|

市场调查报告书

商品编码

1850287

火花电浆烧结:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Spark Plasma Sintering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

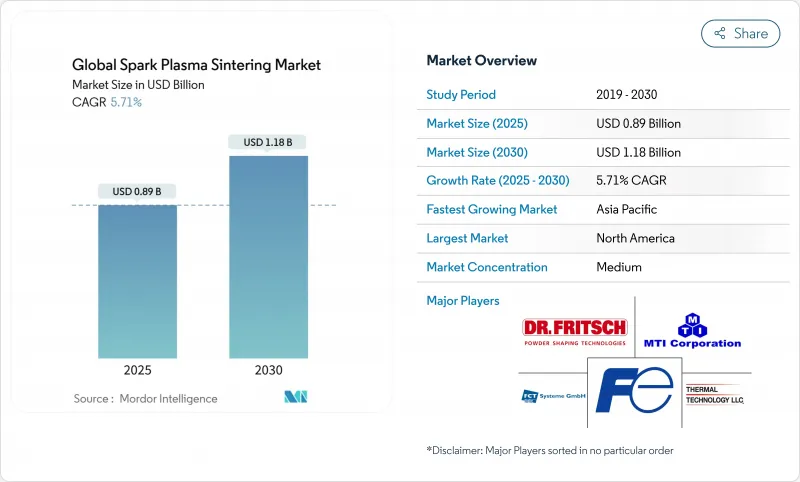

预计到 2025 年,火花电浆烧结市场规模将达到 8.9 亿美元,到 2030 年将达到 11.8 亿美元,复合年增长率为 5.71%。

推动市场需求的因素包括:製造商将快速热烧结技术与边缘感测器、板载人工智慧晶片和情境分析相结合,从而持续优化过程参数。半导体后端封装、精密家电和电动汽车零件等领域的日益普及表明,这项技术能够实现更严格的公差、减少废品并缩短生产週期。设备供应商目前正在整合运行本地预测演算法的神经网路处理单元,而5G链路则将分散的生产线连接到整合控制中心。同时,政府对国内晶片製造和清洁技术材料的激励措施持续吸引资金用于新增产能,而劳动力短缺也推动了工厂自动化进程。

全球火花电浆烧结市场趋势及洞察

整合物联网产品的兴起

製造商现在将微型热电偶、压力感测器和緻密化感测器直接嵌入晶粒组内,以毫秒精度向边缘网关传输数据,用于分析升温和保温时间。这种封闭式回馈无需人工干预即可降低能耗并提高零件密度。基于感测器历史资料建构的预测性维护模型可以在故障发生前数小时检测到异常情况,例如电极异常磨损,从而避免计划外停机。感测器模组中晶片级加密技术的广泛应用,减轻了IT部门对将生产网路开放给外部分析引擎的担忧。据美国製造业协会(Manufacturing Institute)称,大多数企业高管将物联网视为竞争优势的核心支柱,而边缘运算使这些设备能够在本地分析数据,从而降低即时控制的延迟。

将人工智慧整合到行动和边缘应用程式中

平板电脑仪錶板运行着一个轻量级视觉模型,扫描烧结零件以检测光学比较器无法检测到的微裂纹;同时,语音助理会根据即时緻密化曲线提案温度偏移量。控制器内的AI代理会在电阻出现峰值时自动微调脉衝宽度和压力,以保持晶粒均匀生长。由于推理过程在NPU(神经网路处理单元)上进行,即使云端连接中断,远端工厂也能保持完全运作。 LTI Mindtree观察到,製造商正在转向基于代理的AI来管理文件和设计迭代,使工程师能够在数小时内而非数週内迭代新的材料配方。

计算复杂性

运行在嵌入式GPU上的即时有限元素求解器和自适应控制器对处理能力的要求远超传统PLC。许多中型企业缺乏足够的IT人才编配运行调优演算法的容器化微服务,迫使它们将这项工作外包给託管边缘服务提供者。 NetSuite率先解决了这个技能缺口问题,帮助企业实现ERP系统现代化,无需从零开始编写程式码即可利用机器资料。在承包平台成熟之前,其复杂性将限制其普及应用。

細項分析

到2024年,软体将占据46%的收入份额,这主要得益于情境分析引擎能够解读多元感测器资料流并制定节能配方。火花电浆烧结市场依赖中间件,该中间件将旗舰级炉与MES和ERP套件连接起来,并同步批次追踪。人工智慧晶片/神经网路处理器(NPU)预计将以23.4%的复合年增长率成长,这反映了市场对边缘推理的需求,以将回馈迴路缩短至50毫秒或更短。随着新型炉配备高密度的仪器,硬体感测器也不断扩展。託管服务团队提供基于订阅的监控服务,使小型企业无需聘请专家即可受益于资料科学。生成式人工智慧模组透过记录製程调整和自动产生品质报告,进一步拓展了软体的价值提案。

其次,服务透过整合、培训和生命週期支援发挥作用。产品类型捆绑了反映基于合金类型的腔室动态的数位双胞胎模板,从而缩短了产品推出期间的试验週期。过去需要数月才能完成的计划,现在只需几週即可完成,因为工程师可以从共用库中导入最佳实践烧结曲线。这种集体学习促进了软体的普及,而定期升级则增加了异常分割和音讯仪表板等功能。

到2024年,设备製造商将凭藉预先安装嵌入式分析功能的承包压力机占据37.2%的市占率。他们在脉衝生成和电极磨损模式方面的专业知识,使得机器设计和计算模组的整合成为可能。在火花电浆烧结市场,这些原始设备製造商(OEM)目前正与感测器製造商和云端供应商合作,建构端到端解决方案,从而缩短试运行时间。同时,提供配方库託管和閒置炉容量经纪服务的线上/网路供应商,预计将以每年21.1%的速度成长。

行动网路营运商正在加入联盟,以确保服务等级协议,满足在分散式园区内同步加热波所需的 10 毫秒以下的延迟要求;供应商正在发布开放 API,允许第三方应用程式调用即时数据流,从而推动了微服务市场的发展,该市场专注于电极寿命预测和真空密封诊断等细分任务。

火花电浆烧结市场已按组件(硬体、软体、服务)、供应商(设备製造商、行动网路营运商等)、应用场景(计算应用场景、用户应用场景)、网路(无线蜂窝、WLAN/Wi-Fi、PAN/BLE)、终端用户垂直领域(BFSI、消费性电子产品等)和地区进行细分。市场预测以美元计算。

区域分析

2024年,北美将占全球销售额的34%,这主要得益于成熟的半导体生态系统、强大的产学合作以及联邦政府的奖励,例如390亿美元的CHIPS法案基金。亚利桑那州、德克萨斯和纽约州的工厂正在扩建其后端封装生产线,从而持续推动对能够黏合金属和陶瓷中介层的脉衝电流压机的需求。加拿大致力于发展低碳产业,这与缩短烧结週期和降低能源消耗密切相关。墨西哥的电子组装产业正在国内采购烧结馈通件和散热器,缩短了原始设备製造商(OEM)的供应链。

亚太地区正以18.5%的复合年增长率成长,这主要得益于中国製造业自动化程度的提高、日本在粉末冶金领域的深厚积累以及韩国竞相扩大存储晶片产能。政府支持的基金正投入数十亿美元用于智慧工厂维修,以引入新一代烧结技术。印度的电子产品生产关联奖励计画正在推动待开发区工厂采用高循环烧结技术生产功率装置。台湾的OSAT厂商正引进新型压机生产先进基板,进而巩固其在区域内的领先地位。

欧洲强调永续性和工人安全,鼓励使用闭合迴路熔炉,以捕获废气并最大限度地减少颗粒排放排放。德国的工业4.0框架正在加速采用具有开放式OPC-UA介面的互联压力机。法国正在将这项技术用于轻型航太支架,义大利则将其用于超合金涡轮盘。在中东和非洲,沙乌地阿拉伯和阿拉伯联合大公国的新兴工业正在采用烧结技术製造积层製造压平机,而南非则在探索矿业耐磨件的在地化生产。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概况

- 市场驱动因素

- 整合物联网产品正成为主流

- 将人工智慧主流化整合到行动和边缘应用程式中

- 5G相容智慧型装置的普及

- 零售媒体中低调、情境化广告的投资报酬率飙升

- 原始设备製造商对车载情感感知技术的潜在需求

- 工业 4.0 线中 OT 与网路的隐藏融合

- 市场限制

- 主流运算复杂度

- 加强主流资料隐私法规

- 边缘人工智慧硅供应中不为人知的瓶颈

- 细微的上下文漂移会降低机器学习模型的准确性

- 价值/供应链分析

- 监管格局

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 按组件

- 硬体

- 感测器和微控制器

- AI晶片/NPU

- 软体

- SDK 和中介软体

- 情境分析平台

- 服务

- 託管边缘服务

- 专业服务

- 硬体

- 依供应商类型

- 设备製造商

- 行动网路营运商

- 线上、网路和社交网路供应商

- 依网路类型

- 无线蜂巢

- 无线区域网路/Wi-Fi

- PAN/BLE

- 按最终用户产业

- BFSI

- 家电

- 媒体与娱乐

- 车

- 卫生保健

- 通讯

- 物流与运输

- 其他行业

- 依上下文类型

- 计算环境

- 使用者情境

- 物理环境

- 时间背景

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 中东和非洲

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲国家

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Google LLC

- Oracle Corporation

- Amazon Web Services Inc.

- Verizon Communications Inc.

- Samsung Electronics Co. Ltd

- Intel Corporation

- Apple Inc.

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- ATandT Inc.

- Huawei Technologies Co. Ltd

- Baidu Inc.

- Infosys Ltd.

- Ericsson AB

- Telefonica, SA

- Bosch Sensortec GmbH

- STMicroelectronics NV

- Arm Ltd.

第七章 市场机会与未来展望

The spark plasma sintering market size is estimated at USD 0.89 billion in 2025 and is projected to reach USD 1.18 billion by 2030, registering a 5.71% CAGR.

Demand is fuelled by manufacturers combining rapid-heating sintering physics with edge-ready sensors, on-board AI chips, and contextual analytics that continually refine process parameters. Wider adoption in semiconductor back-end packaging, precision consumer electronics, and electrified vehicle components underscores how the technology supports tighter tolerances, lower scrap, and shorter production cycles. Equipment vendors now embed neural processing units that run predictive algorithms locally, while 5G links tie scattered lines into unified control hubs. At the same time, government incentives for domestic chip fabrication and clean-tech materials keep capital flowing into new installations, even as labour shortages push factories toward deeper automation.

Global Spark Plasma Sintering Market Trends and Insights

Rise in Integrated IoT Offerings

Manufacturers now embed miniature thermocouples, pressure cells, and densification sensors directly inside die sets, feeding millisecond data into edge gateways that analyse heating ramps and hold times. This closed-loop feedback lowers energy use and improves part density without human intervention. Predictive maintenance models built on sensor history flag anomalies, such as abnormal electrode wear hours before failure, avoid unplanned downtime. Wider deployment of chip-level encryption within sensor modules eases IT concerns about opening production networks to external analytics engines. The Manufacturing Institute reports that most executives see IoT as a core pillar of competitiveness, and edge computing now lets those devices crunch data locally, cutting latency for real-time control.

Integration of AI in Mobile and Edge Apps

Tablet dashboards running lightweight vision models scan sintered parts for micro-cracks that escape optical comparators, while voice-driven assistants suggest temperature offsets based on live densification curves. AI agents inside controllers autonomously fine-tune pulse width and pressure as soon as resistance spikes, maintaining uniform grain growth. Because inference happens on-board NPUs, remote plants keep full functionality even if cloud links drop. LTIMindtree observes manufacturers pivoting toward agentic AI that governs both documentation and design iterations, letting engineers iterate new material recipes in hours rather than weeks.

Computational Complexities

Real-time finite-element solvers and adaptive controllers running on embedded GPUs elevate the processing burden well beyond classic PLCs. Many midsized job shops lack the IT talent to orchestrate containerized microservices that run tuning algorithms, forcing them to outsource to managed edge providers. NetSuite identifies this skills gap as a top challenge, with firms modernizing ERP stacks to harness machine data without coding from scratch. Until turnkey platforms mature, complexity tempers adoption speed.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of 5G-Enabled Smart Devices

- Contextual-Ads ROI Surge in Retail Media

- OEM Demand for In-Vehicle Emotion Sensing

- OT-Cyber Convergence in Industry 4.0 Lines

- Data-Privacy Regulations Tightening

- Edge-AI Silicon Supply Bottlenecks

- Context Drift Undermining ML Model Accuracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 46% of 2024 revenue because contextual analytics engines interpret multivariate sensor streams and prescribe energy-efficient recipes. The spark plasma sintering market relies on middleware to connect flagship furnaces with MES and ERP suites, allowing synchronized lot tracking. AI chips/NPUs are slated to grow at a 23.4% CAGR, reflecting demand for edge inference that keeps feedback loops under 50 milliseconds. Hardware sensors continue to expand because each new furnace ships with denser instrumentation footprints. Managed services teams offer subscription-based monitoring so smaller plants can benefit from data science without hiring specialists. Generative AI modules document process adjustments and auto-populate quality reports, further widening the software's value proposition.

Secondarily, services contribute through integration, training, and lifecycle support. Providers bundle digital twin templates that mirror chamber thermodynamics based on alloy type, reducing trial cycles during product launch. Projects that once ran for months now close in weeks as engineers import best-practice sintering curves from shared libraries. This collective learning adds momentum to software adoption, ensuring recurring upgrades add features such as anomaly segmentation and voice-activated dashboards.

Device manufacturers held 37.2% share in 2024 by shipping turnkey presses pre-loaded with embedded analytics. Their expertise in pulse generation and electrode wear patterns positions them to fuse mechanical design with compute modules. The spark plasma sintering market now sees these OEMs partnering with sensor fabricators and cloud vendors, creating end-to-end stacks that shorten commissioning time. Meanwhile, online/web vendors grow 21.1% annually by hosting recipe repositories and brokering idle furnace capacity-effectively creating "manufacturing clouds" that match demand and supply.

Mobile network operators join consortia to guarantee service-level agreements for sub-10 millisecond latency needed in synchronous heating waves across distributed campuses. The ecosystem approach means competitive dynamics revolve around interoperability; vendors publish open APIs so third-party apps can call real-time data streams, spurring a marketplace of micro-services for niche tasks such as electrode life prediction or vacuum seal diagnostics.

Spark Plasma Sintering Market is Segmented by Component (Hardware, Software and Services), Vendor Type (Device Manufacturers, Mobile Network Operators and More), Context Type (Computing Context, User Context), Network Type (Wireless Cellular, WLAN /Wi-Fi and PAN /BLE), End-User Industry (BFSI, Consumer Electronics and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America owns 34% of 2024 revenue thanks to a mature semiconductor ecosystem, strong university-industry collaboration, and federal incentives such as the CHIPS Act's USD 39 billion fund. Plants in Arizona, Texas, and New York expand back-end packaging lines, generating sustained demand for pulse-current presses capable of joining metal-ceramic interposers. Canada's push toward a low-carbon industry dovetails with sintering's shorter cycle times and lower energy footprint. Mexico's rising electronics assembly sector sources sintered feedthroughs and heat spreaders domestically, shortening supply chains for near-shoring OEMs.

Asia-Pacific is on track for an 18.5% CAGR, driven by China's manufacturing automation push, Japan's heritage in powder metallurgy, and South Korea's memory-chip capacity race. State-backed funds channel billions into smart-factory retrofits that bundle next-gen sintering. India's Production Linked Incentive scheme for electronics spurs greenfield fabs incorporating fast cycle sintering for power devices. Taiwan's OSAT players install new presses to produce advanced substrates, reinforcing regional leadership.

Europe stresses sustainability and worker safety, encouraging closed-loop furnaces that reclaim off-gas and minimize particulate emissions. Germany's Industry 4.0 framework speeds adoption of connected presses with open OPC-UA interfaces. France exploits the technology for lightweight aerospace brackets, and Italy for super-alloy turbine disks. In the Middle East and Africa, budding industrial parks in Saudi Arabia and the UAE adopt sintering for additive-manufactured tooling, while South Africa explores localized production of mining wear parts.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Google LLC

- Oracle Corporation

- Amazon Web Services Inc.

- Verizon Communications Inc.

- Samsung Electronics Co. Ltd

- Intel Corporation

- Apple Inc.

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- ATandT Inc.

- Huawei Technologies Co. Ltd

- Baidu Inc.

- Infosys Ltd.

- Ericsson AB

- Telefonica, S.A.

- Bosch Sensortec GmbH

- STMicroelectronics N.V.

- Arm Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Rise in integrated IoT offerings

- 4.2.2 Mainstream Integration of AI in mobile and edge apps

- 4.2.3 Mainstream Proliferation of 5G-enabled smart devices

- 4.2.4 Under-the-Radar Contextual-ads ROI surge in retail media

- 4.2.5 Under-the-Radar OEM demand for in-vehicle emotion sensing

- 4.2.6 Under-the-Radar OT-cyber convergence in Industry 4.0 lines

- 4.3 Market Restraints

- 4.3.1 Mainstream Computational complexities

- 4.3.2 Mainstream Data-privacy regulations tightening

- 4.3.3 Under-the-Radar Edge-AI silicon supply bottlenecks

- 4.3.4 Under-the-Radar Context drift undermining ML model accuracy

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Sensors and MCUs

- 5.1.1.2 AI Chips/NPUs

- 5.1.2 Software

- 5.1.2.1 SDKs and Middleware

- 5.1.2.2 Contextual Analytics Platforms

- 5.1.3 Services

- 5.1.3.1 Managed Edge Services

- 5.1.3.2 Professional Services

- 5.1.1 Hardware

- 5.2 By Vendor Type

- 5.2.1 Device Manufacturers

- 5.2.2 Mobile Network Operators

- 5.2.3 Online, Web and Social Networking Vendors

- 5.3 By Network Type

- 5.3.1 Wireless Cellular

- 5.3.2 WLAN /Wi-Fi

- 5.3.3 PAN /BLE

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Consumer Electronics

- 5.4.3 Media and Entertainment

- 5.4.4 Automotive

- 5.4.5 Healthcare

- 5.4.6 Telecommunications

- 5.4.7 Logistics and Transportation

- 5.4.8 Other Industries

- 5.5 By Context Type

- 5.5.1 Computing Context

- 5.5.2 User Context

- 5.5.3 Physical Context

- 5.5.4 Time Context

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Israel

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 United Arab Emirates

- 5.6.5.1.4 Turkey

- 5.6.5.1.5 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Google LLC

- 6.4.5 Oracle Corporation

- 6.4.6 Amazon Web Services Inc.

- 6.4.7 Verizon Communications Inc.

- 6.4.8 Samsung Electronics Co. Ltd

- 6.4.9 Intel Corporation

- 6.4.10 Apple Inc.

- 6.4.11 NVIDIA Corporation

- 6.4.12 Qualcomm Technologies Inc.

- 6.4.13 ATandT Inc.

- 6.4.14 Huawei Technologies Co. Ltd

- 6.4.15 Baidu Inc.

- 6.4.16 Infosys Ltd.

- 6.4.17 Ericsson AB

- 6.4.18 Telefonica, S.A.

- 6.4.19 Bosch Sensortec GmbH

- 6.4.20 STMicroelectronics N.V.

- 6.4.21 Arm Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment