|

市场调查报告书

商品编码

1851005

胶带:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Adhesive Tapes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

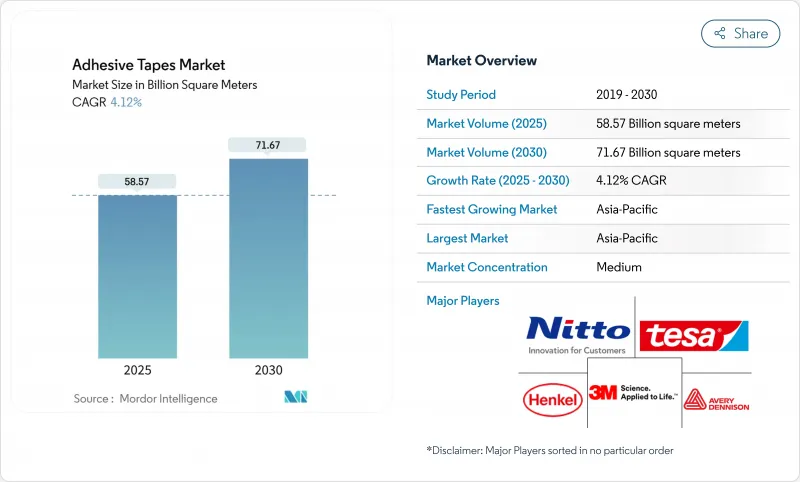

预计到 2025 年,胶带市场规模将达到 585.7 亿平方公尺,到 2030 年将达到 716.7 亿平方公尺,在预测期(2025-2030 年)内,复合年增长率为 4.12%。

来自包装、电子和汽车製造业的稳定需求抵消了原材料成本波动和日益严格的挥发性有机化合物 (VOC)排放法规的影响。随着加工商转向低 VOC 化学品,水性技术正在迅速发展,而压敏胶因其瞬时黏合性和适用于自动化点胶生产线的特性,保持着销量领先地位。亚太地区引领消费和成长,这主要得益于电子产品密集的供应链和庞大的基础设施投入。医疗保健产业正在成为成长最快的经销店,因为亲肤型硅酮黏合剂能够延长医疗设备的使用寿命,从而将价值转移到利润更高的特种等级产品上。领先的製造商正透过垂直整合、区域产能扩张和产品组合调整(转向永续解决方案)来应对成本压力。

全球胶带市场趋势与洞察

电子商务和包装行业的需求增加

数位零售持续推动物流业者采用更快、更安全、更永续的包装。品牌拥有者现在指定使用纤维基易撕胶带和无溶剂纸箱封口系统,以满足可回收性目标并能承受长时间的配送週期。 HB Fuller 的 Earthic 系列产品正是这项转变的典范,它在提供经认证的生物基成分的同时,又不牺牲剪切强度。对合适尺寸纸箱的需求也加速了封箱胶带的客製化,这些胶带可在自动化生产线上黏附于各种瓦楞纸板等级。亚太地区的成长最为显着,跨境小包裹量不断增长,履约中心正在标准化使用水性胶带以减少塑胶用量。这些因素推高了高性能包装平方公尺的平均价格,从而推动了胶带市场的发展。

原始设备製造商转向使用轻质线束胶带

tesa SuperSleeve 51026 PV6 代表了新一代的包覆材料,它将 PET 布与无溶剂丙烯酸黏合剂结合,在高温环境下具有出色的耐磨性。电动车平台正迎来新的发展机会,因为线束的使用时间更长,并且必须保持柔韧性以便于电池组检查。更轻的线束重量有助于延长续航里程,从而促进 OEM 厂商的采用。这些趋势也直接反映在胶带市场,加工商正在调整胶带的宽度和模切方式,以适应自动化线束包覆的需求。

原物料价格波动

增粘树脂和专门食品炭黑等原料价格随原油价格和运输成本波动,对加工商的利润空间造成压力。卡博特公司宣布,受通膨压力影响,炭黑价格将于2024年12月起调高。儘管生产商正透过多供应商采购和指数化合约来缓解价格上涨的影响,但他们仍然面临着营运资金压力,这阻碍了中小加工商的扩张计划,并在短期内拖累了胶带市场。

细分市场分析

丙烯酸酯配方将成为胶带市场最大的贡献者,预计到2024年将销售量的41.12%。其优异的抗紫外线性能和老化稳定性推动了其在户外电子产品和太阳能电池组件领域的应用。橡胶基系统虽然耐久性稍逊,但由于汽车製造商青睐其在线束捆扎和车内NVH控制方面具有高初始粘合力,因此其市场正以4.24%的复合年增长率快速增长。硅酮压敏胶的销售量虽然不高,但其生物相容性和200°C的工作温度使其在医疗穿戴式装置和耐高温电子产品领域拥有较高的价格。环氧树脂和聚氨酯材料则满足了结构胶合剂的需求,这类材料更注重剪切强度而非可重复定位性。像Lohmann这样的供应商目前提供导热性能优异的丙烯酸-硅酮混合材料,其散热性能可达2 W/mK,适用于电动车电池组。

树脂产品组合的多元化满足了特定终端应用的需求,同时又不影响丙烯酸树脂的市场份额。橡胶升级的重点是能够承受引擎室125°C高温的合成橡胶,填补了丙烯酸树脂长期以来的空白。硅酮树脂的研发重点是符合欧洲医疗法规的低环硅氧烷等级,而环氧树脂胶带则添加了常温固化潜伏催化剂,以增强其在航太复合材料修復方面的应用。这些创新使树脂化学成分与不断变化的性能需求相匹配,并保持了市场竞争力。

2024年,水性体系将占销售额的45.19%,反映出该产业对低VOC(挥发性有机化合物)加工的重视。自1990年以来,3M等製造商通过去除溶剂载体,已将VOC含量降低了99%。随着加工商改进涂布机以处理与溶剂型剪切机相当的高固态丙烯酸乳液,该行业将以4.47%的复合年增长率成长。溶剂型生产线由于其在低表面能基板上优异的润湿性能,仍然主导着高温电子产业,但它们面临资本投资监管收紧的挑战。热熔压敏胶在电子商务包装领域市场份额不断增长,其瞬时黏合速度可最大限度地提高生产效率。反应性化学品,包括可与环境水分交联的聚氨酯泡棉,正在汽车结构连接领域找到新的应用。

双系统涂布机现已具备水溶性混合涂布能力,可快速换型并节省能源。创新也延伸至源自萜烯和淀粉的生物基分散体,使水性黏合剂能够应用于下一代循环经济领域。随着加工商将环保目标与高性能需求相结合,这种技术的多元化将扩大胶带市场。

区域分析

到2024年,亚太地区将占全球产量的58.91%,年复合成长率达5.01%,主要得益于中国、印度和东南亚地区电子、汽车和建筑业的快速发展。该地区的製造商正在增加本地化的涂布和切断机能力,以缩短前置作业时间并提供符合当地需求的客製化产品。中国和印度政府对半导体工厂的激励措施正在推动对超级净切割胶带和遮罩胶带的需求。同时,位于清奈和苏州的太阳能胶合剂工厂正在加强永续性力度,增强胶带市场的供应韧性。

北美凭藉着在医疗保健和航太领域的先进研发实力,保持其技术领先地位。 3M的无溶剂平台和艾利丹尼森的UL-94认证电动车电池胶带,体现了创新主导的向特种应用领域的转变。劳动市场紧张刺激了自动化投资,有利于采用模切压敏胶零件以加快组装。 《美国墨加协定》也支持汽车线束胶带生产的近岸外包,并有助于缓解外汇波动的影响。

欧洲对生态设计和VOC合规性的重视正在加速水性压敏胶的普及。汽车轻量化和电气化政策推动了对高性能黏合胶带的需求,以取代铆钉和焊接。同时,中东和非洲市场正在大型基础建设计划中采用耐高温外墙胶带。受巴西农产品包装产业和区域性软质包装工厂的推动,南美胶带市场正经历稳定扩张。新兴市场的扩张和已开发地区产业回流的共同作用将支撑全球成长前景。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 来自电子商务和包装行业的需求不断增长

- 原始设备製造商开始使用轻量化线束胶带

- 在穿戴医疗设备中采用低创伤硅胶带

- 东协和中东地区的建筑热潮推动了胶带使用量的成长。

- 电子业对胶带的需求不断增长

- 市场限制

- 原物料价格波动

- 极端条件下产品性能的局限性

- 对挥发性有机化合物排放的担忧

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章 市场规模与成长预测

- 树脂

- 丙烯酸纤维

- 橡胶底座

- 硅酮

- 环氧树脂

- 聚氨酯

- 透过技术

- 水溶液

- 溶剂型

- 热熔胶

- 反应型

- 依产品类型

- 感压胶带

- 水活化胶带

- 导热胶带

- 特殊胶带

- 按最终用途行业划分

- 包裹

- 车

- 电机与电子工程

- 卫生保健

- 消费者/DIY

- 其他(建筑、施工等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- Avery Dennison Corporation

- Berry Global Inc.

- CCT(Coating & Converting Technologies, LLC)

- DuPont

- HB Fuller Company

- Henkel AG & Co. KGaA

- IPG

- LINTEC Corporation

- Lohmann

- Mativ

- Nitto Denko Corporation

- Oji Holdings Corporation

- Scapa Group Ltd

- Sekisui Chemical Co., Ltd.

- Shurtape Technologies, LLC

- Sika AG

- tesa SE-A Beiersdorf Company

第七章 市场机会与未来展望

The Adhesive Tapes Market size is estimated at 58.57 billion square meters in 2025, and is expected to reach 71.67 billion square meters by 2030, at a CAGR of 4.12% during the forecast period (2025-2030).

Consistent demand from packaging, electronics, and automotive manufacturing is offsetting raw-material cost swings and stricter limits on volatile organic compound (VOC) emissions. Water-based technologies are scaling quickly as converters pivot toward low-VOC chemistries, while pressure-sensitive formats retain volume leadership because they bond instantly and suit automated application lines. Asia-Pacific leads consumption and growth, propelled by a dense electronics supply chain and large-scale infrastructure spending. Healthcare is emerging as the fastest-growing outlet as skin-friendly silicone adhesives enable longer-wear medical devices and shift value toward high-margin specialty grades. Major producers are countering cost pressures through vertical integration, regional capacity additions, and portfolio realignment toward sustainable solutions.

Global Adhesive Tapes Market Trends and Insights

Rising Demand from E-Commerce and the Packaging Industry

Digital retail continues to push logistics operators toward faster, safer, and more sustainable packaging. Brand owners now specify fiber-based tear tapes and solvent-free box-closing systems that meet recyclability targets while surviving long distribution cycles. H.B. Fuller's Earthic portfolio exemplifies this shift, delivering certified bio-based content without sacrificing shear strength. Demand for right-sized cartons is also accelerating the customization of carton-sealing tapes that adhere to diverse corrugate grades in automated lines. Growth is most pronounced in Asia-Pacific, where cross-border parcel volumes are rising and fulfillment centers standardize on water-activated tapes to cut plastic use. These forces collectively lift the adhesive tapes market by improving the average price per square meter for high-performance packaging grades.

OEM Shift to Lightweight Wire-Harness Tapes

Automakers are replacing bulky PVC tubing with specialty cloth and PET adhesive tapes that save up to 50% harness weight while absorbing vibration and withstanding 150 °C engine-bay temperatures. tesa SuperSleeve 51026 PV6 typifies next-generation wraps that combine PET cloth with a solvent-free acrylic adhesive to resist abrasion in high-heat zones. Electric-vehicle platforms amplify the opportunity because harnesses run longer and must remain flexible for battery-pack servicing. Lighter harness assemblies help extend driving range, reinforcing OEM adoption curves. These trends feed directly into the adhesive tapes market as converters qualify tailored widths and die-cuts for automated loom wrapping.

Volatility in Prices of Raw Materials

Feedstocks such as tackifier resins and specialty carbons swing with crude oil and freight costs, compressing converter margins. Cabot announced carbon-black price increases effective December 2024, citing inflationary pressures. Producers mitigate spikes through multi-supplier sourcing and indexed contracts, but still face working-capital strain that can stall smaller converters' expansion plans, placing a near-term drag on the adhesive tapes market.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Low-Trauma Silicone Tapes for Wearable Medical Devices

- Construction Boom in ASEAN and Middle East Region

- Limitations in Product Performance Under Extreme Conditions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic formulations secured 41.12% of 2024 volume, making them the largest contributor to adhesive tapes market size because they bond metals, plastics, and glass without extensive surface treatment. Their excellent UV resistance and aging stability drive uptake in outdoor electronics and solar assemblies. Rubber systems, despite lower durability, are scaling at 4.24% CAGR as automakers favor their high initial tack for wire-loom bundling and interior NVH control. Silicone PSAs, though niche in volume, command premium pricing in medical wearables and high-heat electronics thanks to biocompatibility and 200 °C service temperatures. Epoxy and polyurethane chemistries cater to structural bonding niches where shear strength outweighs repositionability. Suppliers such as Lohmann now offer thermally conductive acrylic-silicone hybrids that dissipate 2 W/mK in electric-vehicle battery packs.

Diversification within resin portfolios supports specialized end-use needs without cannibalizing acrylic share. Rubber upgrades focus on synthetic variants that withstand 125 °C engine-bay peaks, closing the historical gap with acrylics. Silicone development centers on low-cyclic-siloxane grades to satisfy European medical regulations, while epoxy tapes add latent catalysts for room-temperature cure, expanding repair capabilities in aerospace composites. These innovations collectively keep the adhesive tapes market competitive as formulators match resin chemistries to evolving functional demands.

Water-based systems represented 45.19% of 2024 sales, reflecting the sector's pivot to low-VOC processing. Producers such as 3M have slashed VOCs by 99% since 1990 by phasing out solvent carriers. The segment grows at 4.47% CAGR as converters retrofit coaters to handle high-solids acrylic emulsions that rival solvent-borne shear. Solvent-based lines still dominate high-temperature electronics because of superior wet-out on low-surface-energy substrates, but they face tightening regulatory capex. Hot-melt PSAs gain share in e-commerce packaging, where instant bond speeds maximize throughput. Reactive chemistries, including polyurethane foams that crosslink with ambient moisture, secure niche adoption in structural automotive joints.

Twin-system coaters now deliver hybrid water/solvent capability, allowing rapid changeovers and energy savings. Innovation extends to bio-based dispersions from terpene or starch feedstocks, positioning water-based adhesives for next-generation circular-economy metrics. This technology heterogeneity broadens the adhesive tapes market as converters align environmental targets with high-performance demands.

The Adhesive Tapes Market Report Segments the Industry by Resin (Acrylic, Rubber-Based, and More), Technology (Water-Based, Solvent-Based, and More), Product Type (Pressure-Sensitive Tapes, Water-Activated Tapes, and More), End-User Industry (Packaging, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific held 58.91% of the 2024 volume and is set to grow at a 5.01% CAGR as China, India, and Southeast Asia expand electronics, automotive, and construction output. Regional producers add local coating and slitting capacity, reducing lead times and tailoring SKUs to domestic requirements. Government incentives for semiconductor fabs in China and India amplify demand for ultra-clean dicing and masking tapes. Concurrently, solar-powered adhesive plants in Chennai and Suzhou demonstrate growing sustainability commitments, reinforcing supply resilience in the adhesive tapes market.

North America retains technology leadership, leveraging advanced R&D in healthcare and aerospace. 3M's solvent-free platforms and Avery Dennison's UL-94-rated EV battery tapes illustrate an innovation-driven shift toward specialized applications. Tight labor markets stimulate automation investments, favoring die-cut PSA components that accelerate assembly. The United States-Mexico-Canada Agreement also supports near-shoring of automotive harness tape production, buffering currency volatility.

Europe emphasizes eco-design and VOC compliance, accelerating water-based PSA adoption. Automotive lightweighting and electrification policies sustain demand for high-performance bonding tapes that replace rivets and welds. Meanwhile, Middle East and Africa markets benefit from infrastructure megaprojects that specify high-temperature exterior facade tapes. South America's adhesive tapes market gains incrementally through Brazil's agriculture-linked packaging sector and localized flexible-packaging plants. The combined effect of emerging-market expansion and industrial re-shoring in developed regions sustains the global growth outlook.

- 3M

- Avery Dennison Corporation

- Berry Global Inc.

- CCT (Coating & Converting Technologies, LLC)

- DuPont

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- IPG

- LINTEC Corporation

- Lohmann

- Mativ

- Nitto Denko Corporation

- Oji Holdings Corporation

- Scapa Group Ltd

- Sekisui Chemical Co., Ltd.

- Shurtape Technologies, LLC

- Sika AG

- tesa SE - A Beiersdorf Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from the E-Commerce and Packaging Industry

- 4.2.2 OEM shift to lightweight wire-harness tapes

- 4.2.3 Adoption of low-trauma silicone tapes for wearable medical devices

- 4.2.4 Construction boom in ASEAN and Middle-East region boosting adhesive tape usage

- 4.2.5 Growing Demand for Adhesive Tapes from Electronics Industry

- 4.3 Market Restraints

- 4.3.1 Volatility in Prices of Raw Materials

- 4.3.2 Limitations in Product Performance Under Extreme Conditions

- 4.3.3 Concerns of VOC Emissions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Rubber-based

- 5.1.3 Silicone

- 5.1.4 Epoxy

- 5.1.5 Polyurethane

- 5.2 By Technology

- 5.2.1 Water-based

- 5.2.2 Solvent-based

- 5.2.3 Hot-melt

- 5.2.4 Reactive

- 5.3 By Product Type

- 5.3.1 Pressure-Sensitive Tapes

- 5.3.2 Water-Activated Tapes

- 5.3.3 Heat-Sensitive Tapes

- 5.3.4 Specialty Tapes

- 5.4 By End-use Industry

- 5.4.1 Packaging

- 5.4.2 Automotive

- 5.4.3 Electrical and Electronics

- 5.4.4 Healthcare

- 5.4.5 Consumer/DIY

- 5.4.6 Others (Building and Construction, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Avery Dennison Corporation

- 6.4.3 Berry Global Inc.

- 6.4.4 CCT (Coating & Converting Technologies, LLC)

- 6.4.5 DuPont

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 IPG

- 6.4.9 LINTEC Corporation

- 6.4.10 Lohmann

- 6.4.11 Mativ

- 6.4.12 Nitto Denko Corporation

- 6.4.13 Oji Holdings Corporation

- 6.4.14 Scapa Group Ltd

- 6.4.15 Sekisui Chemical Co., Ltd.

- 6.4.16 Shurtape Technologies, LLC

- 6.4.17 Sika AG

- 6.4.18 tesa SE - A Beiersdorf Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

胶带市场规模、份额、趋势和预测:按材料、树脂、技术、应用和地区划分,2026-2034年

胶带市场规模、份额、趋势和预测:按材料、树脂、技术、应用和地区划分,2026-2034年 胶带市场分析及预测(至2035年):类型、产品类型、应用、材料类型、技术、最终用户、形态、组件、功能、工艺日本胶带市场规模、份额、趋势及预测(依材料、树脂、技术、应用及地区划分),2026-2034年

胶带市场分析及预测(至2035年):类型、产品类型、应用、材料类型、技术、最终用户、形态、组件、功能、工艺日本胶带市场规模、份额、趋势及预测(依材料、树脂、技术、应用及地区划分),2026-2034年 2026年全球胶带市场报告

2026年全球胶带市场报告 胶带市场规模、份额和趋势分析报告:按树脂类型、最终用途、地区和细分市场预测(2026-2033 年)

胶带市场规模、份额和趋势分析报告:按树脂类型、最终用途、地区和细分市场预测(2026-2033 年) 电动汽车电池胶带市场按胶带类型、黏合剂类型、电池化学成分、基材、应用和最终用途划分-2026-2032年全球预测

电动汽车电池胶带市场按胶带类型、黏合剂类型、电池化学成分、基材、应用和最终用途划分-2026-2032年全球预测 胶带市场规模、份额和成长分析(按类型、黏合技术、树脂、材料、终端用途产业和地区划分)—产业预测(2026-2033 年)

胶带市场规模、份额和成长分析(按类型、黏合技术、树脂、材料、终端用途产业和地区划分)—产业预测(2026-2033 年) 全球胶带市场研究报告 - 产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球胶带市场研究报告 - 产业分析、规模、份额、成长、趋势及2025年至2033年预测 全球胶带市场(按树脂类型、技术、内衬、类别、最终用途行业、黏合剂类型、黏合类型、厚度和地区划分)- 预测至2030年

全球胶带市场(按树脂类型、技术、内衬、类别、最终用途行业、黏合剂类型、黏合类型、厚度和地区划分)- 预测至2030年 车身胶带市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

车身胶带市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测