|

市场调查报告书

商品编码

1851123

雷射清洗:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Laser Cleaning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

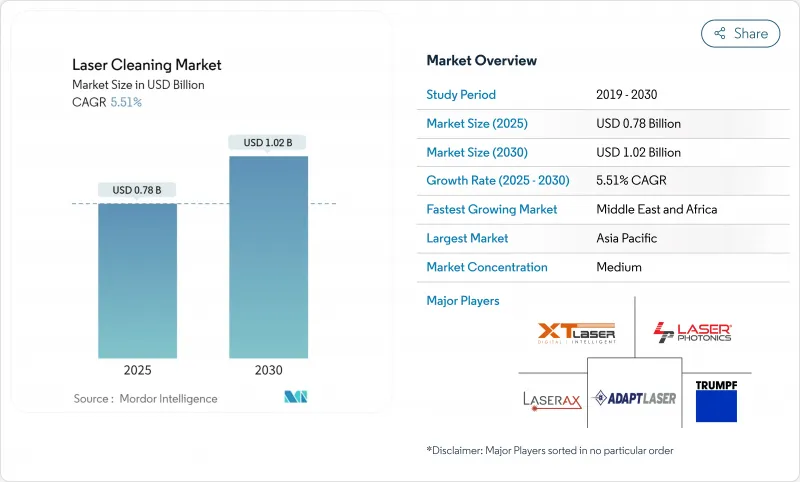

预计到 2025 年,雷射清洗市场规模将达到 7.8 亿美元,到 2030 年将达到 10.2 亿美元,复合年增长率为 5.51%。

北美和欧洲对化学溶剂的限制日益严格,亚洲光纤雷射的每瓦成本不断下降,以及汽车、航太和半导体工厂对非接触式表面处理的需求不断增长,共同推动了该领域的发展。超快脉衝技术正在拓展其在微电子和文化遗产修復等领域的精密应用,而与机器人技术的快速融合正在重塑生产线。儘管随着零件价格的下降,资本投资有所放缓,但高功率系统在发展中地区仍然价格昂贵。

全球雷射清洗市场趋势与洞察

严格的环境法规取代了化学溶剂

美国环保署(EPA)关于高氯酸乙烯酯的法规将于2024年12月最终确定,届时将禁止其大部分工业用途,从而加速从化学清洗到雷射清洗的转变。类似的有害空气污染物法规将于2025年1月实施,将加大合规压力。雷射清洗解决方案不会产生二次废弃物,从而降低了以往依赖溶剂的工厂的处置成本和报告义务。这种政策环境缩短了雷射清洗的投资回收期,直接促进了雷射清洗市场的成长。供应商正在调整其产品以符合政府支持低排放设备升级的补贴计画。

非接触式表面处理自动化需求日益增长

大型製造工厂正将光纤雷射与协作机器人结合,以减少工时并实现一致的表面品质。 IPG 光电于 2024 年 5 月推出的 LightWELD 机器人单元,展示了一种即插即用系统,只需轻触萤幕即可在焊接和清洗之间切换。自动化也缓解了技术纯熟劳工短缺的问题,使一名操作员能够管理多个工位。这种效率的提升预计将推动机器人雷射工作单元实现 14.6% 的复合年增长率,显着高于雷射清洗市场的整体成长速度。供应商正在整合视觉软体和人工智慧技术,以自动调整参数,从而缩短操作员培训时间并提高其应用普及率。

高昂的资本投资障碍阻碍了市场发展

功率超过1千瓦的高功率雷射售价可能高达30万至50万美元。如此高昂的价格令小型製造商的预算捉襟见肘,并减缓了印尼、巴西和肯亚等国的订单。儘管二极体价格的下降导致拥有成本逐年降低,但资金筹措障碍仍然存在。租赁方案正在兴起,但利率推高了总支出。各国政府提供的绿色设备税额扣抵提高了设备的可负担性,但在大型工业场所之外,其普及速度仍然缓慢。因此,儘管存在安全和环境方面的缺陷,许多新兴经济体的买家仍然依赖喷砂进行重型清洁,这阻碍了雷射清洗市场的渗透。

细分市场分析

到2024年,光纤光源将占据雷射清洗市场58%的收入份额。这是因为其内部二极体耦合可提供40%的电能转换效率,密封的光路可避免污染,且设备无需维护即可运作5万小时。中国加工厂正在采购300W的设备用于模具维护,德国电动车工厂则正在安装3kW的雷射头用于车轴除垢。随着二极体价格降至10美元/瓦以下,甚至越南的纺织机械翻新商也加入了客户行列,这表明雷射清洗市场已在全球范围内蓬勃发展。

超快脉衝雷射设备以6.6%的复合年增长率成长,利用冷烧蚀技术去除硅片上20奈米的氧化层,而不会熔化基板。供应商正在出货用于手錶机芯的50瓦飞秒雷射头和用于高密度互连基板的100瓦皮秒钻机,这凸显了该技术已从学术界扩展到大规模生产领域。固体雷射和二氧化碳雷射仍然占据着特定的应用领域。石材雕刻清洗使用波长较长的激光,可以有效地与碳酸盐基质结合;而塑胶加工则依赖于10.6微米的二氧化碳激光,以避免加热金属基板。

到2024年,中功率(100W-1kW)的雷射清洗设备将占据46%的市场份额,其去除率足以满足汽车副车架的清洗需求,并且能够连接标准的工厂电源。据一级供应商称,500W手持式雷射枪去除氧化皮的速度比120目砂纸打磨快60%,而且无需使用耗材砂碟。这种高效的性能能够促进重复订单,并在资本预算紧张时增强市场韧性。

随着造船厂和铁路船厂寻求更快速的船体除垢方法,高功率(1kW以上)雷射清洗设备市场将以7.1%的复合年增长率成长。澳洲的Precision Laser Cleaning公司展示了每小时20平方公尺的防污涂层去除能力,从而缩短了船舶的干船坞维修时间并节省了燃料。 Gold Mark公司的四合一3kW平台整合了焊接、清洗、切割和纹理处理功能,促使製造商用一台多功能设备取代多台机器。低功率(100W以下)设备则满足珠宝商和檔案管理员去除亚微米级污染物的需求,在这些应用中,热敏感性比循环时间更为重要。

区域分析

亚太地区占2024年销售额的41%,反映了中国、日本和韩国的电子产业群聚和汽车供应链的优势。该地区各国政府正在推行高科技製造业奖励,使企业更容易证明对雷射的资本支出是合理的。随着二极体价格的下降,该地区的中小型企业正在越来越多地采用300W光纤雷射。三井物产的红外线雷射除锈系统等先导计画凸显了业界对更清洁船舶维护的需求。

欧洲在永续製造和文物保护领域持续保持强劲的成长动能。严格的溶剂禁令恰逢雷射清洗市场蓬勃发展。欧盟致力于实现净零排放的工业政策,为工厂升级改造提供了资金筹措支持;同时,博物馆也开始部署飞秒雷射设备,用于精细修復壁画。德国弗劳恩霍夫雷射技术研究所(Fraunhofer ILT)透过其IDEEL计划,正在展示卷轴式雷射干燥技术,以辅助电池生产线中的电极清洗。

北美正充分利用其成熟的航太、国防和核能产业。津贴,雷射清洗技术能够去除涡轮叶片上的氧化膜,并对核子反应炉容器进行消毒。墨西哥新莱昂州和瓜纳华托州的汽车产业丛集正在投资300瓦手持式设备,以升级焊接夹具。中东和非洲地区以6.1%的复合年增长率领先,这主要得益于各国石油公司对防腐蚀技术的投资以及文物保护机构对考古遗址的修復。拉丁美洲的巴西汽车工厂和智利的矿业输送带发展势头强劲,但由于资金筹措有限,规模较小的经济体采用该技术的速度较为缓慢。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟和北美地区严格的环境法规正在取代化学溶剂。

- 汽车车体修理厂对自动化非接触式表面处理的需求日益增长

- 欧洲和亚洲历史建筑修復计划的成长

- 对需要远程雷射去污的核能设施退役投资

- 电动车电池生产线需要无残留电极清洗

- 光纤雷射每瓦成本的下降促使亚洲中小企业更多地采用该技术。

- 市场限制

- 开发中国家对高功率系统的大量资本投资

- 海上维护的现场便携性有限

- 热敏性材料基板有热损伤风险

- 新兴市场认证雷射清洗技术人员短缺

- 生态系分析

- 技术展望

- 超短脉衝(Ps/Fs)源的进展

- 协作机器人集成

- 监理展望

- 全球挥发性有机化合物与危险化学品指令

- OSHA 和 IEC 雷射安全标准

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(金额)

- 依雷射类型

- 光纤雷射

- 固体(Nd:YAG/Yb:YAG)雷射器

- 二氧化碳雷射

- 超短脉衝(皮秒/飞秒)激光

- 按输出范围

- 高功率(超过1千瓦)

- 中等功率(100瓦-1千瓦)

- 低功率(小于100瓦)

- 可移植性

- 手持/可携式系统

- 桌面/固定式系统

- 机器人/自动化堆迭单元

- 脉衝时间

- 共同波

- 奈秒脉衝

- 超短脉衝(Ps/Fs)

- 透过使用

- 油漆和涂层去除

- 除銹除氧化物

- 表面和焊接准备

- 霉菌清洁和霉菌维护

- 文化遗产与艺术修復

- 微电子、精密清洗

- 核能污染清除

- 按最终用户行业划分

- 汽车和运输设备

- 航太/国防

- 造船/海洋

- 基础设施和建筑

- 能源与电力

- 石油和天然气

- 核能

- 可再生能源

- 电子和半导体

- 文化遗产

- 製造和工业机械

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 东南亚

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 其他南美洲

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- TRUMPF Group

- IPG Photonics Corporation

- Clean-Lasersysteme GmbH

- Laser Photonics Corporation

- P-Laser NV

- Laserax Inc.

- Adapt Laser Systems LLC

- Jinan Xintian Technology Co. Ltd(XT Laser)

- HGLaser Engineering Co. Ltd

- Han's Laser Technology Industry Group Co. Ltd

- Coherent Corp.

- Scantech Laser Pvt. Ltd

- Anilox Roll Cleaning Systems

- Shenzhen Riselaser Technology Co. Ltd

- Sukjin Laser Co.

- Allied Scientific Pro

- CyCleanLaser GmbH

- PharosQuartz(Light Conversion)

- Suresh Industech Pvt. Ltd

- RMA Technik GmbH

- Jinan Vmade CNC Machine Co., Ltd

- Shanghai Mactron Technology Co. Ltd

- Lynton Lasers Ltd

第七章 市场机会与未来展望

The laser cleaning market size stands at USD 0.78 billion in 2025 and is forecast to reach USD 1.02 billion by 2030, reflecting a 5.51% CAGR.

Growth is propelled by strict limits on chemical solvents in Europe and North America, falling cost-per-watt of fiber lasers in Asia, and rising demand for contact-free surface preparation across automotive, aerospace, and semiconductor plants. Rapid integration with robotics is reshaping production lines, while ultrashort-pulse technology broadens precision applications in micro-electronics and cultural heritage restoration. Capital spending is easing as component prices decline, yet high-power systems remain cost-intensive in developing regions.

Global Laser Cleaning Market Trends and Insights

Stringent Environmental Regulations Replacing Chemical Solvents

EPA restrictions on perchloroethylene, finalized in December 2024, prohibit most industrial uses and accelerate the shift from chemical cleaning to lasers.Similar limits on hazardous air pollutants introduced in January 2025 add compliance pressure. Laser solutions generate no secondary waste, trimming disposal fees and reporting burdens for plants that once relied on solvents. The policy environment therefore shortens payback periods for laser installations and directly fuels laser cleaning market growth. Suppliers are aligning products with government rebate programs that support low-emission equipment upgrades.

Rising Automation Demand for Non-contact Surface Preparation

High-volume factories now pair fiber lasers with collaborative robots to cut labor time and achieve consistent surface quality. IPG Photonics' LightWELD robotic cell launched in May 2024 illustrates a plug-and-play system that toggles between welding and cleaning at the tap of a screen.Automotive body shops adopt similar cells for seam preparation before welding aluminum body panels. Automation also mitigates skilled-worker shortages, letting one operator supervise multiple stations. This efficiency edge underpins the 14.6% CAGR projected for robotic laser work cells-well above the overall laser cleaning market trajectory. Vendors are integrating vision software and AI to auto-adjust parameters, reducing operator training time and widening adoption.

High Capital Expenditure Barriers in Developing Markets

High-power lasers above 1 kW cost USD 300,000-500,000, a sum that strains small manufacturers' budgets and delays orders in Indonesia, Brazil, and Kenya usni.org. Although falling diode prices reduce ownership costs each year, financing hurdles remain. Leasing programs are emerging, yet interest rates elevate total outlay. Governments that offer green-equipment tax credits improve affordability, but uptake is slow outside large industrial hubs. As a result, many buyers in emerging economies continue to rely on abrasive blasting for heavy-duty cleaning despite safety and environmental drawbacks, moderating laser cleaning market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Restoration Projects of Historical Monuments

- EV Battery Production Lines Necessitating Residue-free Electrode Cleaning

- Field Deployment Challenges for Remote Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber sources delivered 58% of 2024 revenue for the laser cleaning market because internal diode coupling yields 40% wall-plug efficiency and sealed optical paths avert contamination, letting units run 50,000 hours without realignment. Chinese job shops buy 300 W units for mold maintenance, while German EV factories deploy 3 kW heads for axle de-scaling, illustrating versatility across power classes. As diode prices dip below USD 10/W, even textile-machinery rebuilders in Vietnam join the customer roster, broadening global reach of the laser cleaning market.

Ultrashort-pulse machines, growing 6.6% CAGR, exploit cold-ablation to lift 20 nm oxides from silicon wafers without melting substrates.Vendors ship 50 W femtosecond heads for watch-movement restoration and 100 W picosecond rigs for high-density interconnect boards, highlighting expansion beyond academia into volume manufacturing. Solid-state and CO2 lasers maintain niche roles: stone sculpture cleaning makes use of longer wavelengths that couple efficiently into carbonate matrices, whereas plastics processors rely on 10.6 µm CO2 energy to avoid metal substrate heating.

Medium-power (100 W-1 kW) units controlled 46% of the 2024 laser cleaning market size, offering removal rates suitable for automotive subframes yet plugging into standard factory mains. Tier-1 suppliers report that 500 W handheld guns strip mill scale 60% faster than 120 grit sanding while eliminating consumable discs. This productivity sweet spot drives repeat orders and underpins market resilience when capital budgets tighten.

High-power segments above 1 kW grow 7.1% CAGR as shipyards and rail depots seek faster hull descaling. Precision Laser Cleaning in Australia demonstrates 20 m2/h removal of antifouling coatings, cutting dry-dock time and saving fuel on cleaned vessels.au. Gold Mark's 4-in-1 3 kW platform combines welding, cleaning, cutting, and texturing, persuading fabricators to replace multiple machines with a single multipurpose asset. Low-power (<100 W) devices cater to jewelers and archivists for sub-micron contaminant removal where heat sensitivity overrides cycle-time concerns.

The Laser Cleaning Market Report is Segmented by Laser Type (Fiber Lasers, Solid-State (Nd:YAG/Yb:YAG) Lasers, and More), Portability (Handheld/Portable Systems, and More), Pulse Duration (Continuous-Wave, and More), Application (Paint and Coating Removal, and More), Power Range (High, Medium, and Low), End-User Industry (Automotive and Transport, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominated 2024 revenue with 41%, reflecting dense electronics clusters and automotive supply chains in China, Japan, and South Korea. Regional governments promote high-tech manufacturing incentives that make capital spending on lasers easier to justify. The region's small-to-medium enterprises increasingly embrace 300 W fiber tools as diode prices fall. Pilot projects such as Mitsui O.S.K. Lines' InfraLaser rust-removal system confirm industry appetite for cleaner ship maintenance.

Europe follows with strong adoption across sustainable manufacturing and heritage conservation. Strict solvent bans align with laser cleaning market momentum. The EU's focus on net-zero industry policies creates funding channels for plant upgrades, while museums deploy femtosecond units to delicately restore frescoes. Germany's Fraunhofer ILT, through the IDEEL project, demonstrates roll-to-roll laser drying that complements electrode cleaning in battery lines.

North America leverages mature aerospace, defense, and nuclear sectors. Laser cleaning removes oxide films from turbine blades and decontaminates reactor vessels, supported by Department of Energy R&D grants. Mexico's auto clusters in Nuevo Leon and Guanajuato invest in 300 W handheld gear to upgrade welding jigs. The Middle East & Africa leads growth at 6.1% CAGR as national oil companies invest in corrosion control and heritage authorities restore archaeological sites. Latin America grows steadily in Brazil's auto plants and Chile's mining conveyors, but limited financing slows penetration in smaller economies.

- TRUMPF Group

- IPG Photonics Corporation

- Clean-Lasersysteme GmbH

- Laser Photonics Corporation

- P-Laser NV

- Laserax Inc.

- Adapt Laser Systems LLC

- Jinan Xintian Technology Co. Ltd (XT Laser)

- HGLaser Engineering Co. Ltd

- Han's Laser Technology Industry Group Co. Ltd

- Coherent Corp.

- Scantech Laser Pvt. Ltd

- Anilox Roll Cleaning Systems

- Shenzhen Riselaser Technology Co. Ltd

- Sukjin Laser Co.

- Allied Scientific Pro

- CyCleanLaser GmbH

- PharosQuartz (Light Conversion)

- Suresh Industech Pvt. Ltd

- RMA Technik GmbH

- Jinan Vmade CNC Machine Co., Ltd

- Shanghai Mactron Technology Co. Ltd

- Lynton Lasers Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Environmental Regulations Replacing Chemical Solvents in EU and North America

- 4.2.2 Rising Automation Demand for Non-contact Surface Preparation in Automotive Body Shops

- 4.2.3 Growth in Restoration Projects of Historical Monuments in Europe and Asia

- 4.2.4 Investments in Nuclear Facility Decommissioning Requiring Remote Laser Decontamination

- 4.2.5 EV Battery Production Lines Necessitating Residue-free Electrode Cleaning

- 4.2.6 Falling Cost-per-Watt of Fiber Lasers Broadening SME Adoption in Asia

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for High-power Systems in Developing Economies

- 4.3.2 Limited Field Portability for Offshore Maintenance

- 4.3.3 Substrate Thermal Damage Risk on Heat-Sensitive Materials

- 4.3.4 Scarcity of Certified Laser Cleaning Technicians in Emerging Markets

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.5.1 Advances in Ultrashort-Pulse (Ps/Fs) Sources

- 4.5.2 Integration with Collaborative Robots

- 4.6 Regulatory Outlook

- 4.6.1 Global VOC and Hazardous-Chemical Directives

- 4.6.2 OSHA and IEC Laser-Safety Standards

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Laser Type

- 5.1.1 Fiber Lasers

- 5.1.2 Solid-state (Nd:YAG/Yb:YAG) Lasers

- 5.1.3 CO2 Lasers

- 5.1.4 Ultrashort-Pulse (Picosecond/Femtosecond) Lasers

- 5.2 By Power Range

- 5.2.1 High Power (Greater than 1 kW)

- 5.2.2 Medium Power (100 W-1 kW)

- 5.2.3 Low Power (Less than 100 W)

- 5.3 By Portability

- 5.3.1 Handheld/Portable Systems

- 5.3.2 Benchtop/Stationary Systems

- 5.3.3 Robotic/Automated Integrated Cells

- 5.4 By Pulse Duration

- 5.4.1 Continuous-Wave

- 5.4.2 Nanosecond Pulsed

- 5.4.3 Ultrashort-Pulse (Ps/Fs)

- 5.5 By Application

- 5.5.1 Paint and Coating Removal

- 5.5.2 Rust and Oxide Removal

- 5.5.3 Surface Pretreatment and Welding Preparation

- 5.5.4 Mold Cleaning and Tooling Maintenance

- 5.5.5 Cultural Heritage and Artwork Restoration

- 5.5.6 Micro-electronics and Precision Cleaning

- 5.5.7 Nuclear Decontamination

- 5.6 By End-user Industry

- 5.6.1 Automotive and Transport

- 5.6.2 Aerospace and Defense

- 5.6.3 Shipbuilding and Marine

- 5.6.4 Infrastructure and Construction

- 5.6.5 Energy and Power

- 5.6.5.1 Oil and Gas

- 5.6.5.2 Nuclear

- 5.6.5.3 Renewables

- 5.6.6 Electronics and Semiconductor

- 5.6.7 Cultural Heritage Institutions

- 5.6.8 Manufacturing and Industrial Machinery

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 South Korea

- 5.7.3.4 India

- 5.7.3.5 South East Asia

- 5.7.3.6 Australia

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 TRUMPF Group

- 6.4.2 IPG Photonics Corporation

- 6.4.3 Clean-Lasersysteme GmbH

- 6.4.4 Laser Photonics Corporation

- 6.4.5 P-Laser NV

- 6.4.6 Laserax Inc.

- 6.4.7 Adapt Laser Systems LLC

- 6.4.8 Jinan Xintian Technology Co. Ltd (XT Laser)

- 6.4.9 HGLaser Engineering Co. Ltd

- 6.4.10 Han's Laser Technology Industry Group Co. Ltd

- 6.4.11 Coherent Corp.

- 6.4.12 Scantech Laser Pvt. Ltd

- 6.4.13 Anilox Roll Cleaning Systems

- 6.4.14 Shenzhen Riselaser Technology Co. Ltd

- 6.4.15 Sukjin Laser Co.

- 6.4.16 Allied Scientific Pro

- 6.4.17 CyCleanLaser GmbH

- 6.4.18 PharosQuartz (Light Conversion)

- 6.4.19 Suresh Industech Pvt. Ltd

- 6.4.20 RMA Technik GmbH

- 6.4.21 Jinan Vmade CNC Machine Co., Ltd

- 6.4.22 Shanghai Mactron Technology Co. Ltd

- 6.4.23 Lynton Lasers Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment