|

市场调查报告书

商品编码

1850349

MicroLED:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Micro LED - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

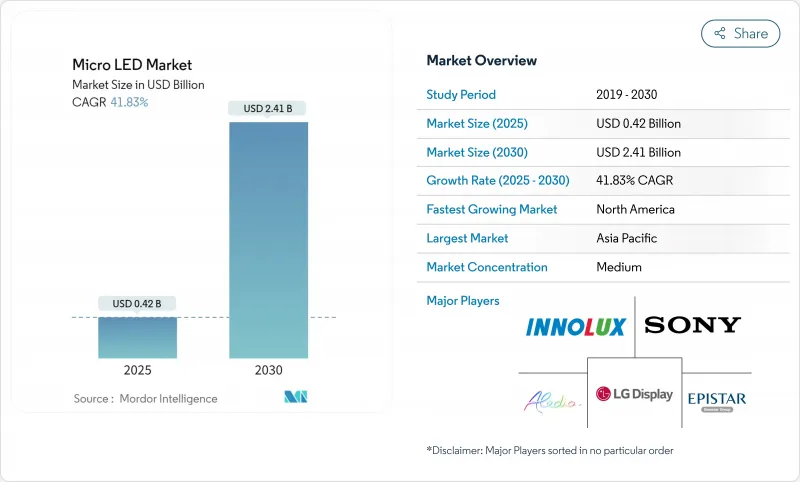

预计到 2025 年,微型 LED 市场规模将达到 4.2 亿美元,到 2030 年将达到 24.1 亿美元,年复合成长率为 41.83%。

商业性发展依赖于该技术的高亮度、低电力消耗以及超越LCD和OLED显示器的超长寿命。製造商正在稳步提高量产产量比率,台湾和韩国的资本密集型试点生产线正在扩大该技术在穿戴式装置、大型标誌和汽车驾驶座等领域的应用规模。亚太地区凭藉着成熟的半导体生态系统和扶持性的产业政策,引领着微型LED的製造主导;而北美则正在加速对国防和AR/VR项目的投资。儘管价格仍然较高,但对功耗、散热和阳光下可视性有严格领先的终端用户正在增强微型LED市场的长期竞争力。

全球MicroLED市场趋势与洞察

苹果和三星的MicroLED穿戴蓝图了对小型显示器的需求

苹果收购 LuxVue 后投入的 30 亿美元以及三星的同步研发项目,显示儘管短期内进度有所调整,但双方仍保持长期的投入。驱动 IC 和处理设备供应商不断增加的设计订单表明,供应链正在向 2 英寸以下面板转型。智慧型手錶显示器预计将以 45% 的复合年增长率成长。专业工具供应商正在将高通量贴片系统商业化,这有助于在旗舰品牌之外推广试生产。这种动态清晰地表明,这两家市场领导者的策略蓝图正在影响整个 MicroLED 市场的更广泛的资本配置。

海湾合作委员会和东亚地区透明弹性零售指示牌的普及

杜拜的豪华购物中心和首尔的旗舰店正在安装无边框透明的MicroLED建筑幕墙,将数位内容与实体零售融为一体。天马的PID原型设计户外亮度高达4000尼特,展现出其优于LCD萤幕的性能优势。模组化架构简化了客製化尺寸,缩短了零售整合商的安装週期。此外,其卓越的能源效率也降低了全天候运作的总拥有成本。这些优势巩固了数位指示牌38%的应用领先地位,并为MicroLED市场开闢了新的收入来源。

4吋晶圆上10微米以下LED的量产产量比率低于60%。

在大型基板上放置数百万个微型发送器,其精度仍低于 60%,导致废品率上升,生产线运转率下降。设备製造商正在尝试采用雷射诱导转移和电磁拾取技术来实现 99.99% 的放置精度,其中 ViewReal 的 MicroSolid Printing 技术已展现出小于 7µm 间距的放置能力。在这些解决方案成熟之前,MicroLED 的产出成本将高于 OLED,这将限制其在 MicroLED 市场中近期在大众电视和智慧型手机领域的应用。

细分市场分析

到2024年,数位电子看板将占总收入的38%,这表明MicroLED非常适合用于打造高衝击力、日光下清晰可见的电视墙。高端零售连锁店正在采用可形成无缝拼接的模组化组件,而交通运输机构则利用MicroLED的低故障率来製作重要的资讯显示器。该领域的稳定订单有助于实现早期运转率,并进一步巩固MicroLED市场。

相较之下,智慧型手錶的出货量将与消费性电子产品的发布週期同步成长。受电池续航限制的可穿戴设备需要功耗低于1瓦的显示屏,而3000尼特的峰值亮度则能提升户外使用体验。预计该细分市场的复合年增长率将达到45%,成为推动销售成长的关键因素。随着像素密度超过4000 PPI,近眼AR模组也将取得进展,为更广泛的应用奠定基础,并支撑MicroLED小面板市场规模的长期扩张。

到2024年,家用电器将占microLED需求的72.1%,因为高阶电视、手錶和智慧型手机都将采用microLED技术的高对比度和长寿命特性。三星的旗舰电视「The Wall」安装在大型展示柜中,售价不斐。这个领域将在microLED市场中扮演核心角色,稳定对背板、驱动IC和侦测工具等组件的需求。

随着欧洲阳光可见度法规日益严格,汽车市场对抬头显示器(HUD)的需求正以47%的复合年增长率成长。 HUD原型机的亮度已超过10,000尼特,确保透过偏光挡风玻璃也能清晰可见。其优异的耐温性和抗振性也符合AEC-Q标准。随着越来越多的汽车製造商整合先进的驾驶员显示屏,用于驾驶座电子设备的microLED市场规模将不断扩大,使收入来源不再局限于消费性电子产品。

到2024年,50吋以上尺寸的面板将占总收入的55.6%。豪华住宅和企业大厅正在采用110英寸至220英寸的面板,其安装灵活性和无与伦比的峰值亮度使其高昂的价格物有所值。高端酒店场所正在利用无边框面板打造沉浸式体验,进一步巩固其在MicroLED市场的领先地位。

到2030年,随着製造技术的突破降低晶粒成本,10吋以下面板的复合年增长率将达到49%。 1吋以下微型显示器的像素密度将达到6500 PPI,用于VR头戴装置;而汽车仪錶板需要小尺寸、高解析度的显示器。先进转印的应用将加速技术进步,这意味着未来十年,小尺寸面板的产量将日益再形成市场动态。

区域分析

亚太地区预计到2024年将占全球营收的46.9%,主要得益于台湾的后端优势和韩国深厚的显示技术。京东方收购HC SemiTek以及三安半导体20亿美元的晶圆厂建设计画凸显了持续的资本流入。包括氮化镓晶圆出口退税在内的政府支持措施,正帮助该地区保持成本优势,并巩固其在MicroLED市场的领先地位。

北美地区将以43%的复合年增长率(CAGR)实现最快成长,直至2030年。 《晶片法案》(CHIPS Act)下的联邦激励措施将刺激新的氮化镓生产线建设,而国防和扩增实境/虚拟实境(AR/VR)项目将锁定采购合约。苹果公司多地点的研发中心和Meta公司在头戴式设备领域的雄心壮志将集中生态系统活动,推动稳健的设计迭代,并支援不断增长的基板需求。

欧洲将在汽车和工业应用领域发挥专业作用。强制性的太阳能电池可读性将加速抬头显示器(HUD)的集成,而本地一级供应商将与亚洲LED製造商合作,以确保稳定的晶片供应。欧盟对无尘室维修的补贴将促进新兴晶圆供应基地的形成,同时为因应亚洲市场垄断提供战略对冲。中东和非洲的推广应用将首先从海湾合作委员会(GCC)购物中心的高端零售指示牌开始,而拉丁美洲将试行与体育基础设施投资相关的大型场馆显示器。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 苹果和三星发表MicroLED穿戴装置蓝图,加速对小型显示器的需求

- 在波湾合作理事会和东亚地区推广透明且灵活的零售标牌

- 由美国和欧盟政府资助的国防级微型显示器

- 台湾迷你LED成本下降,使得微型LED的试生产成为可能。

- 欧洲汽车阳光可视性标准推动微型LED抬头显示器的集成

- 市场限制

- 在4吋晶圆上,10µm以下LED的质量传递效率低于60%

- 非标准化车辆鑑定通讯协定

- 氮化镓硅基晶片供应集中在亚洲

- 超过6亿美元的资本支出需求限制了南美洲和非洲的扩张。

- 产业生态系分析

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过使用

- 智慧型手錶

- 近场观看设备(AR/VR)

- 电视机

- 智慧型手机和平板电脑

- 显示器和笔记型电脑

- 抬头显示器

- 数位电子看板

- 微型投影仪

- 医疗和外科展示

- 工业检查面板

- 按最终用途行业划分

- 消费性电子产品

- 车

- 航太与国防

- 卫生保健

- 广告与零售

- 工业和製造业

- 其他的

- 按面板尺寸

- 10吋以下(小型和微型显示器)

- 10 至 50 英吋(中)

- 50吋或更大(大号)

- 像素间距

- 细间距(小于1.5毫米)

- 标准(1.5-2.5毫米)

- 大号(超过 2.5 毫米)

- 按技术(彩色)

- RGB全彩

- 单色

- 按组件

- 外延芯片

- 背板

- 驱动IC

- 转移和连接设备

- 检查和维修工具

- 透过製造工艺

- 传质

- 外延芯片晶圆键合技术

- 杂化键

- 报价

- 显示模组

- 照明模组

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 东南亚

- 亚太其他地区

- 南美洲

- 巴西

- 其他南美洲

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Samsung Electronics Co. Ltd.

- Sony Corporation

- LG Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- AU Optronics Corp.

- Epistar Corporation

- PlayNitride Inc.

- Innolux Corporation

- Apple Inc.(LuxVue Technology)

- Tianma Microelectronics Co. Ltd.

- Nichia Corporation

- Sharp Corporation

- VueReal Inc.

- Plessey Semiconductors Ltd.

- Aledia SA

- Ostendo Technologies Inc.

- Rohinni LLC

- Leyard Optoelectronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- Allos Semiconductors GmbH

- Optovate Ltd.

- Foxconn(Hon Hai Precision)

- Konka Group Co. Ltd.

第七章 市场机会与未来展望

The Micro LED market stood at USD 0.42 billion in 2025 and is forecast to reach USD 2.41 billion by 2030, advancing at a 41.83% CAGR.

Commercial traction hinges on the technology's high brightness, low power draw, and proven longevity that outperforms LCD and OLED displays. Manufacturers are steadily lifting mass-transfer yields, and capital-intensive pilot lines in Taiwan and South Korea are scaling the technology for wearables, large-format signage, and automotive cockpits. Asia Pacific commands manufacturing leadership on the back of mature semiconductor ecosystems and supportive industrial policies, while North America is accelerating investment for defense and AR/VR programs. Pricing remains elevated, yet end-users with severe power, thermal, or sunlight-readability constraints are moving first, reinforcing premium positioning and underscoring the long-run competitiveness of the Micro LED market.

Global Micro LED Market Trends and Insights

Apple and Samsung Roadmaps for Micro-LED Wearables Accelerating Small-Display Demand

Apple's USD 3 billion outlay since acquiring LuxVue and Samsung's parallel R&D programs signal long-term commitment despite near-term schedule shifts. Rising design wins for driver ICs and transfer equipment suppliers indicate a supply-chain pivot toward sub-2-inch panels. High brightness, stringent power budgets, and demand for outdoor readability underpin a projected 45% CAGR for smartwatch displays. Specialized tool vendors are commercializing high-throughput pick-and-place systems, helping democratize pilot production beyond flagship brands. This dynamic underlines how strategic roadmaps from two market leaders shape broader capital allocation across the Micro LED market.

Transparent and Flexible Retail Signage Uptake in GCC and East Asia

Luxury malls in Dubai and flagships in Seoul are installing bezel-less, transparent Micro LED facades that merge digital content with physical storefronts. Tianma's PID prototypes, engineered for 4,000-nit outdoor brightness, illustrate performance headroom over LCD alternatives. Modular architectures simplify custom dimensions, trimming installation cycles for retail integrators. Energy efficiency also reduces total cost of ownership for 24/7 operation. These attributes safeguard the 38% application lead held by digital signage and set the stage for new revenue pools inside the Micro LED market.

Mass-Transfer Yield Sub 60% for Sub-10 µm LEDs Beyond 4-Inch Wafers

Placement accuracy for millions of micro-emitters on large substrates remains below 60%, inflating scrap rates and depressing line utilization. Equipment makers are trialing laser-induced transfer and electromagnetic pick-up to reach 99.99% placement accuracy, while VueReal's MicroSolid Printing demonstrates sub-7 µm pitch capability. Until these solutions mature, output costs will stay above OLED equivalents, limiting near-term penetration in mass-market televisions and smartphones inside the Micro LED market.

Other drivers and restraints analyzed in the detailed report include:

- Defense-Grade Micro-Displays Funded by US and EU Governments

- Taiwanese Mini-LED Cost Decline Enabling Pilot Micro-LED Lines

- GaN-on-Si Wafer Supply Concentration in Asia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital signage delivered 38% of 2024 revenue, validating Micro LED's suitability for high-impact, day-light-readable video walls. Luxury retail chains deploy modular tiles that form seamless canvases, while transportation hubs favor Micro LED's low failure rates for critical information boards. The segment's stable order flow underpins early capacity utilization, reinforcing the Micro LED market.

Smartwatch shipments, in contrast, scale with consumer electronics release cycles. Battery-limited wearables demand sub-1-watt displays, and 3,000-nit peak brightness extends outdoor usability. The segment's 45% forecast CAGR positions it as a pivotal volume driver. Near-eye AR modules are also progressing as pixel densities exceed 4,000 PPI, setting the stage for broader adoption and supporting the long-run expansion of the Micro LED market size at the small-panel end.

Consumer electronics captured 72.1% of 2024 demand as premium TVs, watches, and smartphones embraced the technology's high contrast and longevity. Samsung's flagship television line, The Wall, anchors large-screen showcase deployments and validates premium pricing. The segment's breadth stabilizes component demand across backplanes, driver ICs, and inspection tools, cementing its central role in the Micro LED market.

Automotive demand is rising at a projected 47% CAGR amid stricter European sun-readability mandates. HUD prototypes achieve over 10,000 nits, ensuring legibility through polarized windscreens. Extended temperature tolerance and vibration resistance also meet AEC-Q standards. As more carmakers integrate advanced driver displays, the Micro LED market size for cockpit electronics is set to widen, diversifying revenue beyond consumer gadgets.

Panels larger than 50 inches held 55.6% of 2024 revenue. Luxury residential and corporate lobbies adopt 110-inch to 220-inch assemblies where installation flexibility and unrivaled peak luminance justify premium prices. High-end hospitality venues leverage bezel-free surfaces to create immersive experiences, reinforcing share dominance within the Micro LED market.

Panels below 10 inches will grow 49% CAGR to 2030 as manufacturing breakthroughs lower cost per die. Sub-1-inch micro-displays now reach 6,500 PPI for VR headsets, and smart-instrument clusters in vehicles demand compact, high-resolution formats. Adoption of advanced transfer printing hastens the learning curve, signaling that small-panel volumes will increasingly reshape Micro LED market share dynamics later in the decade.

The Micro LED Market Report is Segmented by Application (Smartwatch, and More), End-Use Industry (Automotive, and More), Panel Size (Less Than 10 Inch, and More), Pixel Pitch (Fine Pitch, and More), Technology (Color) (RGB, and More), Component (Epitaxial Wafers, and More), Manufacturing Process (Mass Transfer, and More), Offering (Display Modules, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held 46.9% of 2024 revenue, powered by Taiwan's role in back-end processing and South Korea's deep display know-how. BOE's acquisition of HC SemiTek and Sanan's USD 2 billion fab plan underscore continued capital inflows. Government facilitation, including export rebates on GaN wafers, sustains regional cost advantages and solidifies leadership in the Micro LED market.

North America is growing fastest at 43% CAGR to 2030. Federal incentives under the CHIPS Act spur new gallium-nitride lines, while defense and AR/VR programs lock in offtake agreements. Apple's multi-site R&D footprint and Meta's headset ambitions concentrate ecosystem activity, driving robust design iterations and supporting higher substrate demand.

Europe carves out a specialty role in automotive and industrial deployments. Sun-readability mandates accelerate HUD integration, and local tier-1 suppliers collaborate with Asian LED makers to secure stable die flow. Parallel EU subsidies for clean-room retrofits nurture a nascent wafer supply base, providing strategic hedges against Asian concentration. Adoption in Middle East and Africa begins with premium retail signage in GCC malls, whereas Latin America pilots large-venue displays tied to sports infrastructure investments.

- Samsung Electronics Co. Ltd.

- Sony Corporation

- LG Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- AU Optronics Corp.

- Epistar Corporation

- PlayNitride Inc.

- Innolux Corporation

- Apple Inc. (LuxVue Technology)

- Tianma Microelectronics Co. Ltd.

- Nichia Corporation

- Sharp Corporation

- VueReal Inc.

- Plessey Semiconductors Ltd.

- Aledia SA

- Ostendo Technologies Inc.

- Rohinni LLC

- Leyard Optoelectronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- Allos Semiconductors GmbH

- Optovate Ltd.

- Foxconn (Hon Hai Precision)

- Konka Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Apple and Samsung Roadmaps for Micro-LED Wearables Accelerating Small-Display Demand

- 4.2.2 Transparent and Flexible Retail Signage Uptake in Gulf Cooperation Council Countries and East Asia

- 4.2.3 Defense-grade Micro-Displays Funded by United States and EU Governments

- 4.2.4 Taiwanese Mini-LED Cost Decline Enabling Pilot Micro-LED Lines

- 4.2.5 European Automotive Sun-Readability Norms Boosting Micro-LED HUD Integration

- 4.3 Market Restraints

- 4.3.1 Mass-Transfer Yield Sub 60 % for Sub-10 µm LEDs Beyond 4-inch Wafers

- 4.3.2 Non-standardised Automotive Qualification Protocols

- 4.3.3 GaN-on-Si Wafer Supply Concentration in Asia

- 4.3.4 More than USD 600 m Capex Requirement Limiting Expansion in South America and Africa

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Application

- 5.1.1 Smartwatch

- 5.1.2 Near-to-Eye Devices (AR/VR)

- 5.1.3 Television

- 5.1.4 Smartphone and Tablet

- 5.1.5 Monitor and Laptop

- 5.1.6 Head-up Display

- 5.1.7 Digital Signage

- 5.1.8 Micro-Projector

- 5.1.9 Medical and Surgical Displays

- 5.1.10 Industrial Inspection Panels

- 5.2 By End-use Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive

- 5.2.3 Aerospace and Defense

- 5.2.4 Healthcare

- 5.2.5 Advertising and Retail

- 5.2.6 Industrial and Manufacturing

- 5.2.7 Others

- 5.3 By Panel Size

- 5.3.1 Less than 10 inch (Small and Micro-Displays)

- 5.3.2 10 - 50 inch (Medium)

- 5.3.3 Above 50 inch (Large)

- 5.4 By Pixel Pitch

- 5.4.1 Fine Pitch (Less than 1.5 mm)

- 5.4.2 Standard (1.5 - 2.5 mm)

- 5.4.3 Large (Above 2.5 mm)

- 5.5 By Technology (Color)

- 5.5.1 RGB Full-Color

- 5.5.2 Monochrome

- 5.6 By Component

- 5.6.1 Epitaxial Wafers

- 5.6.2 Backplanes

- 5.6.3 Driver ICs

- 5.6.4 Transfer and Bonding Equipment

- 5.6.5 Inspection and Repair Tools

- 5.7 By Manufacturing Process

- 5.7.1 Mass Transfer

- 5.7.2 Epitaxial Wafer Bonding

- 5.7.3 Hybrid Bonding

- 5.8 By Offering

- 5.8.1 Display Modules

- 5.8.2 Lighting Modules

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Mexico

- 5.9.2 Europe

- 5.9.2.1 Germany

- 5.9.2.2 United Kingdom

- 5.9.2.3 France

- 5.9.2.4 Italy

- 5.9.2.5 Spain

- 5.9.2.6 Rest of Europe

- 5.9.3 Asia-Pacific

- 5.9.3.1 China

- 5.9.3.2 Japan

- 5.9.3.3 South Korea

- 5.9.3.4 India

- 5.9.3.5 South East Asia

- 5.9.3.6 Rest of Asia-Pacific

- 5.9.4 South America

- 5.9.4.1 Brazil

- 5.9.4.2 Rest of South America

- 5.9.5 Middle East and Africa

- 5.9.5.1 Middle East

- 5.9.5.1.1 United Arab Emirates

- 5.9.5.1.2 Saudi Arabia

- 5.9.5.1.3 Rest of Middle East

- 5.9.5.2 Africa

- 5.9.5.2.1 South Africa

- 5.9.5.2.2 Rest of Africa

- 5.9.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co. Ltd.

- 6.4.2 Sony Corporation

- 6.4.3 LG Display Co. Ltd.

- 6.4.4 BOE Technology Group Co. Ltd.

- 6.4.5 AU Optronics Corp.

- 6.4.6 Epistar Corporation

- 6.4.7 PlayNitride Inc.

- 6.4.8 Innolux Corporation

- 6.4.9 Apple Inc. (LuxVue Technology)

- 6.4.10 Tianma Microelectronics Co. Ltd.

- 6.4.11 Nichia Corporation

- 6.4.12 Sharp Corporation

- 6.4.13 VueReal Inc.

- 6.4.14 Plessey Semiconductors Ltd.

- 6.4.15 Aledia SA

- 6.4.16 Ostendo Technologies Inc.

- 6.4.17 Rohinni LLC

- 6.4.18 Leyard Optoelectronics Co. Ltd.

- 6.4.19 Seoul Semiconductor Co. Ltd.

- 6.4.20 San'an Optoelectronics Co. Ltd.

- 6.4.21 Allos Semiconductors GmbH

- 6.4.22 Optovate Ltd.

- 6.4.23 Foxconn (Hon Hai Precision)

- 6.4.24 Konka Group Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

微型LED光学引擎市场:按组件、技术、材料、应用和终端用户产业分類的全球预测(2026-2032年)微型LED晶圆质传设备市场:2026-2032年全球预测(依设备类型、传输技术、晶圆尺寸、自动化程度及最终用途产业划分)

微型LED光学引擎市场:按组件、技术、材料、应用和终端用户产业分類的全球预测(2026-2032年)微型LED晶圆质传设备市场:2026-2032年全球预测(依设备类型、传输技术、晶圆尺寸、自动化程度及最终用途产业划分) MicroLED市场规模、份额和成长分析:按应用、显示像素密度、最终用途和地区划分-产业预测(2026-2033年)

MicroLED市场规模、份额和成长分析:按应用、显示像素密度、最终用途和地区划分-产业预测(2026-2033年) GaN MicroLED市场分析与预测(至2035年):按类型、产品类型、服务、技术、组件、应用、材料类型、装置、最终用户和功能划分MicroLED市场分析及预测(至2035年):按类型、产品、技术、组件、应用、材料类型、装置、最终用户和製程划分

GaN MicroLED市场分析与预测(至2035年):按类型、产品类型、服务、技术、组件、应用、材料类型、装置、最终用户和功能划分MicroLED市场分析及预测(至2035年):按类型、产品、技术、组件、应用、材料类型、装置、最终用户和製程划分 2026年全球微型发光二极体(LED)显示器市场报告AR微光学引擎市场按技术、引擎类型、显示类型、解析度和应用划分-2026-2032年全球预测扩增实境光学引擎市场:按设备、组件、技术和最终用户产业划分 - 全球预测(2026-2032 年)

2026年全球微型发光二极体(LED)显示器市场报告AR微光学引擎市场按技术、引擎类型、显示类型、解析度和应用划分-2026-2032年全球预测扩增实境光学引擎市场:按设备、组件、技术和最终用户产业划分 - 全球预测(2026-2032 年) 全球微型LED大容量传输市场:依产品类型、应用和地区划分 - 市场规模、产业趋势、机会分析和预测(2026-2035)

全球微型LED大容量传输市场:依产品类型、应用和地区划分 - 市场规模、产业趋势、机会分析和预测(2026-2035) OLED供应链市场:2025-2030年预测

OLED供应链市场:2025-2030年预测