|

市场调查报告书

商品编码

1850130

化学注入橇:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Chemical Injection Skids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

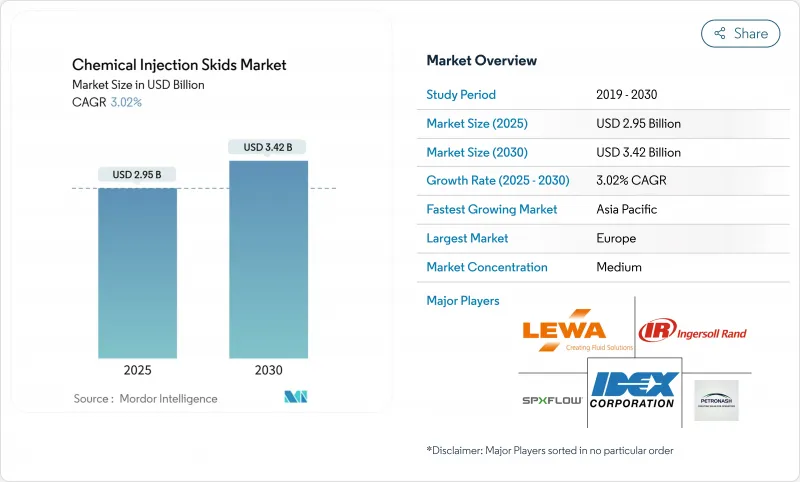

预计 2025 年化学注入橇市场价值将达到 29.5 亿美元,到 2030 年预计将达到 34.2 亿美元,复合年增长率为 3.02%。

下游石化联合企业的扩张、排放法规的日益严格以及油气作业对可靠流量保障的需求推动了行业的稳步增长。业者将精密注入撬块视为防止因结垢、腐蚀和微生物污染而导致意外停机的保障。随着水处理厂采用自动化技术以满足营养物去除法规(不合规将面临经济处罚),投资需求也不断增加。随着乙烯、氨和PTA产能的扩张,亚太地区大型多进料机组的订单正在加速成长。泵浦专家和系统整合商之间的适度整合标誌着一个成熟阶段,在这个阶段,服务可靠性、材料工程和数位监控将使供应商脱颖而出。

全球化学注入撬市场趋势与洞察

下游石化产能快速成长

像中国耗资200亿美元的山东综合体这样的大型企划需要数百个专用注入点,用于腐蚀抑制、抗氧化剂注入和催化剂淬灭。系统供应商正在透过扩大生产线来应对这项挑战:先进精密工业服务公司(Advanced Precision Industrial Services)将其沙乌地阿拉伯工厂的年撬装产量提高了500%,以解决中东地区EPC订单积压问题。新建裂解装置对流量控制公差的要求比钻井和生产作业更严格,这使得化学品注入撬装设备从选用配件转变为关键路径设备。聚合物岛、芳烃岛和公用工程岛都需要单独的计量迴路,每增加一个乙烯装置就能产生乘数效应。下游扩建计画创造了持久的、与计划相关的需求,从而缓衝了化学品注入撬装市场对油价波动的影响。

对水处理应用的需求不断增长

市政当局现在在单一製程中部署多种聚合物、凝聚剂和气味控制混合物。这种复杂性促使营运商转向整合高黏度聚合物帮浦和重量式给料器的全自动多化学品撬装系统。精确的剂量可减少化学品过度使用的损失并降低污泥处理成本,使北美工厂的平均投资回收期为两年。工业用户也支持这一趋势,因为特种化学品製造商在排放到下水道之前必须遵守严格的氯化物、磷酸盐和 COD 限制。设备供应商透过併购扩展其产品组合。英格索兰 (Ingersoll Rand) 对 SSI 充气的收购增强了曝气专业知识并补充了其用于完整水包的计量泵产品线。即使在传统石油和天然气订单疲软的情况下,这种转变也创造了一个充满活力的化学注入撬装市场。

初期投资成本高

在提高采收率测试中,整合化学注入站的资本支出可能超过1500万美元,这为在价格低迷时期转向手动鼓式供油技术的独立运营商设置了进入门槛。配备防爆马达、无密封计量帮浦、PLC和冗余仪器的复杂撬装系统也构成了较高的进入门槛。额外的试运行和培训成本可能会使费用翻倍,并延迟中端营运商的投资回报。供应商正在透过租赁车队和基于绩效的租赁计划来应对,但在融资紧张的领域,采用这些技术仍然谨慎。

細項分析

到2024年,石化产业将占据化学品注入撬块市场份额的35.16%,这得益于遍布裂解、加氢和聚合装置的分散式加药点。由于大型联合装置很少容忍计划外停机,因此运营商青睐配备热备用泵的双撬式机架,这些泵可以在不中断流程的情况下进行更换。由于每个新的乙烯装置都需要根据具体情况配备酸抑制剂、消泡剂、中和剂和除生物剂迴路,因此该细分市场支撑了化学品注入撬块的市场规模。

到2030年,用水和污水处理设施的复合年增长率将达到3.78%,是最快的。随着公共寻求营养物去除合规性,多进料系统正在将聚合物、明矾和聚合氯化铝注入整合到单一框架中,节省占地面积。随着市政当局从劳力密集罐式测试转向自动回馈迴路,将聚合物过量减少15%,多进料系统的应用将会增加。水处理化学品注入撬装设备的市场规模预计将会增加,这反映了三级处理和污泥脱水生产线的扩张。

区域分析

2024年,欧洲将占销售额的28.65%,这得益于德国1,600亿欧元的化学品产量以及鼓励高精度分配设备的合规文化。占该行业96%的德国中小企业正在采购紧凑型撬装设备,用于批量特种生产;而像BASF这样规模的综合体则正在采购带有自动切换功能的全封闭ISO集装箱解决方案。 2010年至2020年期间,能源价格较平均上涨了四倍,促使工厂升级为变速驱动装置,从而将泵浦功率降低20%,这刺激了现有设施的改造活动。

到2030年,亚太地区将实现最快的复合年增长率,达到3.36%。中国的炼油化工一体化浪潮和印度製药业的扩张需要同步的添加剂流程,以确保原料纯度和反应器保护。 SCG Chemicals在越南投资7亿美元的乙烷扩建计划采用三泵撬装系统和重量式混合系统,以适应乙烷成分的波动。区域EPC公司正在采用模组化成套设备,这些设备在运输过程中已进行预接线和测试,以最大限度地减少现场劳动力,因为熟练焊工短缺。

北美市场在页岩油石化投资和成熟的海上油田(滑橇每七年更换一次)的推动下,市占率保持稳定。预测性维护的重点是添加数位双胞胎和振动分析,使操作员能够在发生故障之前安排软管和隔膜的更换。墨西哥的保税加工工厂正在扩建,透过为油漆、黏合剂和电子产品涂装生产线提供小容量滑橇来扩大基本客群。在南美、中东和非洲,巴西的Comperj计划和沙乌地阿拉伯的「愿景2030」下游多元化计划正在部署整合先进化学注入功能的连续製程装置,虽然规模有所滞后,但发展势头正在增强。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 下游石化产能新增快速成长

- 水处理应用需求不断成长

- 更严格的环境排放标准

- 在腐蚀和阻垢应用中的使用日益增多

- 越来越多地使用绿色化学品需要多进料滑轨设计

- 市场限制

- 初期投资成本高

- 滑轨製造和维修领域技术纯熟劳工短缺

- 原物料价格波动

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 按最终用户产业

- 石化产品

- 化学品

- 能源和电力

- 石油和天然气

- 水处理

- 按泵类型

- 活塞/柱塞泵

- 隔膜泵

- 蠕动帮浦

- 其他计量泵

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AES Arabia Ltd.

- Carotek, Inc

- Casainox FS Pty Ltd

- Euro Mechanical

- IDEX Corporation

- Ingersoll Rand

- INTECH

- Integrated Flow Solutions, Inc.

- ITC SL

- Lewa GmbH

- Petrak Industries, Inc.

- Petronash

- Proserv UK Ltd

- SEKO SpA

- SLB

- SPX FLOW, Inc.

- TechnipFMC plc

- Watson-Marlow Fluid Technology Solutions

第七章 市场机会与未来展望

The chemical injection skids market is valued at USD 2.95 billion in 2025 and is forecast to reach USD 3.42 billion by 2030, expanding at a 3.02% CAGR.

Steady growth is anchored in the expansion of downstream petrochemical complexes, tougher discharge regulations, and the need for reliable flow assurance across oil-and-gas operations. Operators view precision-dosing skids as insurance against unplanned shutdowns caused by scaling, corrosion, or microbial fouling. Investment momentum is reinforced as water-treatment plants adopt automation to meet nutrient-removal rules that carry financial penalties for non-compliance. Europe continues to purchase high-specification equipment to satisfy the EU's Fit-for-55 goals, while Asia-Pacific accelerates orders for large multi-feed packages alongside new ethylene, ammonia, and PTA capacity. Moderate consolidation among pump specialists and system integrators signals a maturity phase in which service reliability, materials engineering, and digital monitoring differentiate suppliers.

Global Chemical Injection Skids Market Trends and Insights

Rapid Growth in Downstream Petrochemical Capacity Additions

Mega-projects such as China's USD 20 billion Shandong complex require hundreds of dedicated dosing points for corrosion inhibition, antioxidant injection, and catalyst quenching. System suppliers respond by scaling fabrication lines: Advanced Precision Industrial Services lifted annual skid output 500% at its Saudi plant to meet Middle-East EPC backlogs. New crackers demand tighter flow-control tolerances than drilling or production operations, turning chemical injection skids from optional accessories into critical path equipment. Each additional ethylene train creates a multiplier effect because polymer, aromatics, and utilities islands all mandate separate dosing loops. The downstream build-out produces durable, project-linked demand that buffers the chemical injection skids market from oil price volatility.

Accelerating Demand from Water Treatment Applications

Municipalities now deploy multiple polymers, coagulants, and odor-control blends in a single process train; this complexity pushes operators toward fully automated, multi-chemical skids that integrate high-viscosity polymer pumps with gravimetric feeders. Accurate dosing trims chemical overuse penalties and reduces sludge-handling costs, bringing a two-year average payback in North American plants. Industrial users echo the trend as specialty-chemical producers face strict chloride, phosphate, and COD limits before discharging to sewers. Equipment vendors expand portfolios through M&A: Ingersoll Rand's purchase of SSI Aeration adds diffused-air expertise that complements its metering-pump line for complete water packages. Such shifts keep the chemical injection skids market vibrant even when traditional oil-and-gas orders soften.

High Initial Cost of Investment

Capital outlays for integrated chemical injection stations on an enhanced-oil-recovery test can top USD 15 million, a barrier that pushes independents toward manual drum-feed techniques during price downturns. The entry hurdle persists because sophisticated skids bundle explosion-proof motors, seal-less metering pumps, PLCs, and redundant instrumentation. Added spend on commissioning and training can double the invoice value, delaying payback for mid-tier operators. Vendors respond with rental fleets and performance-based leasing plans, yet adoption remains cautious in cash-constrained segments.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Environmental Discharge Norms

- Increasing Usage for Corrosion and Scale Inhibition Application

- Skilled-Labor Shortage for Skid Fabrication & Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The petrochemical sector held 35.16% of the chemical injection skids market share in 2024, underpinned by distributed dosing points across cracking, hydrogenation, and polymerization trains. Large complexes seldom tolerate unscheduled downtime, so operators favor duplex skid racks with hot-standby pumps that swap without disrupting flow. The segment anchors the chemical injection skids market size because each new ethylene unit demands conditions-specific acid inhibitors, antifoam, neutralizers, and biocide loops.

Water and wastewater facilities register the fastest 3.78% CAGR through 2030. Utilities seek nutrient-removal compliance, so multi-feed systems integrate polymer, alum, and PAC dosing on a single frame to conserve floor space. Adoption rises as municipalities shift from labor-intensive jar testing toward automated feedback loops that cut polymer overshoot by 15%. The chemical injection skids market size for water treatment is projected to rise, mirroring the build-out of tertiary treatment and sludge-dewatering lines.

The Chemical Injection Skids Market Report Segments the Industry by End-User Industry (Petrochemicals, Chemicals, Energy and Power, and More), Pump Type (Piston/Plunger Pumps, Diaphragm Pumps, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe accounted for 28.65% revenue in 2024, supported by Germany's EUR 160 billion chemical output and a compliance climate that rewards high-accuracy dosing equipment. German SMEs representing 96% of sector companies purchase compact skids for batch specialty production, whereas BASF-scale complexes procure fully enclosed ISO-container solutions with automated switchover. Energy prices have quadrupled versus 2010-2020 averages, so plants upgrade to variable-speed drives that cut pump power by 20%, stimulating retrofit activity across existing installations.

Asia-Pacific posts the fastest 3.36% CAGR through 2030. China's refinery-to-chemicals integration wave and India's pharmaceuticals build-out require synchronized additive streams that ensure feedstock purity and reactor protection. The USD 700 million SCG Chemicals ethane-enhancement project in Vietnam specifies triple-pump skids with gravimetric blending to accommodate variable ethane composition. Regional EPCs embrace modular packages shipped fully wired and tested, minimizing site labor where skilled welders remain scarce.

North America secures a stable share via shale-driven petrochemical investments and mature offshore fields that rotate skids on 7-year renewal cycles. Emphasis on predictive maintenance adds digital twins and vibration analytics, allowing operators to schedule hose or diaphragm replacement before failure. Mexico's maquiladora expansion adopts smaller capacity skids feeding paint, adhesive, and electronics finishing lines, broadening the customer base. South America, and Middle East and Africa trail in volume but gain traction as Brazil's Comperj project and Saudi Arabia's Vision 2030 downstream diversification roll out continuous-process units that integrate advanced chemical injection functionality.

- AES Arabia Ltd.

- Carotek, Inc

- Casainox FS Pty Ltd

- Euro Mechanical

- IDEX Corporation

- Ingersoll Rand

- INTECH

- Integrated Flow Solutions, Inc.

- ITC SL

- Lewa GmbH

- Petrak Industries, Inc.

- Petronash

- Proserv UK Ltd

- SEKO S.p.A.

- SLB

- SPX FLOW, Inc.

- TechnipFMC plc

- Watson-Marlow Fluid Technology Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth in downstream petrochemical capacity additions

- 4.2.2 Accelerating demand from water treatment applications

- 4.2.3 Stricter environmental discharge norms

- 4.2.4 Increasing usage for corrosion and scale inhibition application

- 4.2.5 Rising use of green chemicals requiring multi-feed skid designs

- 4.3 Market Restraints

- 4.3.1 High initial cost of investment

- 4.3.2 Skilled-labor shortage for skid fabrication & maintenance

- 4.3.3 Volatility in raw material prices

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Petrochemicals

- 5.1.2 Chemicals

- 5.1.3 Energy and Power

- 5.1.4 Oil and Gas

- 5.1.5 Water Treatment

- 5.2 By Pump Type

- 5.2.1 Piston/Plunger Pumps

- 5.2.2 Diaphragm Pumps

- 5.2.3 Peristaltic Pumps

- 5.2.4 Other Metering Pumps

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%) / Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AES Arabia Ltd.

- 6.4.2 Carotek, Inc

- 6.4.3 Casainox FS Pty Ltd

- 6.4.4 Euro Mechanical

- 6.4.5 IDEX Corporation

- 6.4.6 Ingersoll Rand

- 6.4.7 INTECH

- 6.4.8 Integrated Flow Solutions, Inc.

- 6.4.9 ITC SL

- 6.4.10 Lewa GmbH

- 6.4.11 Petrak Industries, Inc.

- 6.4.12 Petronash

- 6.4.13 Proserv UK Ltd

- 6.4.14 SEKO S.p.A.

- 6.4.15 SLB

- 6.4.16 SPX FLOW, Inc.

- 6.4.17 TechnipFMC plc

- 6.4.18 Watson-Marlow Fluid Technology Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Development of Technologically Advanced Chemical Injection System

2026年全球化学注入撬装设备市场报告

2026年全球化学注入撬装设备市场报告 化学注入撬装设备市场-全球产业规模、份额、趋势、机会和预测:按功能、应用、地区和竞争格局划分,2021-2031年

化学注入撬装设备市场-全球产业规模、份额、趋势、机会和预测:按功能、应用、地区和竞争格局划分,2021-2031年 化学注入撬装设备:全球市场份额和排名、总收入和需求预测(2025-2031 年)

化学注入撬装设备:全球市场份额和排名、总收入和需求预测(2025-2031 年) 化学注入撬装设备市场:依应用、帮浦设计、结构材料、压力等级和系统配置划分-全球预测,2025-2032年液态氮分配系统市场(按系统类型、控制类型、系统元件、应用和分销管道)—2025-2030 年全球预测

化学注入撬装设备市场:依应用、帮浦设计、结构材料、压力等级和系统配置划分-全球预测,2025-2032年液态氮分配系统市场(按系统类型、控制类型、系统元件、应用和分销管道)—2025-2030 年全球预测 化学品注入撬市场规模、份额、趋势分析报告:按功能、最终用途、地区、细分市场预测,2025-2030 年

化学品注入撬市场规模、份额、趋势分析报告:按功能、最终用途、地区、细分市场预测,2025-2030 年 化学注入撬市场(功能:消泡、腐蚀抑制、破乳等)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测

化学注入撬市场(功能:消泡、腐蚀抑制、破乳等)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测