|

市场调查报告书

商品编码

1851160

草坪保护:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Turf Protection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

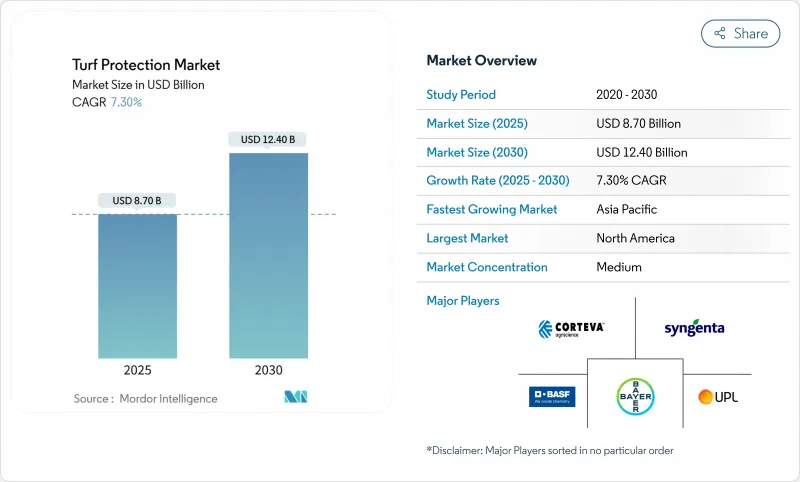

预计到 2025 年,草坪保护市场规模将达到 87 亿美元,到 2030 年将达到 124 亿美元,在此期间的复合年增长率为 7.3%。

这一市场扩张反映了对需要兼具耐用性和美观休閒的运动和休閒场所(例如高尔夫球场、专业体育场馆和豪华住宅区)的投资不断增长。日益加剧的气候变迁、更严格的球员安全标准以及向综合虫害管理方案的转变,都推动了对先进杀菌剂、生物刺激剂和精准施用技术的需求。随着监管机构对合成化学品的严格审查以及业主寻求减少环境足迹,生物製品正经历两位数的增长。在竞争方面,先正达占据最大的市场份额,其次是拜耳作物科学。然而,市场分散化程度日益加剧,导致区域性专业公司在生物刺激剂和精准感测器组件等细分领域占据主导地位。北美凭藉其成熟的体育基础设施和较高的家庭草坪护理支出,保持着主导地位;而亚太地区则经历了最快的增长,都市化和大型设施的建设刺激了需求的增长。

全球草坪保护市场趋势与洞察

高尔夫球场和专业运动设施建设增加

疫情后,新建场馆的资本投资激增,尤其是在印度、中国和海湾国家,这为兼具耐用性和自然运动性能的混合草坪系统创造了稳定的持续需求。职业联赛制定了评估场地品质的正式标准,场馆业主也开始指定使用通过更严格安全测试的杀菌剂、植物生长调节剂和抗逆剂。场馆建成后,需要进行赛季期间的病虫害防治,从而确保供应商的持续收入。市场先驱也开始推出包含种子、营养液和数位化监控的一体化解决方案,这为草坪保护市场开闢了交叉销售机会。

草坪病害发生率增加

冬季气温升高、持续时间延长以及湿度增加加剧了草坪褐斑病和豆斑病的爆发,促使草坪管理人员采用动态轮作方案,以应对病原体实时压力,而不是仅仅遵循固定的施肥计划。研究表明,高氮肥施用量的羊茅草坪褐斑病发病率比中等施肥量的草坪高出40%,凸显了均衡营养策略的重要性。先进的诊断试剂套件和人工智慧模型目前能够以97%的准确率检测出豆斑病,从而实现早期干预和优化杀菌剂施用量。这一趋势正推动草坪保护产业朝向预测分析和针对特异性地点的处理方法发展,以保护有益的土壤微生物。

人工草皮解决方案的快速普及

人工草皮草坪因其无需定期修剪和使用杀虫剂,而受到面临劳动力和水资源短缺的学校董事会和市政当局的青睐。目前,美国每年新增人造草坪安装量在1200至1500个之间。然而,欧洲发现的PFAS污染以及每年约1.6万吨的微塑胶洩漏量,引发了政策审查,这可能会阻碍人造草坪的普及,并促使人们重新关注天然草坪。草坪保护供应商正积极应对,推出混合技术和宣传宣传活动,强调天然草坪系统在健康和永续性方面的益处。

细分市场分析

杀菌剂将占据草坪保护市场收入的最大份额,预计到2024年将达到38.1%,这反映了草坪褐斑病、褐斑病和腐霉病等病害持续存在的威胁。对于希望保持锦标赛级草坪的球场而言,采用包含多种杀菌剂(如SDHI、QoI和DMI)的复杂轮换方案至关重要。然而,生物刺激剂的复合年增长率高达11.5%,凸显了市场正转向具有已证实的抗逆性和根系健康增强作用的永续投入品。除草剂约占需求的31.4%,用于应对一年生早熟禾和阔叶杂草,而植物生长调节剂则透过降低割草机的燃料和人事费用推动了市场成长。

随着劳动力短缺和永续性目标的日益明确,草坪植物生长调节剂市场正在不断扩大。铁基替代品和微生物混合物如今已成为传统杀菌剂的补充,在维持经济效益的同时,也能降低环境风险。生物製药和合成製剂的结合,催生了具有更高吸收性和持久性的复配配方,为草坪管理者提供了更多选择。

到2024年,路面材料的需求将占总整体需求的42.5%,这主要得益于住宅和商业房地产对美观外观的大力投入。产品组合着重于广谱除草剂、缓释性养分和用于打造统一外观的着色剂。相较之下,运动场地材料以9.8%的复合年增长率领先成长榜单,因为各俱乐部和大学都将运动员安全和场地平整度放在首位。美国国家美式足球联盟(NFL)积极推动场地测试标准化,已製定了高性能杀菌剂方案和混合补播草种的采购规范。

高尔夫球场草坪保护的市场规模依然庞大,占比达28.6%,但与体育场馆相比,其增长速度有所放缓,因为许多成熟的高尔夫球场正从扩建转向维修。草皮农场虽然市场定位小众,但其供应的无病虫害草捲(需要进行密集的病虫害防治)正发挥着重要作用。

区域分析

北美地区预计到2024年将保持全球收入的35.0%,这主要得益于该地区超过15,000个高尔夫球场以及全球规模最大的专业体育场馆群之一。美国约占该地区需求的90%,受益于物联网土壤探测和人工智慧喷洒调度工具的早期应用。加拿大生长季较短,夏季是病害爆发的高峰期,因此需要采用高端杀菌剂。墨西哥的度假区将专注于耐盐草坪品种和适合沿海土壤的施肥方案。

亚太地区预计将以8.7%的复合年增长率成为全球成长最快的地区。儘管中国科研机构正在扩充耐逆性草坪草种质资源,但球场业者仍需要进口许多优质品种。印度的城市高尔夫和板球场地对能够应对季风变化的杀菌剂和生长调节剂组合有着强劲的需求。日本成熟的高尔夫产业正在转向精准灌溉和生物製剂,以满足政府的永续性目标。面对严格的用水限制,澳洲球场管理人员越来越依赖润湿剂和耐旱组合药物来保障球场品质。

欧洲仍然是一个技术和监管主导的领域。欧盟委员会正积极推动永续农药使用和微塑胶禁令,奖励生物防治计画和可生物降解载体的应用。德国和英国率先部署互联感测器网络,以精准控制杀菌剂的使用时间。法国地面作业人员率先采用生物刺激剂种子处理技术,以符合国家农药减量目标,显示政策如何影响采购选择。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 高尔夫球场和专业体育场建设增加

- 草坪病害增加

- 居民对美观草坪的需求日益增长

- 转向生物消毒剂和生物刺激剂

- 基于感测器的精准草坪管理

- 缓解气候变迁引起的热应激的解决方案

- 市场限制

- 人工草皮解决方案的快速普及

- 新化学品的研发成本很高

- 对传统杀菌剂的监管压力

- 人们对人工草皮造成的微塑胶和奈米塑胶污染表示担忧

- 技术展望

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 消毒剂

- 除草剂

- 杀虫剂

- 植物生长调节剂

- 生物刺激剂和生物肥料

- 透过使用

- 景观设计

- 高尔夫球场

- 运动的

- 草皮农场

- 最终用户

- 住宅用户

- 商业景观设计师

- 体育设施所有者

- 地方政府和学校

- 透过作用机制

- 化学

- 生物学

- 整合解决方案

- 按剂型

- 颗粒状

- 浓缩液

- 可湿性粉

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Syngenta AG

- Bayer Cropscience AG

- BASF SE

- UPL Limited

- Nufarm Limited

- AMVAC Chemical Corporation

- Sumitomo Group

- Bioceres LLC(Morrone Bio Innovations)

- ICL Group

- FMC Corporation

- Corteva Agriscience

- SePRO Corporation

- Gowan Company, LLC

- Koch Agronomic Services, LLC

- LebanonTurf(Lebanon Seaboard Corporation)

第七章 市场机会与未来展望

The turf protection market size stands at USD 8.7 billion in 2025 and is forecast to reach USD 12.4 billion by 2030, translating into a 7.3% CAGR over the period.

This expansion reflects accelerating investment in golf courses, professional sports venues, and high-end residential landscapes that demand resilient, visually appealing playing and leisure surfaces. Rising climate volatility, tighter player-safety standards, and the shift toward integrated pest-management programs are lifting demand for advanced fungicides, biostimulants, and precision application technologies. Biological products are registering double-digit growth as regulators scrutinize synthetic chemistries and owners look to reduce environmental footprints. On the competitive front, the top five suppliers account for the majority share in global revenue, with Syngenta accounting for the highest share, followed by Bayer CropScience yet fragmentation still enables regional specialists to penetrate niches such as biostimulants and precision-sensor packages. North America sustains leadership due to mature sports infrastructure and high household spending on lawn care, while Asia-Pacific logs the fastest gains as urbanization and mega-facility construction spur incremental demand.

Global Turf Protection Market Trends and Insights

Rising Construction of Golf Courses and Professional Sports Venues

Capital allocations for new facilities surged after the pandemic, particularly across India, China, and Gulf states, creating steady pull-through demand for hybrid turf systems that balance durability with natural playability. Professional leagues have formalized surface-quality metrics, prompting venue owners to specify fungicides, plant growth regulators, and stress-mitigation products that pass stricter safety tests. Once built, each venue requires season-long disease control, anchoring recurring revenue for suppliers. Developers also lean on integrated packages that bundle seed, nutrition, and digital monitoring, opening cross-selling opportunities in the turf protection market.

Increasing Incidence of Turfgrass Disease

Milder winters and prolonged humidity are intensifying outbreaks of dollar spot and brown patch, prompting superintendents to adopt dynamic rotation programs that respond to real-time pathogen pressure instead of calendar schedules. Research shows tall fescue plots receiving high nitrogen suffer 40% higher brown patch severity than moderately fertilized turf, underscoring the need for balanced nutrition strategies. Advanced diagnostic kits and AI models now detect dollar spot with 97% accuracy, enabling earlier interventions and optimized fungicide loads. The trend is pushing the turf protection industry toward predictive analytics and site-specific treatments that preserve beneficial soil organisms.

Rapid Penetration of Artificial Turf Solutions

Synthetic fields eliminate routine mowing and pesticide spending, enticing school boards and municipalities wrestling with labor and water constraints. Installations in the United States now run between 1,200 and 1,500 per year. Nonetheless, PFAS contamination findings and microplastic-shed estimates of 16,000 tons annually in Europe have triggered policy reviews that could stall conversions and breathe life into natural alternatives. Turf protection vendors are responding with hybrid technology and communication campaigns highlighting the health and sustainability benefits of natural systems.

Other drivers and restraints analyzed in the detailed report include:

- Growing Residential Demand for Aesthetic Lawns

- Shift Toward Biological Fungicides and Biostimulants

- Regulatory Pressure on Conventional Fungicides

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fungicides generated the largest slice of turf protection market revenue with a 38.1% share in 2024, reflecting the continual threat of dollar spot, brown patch, and Pythium. Sophisticated rotation plans mixing SDHI, QoI, and DMI chemistry remain indispensable for courses aiming to maintain tournament-grade surfaces. However, biostimulants, posting an 11.5% CAGR, highlight the market's pivot toward sustainable inputs backed by proven stress tolerance and root health gains. Herbicides corner roughly 31.4% of demand as managers tackle annual bluegrass and broadleaf weeds, while plant growth regulators find traction by trimming mower fuel and labor costs.

The turf protection market size for plant growth regulators is poised to expand alongside heightened labor constraints and sustainability targets. Iron-based alternatives and microbial cocktails now supplement conventional fungicides, demonstrating equivalent dollar spot suppression with lower environmental risk. Biologicals and synthetics are spawning co-formulations that enhance uptake and persistence, broadening choice for superintendents.

Landscaping maintained 42.5% of overall demand in 2024, supported by steady residential and commercial spending on curb appeal. Product mixes focus on broad-spectrum weed control, slow-release nutrition, and colorants that deliver a uniform appearance. In contrast, sports fields are heading the growth table at 9.8% CAGR as franchises and universities prioritize athlete safety and surface consistency. The NFL's push for standardized field testing is already shaping purchasing specifications toward high-performance fungicide programs and hybrid overseeding blends.

The turf protection market size dedicated to golf courses remains sizable at 28.6%, but growth plateaus relative to sports arenas as many mature courses transition from capital expansion to renovation mode. Sod farms, while niche, exert influence through their role in supplying disease-free rolls that demand intensive pest shielding.

The Turf Protection Market Report is Segmented by Product Type (Fungicides, Herbicides, and More), Application (Landscaping, Golf Courses, Sports Fields, and More), End-User (Residential Customers, and More), Mode of Action (Chemical, Biological, and Integrated Solution), Formulation (Granular, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Report Offers Forecasts in Terms of Value (USD).

Geography Analysis

North America retained 35.0% of global revenue in 2024, anchored by more than 15,000 golf courses and one of the world's largest portfolios of professional stadiums. The United States represents roughly 90% of regional demand and benefits from the early adoption of IoT soil probes and AI spray scheduling tools. Canada's shorter growing window concentrates disease outbreaks into intense summer peaks, encouraging premium fungicide programs. Mexico's resort corridors channel investment into salt-tolerant turf cultivars and fertility programs that thrive in coastal soils.

Asia-Pacific is projected to clock an 8.7% CAGR, the fastest worldwide. China's research institutes are expanding germplasm collections for stress-resistant turf, but course operators still import many premium cultivars. India's urban golf and cricket infrastructure underpins robust demand for fungicide and growth-regulator packages capable of withstanding monsoon swings. Japan's mature golf scene is pivoting toward precision irrigation and biological inputs to meet government sustainability targets. Australian course managers face stringent water quotas, increasing reliance on wetting agents and drought-resilient blends to safeguard playing quality.

Europe remains a technology- and regulation-driven arena. The European Commission's push for sustainable pesticide use and microplastic bans incentivizes biological programs and biodegradable carriers. Germany and the United Kingdom spearhead the uptake of connected-sensor networks that fine-tune fungicide timing. France's grounds crews are early adopters of biostimulant seed treatments to comply with national pesticide-reduction objectives, showcasing how policy influences procurement choices.

- Syngenta AG

- Bayer Cropscience AG

- BASF SE

- UPL Limited

- Nufarm Limited

- AMVAC Chemical Corporation

- Sumitomo Group

- Bioceres LLC (Morrone Bio Innovations)

- ICL Group

- FMC Corporation

- Corteva Agriscience

- SePRO Corporation

- Gowan Company, L.L.C.

- Koch Agronomic Services, LLC

- LebanonTurf (Lebanon Seaboard Corporation)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising construction of golf courses and professional sports venues

- 4.2.2 Increasing incidence of turfgrass diseases

- 4.2.3 Growing residential demand for aesthetic lawns

- 4.2.4 Shift toward biological fungicides and biostimulants

- 4.2.5 Adoption of sensor-based precision turf management

- 4.2.6 Climate-change-induced heat-stress mitigation solutions

- 4.3 Market Restraints

- 4.3.1 Rapid penetration of artificial turf solutions

- 4.3.2 High Research and Development cost for novel chemistries

- 4.3.3 Regulatory pressure on conventional fungicides

- 4.3.4 Micro- and nanoplastic pollution concerns from turf inputs

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Fungicides

- 5.1.2 Herbicides

- 5.1.3 Insecticides

- 5.1.4 Plant Growth Regulators

- 5.1.5 Biostimulants and Bio-fertilizers

- 5.2 By Application

- 5.2.1 Landscaping

- 5.2.2 Golf Courses

- 5.2.3 Sports Fields

- 5.2.4 Sod Farms

- 5.3 By End-user

- 5.3.1 Residential Customers

- 5.3.2 Commercial Landscape Contractors

- 5.3.3 Sports Facility Owners

- 5.3.4 Municipalities and Schools

- 5.4 By Mode of Action

- 5.4.1 Chemical

- 5.4.2 Biological

- 5.4.3 Integrated Solutions

- 5.5 By Formulation

- 5.5.1 Granular

- 5.5.2 Liquid Concentrate

- 5.5.3 Wettable Powder

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of the North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Syngenta AG

- 6.4.2 Bayer Cropscience AG

- 6.4.3 BASF SE

- 6.4.4 UPL Limited

- 6.4.5 Nufarm Limited

- 6.4.6 AMVAC Chemical Corporation

- 6.4.7 Sumitomo Group

- 6.4.8 Bioceres LLC (Morrone Bio Innovations)

- 6.4.9 ICL Group

- 6.4.10 FMC Corporation

- 6.4.11 Corteva Agriscience

- 6.4.12 SePRO Corporation

- 6.4.13 Gowan Company, L.L.C.

- 6.4.14 Koch Agronomic Services, LLC

- 6.4.15 LebanonTurf (Lebanon Seaboard Corporation)