|

市场调查报告书

商品编码

1851025

EHS软体:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030年)EHS Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

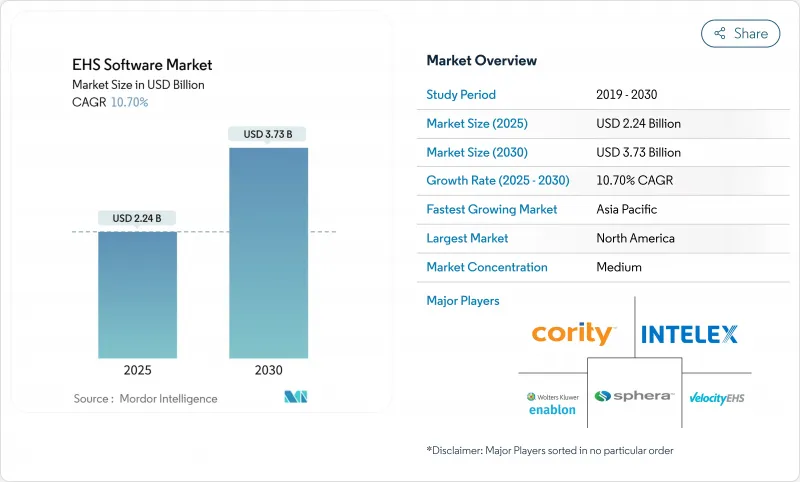

环境健康与安全 (EHS) 软体市场预计将从 2025 年的 22.4 亿美元成长到 2030 年的 37.3 亿美元,复合年增长率为 10.7%。

监管力度的持续收紧、ESG规范的快速规范化以及向人工智慧驱动的安全分析的转变,都推动了这一成长。欧洲企业永续发展报告指令(CSRD)实施的延迟,也促使企业对自动化合规工作流程的需求增加。在营运层面,企业倾向采用SaaS架构以降低整体拥有成本。云端部署已占活跃部署的62%,其中服务占60%,显示部署专业知识对于SaaS的普及仍然至关重要。大型企业正在利用各种平台来应对跨境风险,而中小企业则以最快的速度进行迁移,因为订阅模式消除了前期投资的障碍。

全球EHS软体市场趋势与洞察

更严格的监管和更高的问责制

欧盟的企业社会责任数据(CSRD)显着扩大了资讯揭露的范围和频率,迫使跨国公司实现跨司法管辖区报告工作流程的自动化。同时,美国也出现了类似的倡议,例如纽约州强制要求报告温室气体排放,这导致企业因违规承担的责任日益加重。因此,企业纷纷转向环境、健康与安全(EHS)软体市场寻求解决方案,以作为先发制人的法律保障。日本的网路安全战略要求建立软体材料清单)以保护供应链,从而推动了对整合风险平台的需求。由此产生的结构化资料量空前庞大,已远远超出人工处理能力。

扩大ESG和永续性报告要求

强制性ESG资讯揭露已从投资者的期望发展成为法律义务。欧盟的碳边境调节机制要求进口商追踪隐含排放,并强制全球供应商将环境资料收集制度化。英国仅有19%的中小企业具备ESG意识,随着新的处罚措施生效,在閒置频段推广应用的潜力日益凸显。肯亚的绿色金融分类法鼓励贷款机构投资气候友善计划,并建立了一套资讯揭露框架。因此,业内相关人员将环境健康与安全软体市场视为一种扩充性的途径,可以将符合审核要求的ESG分析融入日常运营,从而实现合规。

高昂的初始实施和变更管理成本

义大利小型製造商认为,采购价格、系统迁移的复杂性以及员工培训是阻碍他们采用数位安全技术的主要因素。 40%的中小企业收集环境数据,但只有18%将其整合到绩效指标中。儘管供应商正在提供打包的入门服务和模板化配置来应对这项挑战,但预算限制仍会减缓转换速度,并限制EHS软体市场近期的成长。

细分市场分析

到2024年,服务将占EHS软体市场份额的60%。法规解读、资料迁移和使用者培训决定着计划的成败。 ERA Environmental定义的实施生命週期(评估、同步部署和检验)阐明了咨询人才的重要性。在预测期内,随着人工智慧和ESG模组的出现,EHS软体的复杂性日益增加,许多公司选择将这些复杂性外包,因此与服务相关的EHS软体市场规模将稳定成长。

随着企业向云端原生套件和行动扩展转型,软体收入将以 10.7% 的复合年增长率成长。供应商正在整合可配置的 ESG 模板和基于人工智慧的风险引擎,以缩短设定时间并提高采用率。因此,长期利润率的提升将有利于平台授权商,而短期规模的扩大则取决于服务合作伙伴能否加速企业部署。

至2024年,云端解决方案将占EHS软体市场规模的62%。集中式资料管理、弹性储存和即时修补程式等优势,足以抵消长期以来的安全隐患。日本企业正迈入数位转型的第三阶段:数据分析,凸显了云端基础设施如何协助提升效率。

在延迟、主权或客製化工作流程需要本地控制的情况下,本地部署仍然存在,但其成长速度比云端运算慢了6个百分点。按行业划分,供应商正逐步放弃原生桌面版本,鼓励高度监管的产业采用混合策略。随着跨国公司对其伺服器设施进行精简,EHS软体市场将更加倾向于基于使用量的定价模式,以使成本与规模相符。

EHS软体市场按部署类型(云端、本地部署)、元件(软体、服务)、最终用户产业(石油天然气、能源公共产业、其他)、解决方案类型(事故与安全管理、审核与检查、其他)、组织规模(大型企业、其他)和地区进行细分。市场预测以美元计价。

区域分析

到2024年,北美将维持37.5%的EHS(环境、健康与安全)软体市场份额,这得益于成熟的OSHA合规文化以及各州交通机构对人工智慧的早期应用。像加州大学圣地牙哥分校医疗中心这样的医疗网路正在投资2,200万美元用于人工智慧以改善病患治疗效果,这表明各级经营团队对数位安全工具的广泛承诺。联邦政府关于网路安全卫生的指南将进一步加速人们对云端平台的信任。

亚太地区是成长引擎,预计到2030年将以10.1%的复合年增长率成长。日本的「数位社会优先计画」以及每季1.54兆日圆(约107亿美元)的软体投资,便是公私合作提升生产力的典范。从越南到印度,各区域监管机构正在协调化学品和气候框架,从而扩大了环境、健康与安全(EHS)软体市场的潜在用户群。

随着共同体可持续发展指令(CSRD)最后期限的临近,欧洲经济正经历谨慎成长。各公司正积极调动审核团队,将永续性指标纳入财务报表,进而持续推升对彙报模组的需求。欧盟的碳边境调节机制将间接促进贸易伙伴采用相关指标,扩大环境、健康与安全(EHS)软体产业的使用者基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 更严格的监管和更高的问责制

- 扩大环境、社会及公司治理(ESG)及永续性报告义务

- 以SaaS和行动装置优先的EHS平台可降低整体拥有成本

- 人工智慧驱动的预测分析助力安全与合规

- 与数位双胞胎/资产管理堆迭集成

- 市场限制

- 高昂的初始实施和变更管理成本

- 云端部署中的网路安全和资料隐私问题

- 下一代EHS工具面临资料科学人才短缺问题。

- 供应商整合带来的整合锁定风险

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特的五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按组件

- 软体

- 服务

- 透过部署模式

- 云

- 本地部署

- 按解决方案类型

- 事故与安全管理

- 审核和检查

- 合规与风险管理

- ESG/碳管理

- 培训与学习

- 按组织规模

- 大公司

- 中小企业

- 按最终用户行业划分

- 能源与公共产业

- 石油和天然气

- 化工/石油化工

- 医疗保健与生命科学

- 建筑/製造

- 采矿和金属

- 饮食

- 其他行业

- 按地区

- 北美洲

- 美国

- 加拿大

- 南美洲

- 巴西

- 其他南美洲

- 欧洲

- 德国

- 法国

- 英国

- 俄罗斯

- 其他欧洲地区

- 亚洲

- 中国

- 印度

- 日本

- 韩国

- 其他亚洲地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Enablon(Wolters Kluwer NV)

- Intelex Technologies ULC

- VelocityEHS Holdings Inc.

- Cority Software Inc.

- Sphera Solutions Inc.

- Sai Global Pty Ltd(Intertek Group PLC)

- Dakota Software Corporation

- Benchmark Digital Partners LLC

- ProcessMAP Corporation

- Quentic GmbH

- IsoMetrix

- SAP SE

- iPoint-Systems GmbH

- Evotix(SHE Software)

- DNV Business Assurance

- EcoOnline

- ETQ, part of Hexagon

- Origami Risk LLC

- Alcumus Group

- Ideagen PLC

- Vector Solutions

- KPA

- EHS Insight

- Quber Tech

第七章 市场机会与未来展望

The environmental health safety software market is valued at USD 2.24 billion in 2025 and is forecast to reach USD 3.73 billion by 2030, advancing at a 10.7% CAGR.

Persistent regulatory tightening, rapid ESG formalization and the shift toward AI-enabled safety analytics collectively anchor this expansion. European delays in the Corporate Sustainability Reporting Directive (CSRD) are generating pent-up demand for automated compliance workflows, while New York's mandatory greenhouse-gas disclosures preview similar obligations in other jurisdictions. At an operational level, enterprises favor software-as-a-service architectures to reduce total cost of ownership; cloud deployments already account for 62% of active installations, and services commanding 60% illustrate that implementation expertise remains critical for adoption.Large enterprises leverage platform breadth to address cross-border risk, yet small and mid-sized firms are the fastest movers because subscription pricing removes upfront capital barriers.

Global EHS Software Market Trends and Insights

Stringent regulatory enforcement & rising liability exposure

The European Union's CSRD markedly widens disclosure scope and frequency, compelling multinationals to automate multi-jurisdictional reporting workflows. Parallel action in the United States-such as New York's greenhouse-gas reporting requirement-signals rising liability for non-compliance. Businesses therefore treat environmental health safety software market solutions as a pre-emptive legal safeguard. Asian regulators are converging; Japan's cybersecurity strategy now requires Software Bills of Materials to protect supply chains, elevating demand for integrated risk platforms . The cumulative result is an unprecedented volume of structured data that exceeds manual processing capacity, turning automation into necessity rather than choice.

Expansion of ESG & sustainability reporting mandates

Mandatory ESG disclosures have expanded from investor-led expectations to statutory obligations. The EU's Carbon Border Adjustment Mechanism forces importers to track embedded emissions, compelling global suppliers to institutionalize environmental data capture. Only 19% of UK SMEs have any ESG awareness, revealing white-space adoption potential as new penalties take hold. Emerging economies are aligning; Kenya's Green Finance Taxonomy now directs lenders toward climate-aligned projects, institutionalizing disclosure frameworks. Industry practitioners therefore view the environmental health safety software market as a scalable route to compliance, embedding audit-ready ESG analytics into day-to-day operations.

High upfront implementation & change-management cost

Small manufacturers in Italy cite purchase price, system migration complexity and workforce training as principal inhibitors to digital safety adoption. Similar feedback is recorded across, economies, where 40% of SMEs collect environmental data but only 18% integrate it into performance metrics . Vendors respond with packaged onboarding services and templated configurations, yet budget constraints still delay conversions and trim near-term growth in the environmental health safety software market.

Other drivers and restraints analyzed in the detailed report include:

- SaaS-first, mobile-first EHS platforms reduce TCO

- AI-driven predictive safety & compliance analytics

- Cyber-security & data-privacy concerns in cloud roll-outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services held 60% of environmental health safety software market share in 2024 . Organizations acknowledge that platform acquisition addresses only a fraction of compliance complexity; regulatory interpretation, data migration and user training determine project success. The implementation lifecycle set out by ERA Environmental-assessment, tandem deployment and validation-illustrates why consultancy talent remains integral. Over the forecast period, the environmental health safety software market size linked to Services will expand steadily as AI and ESG modules add intricacy that many firms outsource.

Software revenue grows at an aligned 10.7% CAGR as buyers progress toward cloud-native suites and mobile extensions. Vendors embed configurable ESG templates and AI-based risk engines, compressing setup time and increasing stickiness. Consequently, long-term margin expansion favors platform licensors, yet near-term scale depends on service partners to accelerate enterprise roll-outs.

Cloud solutions commanded 62% of environmental health safety software market size in 2024. Centralized data management, elastic storage and instant patching outweigh long-standing security concerns. Japanese corporates have progressed to the third stage of digital transformation-data analytics underscoring how cloud infrastructure underpins efficiency gains .

On-premise installations persist where latency, sovereignty or bespoke workflows require localized control, but growth lags cloud by six percentage points. Vendors increasingly sunset native desktop editions, encouraging hybrid strategies in heavily regulated verticals. As multinationals rationalize server estates, the environmental health safety software market tilts further toward usage-based pricing that aligns cost with scale.

EHS Software Market is Segmented by Deployment Mode (Cloud, On-Premise), by Component (Software, Services) by End-User Vertical (Oil and Gas, Energy and Utilities, and More), by Solution Type (Incident and Safety Management, Audit and Inspection and More), by Organization Size (Large Enterprises and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 37.5% of environmental health safety software market size in 2024, underpinned by mature OSHA compliance culture and early AI adoption by state transportation agencies. Healthcare networks such as UC San Diego Health invest USD 22 million in AI to elevate patient outcomes, demonstrating broad management commitment to digital safety tools . Federal guidance on cyber hygiene further accelerates trust in cloud platforms

Asia-Pacific is the growth engine, poised for 10.1% CAGR through 2030. Japan's Digital Society priority program and JPY 1.54 trillion (USD 10.7 billion) quarterly software investments exemplify government-private collaboration on productivity gains. Regional regulators-from Vietnam to India-are rolling out harmonized chemical and climate frameworks, expanding the environmental health safety software market addressable base.

Europe shows measured growth as CSRD deadlines loom. Corporates mobilize audit teams to integrate sustainability metrics with financial statements, creating recurring demand for reporting modules . The EU Carbon Border Adjustment Mechanism indirectly pulls adoption in trading partners, broadening the environmental health safety software industry footprint.

- Enablon (Wolters Kluwer NV)

- Intelex Technologies ULC

- VelocityEHS Holdings Inc.

- Cority Software Inc.

- Sphera Solutions Inc.

- Sai Global Pty Ltd (Intertek Group PLC)

- Dakota Software Corporation

- Benchmark Digital Partners LLC

- ProcessMAP Corporation

- Quentic GmbH

- IsoMetrix

- SAP SE

- iPoint-Systems GmbH

- Evotix (SHE Software)

- DNV Business Assurance

- EcoOnline

- ETQ, part of Hexagon

- Origami Risk LLC

- Alcumus Group

- Ideagen PLC

- Vector Solutions

- KPA

- EHS Insight

- Quber Tech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent regulatory enforcement & rising liability exposure

- 4.2.2 Expansion of ESG & sustainability reporting mandates

- 4.2.3 SaaS-first, mobile-first EHS platforms reduce TCO

- 4.2.4 AI-driven predictive safety & compliance analytics

- 4.2.5 Convergence with digital-twin/asset-management stacks

- 4.3 Market Restraints

- 4.3.1 High upfront implementation & change-management cost

- 4.3.2 Cyber-security & data-privacy concerns in cloud roll-outs

- 4.3.3 Shortage of data-science talent for next-gen EHS tools

- 4.3.4 Vendor consolidation creating integration lock-in risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Solution Type

- 5.3.1 Incident & Safety Management

- 5.3.2 Audit & Inspection

- 5.3.3 Compliance & Risk Management

- 5.3.4 ESG / Carbon Management

- 5.3.5 Training & Learning

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small & Mid-Sized Enterprises (SME)

- 5.5 By End-user Industry

- 5.5.1 Energy & Utilities

- 5.5.2 Oil & Gas

- 5.5.3 Chemicals & Petro-chemicals

- 5.5.4 Healthcare & Life Sciences

- 5.5.5 Construction & Manufacturing

- 5.5.6 Mining & Metals

- 5.5.7 Food & Beverages

- 5.5.8 Other Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia

- 5.6.5 Middle East & Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Enablon (Wolters Kluwer NV)

- 6.4.2 Intelex Technologies ULC

- 6.4.3 VelocityEHS Holdings Inc.

- 6.4.4 Cority Software Inc.

- 6.4.5 Sphera Solutions Inc.

- 6.4.6 Sai Global Pty Ltd (Intertek Group PLC)

- 6.4.7 Dakota Software Corporation

- 6.4.8 Benchmark Digital Partners LLC

- 6.4.9 ProcessMAP Corporation

- 6.4.10 Quentic GmbH

- 6.4.11 IsoMetrix

- 6.4.12 SAP SE

- 6.4.13 iPoint-Systems GmbH

- 6.4.14 Evotix (SHE Software)

- 6.4.15 DNV Business Assurance

- 6.4.16 EcoOnline

- 6.4.17 ETQ, part of Hexagon

- 6.4.18 Origami Risk LLC

- 6.4.19 Alcumus Group

- 6.4.20 Ideagen PLC

- 6.4.21 Vector Solutions

- 6.4.22 KPA

- 6.4.23 EHS Insight

- 6.4.24 Quber Tech

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space & Unmet-Need Assessment

2026年全球环境、健康与安全市场报告2026年全球环境健康与安全(EHS)软体市场报告

2026年全球环境、健康与安全市场报告2026年全球环境健康与安全(EHS)软体市场报告 环境、健康与安全 (EHS) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分

环境、健康与安全 (EHS) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分 职业安全与健康(OHS)全球市场规模、份额、趋势和成长分析报告(2026-2034)

职业安全与健康(OHS)全球市场规模、份额、趋势和成长分析报告(2026-2034) 全球环境、健康与安全(EHS)市场:依组件、部署方式、企业规模、应用和行业划分 - 市场规模、行业动态、机会分析和预测(2026–2035)

全球环境、健康与安全(EHS)市场:依组件、部署方式、企业规模、应用和行业划分 - 市场规模、行业动态、机会分析和预测(2026–2035) 职业健康市场规模、份额和成长分析(按类型、地点、应用、组织规模和地区划分)—产业预测(2026-2033 年)

职业健康市场规模、份额和成长分析(按类型、地点、应用、组织规模和地区划分)—产业预测(2026-2033 年) 环境、健康与安全市场:2025-2032年全球预测(按最终用户产业、解决方案类型、应用、部署类型和组织规模划分)2025年全球职业健康市场报告2025年职业治疗全球市场报告

环境、健康与安全市场:2025-2032年全球预测(按最终用户产业、解决方案类型、应用、部署类型和组织规模划分)2025年全球职业健康市场报告2025年职业治疗全球市场报告 全球职业健康与安全(OHS)市场

全球职业健康与安全(OHS)市场