市场报告(按类型、热交换器类型、运作週期、温度、应用和地区)

2025-2033 年低温冷却器市场报告(按类型、热交换器类型、运作週期、温度、应用和地区) 低温冷冻机市场按分销管道、冷却能力、类型、应用和最终用户产业划分-2025-2032年全球预测

低温冷冻机市场按分销管道、冷却能力、类型、应用和最终用户产业划分-2025-2032年全球预测 全球低温冷冻机市场(至 2030 年)按低温冷冻机类型、产品类别、热交换器、运转週期、温度范围和应用划分

全球低温冷冻机市场(至 2030 年)按低温冷冻机类型、产品类别、热交换器、运转週期、温度范围和应用划分 2025年低温冷冻机全球市场报告

2025年低温冷冻机全球市场报告 全球低温冷却器市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球低温冷却器市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测 低温冷冻机市场规模、份额和增长分析(按组件、热交换器类型、运行週期、类型、应用和地区)- 2025-2032 年行业预测

低温冷冻机市场规模、份额和增长分析(按组件、热交换器类型、运行週期、类型、应用和地区)- 2025-2032 年行业预测 低温冷冻机市场规模、份额、趋势分析报告:按热交换器类型、按应用、按地区、细分市场预测,2025-2030

低温冷冻机市场规模、份额、趋势分析报告:按热交换器类型、按应用、按地区、细分市场预测,2025-2030 全球低温冷冻机市场(2024-2028)

全球低温冷冻机市场(2024-2028) 低温冷却器市场(运作週期:恢復循环和再生循环)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测

低温冷却器市场(运作週期:恢復循环和再生循环)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测 到 2030 年低温冷冻机市场预测:按类型、热交换方法、产品、运作週期、应用、最终用户和地区进行全球分析

到 2030 年低温冷冻机市场预测:按类型、热交换方法、产品、运作週期、应用、最终用户和地区进行全球分析