|

市场调查报告书

商品编码

1850059

智慧采矿:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Smart Mining - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

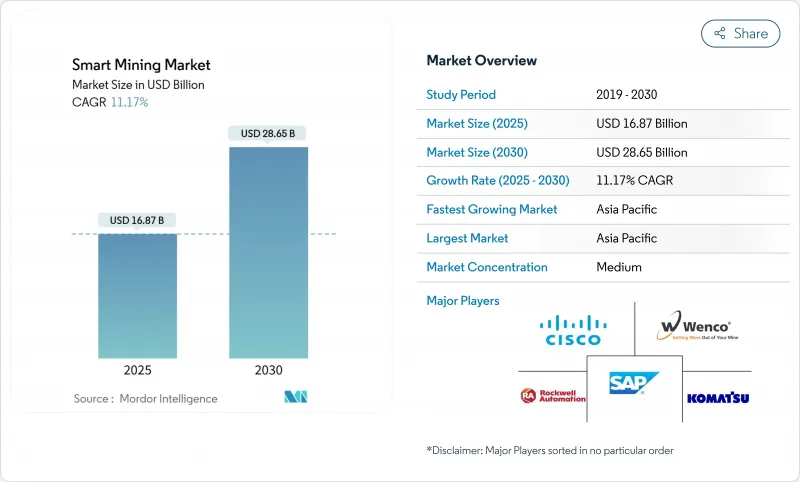

预计2025年智慧采矿市场规模将达168.7亿美元,2030年将达286.5亿美元,复合年增长率为11.2%。

快速数位化正在重塑矿山规划、车队管理和矿物加工,帮助营运商应对矿石品位下降、安全要求更严格以及脱碳目标。自主运输、物联网预测性维护和私有 5G 网路能够持续提高生产力并降低营运风险。锂、镍和稀土的需求不断增长,推动了对互联设备的投资,以最大限度地提高回收率。全球自动化供应商与细分矿业技术专家之间的伙伴关係,催生了整合平台,整合了从矿场到港口的数据。

全球智慧采矿市场趋势与洞察

关键矿物需求激增

国际能源总署 (IEA) 预测,到 2040 年,锂需求将增加 40 倍以上。矿业公司正在加速扩建计划和探勘宣传活动依靠联网钻机和云端基础的地质模型来寻找高等级的矿床。澳洲、加拿大和美国政府都推出了奖励,以降低采矿自动化成本,并将生产集中在安全的供应链中。数位双胞胎有助于模拟加工厂,即时调整试剂剂量和能源投入,从而提高回收率并降低成本。随着买家签订多年的承购协议,营运商越来越多地将智慧设备的部署视为一项策略性投资,而不是一项可自由支配的开支。

采用自动驾驶交通工具

日本小松公司的 FrontRunner 卡车自推出以来已运输了超过 20 亿吨物料,在铁矿石、铜和煤炭计划中展示了可靠的全天候运作。卡特彼勒将于 2024 年将这项技术扩展到 Lac Stone维吉尼亚采石场的中型 777 卡车,以展示其在大型矿场作业之外的适用性。力拓正在其皮尔巴拉矿山的高流量区域消除人际接触,淡水河谷正在布鲁克林研发全自动驾驶汽车,检验其安全性和成本效益。从 Wi-Fi 到私有 LTE 和 5G 的过渡将解决先前限制深矿和山区自动驾驶的延迟和覆盖范围差距。供应商现在正在将车队管理软体与车载感知感测器捆绑在一起,加速发达和发展中地区的采用。

资本支出和投资报酬率不确定性度高

综合自动化计划涉及感测器、软体、通讯和变更管理的多年支出,这使得小型企业难以融资。儘管电池金属需求强劲,但2024年的投资意愿疲软,显示经营团队在权衡相互竞争的优先事项时持谨慎态度。收益通常跨越采矿、加工和物流的各个环节,使净现值的计算变得复杂。分析师估计,到2030年,满足矿产需求将需要5.4兆美元,凸显了分阶段部署的重要性,这些部署在全面部署之前必须证明其回报。

細項分析

到 2024 年,智慧资产管理将占智慧采矿市场的 31.5%。这一领域利用感测器融合、人工智慧诊断和生命週期仪表板,以适度的投资实现快速节约。许多公司在六个月的试点期内将润滑监测盒和振动节点整合到运输卡车、破碎机和压碎机中,从而提高了大型计划的可靠性。自动运输和钻井是成长最快的解决方案,到 2030 年的复合年增长率为 11.5%,这标誌着一旦部署底层远端检测,将转向无人操作。数据管理和分析平台整合了来自车队、工厂和环境感测器的信息,使跨职能团队能够将原始数据转化为可操作的见解,以提高回收率并减少排放。安全和安保系统将受益于越来越多的要求持续人员追踪和地理围栏的法规。监控和视觉化仪表板透过显示预测警报和生产 KPI 来完成闭合迴路控制。从区块链可追溯性到矿石分选数位双胞胎等其他新工具完善了解决采矿业独特痛点的多样化产品组合。

智慧资产管理也成为永续性相关融资的门户,因为贷款机构可以根据环境契约检验设备效率提升。随着工厂经理看到计划外停机时间的显着减少,董事会委员会核准广泛采用自动钻机、斗轮挖掘机和远端操作铲运机。在感测器成本下降和5G网路覆盖强劲的推动下,由自动物料搬运解决方案带来的智慧采矿市场规模预计将在2025年至2030年间扩大4.7倍。早期采用者宣传基准週期时间的改进,鼓励竞争对手投资升级专案。平台供应商围绕可用性保证重写服务等级协议,并引入基于结果的定价机制,使技术支出与生产绩效保持一致。

到2024年,系统整合将贡献58.0%的业务收益,因为矿业公司难以将其专有的车队管理软体与传统的PLC、历史资料库和ERP套件连接起来。领先的自动化供应商正在将架构审核、光纤设计和网路安全增强功能捆绑到承包专案中,以降低现代化风险。託管服务预计将以12.2%的复合年增长率成长,对于那些更倾向于可预测的营运预算而非技术专长资本激增的公司来说,它具有吸引力。服务供应商营运远端营运中心,监控感测器健康状况,修补漏洞,并在一夜之间推送分析更新,减轻了现场工作人员的负担。工程和维护服务仍然至关重要,包括检验感测器位置、校准雷射雷达单元以及修復暴露在振动和灰尘中的边缘电脑机壳。

顾问公司主导数位化成熟度评估,与同业进行基准比较,并优先考虑快速见效的方案。训练部门将电工和机械师提升为能够解读状态监控仪錶板的数据技术人员。采矿设备、技术和服务 (METS) 产业的成长预计将在未来十年翻一番,这突显出从一次性硬体销售到定期服务合约的明显转变。随着订阅服务在全球范围内的扩展,智慧采矿託管服务市场预计到 2030 年将超过 42 亿美元。供应商现在保证零件供应和软体执行时间,从而将营运风险从矿主转移,并加强了长期伙伴关係关係。

智慧采矿市场报告按解决方案(智慧控制系统、智慧资产管理等)、服务类型(系统整合、咨询服务等)、采矿类型(地下采矿、露天采矿)、技术(物联网、人工智慧、分析等)和地区细分。

区域分析

预计到 2024 年,亚太地区将占据智慧采矿市场的 38.3%,到 2030 年的复合年增长率为 12.0%。中国正在利用其在锂、稀土和石墨加工方面的优势,为在自动运输和人工智慧驱动的选矿厂方面进行大量投资提供理由,这得益于《中国製造 2025》和「一带一路」倡议对垂直矿物运输的支持。澳洲拥有丰富的铁矿石和黄金蕴藏量,加上严格的安全法规,将推动其儘早采用珀斯的远端营运中心来管理数百公里外的车辆。日本和韩国优先考虑电池金属的供应链弹性,并资助机器人技术研究,这些研究将溢出到采矿应用领域。东南亚国协将在 2023 年获得 2,300 亿美元的外国直接投资,而印尼和菲律宾正在吸引资金用于从一开始就包含数位基础设施的镍和铜计划。

北美仍是技术强国,拥有感测器、分析和工业人工智慧供应商,同时也营运大型露天铜矿、金矿和油砂。加拿大的关键矿产策略加速了电动运输卡车和预测维修系统的采用,使该国成为永续采矿的领导者。美国正致力于确保国内锂、镍和稀土计划,并在能源部的津贴下在内华达州和亚利桑那州进行实验性自主钻探。墨西哥正在索诺拉州和萨卡特卡斯州扩大丛集发展,整合私人 LTE 和银和锂的模组化加工生产线。在联邦奖励和 ESG 相关融资的支持下,到 2030 年,北美智慧采矿市场预计将超过 63 亿美元。

欧洲正在强调负责任的采购和循环经济原则,加快数位化应用以减少排放并提高可追溯性。德国的原料策略推动其钾肥和建筑材料采石场采用基于区块链的认证和远端设备监控。斯堪的纳维亚半岛正在铁矿石和基底金属矿率先使用电池供电的地下车辆,并藉助丰富的水力发电来改善生命週期排放。在斯堪地那维亚,随着汽车製造商寻求稳定的供应,智利和秘鲁的待开发区铜矿投资正在復苏。智利计划在2032年在矿业领域投资657.1亿美元,私营5G将在偏远的阿塔卡马地区发挥关键作用。中东和非洲正在成为前沿地区,沙乌地阿拉伯的「2030愿景」将采矿业确定为重要的经济支柱,南非正在试点使用氢动力卡车为铂金矿运输,并基于人工智慧优化路线。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 自动驾驶汽车简介

- 利用物联网和人工智慧进行预测性维护

- 以安全为中心的监控需求

- 私有5G部署

- 永续发展相关融资

- 关键矿物需求激增

- 市场限制

- 资本支出和投资报酬率不确定性度高

- 旧有系统整合差距

- 网路安全漏洞

- 熟练的数位人才短缺

- 价值链分析

- 监管格局

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争的激烈程度

- 替代品的威胁

- 评估宏观经济趋势对市场的影响

- 投资分析

第五章市场规模及成长预测

- 按解决方案

- 智慧控制系统

- 智慧资产管理

- 安全与安保系统

- 资料管理与分析软体

- 监控和可见性

- 自主运输与挖掘

- 其他解决方案

- 按服务类型

- 系统整合

- 咨询服务

- 工程与维护

- 託管服务

- 按采矿类型

- 地下采矿

- 露天采矿

- 依技术

- 物联网(IoT)

- 人工智慧和分析

- 机器人与自动化

- 连接性(5G/LTE)

- 云端运算和边缘运算

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- ASEAN

- 澳洲和纽西兰

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd

- Caterpillar Inc.

- Cisco Systems Inc.

- Komatsu Ltd

- Epiroc AB

- Hexagon AB

- Sandvik AB

- Rockwell Automation Inc.

- SAP SE

- Trimble Inc.

- IBM Corporation

- Wenco International Mining Systems Ltd

- Symboticware Inc.

- MineExcellence

- Metso Outotec Oyj

- Siemens AG

- Hitachi Construction Machinery Co., Ltd.

- Honeywell International Inc.

- Schneider Electric SE

- Accenture plc

第七章 市场机会与未来展望

The smart mining market size stands at USD 16.87 billion in 2025 and is forecast to advance to USD 28.65 billion by 2030, reflecting an 11.2% CAGR.

Rapid digitalization is reshaping mine planning, fleet management and mineral processing as operators confront declining ore grades, stricter safety mandates and decarbonization targets. Autonomous haulage, IoT-enabled predictive maintenance, and private 5G networks deliver continuous productivity gains while lowering operating risk. Growing demand for lithium, nickel and rare earths bolsters investment in connected equipment that maximizes recovery rates. Partnerships between global automation vendors and niche mining-tech specialists foster integrated platforms that unify data from pit to port.

Global Smart Mining Market Trends and Insights

Critical-mineral demand surge

Global electrification drives unprecedented demand for lithium, cobalt, and rare earth elements, with the International Energy Agency projecting lithium demand to rise more than fortyfold by 2040. Miners expedite expansion projects and exploration campaigns that depend on connected drilling rigs and cloud-based geological models to locate higher-grade deposits. Governments in Australia, Canada, and the United States allocate incentives that lower the cost of automating extraction and concentrate production within secure supply chains. Digital twins help simulate processing plants that adjust reagent dosage and energy input in real time, cutting costs while improving recovery. As buyers sign multi-year offtake agreements, operators treat smart-equipment roll-outs as strategic investments rather than discretionary spending.

Autonomous haulage adoption

Komatsu's FrontRunner trucks have moved more than 2 billion tons of material since launch, proving consistent 24/7 availability in iron ore, copper, and coal projects. Caterpillar extended the technology to mid-range 777 trucks at Luck Stone's Virginia quarry during 2024, demonstrating applicability beyond mega-pit operations. Rio Tinto eliminated human exposure to high-traffic zones at its Pilbara mines, while Vale committed to fully autonomous fleets at Brucutu, validating safety and cost benefits. Transition from Wi-Fi to private LTE or 5G resolves latency and coverage gaps that once limited autonomous haulage in deep pits or mountainous terrains. Suppliers now bundle fleet management software with on-board perception sensors, accelerating adoption across both developed and developing regions.

High CAPEX and ROI uncertainty

Total automation projects involve multi-year outlays for sensors, software, communications, and change management that smaller firms struggle to finance. Weak investment appetite in 2024, despite strong battery-metal demand, reveals caution as executives weigh competing priorities. Benefits often span mining, processing and logistics silos, complicating net-present-value calculations. Analysts estimate the sector needs USD 5.4 trillion by 2030 to satisfy mineral demand, magnifying the importance of phased roll-outs that prove payback before full-site deployment.

Other drivers and restraints analyzed in the detailed report include:

- IoT-AI predictive maintenance

- Private 5G roll-outs

- Legacy-system integration gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart asset management held a commanding 31.5% share of the smart mining market in 2024 as operators prioritized uptime and cost control before expanding to full autonomy. The segment leverages sensor fusion, AI diagnostics, and lifecycle dashboards that drive quick savings with moderate investment. Many firms integrate lubrication-monitoring cartridges and vibration nodes on haul trucks, mills, and crushers within six-month pilots, building confidence for larger projects. Autonomous haulage and drilling ranks as the fastest-growing solution with an 11.5% CAGR through 2030, signalling a shift toward crewless operations once foundational telemetry is in place. Data management and analytics platforms unify information from fleets, plants, and environmental sensors, allowing cross-functional teams to turn raw data into actionable insights that boost recovery rates and lower emissions. Safety and security systems benefit from tightening regulations that require continuous personnel tracking and geofencing. Monitoring and visualization dashboards complete closed-loop control by displaying predictive alerts alongside production KPIs. Other emerging tools, from blockchain traceability to ore-sorting digital twins, round out a diverse portfolio that addresses mine-specific pain points.

Smart asset management also acts as the entry point for sustainability-linked financing because lenders can verify equipment efficiency gains against environmental covenants. As plant managers witness tangible reductions in unplanned downtime, board committees approve wider deployment of autonomous drill rigs, bucket-wheel excavators, and remote-operated LHDs. The smart mining market size attributed to autonomous haulage solutions is forecast to expand 4.7 times between 2025 and 2030, driven by falling sensor costs and robust 5G coverage. Early adopters publicize benchmark cycle-time improvements, spurring competitors to invest in upgrade programs. Platform vendors rewrite service-level agreements around guaranteed availability, introducing outcome-based pricing that aligns technology spending with production results.

System integration generated 58.0% of service revenue in 2024 as miners grapple with connecting proprietary fleet-management software to legacy PLCs, historian databases, and ERP suites. Large automation vendors bundle architecture audits, fiber-optic design, and cybersecurity hardening into turnkey programs that de-risk modernization. Managed services, forecast to grow at a 12.2% CAGR, appeal to firms that prefer predictable operating budgets over capital spikes for technology expertise. Providers run remote operations centers that monitor sensor health, patch vulnerabilities, and push analytics updates overnight, lowering the burden on site staff. Engineering and maintenance services remain essential for validating sensor placement, calibrating LIDAR units, and repairing edge-compute enclosures exposed to vibration and dust.

Consulting firms lead digital-maturity assessments that benchmark sites against industry peers and prioritize quick wins. Training divisions upskill electricians and mechanics into data technicians who decode condition-monitoring dashboards. Growth of the mining equipment, technology, and services (METS) sector, expected to double this decade, underscores the pivot from one-off hardware sales to recurring service contracts. The smart mining market size of managed services is poised to exceed USD 4.2 billion by 2030 as subscription offerings scale globally. Vendors now guarantee parts availability and software uptime, transferring operational risk away from mine owners and reinforcing long-term partnerships.

The Smart Mining Market Report is Segmented by Solution (Smart Control Systems, Smart Asset Management, and More), Service Type (System Integration, Consulting Service, and More), Mining Type (Underground Mining and Surface (Open-Pit) Mining), Technology (Internet of Things (IoT), Artificial Intelligence and Analytics, and More), and Geography.

Geography Analysis

Asia-Pacific maintained a 38.3% share of the smart mining market in 2024 and is set to deliver a 12.0% CAGR to 2030. China leverages its dominance in lithium, rare earth and graphite processing to justify heavy investment in autonomous haulage and AI-driven concentrators, supported by Made in China 2025 and the Belt and Road mineral verticals. Australia combines vast iron ore and gold reserves with stringent safety regulation to foster early adoption of remote-operating centers in Perth that manage fleets hundreds of kilometers away. Japan and South Korea prioritize supply-chain resilience for battery metals and fund robotics research that spills into mining applications. ASEAN nations secured USD 230 billion in 2023 FDI, with Indonesia and the Philippines drawing capital for nickel and copper projects that embed digital infrastructure from day one.

North America remains a technology powerhouse, hosting suppliers of sensors, analytics and industrial AI while operating large-scale open-pit copper, gold and oil-sands mines. Canada's Critical Minerals Strategy accelerates deployment of electrified haul trucks and predictive maintenance systems, positioning the country as a sustainable mining leader. The United States focuses on securing domestic lithium, nickel and rare earth projects; Nevada and Arizona host pilot autonomous drills under Department of Energy grants. Mexico expands cluster developments in Sonora and Zacatecas that integrate private LTE and modular processing lines for silver and lithium. The smart mining market size for North America is expected to cross USD 6.3 billion by 2030 on the back of federal incentives and ESG-linked financing.

Europe emphasizes responsible sourcing and circular-economy principles, accelerating digital adoption to cut emissions and improve traceability. Germany's raw materials strategy promotes blockchain-based provenance and remote equipment monitoring for domestic potash and construction-material quarries. Scandinavia pioneers battery-electric underground fleets for iron ore and base-metal mines, backed by abundant hydropower that enhances lifecycle emissions profiles. South America witnesses a resurgence of greenfield copper investments in Chile and Peru as automakers seek stable supplies; Chile plans USD 65.71 billion in mining investment through 2032, with private 5G pivotal in remote Atacama sites. Middle East and Africa emerge as frontier regions, with Saudi Arabia's Vision 2030 designating mining a primary economic pillar and South Africa piloting hydrogen haulage trucks for platinum mines that integrate AI route optimization.

- ABB Ltd

- Caterpillar Inc.

- Cisco Systems Inc.

- Komatsu Ltd

- Epiroc AB

- Hexagon AB

- Sandvik AB

- Rockwell Automation Inc.

- SAP SE

- Trimble Inc.

- IBM Corporation

- Wenco International Mining Systems Ltd

- Symboticware Inc.

- MineExcellence

- Metso Outotec Oyj

- Siemens AG

- Hitachi Construction Machinery Co., Ltd.

- Honeywell International Inc.

- Schneider Electric SE

- Accenture plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Autonomous haulage adoption

- 4.2.2 IoT-AI predictive maintenance

- 4.2.3 Safety-driven monitoring demand

- 4.2.4 Private 5G roll-outs

- 4.2.5 Sustainability-linked financing

- 4.2.6 Critical-mineral demand surge

- 4.3 Market Restraints

- 4.3.1 High CAPEX and ROI uncertainty

- 4.3.2 Legacy-system integration gaps

- 4.3.3 Cyber-security vulnerabilities

- 4.3.4 Skilled digital-talent shortage

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Smart Control Systems

- 5.1.2 Smart Asset Management

- 5.1.3 Safety and Security Systems

- 5.1.4 Data Mgmt and Analytics Software

- 5.1.5 Monitoring and Visualization

- 5.1.6 Autonomous Haulage and Drilling

- 5.1.7 Other Solutions

- 5.2 By Service Type

- 5.2.1 System Integration

- 5.2.2 Consulting Services

- 5.2.3 Engineering and Maintenance

- 5.2.4 Managed Services

- 5.3 By Mining Type

- 5.3.1 Underground Mining

- 5.3.2 Surface (Open-Pit) Mining

- 5.4 By Technology

- 5.4.1 Internet of Things (IoT)

- 5.4.2 Artificial Intelligence and Analytics

- 5.4.3 Robotics and Automation

- 5.4.4 Connectivity (5G/LTE)

- 5.4.5 Cloud and Edge Computing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN

- 5.5.3.6 Australia and New Zealand

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ABB Ltd

- 6.4.2 Caterpillar Inc.

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Komatsu Ltd

- 6.4.5 Epiroc AB

- 6.4.6 Hexagon AB

- 6.4.7 Sandvik AB

- 6.4.8 Rockwell Automation Inc.

- 6.4.9 SAP SE

- 6.4.10 Trimble Inc.

- 6.4.11 IBM Corporation

- 6.4.12 Wenco International Mining Systems Ltd

- 6.4.13 Symboticware Inc.

- 6.4.14 MineExcellence

- 6.4.15 Metso Outotec Oyj

- 6.4.16 Siemens AG

- 6.4.17 Hitachi Construction Machinery Co., Ltd.

- 6.4.18 Honeywell International Inc.

- 6.4.19 Schneider Electric SE

- 6.4.20 Accenture plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

智慧采矿市场规模、份额、趋势及预测(按类型、组件、自动化设备及地区划分),2026-2034年

智慧采矿市场规模、份额、趋势及预测(按类型、组件、自动化设备及地区划分),2026-2034年 智慧采矿市场规模、份额和成长分析(按类型、组件和地区划分)-2026-2033年产业预测

智慧采矿市场规模、份额和成长分析(按类型、组件和地区划分)-2026-2033年产业预测 智慧采矿市场分析及2034年预测:类型、产品、服务、技术、组件、应用、设备、解决方案、最终用户

智慧采矿市场分析及2034年预测:类型、产品、服务、技术、组件、应用、设备、解决方案、最终用户 智慧采矿市场 - 全球产业规模、份额、趋势、机会和预测(按解决方案、服务类型、采矿类型、地区和竞争细分,2020-2030 年)

智慧采矿市场 - 全球产业规模、份额、趋势、机会和预测(按解决方案、服务类型、采矿类型、地区和竞争细分,2020-2030 年) 智慧采矿市场机会、成长动力、产业趋势分析与预测 2025 - 2034

智慧采矿市场机会、成长动力、产业趋势分析与预测 2025 - 2034 矿山规划解决方案市场报告:2030 年趋势、预测与竞争分析

矿山规划解决方案市场报告:2030 年趋势、预测与竞争分析 智慧矿业全球市场

智慧矿业全球市场