|

市场调查报告书

商品编码

1850124

美国塑胶包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)US Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

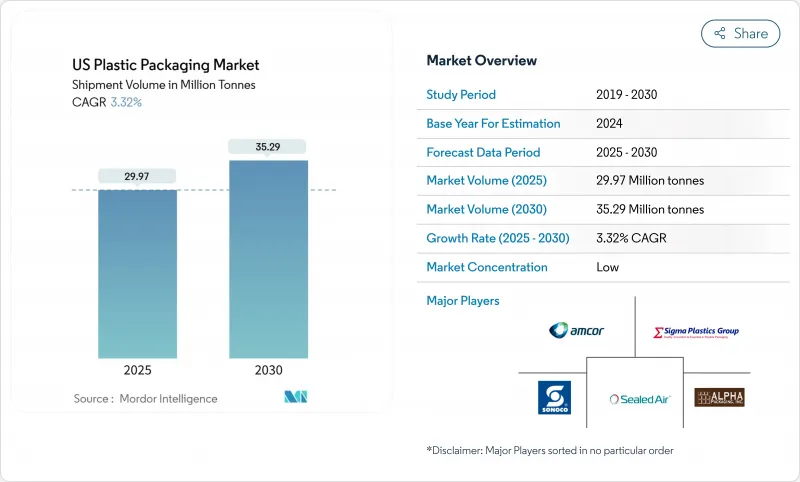

预计到 2025 年,美国塑胶包装市场规模将达到 2,997 万吨,到 2030 年将达到 3,529 万吨,复合年增长率为 3.32%。

需求韧性主要得益于电子商务小包裹的扩展、食品饮料便捷包装形式的普及,以及品牌商致力于在其核心库存产品中整合25%的消费后回收(PCR)树脂。加州SB 54法案和华盛顿州《再生资源法案》等监管框架正在加速设计向更轻薄、单一材料复合材料和繫绳式封口的转变。 FDA批准的rPET、rHDPE和rLLDPE的采用正在逐步缩小供应缺口。此外,美国塑胶包装市场正透过塑胶模塑商在2023年新增1,646台机器人来提高生产效率和产量比率。

美国塑胶包装市场趋势与洞察

美国消费品品牌迅速采用可回收的单一材料包装袋

聚乙烯和聚丙烯的单一材料复合材料正在取代曾经阻碍回收的混合基材薄膜。加工商现在提供符合美国《 2025年塑胶公约》设计目标的耐热高阻隔包装袋,直接向品牌所有者传达「可回收」的声明。 DNP印尼公司针对零食和宠物食品推出的单一材料包装的商业化应用,在维持阻隔性能的同时,简化了产品生命週期末期的处理流程。零售商要求其规格与传统铝箔包装相同,测试数据证实了两者氧气透过率相当,从而实现了广泛的SKU转换。美国塑胶包装市场的包装团队正在将捲材宽度优化与材料减量相结合,以降低单位产品的薄膜消费量。

美国小包裹网路公司发现,电子商务对轻型防护邮件的需求激增

小包裹托运商持续减少不必要的填充物,对可回收的薄型邮寄包装袋越来越感兴趣,这种包装袋既能降低体积重量费用,又能确保产品完整性。亚马逊已将其三分之一的美国境内小包裹替换为纸质包装,自该计画启动以来,已减少了150亿个塑胶空气枕。该公司的试点工厂正在检验每分钟超过250个包裹的生产线速度,为自动化树立了新的标竿。竞争对手正努力达到华盛顿州回收法规定的含30%消费后回收材料(PCR)的单一材料低密度聚乙烯(LDPE)气泡邮寄包装袋的性能水准。美国塑胶包装市场的加工商正在投资高功率吹膜塔和自动化分切系统,以应对每日小包裹量的激增。

扩大州级一次性塑胶禁令,以减少某些类型的包装

加州SB54法案规定,到2032年,该州销售的原生塑胶包装必须减少25%,并要求生产商在2025年前加入生产者责任组织。新泽西州、科罗拉多和缅因州也颁布了类似的强制规定,这使得全国性品牌面临复杂且分散的合规环境。儘管成本更高,加工商仍在积极地从产品目录中剔除PS泡壳和PVC泡壳,转而使用PETG和涂层纸板等替代品。监管的不确定性推高了长期供应合约的风险溢价,并抑制了美国塑胶包装市场的可自由支配资本支出,因为各公司都在等待统一的联邦指导方针出台。

细分市场分析

到2024年,软包装将占美国塑胶包装市场的54.14%,复合年增长率(CAGR)为4.98%。每增加一个软包装袋,其聚合物用量将比硬包装袋减少60-70%,从而降低运输排放和仓储占用空间。电商巨头更青睐可折迭成立方体的扁平包装袋,体积仅为瓦楞纸箱的十分之一,进一步降低了仓储成本。各大品牌正在采用近红外线(NIR)可读油墨,使软包装袋能够在材料回收设施中高效分拣,从而提高净回收率。同时,「智慧」包装袋正在嵌入RFID和NFC标籤,实现从填充到消费者扫描的全过程视觉化。

硬质塑胶在饮料、药品和家用化学品领域仍发挥关键作用,但其成长速度已放缓至2.1%的复合年增长率。轻质高密度聚乙烯(HDPE)瓶的树脂用量将比2023年的设计减少12%,但跌落强度和口感中性等性能指标限制了树脂用量的进一步降低。华盛顿州的再生材料含量法要求瓶子製造商确保稳定的再生高密度聚乙烯(rHDPE)供应,鼓励他们共同投资建造内部清洗生产线。美国塑胶包装市场的竞争主要围绕着扎带盖展开,这种盖帽既方便又能减少浪费,并且符合即将出台的瓶盖密封性要求。

聚乙烯在2024年仍将维持45.54%的软包装市场份额,这得益于其宽广的加工窗口和完善的路边回收基础设施。美国食品药物管理局(FDA)核准100%再生线性低密度聚乙烯(rLLDPE)用于零嘴零食包装,这为食品安全合规铺平了道路,并使全国零售商能够推出「循环」自有品牌产品。研发团队正在采用茂金属催化剂,以更小的线径实现更高的衝击强度,从而节省8-10%的树脂用量。随着共挤出技术能够适应再生颗粒的差异性而不影响薄膜的透明度,美国软塑胶基软包装市场规模持续扩大。

「其他材料」类别将以6.34%的复合年增长率成长,主要成长动力来自可堆肥PLA共混物、纤维素基薄膜和二氧化硅涂层纸。消费品牌正在试用源自甘蔗的生物基聚乙烯(bio-PE),这种材料具有相似的机械性能和更低的碳足迹。双向拉伸聚丙烯(BOPP)仍然是光面零嘴零食和糖果甜点包装纸的必备材料,但新型清漆系统无需金属化即可提供符合单一材料回收指南的阻隔性能。树脂供应商和薄膜加工商之间的伙伴关係将加快资格确认週期,缩短新配方的上市时间。

美国塑胶包装市场按材料类型(硬质塑胶(聚乙烯(PE)、聚丙烯(PP)等);软质塑胶(聚乙烯(PE)、双轴延伸聚丙烯(BOPP)等))、包装类型(硬质塑胶包装、软质塑胶包装)、最终用途产业(食品、食品饮料、製药等)和包装技术(挤出、热成型等)进行细分。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国小包裹网路公司发现,电子商务对轻型防护邮件的需求激增

- 美国消费品品牌迅速采用可回收的单一材料包装袋;《塑胶公约》的目标是2025年后。

- 已调理食品和即食食品市场成长,需要阻隔性柔性薄膜

- 药品低温运输的扩展推动了专用硬质容器和泡壳薄膜的应用。

- 企业对25%消费后回收材料(PCR)含量的承诺推动了对再生PET和再生HDPE瓶的需求。

- 投资先进的数位印刷技术,为小型企业品牌快速客製化。

- 市场限制

- 加强国家层级的一次性塑胶禁令,并减少某些包装形式。

- 聚烯树脂价格因页岩气原料价格波动而波动

- 消费者转向使用纸张和铝製品的永续性替代品

- 资本密集的化学回收基础设施限制了塑胶供应。

- 供应链分析

- 贸易情境分析(基于相关HS编码)

- 美国当前的回收趋势

- 监理展望

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依材料类型

- 硬质塑胶

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 聚苯乙烯(PS)和发泡聚苯乙烯(EPS)

- 其他材料类型

- 软质塑胶

- 聚乙烯(PE)

- 双轴延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 其他材料类型

- 硬质塑胶

- 按包装类型

- 硬质塑胶包装

- 瓶子和罐子

- 瓶盖和封口

- 托盘和泡壳

- 其他产品类型

- 软质塑胶包装

- 小袋

- 包包

- 薄膜和包装

- 其他产品类型

- 硬质塑胶包装

- 按最终用途行业划分

- 食物

- 饮料

- 製药

- 化妆品和个人护理

- 家用和工业化学品

- 宠物食品和动物护理

- 其他终端用户产业

- 透过包装技术

- 射出成型

- 吹塑成型

- 挤压

- 热成型

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Sealed Air Corp.

- Sonoco Products Co.

- Sigma Plastics Group Inc.

- ProAmpac LLC

- Constantia Flexibles

- Alpha Packaging Inc.

- Centor Inc.(Gerresheimer)

- Silgan Holdings Inc.

- Bericap Holdings

- Plastipak Holdings Inc.

- Coveris Holdings SA

- Printpack Inc.

- AptarGroup Inc.

- Pactiv Evergreen Inc.

- Novolex Holdings LLC

- Sabert Corp.

- Genpak LLC

- Mondi plc

第七章 市场机会与未来展望

The United States plastic packaging market size is 29.97 million tonnes in 2025 and is projected to reach 35.29 million tonnes by 2030, exhibiting a 3.32% CAGR.

Demand resilience comes from e-commerce parcel expansion, food and beverage convenience formats, and brand owner commitments to integrate 25% post-consumer recycled (PCR) resin into core stock-keeping units. Regulatory frameworks such as California SB 54 and Washington State's recycled-content law are accelerating design shifts toward lighter gauges, mono-material laminates, and tethered closures. Adoption of FDA-cleared rPET, rHDPE, and rLLDPE has begun closing the feed-stock gap, while robotics installations-1,646 new units added by plastics molders in 2023-are streamlining throughput and raising quality yields within the United States plastic packaging market.

US Plastic Packaging Market Trends and Insights

Rapid Adoption of Recyclable Mono-Material Pouches by US CPG Brands

Mono-material polyethylene and polypropylene laminates are replacing mixed-substrate films that once obstructed recycling streams. Converters now deliver heat-resistant, high-barrier pouches that comply with the U.S. Plastics Pact 2025 design targets, giving brand owners a straightforward route to "recycle-ready" claims. DNP Indonesia's commercial roll-out of mono-material snack and pet-food packs demonstrates how barrier performance can be maintained while simplifying end-of-life processing. Retailers request specification parity with legacy foil structures, and test data confirm comparable oxygen-transmission rates, enabling broad SKU conversion. Packaging teams within the United States plastic packaging market are synchronizing material down-gauging with roll-stock width optimization to shrink film consumption per unit.

Surging E-Commerce Demand for Lightweight Protective Mailers in the US Parcel Network

Parcel shippers continue to eliminate unnecessary void fill, driving interest in thin-gauge, curbside-recyclable mailers that cut dimensional-weight fees while preserving product integrity. Amazon has shifted one-third of its U.S. outbound parcels to paper-based alternatives, eliminating 15 billion plastic air pillows since program inception. The company's pilot plants validate line speeds exceeding 250 parcels per minute, setting new benchmarks for automation. Competitors are matching performance with mono-material LDPE bubble mailers containing 30% PCR, as mandated by Washington's recycled-content law. Converters positioned within the United States plastic packaging market are investing in high-output blown-film towers and automated wicketing to address the spike in daily parcel volumes.

Escalating State-Level Single-Use Plastics Bans Reducing Certain Packaging Formats

California SB 54 mandates a 25% reduction in virgin plastic packaging sold within state borders by 2032, and producers must join a Producer Responsibility Organization by 2025. Similar mandates in New Jersey, Colorado, and Maine create a fragmented compliance map that raises complexity for nationwide brands. Converters are pre-emptively retiring PS clamshells and PVC blisters from their catalogs, turning to PET G and coated paperboard alternatives even when cost of goods rises. The regulatory uncertainty embeds risk premiums into long-term supply contracts, curbing discretionary capital spend within the United States plastic packaging market as firms await harmonized federal guidelines.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Ready-to-Eat and On-the-Go Foods Requiring High-Barrier Flexible Films

- Corporate Commitments to 25% PCR Content Boosting Demand for rPET and rHDPE Bottles

- Consumer Shift Toward Paper and Aluminum Alternatives for Sustainability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible formats delivered 54.14% of United States plastic packaging market share in 2024 and are marching ahead at a 4.98% CAGR. Each new pouch replaces rigid counterparts with 60-70% less polymer, reducing freight emissions and warehouse footprints. E-commerce giants favor flat mailers because they collapse to one-tenth the inbound cube of corrugated boxes, slashing storage overhead. Brands now employ near-infrared (NIR) readable inks so flexibles sort efficiently at material-recovery facilities, improving real recycling rates. Meanwhile, "smart" pouches embed RFID or NFC tags, providing end-to-end visibility from filler to consumer scanning events.

Rigid plastics still account for essential roles in beverages, pharmaceuticals, and household chemicals, yet growth lags at 2.1% CAGR. Lightweight HDPE bottles use up to 12% less resin than 2023 designs, but performance thresholds on drop strength and taste neutrality limit further down-gauging. Washington State's recycled-content law compels bottle makers to secure stable rHDPE streams, prompting co-investment in in-house wash lines. Competition within the United States plastic packaging market now revolves around tethered caps that comply with forthcoming closure-retention mandates, merging convenience and litter reduction.

Polyethylene retained a 45.54% share of flexible volumes in 2024, supported by its broad processing window and robust curbside collection infrastructure. FDA approval for 100% rLLDPE content in snack wrappers confirms food-safety compliance pathways, allowing national retailers to launch "circular" private labels. Development teams adopt metallocene catalysts that provide higher dart impact at reduced gauge, contributing to resin savings of 8-10%. The United States plastic packaging market size for PE-based flexibles will continue scaling as co-extrusion technology accommodates recycled pellet variability without compromising film clarity.

The "other materials" category advances 6.34% CAGR, propelled by compostable PLA blends, cellulose-based films, and silicium-oxide coated papers. Consumer brands experiment with bio-PE derived from sugarcane that offers equivalent mechanical properties and a lower carbon footprint. BOPP remains indispensable for glossy snack and confectionery overwraps, yet new varnish systems deliver metallization-free barrier performance aligned with mono-material recycling guidelines. Partnerships between resin suppliers and film converters accelerate qualification cycles, shortening time-to-market for emerging formulations.

The United States Plastic Packaging Market is Segmented by Material Type ((Rigid Plastic(Polyethylene (PE), Polypropylene (PP) and More) Flexible Plastic (Polyethylene (PE), Biaxially Oriented Polypropylene (BOPP) and More)), Packaging Type (Rigid Plastic Packaging, Flexible Plastic Packaging), End-Use Industry (Food, Beverage, Pharmaceutical, and More) and Packaging Technology (Extrusion, Thermoforming, and More)

List of Companies Covered in this Report:

- Amcor plc

- Sealed Air Corp.

- Sonoco Products Co.

- Sigma Plastics Group Inc.

- ProAmpac LLC

- Constantia Flexibles

- Alpha Packaging Inc.

- Centor Inc. (Gerresheimer)

- Silgan Holdings Inc.

- Bericap Holdings

- Plastipak Holdings Inc.

- Coveris Holdings SA

- Printpack Inc.

- AptarGroup Inc.

- Pactiv Evergreen Inc.

- Novolex Holdings LLC

- Sabert Corp.

- Genpak LLC

- Mondi plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging E-commerce Demand for Lightweight Protective Mailers in US Parcel Network

- 4.2.2 Rapid Adoption of Recyclable Mono-Material Pouches by US CPG Brands Post-2025 Plastics Pact Targets

- 4.2.3 Growth of Ready-to-Eat and On-the-Go Foods Requiring High-Barrier Flexible Films

- 4.2.4 Pharmaceutical Cold-Chain Expansion Driving Specialty Rigid Containers and Blister Films

- 4.2.5 Corporate Commitments to 25 % PCR Content Boosting Demand for rPET and rHDPE Bottles

- 4.2.6 Investments in Advanced Digital Printing Enabling Short-Run Customization for SME Brands

- 4.3 Market Restraints

- 4.3.1 Escalating State-Level Single-Use Plastics Bans Reducing Certain Packaging Formats

- 4.3.2 Volatility in Polyolefin Resin Prices Linked to Shale Gas Feedstock Swings

- 4.3.3 Consumer Shift Toward Paper and Aluminum Alternatives for Sustainability

- 4.3.4 Capital Intensity of Chemical Recycling Infrastructure Limiting rPlastics Supply

- 4.4 Supply-Chain Analysis

- 4.5 Trade Scenario Analysis (under relevant HS codes)

- 4.6 Current Recycling Trends in United States

- 4.7 Regulatory Outlook

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Material Type

- 5.1.1 Rigid Plastic

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.6 Other Material Types

- 5.1.2 Flexible Plastic

- 5.1.2.1 Polyethylene (PE)

- 5.1.2.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.2.3 Cast Polypropylene (CPP)

- 5.1.2.4 Other Material Types

- 5.1.1 Rigid Plastic

- 5.2 By Packaging Type

- 5.2.1 Rigid Plastic Packaging

- 5.2.1.1 Bottles and Jars

- 5.2.1.2 Caps and Closures

- 5.2.1.3 Trays and Clamshells

- 5.2.1.4 Other Product Types

- 5.2.2 Flexible Plastic Packaging

- 5.2.2.1 Pouches

- 5.2.2.2 Bags

- 5.2.2.3 Films and Wraps

- 5.2.2.4 Other Product Types

- 5.2.1 Rigid Plastic Packaging

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Home and Industrial Chemicals

- 5.3.6 Pet Food and Animal Care

- 5.3.7 Other End-use Industry

- 5.4 By Packaging Technology

- 5.4.1 Injection Molding

- 5.4.2 Blow Molding

- 5.4.3 Extrusion

- 5.4.4 Thermoforming

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor plc

- 6.4.2 Sealed Air Corp.

- 6.4.3 Sonoco Products Co.

- 6.4.4 Sigma Plastics Group Inc.

- 6.4.5 ProAmpac LLC

- 6.4.6 Constantia Flexibles

- 6.4.7 Alpha Packaging Inc.

- 6.4.8 Centor Inc. (Gerresheimer)

- 6.4.9 Silgan Holdings Inc.

- 6.4.10 Bericap Holdings

- 6.4.11 Plastipak Holdings Inc.

- 6.4.12 Coveris Holdings SA

- 6.4.13 Printpack Inc.

- 6.4.14 AptarGroup Inc.

- 6.4.15 Pactiv Evergreen Inc.

- 6.4.16 Novolex Holdings LLC

- 6.4.17 Sabert Corp.

- 6.4.18 Genpak LLC

- 6.4.19 Mondi plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

PCR塑胶包装市场:商业机会、成长要素、产业趋势分析及2026-2035年预测

PCR塑胶包装市场:商业机会、成长要素、产业趋势分析及2026-2035年预测 医疗设备和植入用高纯度塑胶市场规模、份额和成长分析:按产品、应用和地区划分-产业预测(2026-2033 年)

医疗设备和植入用高纯度塑胶市场规模、份额和成长分析:按产品、应用和地区划分-产业预测(2026-2033 年) 塑胶包装市场规模、份额和趋势分析报告:按材料、产品、技术、应用、地区和细分市场划分(2026-2033 年)

塑胶包装市场规模、份额和趋势分析报告:按材料、产品、技术、应用、地区和细分市场划分(2026-2033 年) 散装聚苯乙烯包装市场:按应用和地区划分

散装聚苯乙烯包装市场:按应用和地区划分 塑胶包装市场分析及预测(至2035年):依类型、产品类型、应用、材料类型、技术、最终用户、功能及工艺划分

塑胶包装市场分析及预测(至2035年):依类型、产品类型、应用、材料类型、技术、最终用户、功能及工艺划分 再生塑胶包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测

再生塑胶包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测 德国塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

德国塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球PCR塑胶包装市场:按材料、产品、最终用户和地区划分-市场规模、产业趋势、机会分析和未来预测(2026-2035年)

全球PCR塑胶包装市场:按材料、产品、最终用户和地区划分-市场规模、产业趋势、机会分析和未来预测(2026-2035年) 2026年全球PCR塑胶包装市场报告2026年全球塑胶替代包装市场报告

2026年全球PCR塑胶包装市场报告2026年全球塑胶替代包装市场报告