|

市场调查报告书

商品编码

1850983

智慧卡:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Smart Card - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

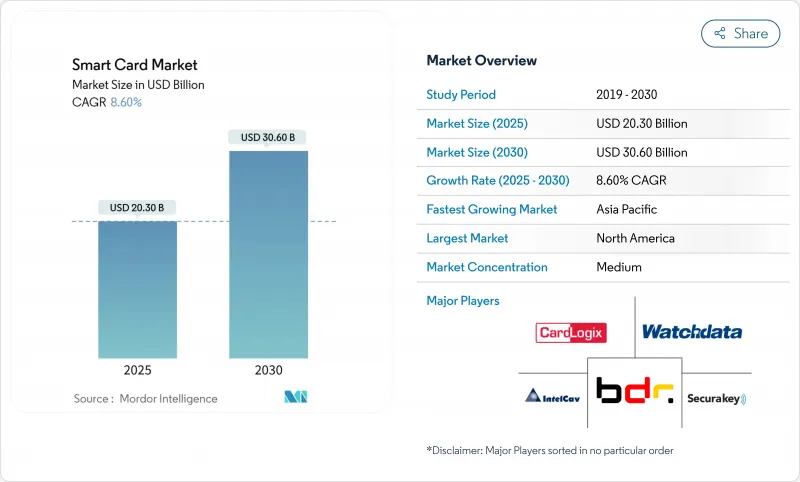

预计到 2025 年智慧卡市场规模将达到 203 亿美元,到 2030 年将达到 306 亿美元,在预测期内复合年增长率将达到 8.6%。

向EMV晶片卡的持续转型、国家数位身分专案的扩展以及对多应用凭证日益增长的需求,持续推动成长。非接触式技术现已成为零售支付的主流,双界面卡为仅拥有传统接触式卡的发卡机构提供了一条循序渐进的升级路径。随着政府和企业融合实体身份和数位身份,卡片上的安全元素正迅速普及,为保全服务创造了新的商机。从区域来看,亚洲拥有最大的安装基础,但非洲预计将迎来最大的成长,因为非洲以行动优先的支付生态系统正在将发卡业务拓展到先前未开发的客户群。儘管竞争程度适中,但第一线製造商正透过永续性相关产品和生物辨识创新来增强其市场份额,从而在价格之外实现差异化。

全球智慧卡市场趋势与洞察

新兴亚洲国家向非接触式EMV的过渡

2024年,孟加拉和尼泊尔建立了本地EMV 3级测试实验室,缩短了认证週期,降低了发卡机构的成本,并加快了EMV技术的推广速度。中国非接触式交易量年增率达37%,印度发卡量年增率达42%。这些数据反映了非接触式支付的普及,并凸显了终端升级所需的基础设施。在竞争激烈的零售市场中,银行将非接触感应卡视为客户维繫手段,而商家则受益于更快的结帐速度,从而提高了交易效率。目前,EMV卡已占全球发卡量的70%,亚洲发卡机构已做好充分准备,直接转换为双介面产品组合。因此,短期销售成长将主要集中在能够支援交通票务和小额线下支付等附加价值服务的安全微控制器卡上。

欧盟和海湾合作委员会国家电子身分证和数位健康卡推广计划

欧盟数位身分法规将于2024年5月生效,届时成员国将被要求同时提供实体卡片和行动凭证,这将持续推高对高安全性聚碳酸酯卡的需求。海湾合作委员会(GCC)国家在推动医疗服务和边境管制系统现代化的同时,也采取类似的措施。目前,CoreLam等公司的聚碳酸酯嵌体已应用于20多个国家专案中。製造商受益于多年期供应合同,这些合同有利于那些能够提供个性化定制、密钥管理和安全小程序加载等服务的垂直整合型企业。电子钱包的普及需要时间,因此,实体电子身分证的发放仍将作为强制性的备用方案,并在过渡期内锁定基本单位数量。

代币化虚拟卡的兴起降低了实体卡的需求。

预计到2027年,虚拟卡交易量将成长四倍,超过1,210亿笔,而万事达卡的目标是标记化,并减少低价值借记卡组合的更换週期。虽然实体卡对于线下交易和线下备用方案仍然至关重要,但在成熟市场,钱包份额可能会向加密货币倾斜,从而减缓实体卡的销售成长。

细分市场分析

到2024年,非接触感应卡将占智慧卡市场份额的54%,进一步巩固其作为日常支付外形规格的地位。双介面卡的发行量正以8.7%的复合年增长率成长,发卡机构力求在不影响非接触式支付功能的前提下,实现与传统接触式终端的向下相容。 EMV C-8通用核心等创新技术降低了终端认证的复杂性,并推动了其更广泛的应用。同时,英飞凌晶片组的改进缩短了交易时间,并提升了高吞吐量零售环境下的用户体验。

发卡机构对非接触式卡的需求在政府和国防部门依然强劲,因为实体介面能够增强安全性,有效抵御继电器攻击。混合卡将多种技术整合于单张基板,以满足特定企业对逻辑和实体混合存取的需求。因此,竞争格局正从纯粹的介面类型转向生物辨识卡匹配和发卡后个人化等增值功能。

到2024年,微控制器卡将占据智慧卡市场62%的份额,这反映了其在支付、电信和身分识别等应用场景中的多功能性;而受电子识别和数位钱包生态系统中日益增长的加密需求驱动,安全元件卡将以10.2%的复合年增长率增长。 SECORA Pay Bio的承包平台展示如何将感测器整合与安全元件捆绑在一起,从而降低物料成本并缩短产品上市时间。

仅记忆卡仍然适用于公共交通和预付礼品卡等应用程式场景,在这些场景中,成本敏感度高于处理需求。像恩智浦半导体 (NXP) 的 MOB10 这样的超薄模组透过提高抗弯曲应力能力,为护照应用开闢了新的途径。总体而言,产品组合向安全元件的转变有利于拥有通用准则 (Common Criteria) 认证产品线的半导体供应商,从而在市场中保持技术主导的护城河。

区域分析

2024年,亚洲将以44%的营收份额引领智慧卡市场,这主要得益于EMV晶片卡的快速普及和国民身分证的发行。儘管中国已拥有QR CODE支付生态系统,但其非接触式交易量仍较去年同期成长37%。印度的非接触感应卡发行量增加了42%,但农村地区的基础设施不足阻碍了其广泛应用。日本正在试办生物辨识支付卡,以因应卡片诈骗激增30%的问题,并预计到2028年,非接触式支付交易额将达到8,700亿美元。

欧洲在价值方面排名第二。 eIDAS-2.0 的强制要求正在推动对实体和数位身分的需求,北欧公司正在率先开发 FIDO2 硬体金钥。 GDPR 相关的复杂性正在减缓跨国发卡平台的发展,并促使发卡机构转向国家级个人化中心。万事达卡承诺在 2030 年实现全面代币化,这标誌着向数位凭证的逐步转变。

非洲是成长最快的地区,复合年增长率达9.3%。 2024年,行动支付服务交易金额将达到1.68兆美元,这将推动对配对签帐金融卡的需求。南非的卡片付款将在2025年超过1,580亿美元,埃及的目标是到2030年实现1,040亿美元的数位支付额。 Orange MEA和万事达卡等策略联盟的目标是到2025年为4,000万用户实现支付数位化。北美致力于减少数位诈骗,南美将受益于SIM卡的扩展,而澳洲已在其2025-2028年安全蓝图中优先考虑令牌化技术(visa.com.au)。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴亚洲经济体向非接触式EMV的过渡

- 欧盟和海湾合作委员会国家电子身分证和数位健康卡推广计划

- 拉丁美洲预付SIM卡的成长推动了安全元件的普及

- 欧盟 eIDAS-2.0 数位钱包法规简介

- 转向永续性的再生塑料和生质塑胶卡片

- FIDO2卡上生物识别认证在北欧的普及

- 市场限制

- 代币化虚拟卡的兴起降低了实体卡的需求

- 解决MCU供应链的不稳定问题

- GDPR 导致跨境发行平台延迟

- 诈欺行为转移到非接触式支付管道导致北美信用卡升级率下降

- 供应链分析

- 监理与技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 供应商定位分析

- 投资分析

第五章 市场规模与成长预测

- 按介面类型

- 接触

- 非接触式

- 双介面

- 杂交种

- 按卡晶片类型

- 记忆

- 微控制器

- 卡上安全元件/系统

- 材料

- PVC

- 聚碳酸酯(PC)

- ABS

- PETG和生物基塑料

- 金属和复合材料

- 按功能/用途

- 支付与银行

- 识别和电子身份识别

- 门禁控制和物理安全

- 通讯和SIM卡

- 交通票

- 医疗保健和保险

- 零售与忠诚度

- 按最终用户行业划分

- BFSI

- 资讯科技和通讯

- 政府和公共部门

- 运输/物流

- 卫生保健

- 零售和酒店业

- 教育及其他

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- Vendor Positioning Analysis

- 公司简介

- Thales Group(Gemalto)

- IDEMIA

- Giesecke and Devrient GmbH

- Infineon Technologies AG

- HID Global(Assa Abloy AB)

- NXP Semiconductors NV

- CPI Card Group Inc.

- Watchdata Technologies

- Bundesdruckerei GmbH

- Fingerprint Cards AB

- Samsung Electronics Co., Ltd.

- KONA I Co., Ltd.

- CardLogix Corporation

- IntelCav

- Secura Key

- Alioth LLC

- Eastcompeace Technology Co., Ltd.

- American Banknote Corporation(ABCorp)

- Paragon ID(ASK)

- Shenzhen Hengbao Co., Ltd.

- VALID SA

第七章 市场机会与未来展望

The smart card market size stands at USD 20.3 billion in 2025 and is projected to reach USD 30.6 billion by 2030, advancing at an 8.6% CAGR through the forecast period.

Consistent migration to EMV, expanding national digital-identity programs, and rising demand for multi-application credentials continue to anchor growth. Contactless technology is now mainstream in retail payments, while dual-interface cards offer an incremental upgrade path for issuers that still maintain legacy contact-only estates. Secure elements on cards are witnessing rapid uptake as governments and enterprises converge physical and digital identity, a trend that creates adjacent opportunities in cybersecurity services. Regionally, Asia commands the largest installed base, yet the deepest expansion runway lies in Africa, where mobile-first payment ecosystems unlock card issuance at previously untapped customer tiers. Competitive intensity is moderate; tier-one manufacturers are consolidating share through sustainability-linked products and biometric innovations that create differentiation beyond price.

Global Smart Card Market Trends and Insights

Contactless EMV Migration in Emerging Asian Economies

Roll-out momentum accelerated in 2024 as Bangladesh and Nepal commissioned local EMV Level 3 test labs that shorten certification cycles and cut issuer costs. China saw a 37% annual rise in contactless transactions, while India logged 42% growth in issuance, figures that reflect the mainstreaming of tap-to-pay and underscore the addressable base for terminal upgrades. Banks frame contactless issuance as a retention lever in overcrowded retail markets, and merchants benefit from faster checkout speeds that lift throughput. With EMV-enabled cards already accounting for 70% of global issuance, Asian issuers are positioned to leapfrog directly to dual-interface portfolios. Near-term sales growth, therefore, skews toward secure microcontroller cards able to support value-added services such as transit ticketing and small-value offline payments.

EU & GCC National eID and Digital Health Card Roll-outs

Implementation of the EU Digital Identity Regulation in May 2024 obliges member states to provide physical and mobile credentials in parallel, sustaining demand for high-security polycarbonate cards. GCC countries follow a similar path as they modernize healthcare delivery and border-control frameworks. Polycarbonate inlays such as CoreLam are now deployed in 20+ national programs. Manufacturers gain from multi-year supply contracts that favor vertically integrated players capable of personalisation, key management, and secure applet loading. Because wallet adoption will take time, physical eID issuance remains a mandatory fallback, locking in baseline unit volumes during the transition period.

Rise of Tokenised Virtual Cards Reducing Physical Demand

Virtual card transactions are forecast to quadruple to more than 121 billion by 2027, while Mastercard targets 100% e-commerce tokenisation in Europe by 2030. The shift diverts issuer budgets toward digital engagements and shrinks replacement cycles for low-value debit portfolios. Physical cards remain essential for face-to-face acceptance and offline fallback, yet the share of wallet could tilt toward virtual instruments in mature markets, dampening unit growth.

Other drivers and restraints analyzed in the detailed report include:

- Pre-paid SIM Expansion Driving Secure Elements in Latin America

- EU eIDAS-2.0 digital wallet regulation adoption

- Secure MCU Supply-chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contactless cards accounted for 54% of the smart card market size in 2024, reaffirming their status as the de facto form factor for everyday payments. Dual-interface issuance is rising at an 8.7% CAGR as issuers seek backward compatibility with legacy contact-only terminals without compromising tap-to-pay functionality. Innovations such as the EMV C-8 universal kernel reduce terminal certification complexity and catalyse acceptance expansion. In parallel, chipset improvements from Infineon shorten transaction time, improving user experience in high-throughput retail environments.

Issuer appetite for contact-only cards persists in government and defence, where a physical interface adds a security layer against relay attacks. Hybrid cards, embedding multiple technologies on a single substrate, satisfy niche enterprise requirements for logical and physical access convergence. The competitive narrative, therefore, shifts from mere interface type to value-added capabilities such as biometric match-on-card and post-issuance personalisation, themes that enable vendors to defend margins in the smart card market.

Microcontroller cards captured 62% of the smart card market share in 2024, reflecting their versatility across payments, telecom, and identity use cases. Secure element cards, however, are expanding at a 10.2% CAGR thanks to heightened cryptographic requirements in eID and digital-wallet ecosystems. The SECORA Pay Bio turnkey platform exemplifies how sensor integration and secure elements can be bundled to compress the bill-of-materials and time-to-market.

Memory-only cards remain relevant for mass transit and prepaid gift applications where cost sensitivity outweighs processing needs. Ultra-thin modules such as NXP's MOB10 unlock new passport applications by improving durability against bending stress. Overall, the product-mix shift toward secure elements benefits semiconductor suppliers with certified Common Criteria product lines, sustaining a technology-led competitive moat within the smart card market.

Smart Card Market Report is Segmented by Interface Type (Contact, Contact-Based, and More), Card Chip Type (Memory, Microcontroller, and More), Material (PVC, Polycarbonate, and More), Application (Payment and Banking, and More), End-User Vertical (BFSI, IT and Telecommunication, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia led the smart card market with 44% revenue share in 2024, anchored by rapid EMV penetration and national ID issuances. Contactless transactions in China rose 37% year-on-year despite coexistence with QR payment ecosystems. India logged 42% growth in contactless card issuance, though rural infrastructure gaps temper full-scale adoption. Japan, responding to a 30% spike in credit-card fraud, is piloting biometric payment cards and expects contactless payment value to reach USD 870 billion by 2028.

Europe holds second place by value. The eIDAS-2.0 mandate drives both physical and digital identity demand, while Nordic enterprises pioneer FIDO2 hardware keys. GDPR-linked complexity delays multi-country issuance platforms, nudging issuers toward domestically hosted personalization centres. Mastercard's commitment to full tokenisation by 2030 signals a gradual pivot to digital credentials, yet physical cards remain obligatory for offline verification and multi-channel access.

Africa is the fastest-growing region at a 9.3% CAGR. Mobile-money services processed transactions worth USD 1.68 trillion in 2024, catalysing demand for companion debit cards. South-African card payments will surpass USD 158 billion in 2025, while Egypt targets USD 104 billion in digital payments by 2030. Strategic alliances, such as Orange MEA and Mastercard, aim to digitize payments for 40 million users by 2025. North America emphasizes digital-fraud mitigation, South America benefits from SIM expansion, and Australia prioritizes tokenisation under its 2025-2028 security roadmap, visa.com.au.

- Thales Group (Gemalto)

- IDEMIA

- Giesecke and Devrient GmbH

- Infineon Technologies AG

- HID Global (Assa Abloy AB)

- NXP Semiconductors N.V.

- CPI Card Group Inc.

- Watchdata Technologies

- Bundesdruckerei GmbH

- Fingerprint Cards AB

- Samsung Electronics Co., Ltd.

- KONA I Co., Ltd.

- CardLogix Corporation

- IntelCav

- Secura Key

- Alioth LLC

- Eastcompeace Technology Co., Ltd.

- American Banknote Corporation (ABCorp)

- Paragon ID (ASK)

- Shenzhen Hengbao Co., Ltd.

- VALID S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Contactless EMV Migration in Emerging Asian Economies

- 4.2.2 EU and GCC National eID and Digital Health Card Roll-outs

- 4.2.3 Pre-paid SIM Expansion Driving Secure Elements in LATAM

- 4.2.4 EU eIDAS-2.0 Digital Wallet Regulation Adoption

- 4.2.5 Sustainability-Driven Shift to Recycled and Bio-Plastic Cards

- 4.2.6 Biometric FIDO2 On-card Authentication Uptake in Nordics

- 4.3 Market Restraints

- 4.3.1 Rise of Tokenised Virtual Cards Reducing Physical Demand

- 4.3.2 Secure MCU Supply-Chain Volatility

- 4.3.3 GDPR-Driven Delays in Cross-border Issuance Platforms

- 4.3.4 Fraud Migration to CNP Channels Curtailing NA Card Upgrades

- 4.4 Supply Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Vendor Positioning Analysis

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Interface Type

- 5.1.1 Contact

- 5.1.2 Contactless

- 5.1.3 Dual Interface

- 5.1.4 Hybrid

- 5.2 By Card Chip Type

- 5.2.1 Memory

- 5.2.2 Microcontroller

- 5.2.3 Secure Element/System-on-Card

- 5.3 By Material

- 5.3.1 PVC

- 5.3.2 Polycarbonate (PC)

- 5.3.3 ABS

- 5.3.4 PETG and Bio-based Plastics

- 5.3.5 Metal and Composite

- 5.4 By Function/Application

- 5.4.1 Payment and Banking

- 5.4.2 Identification and eID

- 5.4.3 Access Control and Physical Security

- 5.4.4 Telecom and SIM

- 5.4.5 Transportation Ticketing

- 5.4.6 Healthcare and Insurance

- 5.4.7 Retail and Loyalty

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecommunications

- 5.5.3 Government and Public Sector

- 5.5.4 Transportation and Logistics

- 5.5.5 Healthcare

- 5.5.6 Retail and Hospitality

- 5.5.7 Education and Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 GCC

- 5.6.5.2 Turkey

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Positioning Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 Thales Group (Gemalto)

- 6.5.2 IDEMIA

- 6.5.3 Giesecke and Devrient GmbH

- 6.5.4 Infineon Technologies AG

- 6.5.5 HID Global (Assa Abloy AB)

- 6.5.6 NXP Semiconductors N.V.

- 6.5.7 CPI Card Group Inc.

- 6.5.8 Watchdata Technologies

- 6.5.9 Bundesdruckerei GmbH

- 6.5.10 Fingerprint Cards AB

- 6.5.11 Samsung Electronics Co., Ltd.

- 6.5.12 KONA I Co., Ltd.

- 6.5.13 CardLogix Corporation

- 6.5.14 IntelCav

- 6.5.15 Secura Key

- 6.5.16 Alioth LLC

- 6.5.17 Eastcompeace Technology Co., Ltd.

- 6.5.18 American Banknote Corporation (ABCorp)

- 6.5.19 Paragon ID (ASK)

- 6.5.20 Shenzhen Hengbao Co., Ltd.

- 6.5.21 VALID S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

晶片级安全增强市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、製程、最终用户、解决方案划分智慧卡市场分析及预测(至2035年):类型、产品、服务、技术、组件、应用、材质类型、部署类型与最终用户

晶片级安全增强市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、製程、最终用户、解决方案划分智慧卡市场分析及预测(至2035年):类型、产品、服务、技术、组件、应用、材质类型、部署类型与最终用户 2026年全球双介面积体电路卡市场报告

2026年全球双介面积体电路卡市场报告 智慧卡MCU市场-全球产业规模、份额、趋势、机会及预测(依产品、功能、终端用户产业、地区及竞争格局划分),2021-2031年

智慧卡MCU市场-全球产业规模、份额、趋势、机会及预测(依产品、功能、终端用户产业、地区及竞争格局划分),2021-2031年 人工智慧智慧型装置市场:2026-2032年全球预测(按产品类型、最终用户、部署类型、公司规模和通路划分)数位电视智慧型装置市场按面板技术、萤幕大小、解析度、作业系统和销售管道-全球预测(2026-2032 年)

人工智慧智慧型装置市场:2026-2032年全球预测(按产品类型、最终用户、部署类型、公司规模和通路划分)数位电视智慧型装置市场按面板技术、萤幕大小、解析度、作业系统和销售管道-全球预测(2026-2032 年) 智慧卡市场规模、份额和成长分析(按类型、组件、功能、应用和地区划分)—2026-2033年产业预测

智慧卡市场规模、份额和成长分析(按类型、组件、功能、应用和地区划分)—2026-2033年产业预测 智慧卡市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

智慧卡市场机会、成长要素、产业趋势分析及预测(2026年至2035年) 政府证件和国民身分证市场的量子技术准备交通智慧卡市场-全球产业规模、份额、趋势、机会和预测,按卡片类型、最终用户、地区和竞争格局划分,2020-2030年预测

政府证件和国民身分证市场的量子技术准备交通智慧卡市场-全球产业规模、份额、趋势、机会和预测,按卡片类型、最终用户、地区和竞争格局划分,2020-2030年预测