|

市场调查报告书

商品编码

1851061

资料保护即服务 (DPaaS):市场占有率分析、产业趋势、统计资料和成长预测 (2025-2030)Data Protection As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

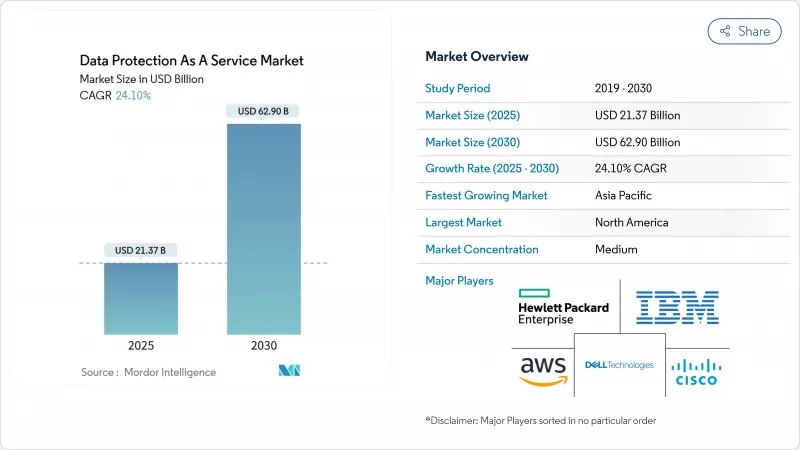

预计到 2025 年,资料保护即服务 (DPaaS) 市场规模将达到 213.7 亿美元,到 2030 年将达到 629 亿美元,预测期(2025-2030 年)的复合年增长率为 24.10%。

非结构化资料的爆炸性成长、零信任安全策略的强制推行以及企业董事会对勒索软体风险日益增长的担忧,共同推动了云端服务市场的发展。企业正迅速用基于使用量的云端订阅服务取代资本密集的本地备份硬件,这些服务提供弹性扩充性。自主云端投资、量子安全加密测试和网路保险需求正在融合重塑产品蓝图,而供应商整合则压缩了市场结构并加速了功能整合。

全球资料保护即服务 (DPaaS) 市场趋势与洞察

严格的资料主权法规再形成全球保护

从巴西到印度,类似GDPR的框架正在逐步推广,迫使企业将资料储存在地化、采用精确的资料映射,并建立基于策略的控制措施来管理跨境资料流。欧盟的《数位营运弹性法案》已于2025年1月生效,要求金融机构提供近乎即时的事件报告。在美国,新规限制了敏感资料传输给外国对手,这增加了跨国公司的复杂性。因此,采购团队在选择资料保护即服务(DPaaS)供应商时,越来越重视主权控制以及復原点目标(RPO)/復原时间目标(RTO)指标。为了满足国家监管机构和内部风险委员会的要求,供应商正在提供区域特定的金钥管理、双重加密选项和区域内復原库等解决方案。

边缘运算革新防护架构

边缘部署将处理能力转移到更靠近感测器端点和分店,使工作负载无需将流量路由到集中式资料中心即可满足延迟目标。到 2025 年底,40% 的大型企业计划在边缘运行关键业务应用程式。这种转变需要轻量级、策略驱动的本机运行备份代理,并且能够非同步同步。此外,一些新产品也开始将基于人工智慧的异常检测整合到边缘网关中,以缩短勒索软体入侵时的停留时间。医疗保健系统正在医院内试点这些功能,以遵守严格的患者资料本地化规则,同时为临床医生提供即时存取权限。

隐藏的云端成本会削弱多重云端策略

流量费用波动和按 API 呼叫计费会对预算造成压力,尤其对于需要频繁恢復的分析密集或监管查询而言更是如此。在规模较小的云端区域中,议价能力有限的企业受到的影响最大。儘管财务营运团队已投入资金开发成本监控仪表板,但储存层级间分散的计费方式以及冷热迁移仍然是预算的一大挑战。

细分市场分析

到2030年,灾害復原服务)细分市场的复合年增长率将达到29.5%,超过其他服务,因为企业领导层已将勒索软体回应提升为策略指标。超过70%的企业计划在容错移转。虽然储存即服务(STaaS)在2024年将占据资料保护即服务(DPaaS)市场份额的43.2%,但它正朝着智慧分层和基于策略的不可变性方向发展,并与零信任架构保持一致。融合平台现在将备份即服务(BaaS)、储存即服务(STaaS)和灾难復原即服务(DRaaS)捆绑在一个统一的策略引擎下,从而简化了采购和管治。

儘管人们对灾难復原即服务 (DRaaS) 的热情日益高涨,但储存订阅市场依然强劲。物件储存的成长势头强劲,这主要得益于人工智慧模型训练集和视讯分析的兴起,它们导致非结构化资料量激增。为了应对这项挑战,服务供应商正在大力推广Petabyte级资料去重和压缩技术。云端超大规模云端服务供应商的全端产品现在整合了自主威胁扫描功能,这意味着勒索软体只会攻击受影响的资料区块,而不是整个资料磁碟区。这种功能的整合预示着未来将朝着以平台为中心的采购模式发展,在这种模式下,恢復自动化、资料分类和合规性映射等功能都将整合在一个统一的控制平面中。

混合模式成长最快,复合年增长率高达 31.5%。监管机构倾向于采用能够在受监管的公共领域进行突发性分析,同时将敏感资料集保留在本地私有私有云端中的架构。这种模式在欧洲银行中尤其明显,这些银行受数位营运弹性法律的约束,这些法律要求为第三方服务制定书面应急安排。策略自动化会根据资料分类标籤选择储存目标,从而优化延迟和合规性。随着企业使用云端连线的资料储存库对其传统磁带归檔进行现代化改造,预计到 2028 年,混合解决方案的资料保护即服务 (DPaaS) 市场规模将翻倍。

私有云端私有云端部署维持了 43.7% 的市场份额,尤其受到国防、公共产业和医疗保健机构的青睐,因为这些机构必须对加密金钥拥有控制权。提供私有云端设备的供应商正越来越多地整合 FIPS 认证的硬体安全模组 (HSM)、基于角色的存取控制和空气间隙的组态管理。对于那些重视区域多样性而非完全主权的数位原民企业而言,公共云端方案仍然很受欢迎。然而,像 AWS 欧洲主权云端这样的主权云端倡议正在模糊两者之间的界限,在本地法律控制下提供公有云的敏捷性,并将受监管的工作负载引入到以前无法进入的环境中。

资料保护即服务 (DPaaS) 市场按服务类型(储存即服务、备份即服务、灾难復原即服务)、部署模式(公共云端、私有云端、混合混合云端)、组织规模(大型企业、中小企业)、最终用户业(银行、金融服务和保险、医疗保健、生命科学等)以及地区进行细分。市场预测以美元计价。

区域分析

北美地区维持了37.8%的收入份额,这得益于云端运算的强劲普及以及联邦政府的强制性规定,例如CISA约束性操作指令25-01,该指令要求各机构对SaaS应用安全配置基准。 《保护美国资料免受外国敌对势力侵害法案》限制了敏感个人资料的跨境传输,从而刺激了对国内资料保险库和金钥託管服务的需求。企业优先考虑能够为审核产生自动化认证报告的合规性对应功能。

亚太地区正以31.4%的复合年增长率实现最快成长,这主要得益于日本、印度和韩国的数位化政府专案推动了数据在地化规则的出台。印度的《数位个人资料保护法》明确规定了敏感个人资讯的在地化,并促使云端服务提供者推出国内恢復区。超大规模云端服务商与国内通讯合作,建立自主设施,在遵守法律储存限制的前提下,实现来自海外的备份服务。新加坡和澳洲的新兴企业正在推出资料保护即服务(DPaaS),将安全的小型资料库与全球容错移转选项相结合,吸引那些需要在贸易和合规之间寻求平衡的中型出口商。

在欧洲,GDPR、DORA、《网路弹性法案》和欧盟资料法案(将于2025年9月生效)正在推动相关技术的快速普及。法国的「信任云」(Cloud de Confiance)和德国的「Gaia-X」等国家级计画正在资助基于标准的基础设施建设,这些基础设施强调透明度和供应商可移植性。服务提供者透过提供区域内元资料处理、欧盟居住者营运人员和可导出的审核追踪来凸显自身优势。自主选择权可以减少监管摩擦,并提高公共机构的连结率。

拉丁美洲、中东和非洲等新兴市场的云端技术应用规模较小。波湾合作理事会政府正在资助主权云端平台,以实现经济多元化并吸引金融科技新兴企业。巴西银行正在跨国复製链路上试行量子安全加密技术,以因应未来的加密需求。非洲通讯业者正在部署SaaS备份,以保护快速发展的行动支付平台,弥补本地资料中心容量的不足。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 严格的资料主权法规(GDPR、CCPA、DORA 等)

- 边缘和云端非结构化资料爆炸性成长

- 勒索软体抵御能力日益受到董事会的重视

- 与网路保险定价相关的云端原生网路復原库

- 为中东和亚太地区的超大规模资料中心业者主权云

- 量子安全加密试点计画将推动资料保护即服务 (DPaaS) 合约续约

- 市场限制

- 多重云端储存中的隐藏退出和 API 成本

- 透过专有备份格式实现供应商锁定

- AI压缩会减少备份檔案大小并延迟升级。

- 双边贸易协定中的资料居住条款限制了跨境灾难復原即服务 (DRaaS)。

- 产业价值链分析

- 监管环境

- 技术展望

- 产业吸引力:波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

第五章 市场规模及成长预测(金额)

- 按服务类型

- Storage-as-a-Service(STaaS)

- Backup-as-a-Service(BaaS)

- Disaster-Recovery-as-a-Service(DRaaS)

- 按部署模式

- 公有云

- 私有云端

- 混合云

- 按组织规模

- 大公司

- 小型企业

- 按最终用户行业划分

- BFSI

- 医疗保健和生命科学

- 政府/国防

- 资讯科技和电讯

- 零售与电子商务

- 製造业

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 新加坡

- 马来西亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Amazon Web Services Inc.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Cisco Systems Inc.

- Oracle Corporation

- VMware Inc.

- Commvault Systems Inc.

- Veritas Technologies LLC

- Asigra Inc.

- Quantum Corporation

- Quest Software Inc.

- NxtGen Datacenter & Cloud Technologies Pvt Ltd

- Hitachi Vantara LLC

- Acronis International GmbH

- Rubrik Inc.

- Druva Inc.

- Cohesity Inc.

- HYCU Inc.

- Backblaze Inc.

- Wasabi Technologies Inc.

- NetApp Inc.

- Zerto LLC

- N-able Inc.

- Arcserve LLC

第七章 市场机会与未来趋势

- 閒置频段与未满足需求评估

The Data Protection As A Service Market size is estimated at USD 21.37 billion in 2025, and is expected to reach USD 62.90 billion by 2030, at a CAGR of 24.10% during the forecast period (2025-2030).

Growth is propelled by a surge in unstructured data, zero-trust mandates, and rising board-level concern over ransomware exposure. Enterprises are rapidly replacing capital-intensive, on-premises backup hardware with cloud-delivered subscriptions that offer usage-based pricing and elastic scale. Sovereign-cloud investments, quantum-safe encryption pilots, and cyber-insurance requirements are converging to reshape product roadmaps, while vendor consolidation is compressing market structure and accelerating feature integration.

Global Data Protection As A Service Market Trends and Insights

Stringent Data-Sovereignty Regulations Reshape Global Protection

The roll-out of GDPR look-alike frameworks from Brazil to India is forcing firms to localize storage, adopt precise data-mapping, and build policy-based controls that govern cross-border flows. The EU Digital Operational Resilience Act took effect in January 2025, mandating near-real-time incident reporting for financial institutions. In the United States, new rules restrict sensitive data transfers to foreign adversaries, adding complexity for multinationals. As a result, procurement teams now rank sovereignty controls alongside RPO/RTO metrics when selecting DPaaS vendors. Providers are responding with region-specific key management, double-encryption options, and in-region recovery vaults that satisfy both national regulators and internal risk committees.

Edge Computing Revolutionizes Protection Architectures

Edge deployments move processing closer to sensor endpoints and branch locations, allowing workloads to meet latency targets without routing traffic back to centralized data hubs. Forty percent of large enterprises plan to run mission-critical applications at the edge by end-2025; that shift necessitates lightweight, policy-driven backup agents capable of executing locally and synchronizing asynchronously. Emerging offerings embed AI-based anomaly detection at edge gateways, reducing dwell time for ransomware incursions. Healthcare systems are piloting these capabilities in hospital campuses to comply with strict patient-data localization rules while ensuring immediate access for clinicians.

Hidden Cloud Costs Undermine Multi-Cloud Strategies

Variable traffic fees and per-API call pricing can inflate budgets, especially for analytics-heavy or regulatory inquiries that require frequent restores. Enterprises with limited negotiation leverage in smaller cloud regions feel the pinch most acutely. FinOps teams are investing in cost-observability dashboards, yet fragmented billing across storage tiers and hot-cold transitions remains a budgetary hazard.

Other drivers and restraints analyzed in the detailed report include:

- Ransomware Resilience Becomes a Board Priority

- Cloud-Native Recovery Vaults Transform Resilience Economics

- Proprietary Formats Create Vendor Lock-In

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Disaster-Recovery-as-a-Service segment recorded a 29.5% CAGR outlook through 2030, outpacing other offerings as leadership teams elevate ransomware readiness to a strategic metric. More than 70% of enterprises intend to integrate DRaaS with SIEM telemetry by 2026, enabling automated failover based on threat scoring. Continuous data protection streams shrink recovery-point objectives to seconds, appealing to finance and healthcare workloads where data loss equates to compliance fines. Storage-as-a-Service, though still capturing 43.2% of the 2024 data protection as a service market share, is evolving toward intelligent tiering and policy-based immutability that aligns with zero-trust architectures. Converged platforms now bundle BaaS, STaaS, and DRaaS under unified policy engines, easing procurement and governance.

While DRaaS enthusiasm rises, storage subscriptions remain foundational. Object-store growth stays strong due to AI model training sets and video analytics that balloon unstructured data volumes. In response, providers are pushing petabyte-scale deduplication and compression to control the footprint. Full-stack offerings from cloud hyperscalers now integrate autonomous threat scanning, meaning that ransomware reels only the affected blocks rather than entire volumes. Such feature alignment signals a longer-term move toward platform-centric purchasing in which recovery automation, data classification, and compliance mapping exist inside a single control plane.

Hybrid models show the fastest expansion at 31.5% CAGR. Regulators endorse architectures that keep sensitive datasets on local private clouds while allowing burstable analytics in regulated public regions. These patterns are especially evident among European banks subject to the Digital Operational Resilience Act, which mandates documented contingency arrangements for third-party services. Policy automation selects storage targets based on data-classification labels, optimizing both latency and compliance. The data protection as a service market size for hybrid solutions is forecast to double by 2028 as enterprises modernize legacy tape archives into cloud-connected vaults.

Private-cloud deployments retain a 43.7% share, favored by defense, utilities, and healthcare agencies that must assert custody over encryption keys. Vendors supplying private-cloud appliances increasingly embed FIPS-validated HSMs, role-based access, and air-gapped configuration management. Public-cloud approaches remain popular among digital-native firms that value region diversity over full sovereignty. However, sovereign-cloud initiatives, such as the AWS European Sovereign Cloud, blur lines: they deliver public-cloud agility under local legal control, pulling regulated workloads into environments previously deemed off-limits.

Data Protection As A Service Market is Segmented by Service Type (Storage-As-A-Service, Backup-As-A-Service, and Disaster-Recovery-As-A-Service), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserves a 37.8% revenue share, anchored by robust cloud adoption and federal directives such as CISA Binding Operational Directive 25-01, which compels agencies to apply secure configuration baselines for SaaS. The Protecting Americans' Data from Foreign Adversaries Act restricts cross-border transfers of sensitive personal data, spurring demand for in-country vaults and key escrow. Enterprises prioritize compliance mapping features that generate automated attestation reports for auditors.

Asia-Pacific posts the fastest trajectory at 31.4% CAGR as digital-government programs in Japan, India, and Korea push data-localization rules. The Indian Digital Personal Data Protection Act codifies explicit localization for critical personal information, pressuring cloud providers to launch domestic recovery zones. Hyperscalers partner with domestic telecom carriers to establish sovereign facilities that allow foreign backup services while respecting legal custody constraints. Start-ups in Singapore and Australia roll out DPaaS offerings that combine secure local storage with global failover options, appealing to mid-market exporters balancing trade and compliance.

Europe remains a sophisticated adopter shaped by GDPR, DORA, the Cyber Resilience Act, and the EU Data Act, effective September 2025. National programs such as France's Cloud de Confiance and Germany's Gaia-X channel funding into federated, standards-based infrastructure that prizes transparency and vendor portability. Providers differentiate by offering in-region metadata processing, EU resident-only operations staff, and exportable audit trails. Sovereign options reduce regulatory friction, driving higher attach rates among public-sector entities.

Emerging markets in Latin America, the Middle East, and Africa register rising adoption from smaller bases. Gulf Cooperation Council governments finance sovereign-cloud platforms to diversify economies and lure fintech start-ups. Brazilian banks pilot quantum-safe encryption on cross-border replication links, anticipating future cryptographic requirements. African telcos deploy SaaS backup to protect rapidly expanding mobile money platforms, offsetting limited local data-center capacity.

- IBM Corporation

- Amazon Web Services Inc.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Cisco Systems Inc.

- Oracle Corporation

- VMware Inc.

- Commvault Systems Inc.

- Veritas Technologies LLC

- Asigra Inc.

- Quantum Corporation

- Quest Software Inc.

- NxtGen Datacenter & Cloud Technologies Pvt Ltd

- Hitachi Vantara LLC

- Acronis International GmbH

- Rubrik Inc.

- Druva Inc.

- Cohesity Inc.

- HYCU Inc.

- Backblaze Inc.

- Wasabi Technologies Inc.

- NetApp Inc.

- Zerto LLC

- N-able Inc.

- Arcserve LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent data-sovereignty regulations (GDPR, CCPA, DORA, etc.)

- 4.2.2 Explosive growth of unstructured data across edge and cloud

- 4.2.3 Board-level focus on ransomware resiliency

- 4.2.4 Cloud-native cyber-recovery vaults tied to cyber-insurance pricing

- 4.2.5 Sovereign-cloud build-outs in Middle-East and APAC hyperscaler

- 4.2.6 Quantum-safe encryption pilots driving refresh of DPaaS contracts

- 4.3 Market Restraints

- 4.3.1 Hidden egress and API costs in multi-cloud storage

- 4.3.2 Vendor lock-in due to proprietary backup formats

- 4.3.3 AI-driven compression reducing backup volumes, delaying upgrades

- 4.3.4 Data-residency clauses in bilateral trade pacts limiting cross-border DRaaS

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 Storage-as-a-Service (STaaS)

- 5.1.2 Backup-as-a-Service (BaaS)

- 5.1.3 Disaster-Recovery-as-a-Service (DRaaS)

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Government and Defense

- 5.4.4 IT and Telecom

- 5.4.5 Retail and E-commerce

- 5.4.6 Manufacturing

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Amazon Web Services Inc.

- 6.4.3 Hewlett Packard Enterprise Company

- 6.4.4 Dell Technologies Inc.

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Oracle Corporation

- 6.4.7 VMware Inc.

- 6.4.8 Commvault Systems Inc.

- 6.4.9 Veritas Technologies LLC

- 6.4.10 Asigra Inc.

- 6.4.11 Quantum Corporation

- 6.4.12 Quest Software Inc.

- 6.4.13 NxtGen Datacenter & Cloud Technologies Pvt Ltd

- 6.4.14 Hitachi Vantara LLC

- 6.4.15 Acronis International GmbH

- 6.4.16 Rubrik Inc.

- 6.4.17 Druva Inc.

- 6.4.18 Cohesity Inc.

- 6.4.19 HYCU Inc.

- 6.4.20 Backblaze Inc.

- 6.4.21 Wasabi Technologies Inc.

- 6.4.22 NetApp Inc.

- 6.4.23 Zerto LLC

- 6.4.24 N-able Inc.

- 6.4.25 Arcserve LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

资料保护即服务市场:2026-2032年全球市场预测(按服务、解决方案、组织规模、安全关注点和产业划分)

资料保护即服务市场:2026-2032年全球市场预测(按服务、解决方案、组织规模、安全关注点和产业划分) 2026年全球资料保护服务(DPaaS)市场报告

2026年全球资料保护服务(DPaaS)市场报告 资料保护即服务 (DPaaS) 市场规模、份额和趋势分析(按服务、部署类型、企业规模、最终用途、地区和细分市场预测,2026-2033 年)

资料保护即服务 (DPaaS) 市场规模、份额和趋势分析(按服务、部署类型、企业规模、最终用途、地区和细分市场预测,2026-2033 年) 资料保护服务市场规模、份额和成长分析(按服务类型、部署类型、组织规模和地区划分)-2026年至2033年产业预测

资料保护服务市场规模、份额和成长分析(按服务类型、部署类型、组织规模和地区划分)-2026年至2033年产业预测 Data-As-A-Service资料服务保护的全球市场:各服务形式,各部署模式,各组织规模,各终端用户业界,各地区,机会,预测,2018年~2032年

Data-As-A-Service资料服务保护的全球市场:各服务形式,各部署模式,各组织规模,各终端用户业界,各地区,机会,预测,2018年~2032年 资料保护即服务市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:依服务类型、部署、企业规模、最终用途产业及地理划分

资料保护即服务市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:依服务类型、部署、企业规模、最终用途产业及地理划分 按服务类型、部署类型、组织规模、行业和地区分類的全球资料保护即服务 (DPaaS) 市场 - 到 2030 年的预测

按服务类型、部署类型、组织规模、行业和地区分類的全球资料保护即服务 (DPaaS) 市场 - 到 2030 年的预测 资料保护服务的全球市场规模、份额和趋势分析:按服务、按部署、按公司规模、按最终用途、按地区、前景和预测,2024-2031 年

资料保护服务的全球市场规模、份额和趋势分析:按服务、按部署、按公司规模、按最终用途、按地区、前景和预测,2024-2031 年 DPaaS(资料保护即服务)的全球市场,2024-2028

DPaaS(资料保护即服务)的全球市场,2024-2028