|

市场调查报告书

商品编码

1851098

容器即服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Container As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

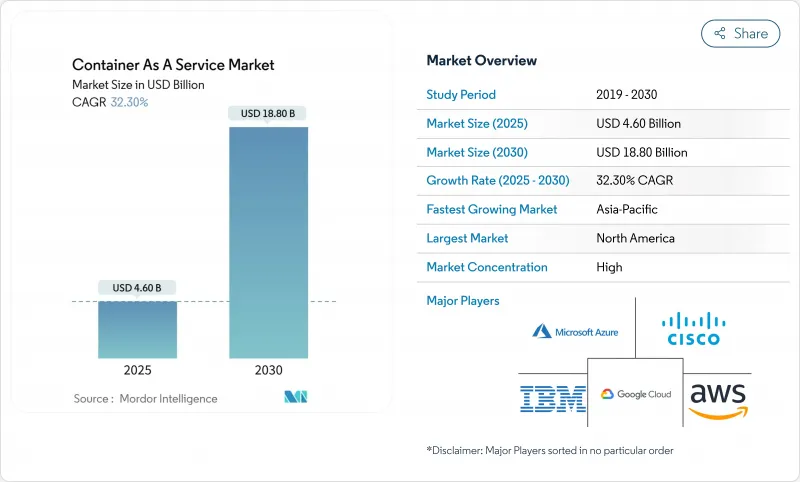

预计到 2025 年,货柜即服务市场规模将达到 46 亿美元,到 2030 年将达到 188 亿美元,年复合成长率为 32.3%。

云端原生敏捷性、多重云端策略的兴起以及对精细化资源分配的强劲需求正在重塑企业基础设施决策。在亚太和欧洲,主权云端指令以及软体材料清单(SBOM) 指令正在推动企业采用云端服务,超越传统的「直接迁移」模式。儘管云端部署仍占营收的 78%,但随着受监管产业采用混合模式,本地部署正以 34% 的复合年增长率加速成长。託管服务占收入的 54%,负责处理先前由企业内部完成的安全扫描和合规自动化任务。中小企业 (SME) 目前是成长最快的客户群体,这反映了按需付费收费和低进入门槛的吸引力。製造业是关键成长产业,它利用轻量级编配来运作支援工业 4.0倡议的 AI 赋能边缘工作负载。

全球容器即服务市场趋势与洞察

与云端平台无关的 Kubernetes 平台避免了厂商锁定

为了避免厂商锁定并争取更优惠的价格,云端编配正被日益广泛地采用。跨厂商运行相同丛集的平台简化了工作负载的可移植性,并在测试有状态微服务时将迁移停机时间减少 77%。像 HPE 这样的厂商正在将虚拟机器和容器整合到单一控制平面中,以强化混合云策略。

计量收费的透明度提高了中小企业的采用率。

面向消费者的定价策略消除了中小企业的资本投资障碍。 AWS Fargate 和 EKS 的成本视觉化工具可协助中小企业无需专门的 DevOps 团队即可部署生产丛集。自动化的实例大小调整和竞价型实例利用率进一步使成本与流量波动保持一致,从而支持了中小企业 36.7% 的复合年增长率。

认证K8S维运人员短缺

人才短缺会减缓技术应用,并增加营运风险。新兴市场的企业往往依赖成本高昂的咨询顾问,导致计划週期延长。训练体系无法满足服务网格、GitOps 和边缘丛集技能的需求。

细分市场分析

儘管云端运算仍保持其主导地位,但预计本地丛集将以 34% 的复合年增长率成长,这反映了合规性需求、本地处理的延迟优势以及企业希望升级现有硬体而非重新部署所有工作负载的愿望。 HPE GreenLake 提供基于使用量的私有云端定价模式,与公共云端的经济模式类似,这表明供应商正在适应混合云的需求。

企业通常在云端运行开发和突发工作负载,同时将对延迟敏感或受监管的应用程式保留在本地。容器即服务 (CaaS) 市场透过统一的控制平面支援无缝的工作负载迁移,使团队能够根据效能和自主需求迁移容器。随着混合部署成熟度的提高,部署决策将更多地取决于成本和合规性等可衡量的变量,而不是预设的云端优先策略。

託管服务占了 54% 的市场份额,年复合成长率达 34.5%。服务提供者正在整合人工智慧主导的资源调优和自动化补丁程序,以确保执行时间,同时减少对内部人员的需求。 T-Mobile 为其通讯业者云端功能采用了託管的 Red Hat OpenShift 技术堆迭,检验了该方法在关键任务型 5G 工作负载方面的有效性。

专业服务对于迁移和复杂整合仍然至关重要,但其带来的收入只是暂时的。随着时间的推移,週期性的託管服务将超越计划工作。容器即服务 (Container-as-a-Service) 市场也反映了这一转变,新功能(例如 BBOM 自动化、供应链安全、FinOps 控制面板)被打包到订阅方案中,从而带来可衡量的成果。

容器即服务 (Containers as A Service) 市场报告按配置类型(本地部署、云端部署)、服务类型(专业服务、託管服务)、公司规模(中小企业、大型企业)、最终用户应用(银行、金融服务和保险 (BFSI)、零售、IT 和通讯、製造业、其他最终用户应用)以及地区对产业进行细分。市场预测以美元计价。

区域分析

北美地区受益于成熟的超大规模生态系统和积极的企业现代化进程,预计到2024年将占据38.5%的云端收入份额。领先的云端服务供应商预计在2025年实现两位数的云端收入成长,进一步巩固该地区的领先地位。然而,Kubernetes维运技能的短缺正在阻碍成长,并推动了对託管服务的需求。

亚太地区预计将以39.4%的复合年增长率实现最快成长,这主要得益于主权云端规则和国家资助的人工智慧基础设施。印度已拨款13亿美元用于运算能力建设,其中包括为公共和私有人工智慧丛集购置1万个GPU。以阿里云、腾讯云和华为云主导的中国生态系统正加速混合云的普及,华为云平台在亚太新兴市场的营收成长高达106%。

欧盟资料法规将于2025年9月生效,届时将强制要求云端资料可携性,并于2027年取消云端切换费用。拥有完全云端无关架构的供应商可能更具优势,而主权条款则可能促进区域性云端即服务(CaaS)平台的发展。德国、法国和英国在采用这项法规方面处于领先地位,但监管的复杂性可能会减缓采购週期,直到认证机制最终确定。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 与云端平台无关的 Kubernetes 平台避免了厂商锁定

- 按使用付费的透明度提高了小型企业的采用率。

- DevSecOps SBOM 指令加速了託管 CaaS 的发展。

- 支援人工智慧/机器学习的GPU集群正在迅速普及

- 5G边缘微型资料中心部署需要轻量级CaaS。

- 主权云端指令推动国内云端即服务(CaaS)发展。

- 市场限制

- Kubernetes认证操作员短缺

- 核心级逃逸和 eBPF 攻击向量

- 难以预测的云端帐单

- 可观测性许可成本细分

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争的激烈程度

- 投资分析

第五章 市场规模与成长预测

- 透过部署

- 云

- 本地部署

- 按服务类型

- 託管服务

- 专业服务

- 按公司规模

- 小型企业

- 大公司

- 透过最终用户使用

- BFSI

- 零售

- 资讯科技/通讯

- 製造业

- 卫生保健

- 政府机构

- 其他(媒体、游戏、教育科技)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services

- Microsoft Azure

- Google Cloud(GKE)

- IBM Corp(Red Hat OpenShift)

- Alibaba Cloud

- VMware Tanzu

- Cisco Systems

- SUSE Rancher

- Oracle Container Engine

- Hewlett Packard Enterprise(Ezmeral)

- Mirantis

- D2iQ

- Platform9 Systems

- Akamai(Linode)

- DigitalOcean

- Rackspace Technology

- Nutanix

- Canonical

- HashiCorp

- Huawei Cloud

- Tencent Cloud

- OVHCloud

第七章 市场机会与未来展望

The Container-as-a-Service market size stands at USD 4.6 billion in 2025 and is forecast to reach USD 18.8 billion by 2030, expanding at a 32.3% CAGR.

Strong demand for cloud-native agility, rising multi-cloud strategies and granular resource allocation are reshaping enterprise infrastructure decisions. Sovereign-cloud directives in Asia-Pacific and Europe, together with mandatory software bill of materials (SBOM) rules, are widening adoption beyond classic lift-and-shift migrations. Cloud deployment still represents 78% of revenue, but on-premise deployment is accelerating at a 34% CAGR as regulated industries embrace hybrid models. Managed services, which hold 54% share, are taking on security scanning and compliance automation tasks once handled internally. Small and medium enterprises now form the fastest-growing customer group, reflecting the appeal of pay-per-use billing and low entry costs. Manufacturing is the leading growth vertical, leveraging lightweight orchestration to operate AI-enabled edge workloads that support Industry 4.0 initiatives.

Global Container As A Service Market Trends and Insights

Cloud-agnostic Kubernetes Platforms Avert Lock-in

Enterprises increasingly deploy cloud-agnostic orchestration to avoid vendor dependency and negotiate favorable pricing. Platforms that run identical clusters across providers simplify workload portability and reduce migration downtime by 77% in stateful microservices tests. Vendors such as HPE integrate virtual machines and containers within one control plane, strengthening hybrid strategies.

Pay-per-use Transparency Grows SME Adoption

Consumption pricing eliminates capital expenditure barriers for smaller firms. AWS Fargate and EKS cost-visibility tools help SMEs deploy production clusters without dedicated DevOps teams. Automated rightsizing and spot-instance use further align expenses with fluctuating traffic, supporting the 36.7% CAGR recorded for SMEs.

Shortage of Certified K8s Operators

The talent gap delays deployments and raises operating risk. Enterprises in emerging markets often rely on costly consultants, lengthening project timelines. Training pipelines have yet to match demand for service-mesh, GitOps and edge cluster skills.

Other drivers and restraints analyzed in the detailed report include:

- DevSecOps SBOM Mandates Accelerate Managed CaaS

- AI/ML GPU-ready Clusters Surge

- Kernel-level Escape and eBPF Attack Vectors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise clusters are forecast to grow at a 34% CAGR even though cloud maintains dominant share. This reflects compliance needs, local-processing latency advantages and a desire to modernize existing hardware rather than relocate every workload. HPE GreenLake offers consumption-based private-cloud pricing that mirrors public-cloud economics, demonstrating how suppliers adapt to hybrid demand.

Organizations usually run development and bursting workloads in the cloud while retaining latency-sensitive or regulated applications on-site. The Container-as-a-Service market supports seamless workload migration through unified control planes, allowing teams to shift containers in response to performance or sovereignty requirements. As hybrid maturity rises, placement decisions hinge on measurable cost and compliance variables rather than a default cloud-first stance.

Managed offerings hold 54% share and are expanding at 34.5% CAGR as enterprises offload day-two operations. Providers integrate AI-driven resource tuning and automated patching, ensuring uptime while lowering internal headcount needs. T-Mobile adopted a managed Red Hat OpenShift stack for telco cloud functions, validating the approach for mission-critical 5G workloads.

Professional services remain essential for migrations and complex integrations, but revenue is episodic. Over time, recurring managed contracts outpace project work. The Container-as-a-Service market reflects this shift as new features-SBOM automation, supply-chain security and FinOps dashboards-are bundled into subscription tiers that deliver measurable outcomes.

Containers As A Service Market Report Segments the Industry Into by Deployment (On-Premise, Cloud), by Service Type (Professional Services, Managed Services), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Application (BFSI, Retail, IT & Telecommunications, Manufacturing, Other End-User Applications), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America earns 38.5% of 2024 revenue, benefitting from established hyperscale ecosystems and aggressive enterprise modernization. Major providers posted double-digit cloud revenue growth in 2025, reinforcing regional dominance. Skills shortages in Kubernetes operations, however, are creating a drag that fuels demand for managed services.

Asia-Pacific is forecast to grow at 39.4% CAGR, the fastest worldwide, due to sovereign-cloud rules and state-funded AI infrastructure. India allocated USD 1.3 billion for compute capacity, including 10,000 GPUs earmarked for public-private AI clusters. China's ecosystem, led by Alibaba Cloud, Tencent Cloud and Huawei Cloud, is expanding hybrid-cloud deployments, with Huawei Cloud Stack reporting 106% revenue growth in emerging Asia-Pacific markets.

Europe faces distinctive dynamics under the EU Data Act, effective September 2025, which mandates cloud portability and removes switching fees by 2027. Providers with genuinely cloud-agnostic architectures appear better positioned, while sovereignty clauses are likely to spur regional CaaS platforms. Germany, France and the United Kingdom lead adoption, but regulatory complexity could slow purchase cycles until certification schemes settle.

- Amazon Web Services

- Microsoft Azure

- Google Cloud (GKE)

- IBM Corp (Red Hat OpenShift)

- Alibaba Cloud

- VMware Tanzu

- Cisco Systems

- SUSE Rancher

- Oracle Container Engine

- Hewlett Packard Enterprise (Ezmeral)

- Mirantis

- D2iQ

- Platform9 Systems

- Akamai (Linode)

- DigitalOcean

- Rackspace Technology

- Nutanix

- Canonical

- HashiCorp

- Huawei Cloud

- Tencent Cloud

- OVHCloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-agnostic Kubernetes platforms avert lock-in

- 4.2.2 Pay-per-use transparency grows SME adoption

- 4.2.3 DevSecOps SBOM mandates accelerate managed CaaS

- 4.2.4 AI/ML GPU-ready clusters surge

- 4.2.5 5G edge micro-DC roll-outs need lightweight CaaS

- 4.2.6 Sovereign-cloud mandates spur domestic CaaS

- 4.3 Market Restraints

- 4.3.1 Shortage of certified K8s operators

- 4.3.2 Kernel-level escape and eBPF attack vectors

- 4.3.3 Unpredictable cloud egress fees

- 4.3.4 Fragmented observability licensing costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.2 By Service Type

- 5.2.1 Managed Services

- 5.2.2 Professional Services

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Application

- 5.4.1 BFSI

- 5.4.2 Retail

- 5.4.3 IT and Telecommunications

- 5.4.4 Manufacturing

- 5.4.5 Healthcare

- 5.4.6 Government

- 5.4.7 Others (Media, Gaming, EdTech)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Israel

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Microsoft Azure

- 6.4.3 Google Cloud (GKE)

- 6.4.4 IBM Corp (Red Hat OpenShift)

- 6.4.5 Alibaba Cloud

- 6.4.6 VMware Tanzu

- 6.4.7 Cisco Systems

- 6.4.8 SUSE Rancher

- 6.4.9 Oracle Container Engine

- 6.4.10 Hewlett Packard Enterprise (Ezmeral)

- 6.4.11 Mirantis

- 6.4.12 D2iQ

- 6.4.13 Platform9 Systems

- 6.4.14 Akamai (Linode)

- 6.4.15 DigitalOcean

- 6.4.16 Rackspace Technology

- 6.4.17 Nutanix

- 6.4.18 Canonical

- 6.4.19 HashiCorp

- 6.4.20 Huawei Cloud

- 6.4.21 Tencent Cloud

- 6.4.22 OVHCloud

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

容器即服务 (CaaS) 市场规模、份额和成长分析(按部署模式、服务类型、最终用户产业、容器技术、收费模式和地区划分)—2026-2033 年产业预测

容器即服务 (CaaS) 市场规模、份额和成长分析(按部署模式、服务类型、最终用户产业、容器技术、收费模式和地区划分)—2026-2033 年产业预测 容器即服务市场 - 全球产业规模、份额、趋势、机会及预测(按服务类型、部署模式、组织规模、产业垂直领域、地区和竞争格局划分,2021-2031 年)

容器即服务市场 - 全球产业规模、份额、趋势、机会及预测(按服务类型、部署模式、组织规模、产业垂直领域、地区和竞争格局划分,2021-2031 年) 容器即服务市场按服务类型、部署模式、组织规模和最终用户产业划分-全球预测,2025-2032年

容器即服务市场按服务类型、部署模式、组织规模和最终用户产业划分-全球预测,2025-2032年 2032 年容器即服务 (CaaS) 市场预测:按服务类型、部署模式、组织规模、最终用户和地区进行的全球分析

2032 年容器即服务 (CaaS) 市场预测:按服务类型、部署模式、组织规模、最终用户和地区进行的全球分析 容器即服务市场规模、份额和趋势分析报告:按服务类型、部署、公司规模、最终用途、地区和细分市场进行预测,2025 年至 2033 年

容器即服务市场规模、份额和趋势分析报告:按服务类型、部署、公司规模、最终用途、地区和细分市场进行预测,2025 年至 2033 年