|

市场调查报告书

商品编码

1851232

巨量资料即服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Big Data As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

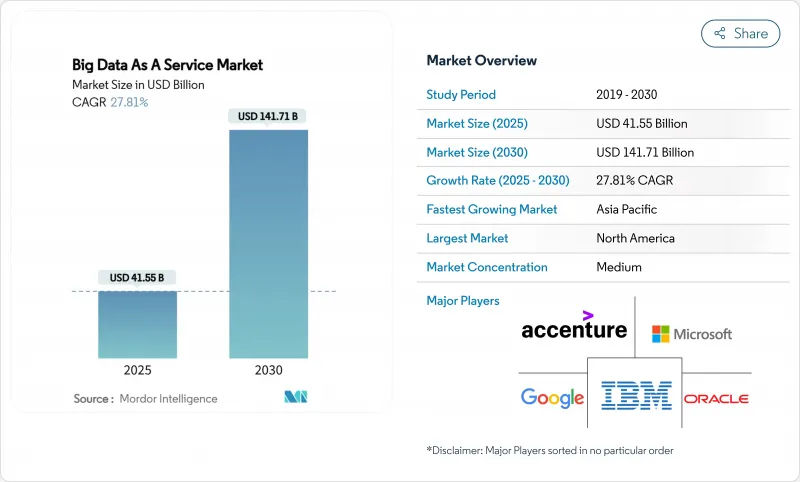

据估计,巨量资料即服务市场规模在 2025 年将达到 415.5 亿美元,预计到 2030 年将达到 1,417.1 亿美元,在预测期(2025-2030 年)内复合年增长率为 27.81%。

预计2025年,巨量资料即服务)市场规模将达到415.5亿美元,2030年将达到1,417.1亿美元,复合年增长率(CAGR)为27.81%。随着企业以基于使用量的云端分析取代资本密集的本地部署系统,并灵活支援人工智慧工作负载,市场需求将持续成长。生成式人工智慧试点计画的激增、工业IoT部署的不断增长以及全球向计量收费的转变,使得大数据即服务的应用门槛正在降低。因此,超大规模资料中心供应商每年投资超过1,050亿美元用于新增容量,以满足其弹性资料处理需求。儘管北美仍保持领先地位,但亚太地区正展现出最强劲的成长势头,这主要得益于製造商和金融机构加速云端迁移。这些因素共同支撑着巨量资料即服务市场在未来十年保持强劲的发展前景。

全球巨量资料即服务市场趋势与洞察

云端采用和数据爆炸

像3M这样的製造商透过在其生产线上部署Azure SQL Edge,将异常检测时间缩短了40%,从而展现了弹性处理在营运方面的显着优势。到2025年,全球年度云端支出将超过8,250亿美元,其中85%的公司将使用多重云端环境来支援分析计划。维护本地Hadoop丛集每年可能需要花费200万至500万美元,而基于使用量的BDaaS(业务资料即服务)则可以根据工作负载的规模进行紧密扩展。在网路边缘,物联网感测器产生的资料量超过了传统管道的处理能力,迫使企业采用分散式架构,在更靠近资料来源的位置执行运算,同时与云端分析平台同步。

生成式人工智慧分析的需求

如今,大规模语言模型与 SQL 引擎一起,已成为大多数企业发展蓝图上的标配。银行机构估计,GenAI 全面运作后,每年将创造 2,000 亿至 3,400 亿美元的新收入,从而推动对非结构化资料处理业务即服务 (BDaaS) 的大规模投资。 Snowflake 预计,人工智慧工作负载将占其 2024 财年 26.7 亿美元收入的 38%,并正与 Anthropic、NVIDIA 和微软合作,将人工智慧训练直接嵌入其资料云中。 AWS 已报告数十亿美元的人工智慧运转率,凸显了其在单一租户中摄取、转换数据并将其交付给机器学习管道的平台发展势头强劲。 GenAI 与搜寻结合,将进一步实现企业文件的商业化,并从閒置的内容库中创造新的收入来源。

资料隐私与网路安全风险

75% 的国家强制要求在地化,导致云端架构碎片化,营运成本上升。诸如 GDPR、中国的云端服务法 (CSL) 和美国的《云端法案》等相互重迭的法规迫使跨国公司建构复杂的资料管治层,使整体拥有成本增加高达 25%。金融机构还必须将交易资料储存在境内,这限制了供应商的选择,并延长了采购週期。虽然这些障碍在某些情况下会减缓迁移速度,但很少是可逆的。服务提供者越来越多地提供合约条款来应对区域集群和法律差异,这可以缓解(但无法消除)这些不利因素。

细分市场分析

到2024年,Hadoop即服务(Hadoop-as-a-Service)将占据巨量资料即服务)市场42%的份额,这表明批次和资料湖架构对现有企业仍然具有价值。然而,分析即服务(Analytics-as-a-Service)预计将以30.61%的复合年增长率(CAGR)成为成长最快的产品,因为企业正在采用整合BI仪表板、机器学习笔记本和向量搜寻且无需丛集维护的託管环境。预计到2025年,分析领域的支出成长将占总支出成长的50%,并在2030年之前保持领先地位。资料平台即服务(Data Platform-as-a-Service)介于原始基础设施和端到端分析套件之间,在需要客製化管治控制的监管场景中仍然至关重要。

客户越来越倾向于以分析所需时间而非硬体利用率来衡量成功。 Snowflake 推出的 Cortex AISQL 预示着未来分析师可以使用自然语言查询生命週期管理 (LLM),并从储存事务资料的相同介面获得受管治的答案。这种融合模糊了 ETL、资料仓储和分析之间的传统界限,迫使供应商整合各项功能。因此,在预测期内,巨量资料即服务)市场将从以基础设施为先的品牌定位转向强调提案支援的即时。

受超大规模云端服务商定价策略的推动,公共云端将在2024年占据63%的收入份额,而混合云端将以29.51%的复合年增长率实现最快增长。企业希望能够灵活地将敏感记录保存在私人区域,同时在需求高峰期将分析任务扩展到公共边缘。混合云方案还能降低厂商锁定风险,并支持合规性,因为75%的司法管辖区都对资料居住规则有明确规定。因此,预计从2025年到2030年,混合云解决方案的巨量资料即服务将成长三倍以上。

多重云端架构如今已成为主流,85% 的公司至少使用两家云端服务供应商来经营巨量资料业务。 Snowflake 最近已与 AWS、Azure 和 Google Cloud 上的 Apache Iceberg 檔案进行了整合。在配备物联网闸道器的工厂中,混合部署方案会在本地硬体上处理异常评分,然后将聚合结果传输送到云端模型进行历史趋势分析。诸如此类的模式将使混合部署成为下一代分析的基石。

巨量资料即服务市场报告按服务模式(Hadoop 即服务 (HaaS)、分析即服务 (AaaS) 等)、部署方式(公共云端、私有云端等)、最终用户行业垂直领域(银行、金融服务和保险、製造业、IT 和通讯等)以及地区进行细分。

区域分析

到2024年,北美将占据巨量资料即服务市场39%的份额,这主要得益于根深蒂固的云端服务供应商、资金筹措以及数据主导的商业文化。美国和加拿大的公司是早期采用者,目前正致力于改善财务营运(FinOps)实践,以应对不断上涨的人工智慧运算成本。欧洲则受到GDPR强制规定的驱动,倾向于能够保证可审核的託管服务。儘管隐私法规严格,但该地区仍维持着15%左右的成长率。

亚太地区引领潮流,预计将以27.85%的复合年增长率成长。中国、印度和东南亚各国政府都在支持国家云端计划,製造业的数位化也为业务数据即服务(BDaaS)管道注入了新的数据。阿里云和腾讯云等本土超大规模云端服务供应商正在投资跨区域可用区,消除以往依赖全球云端服务供应商所带来的延迟损失。作为物联网的早期采用者,日本和韩国目前正在尝试基于区域资料保护框架建构的企业级全人工智慧(GenAI)。

拉丁美洲和中东及非洲地区虽然起步较早,但已展现出令人瞩目的绝对成长动能。巴西的金融科技公司和墨西哥的零售商正在将工作负载转移到大数据即服务(BDaaS)平台,因为他们的资本预算无法支援大型自架丛集。墨西哥湾沿岸的石油公司正在钻机上运作混合型BDaaS边缘节点,用于预测性维护;非洲的电信业者则利用按需付费模式,无需前期资本投入即可推出客户分析专案。这些新兴市场正在推动巨量资料即服务市场的收入成长,从而扩大其全球影响力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要主要发现

第四章 市场情势

- 市场概览

- 市场驱动因素

- 云端采用和数据爆炸

- 比本地部署巨量资料堆迭更具成本效益的替代方案

- 生成式人工智慧分析的需求

- 面向物联网密集型垂直产业的边缘到云端资料架构

- 资料本地化规则旨在促进 BDaaS 中的区域节点发展

- 与财务营运相关的消费定价模式

- 市场限制

- 资料隐私与网路安全风险

- 遗留系统整合复杂性

- 仔细审视超大规模资料中心的碳足迹

- 财务营运与数据工程人才缺口

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按服务模式

- Hadoop-as-a-Service(HaaS)

- 分析即服务 (AaaS)

- 数据平台即服务 (DPaaS)

- 透过部署

- 公有云

- 私有云端

- 混合云

- 按最终用户行业划分

- BFSI

- 资讯科技和电讯

- 医疗保健和生命科学

- 零售与电子商务

- 製造业

- 能源与电力

- 政府和公共部门

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services

- Microsoft

- Google Cloud

- IBM

- Oracle

- SAP

- Hewlett Packard Enterprise

- SAS Institute

- Accenture

- Teradata

- Cloudera

- Snowflake

- Databricks

- Dell Technologies

- Splunk

- Palantir

- Informatica

- Huawei Cloud

- Alibaba Cloud

- Tencent Cloud

- Wipro

第七章 市场机会与未来展望

The Big Data As A Service Market size is estimated at USD 41.55 billion in 2025, and is expected to reach USD 141.71 billion by 2030, at a CAGR of 27.81% during the forecast period (2025-2030).

The big data as a service market reached USD 41.55 billion in 2025 and is forecast to climb to USD 141.71 billion by 2030, reflecting a compound annual growth rate of 27.81%. Demand escalates as enterprises replace capital-intensive on-premises systems with usage-based cloud analytics that flex with artificial-intelligence workloads. A surge in generative-AI pilots, wider industrial IoT rollouts, and a global shift toward pay-as-you-go pricing have narrowed adoption barriers. Hyperscale providers have therefore invested more than USD 105 billion each year in new capacity to meet elastic data-processing needs. North America retains leadership, yet Asia-Pacific shows the steepest trajectory as manufacturers and financial institutions accelerate cloud migrations. Together, these forces uphold a strong outlook for the big data as a service market through the decade.

Global Big Data As A Service Market Trends and Insights

Cloud Adoption and Exploding Data Volumes

Organizations now generate 2.5 quintillion bytes each day, volumes that exceed the practical limits of on-premises clusters.Manufacturers such as 3M cut anomaly-detection time by 40% after installing Azure SQL Edge on production lines, showing the operational impact of elastic processing. Annual global cloud spending topped USD 825 billion in 2025, and 85% of enterprises use multi-cloud environments to support analytics projects. Savings are evident: maintaining local Hadoop farms can cost USD 2-5 million per year, while usage-based BDaaS scales strictly with workload size. At the network edge, IoT sensors produce more data than traditional pipes can carry, forcing firms to adopt distributed architectures that keep compute near the source while synchronizing to cloud analytics platforms.

Generative-AI-Ready Analytics Demand

Large language models now sit beside SQL engines in most enterprise road maps. Banking institutions estimate USD 200-340 billion in new annual profit once GenAI is fully operational, driving heavy BDaaS investments for unstructured-data processing. Snowflake attributes 38% of its USD 2.67 billion fiscal-2024 revenue to AI workloads and has partnered with Anthropic, NVIDIA, and Microsoft to embed AI training directly in its data cloud. AWS already reports multi-billion-dollar AI run rates, underscoring the momentum toward platforms that can ingest, transform and serve data to ML pipelines in a single tenancy. Retrieval-augmented generation further monetizes enterprise documents, creating new revenue streams from dormant content libraries.

Data Privacy and Cybersecurity Risks

Seventy-five percent of countries enforce localization mandates that fragment cloud architectures and inflate operating expenses. Overlapping rules from GDPR, China's CSL and the US CLOUD Act force multinational firms to build complex data-governance layers, lifting total ownership cost by up to 25%. Financial institutions must further store transactional data onshore, restricting vendor options and raising procurement cycles. These hurdles slow some migrations but rarely reverse them; providers increasingly offer region-specific clusters and contract clauses that address legal variance, tempering the headwind but not eliminating it.

Other drivers and restraints analyzed in the detailed report include:

- Edge-to-Cloud Data Fabrics for IoT-Rich Verticals

- FinOps-Linked Consumption Pricing Models

- Talent Gap in FinOps and Data Engineering

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hadoop-as-a-Service retained 42% of the big data as a service market in 2024, indicating that batch processing and data-lake architectures still hold value for established enterprises. However, Analytics-as-a-Service is forecast to grow at 30.61% CAGR, the quickest pace among offerings, as firms favor managed environments that merge BI dashboards, ML notebooks and vector search without cluster maintenance. In 2025, the analytics segment captured 50% share of the big data as a service market size for incremental spending and is projected to widen its lead through 2030. Data Platform-as-a-Service remains relevant in regulated scenarios that need custom governance controls, occupying a middle ground between raw infrastructure and end-to-end analytics suites.

Clients increasingly measure success by time-to-insight rather than hardware utilization. Snowflake's launch of Cortex AISQL signals a future where an analyst can query LLMs with plain language and receive governed answers from the same pane of glass that stores transactional data. This convergence blurs the historical divide between ETL, warehousing and analytics, pushing vendors to consolidate features. Over the forecast period, the big data as a service market will therefore pivot from infrastructure-first branding to value propositions built around immediacy of decision support.

Public cloud commanded 63% of revenue in 2024, driven by hyperscaler pricing, but hybrid cloud will rise fastest at 29.51% CAGR. Organizations seek the flexibility to keep sensitive records in private zones while bursting analytics to the public edge during demand spikes. Hybrid options also mitigate vendor lock-in and support compliance when 75% of jurisdictions impose data-residency rules. As a result, the big data as a service market size for hybrid solutions is projected to more than triple between 2025 and 2030.

Multi-cloud architectures are now mainstream: 85% of enterprises employ at least two providers for big-data tasks. Snowflake's recent integration with Apache Iceberg files across AWS, Azure and Google Cloud enables identical queries on any venue, encouraging workload portability. For plants with IoT gateways, hybrid layouts process anomaly scores on local hardware, then forward aggregates to cloud models for historical trend building. Such patterns will entrench hybrid deployments as the backbone of next-generation analytics.

The Big Data As A Service Market Report is Segmented by Service Model (Hadoop-As-A-Service (HaaS), Analytics-As-A-Service (AaaS), and More), Deployment (Public Cloud, Private Cloud, and More), End User Industry (BFSI, Manufacturing, IT and Telecom, and More), and Geography.

Geography Analysis

North America controlled 39% of the big data as a service market in 2024, buoyed by entrenched cloud providers, venture funding and data-driven business cultures. Enterprises in the United States and Canada were early adopters and now focus on refining FinOps practices to tame runaway AI compute bills. Europe follows, propelled by GDPR obligations that favor managed services able to guarantee auditability. Despite stringent privacy rules, the region still grows in mid-teens percentages because providers certify regional clusters and encryption-key sovereignty.

Asia-Pacific is the pacesetter, projected to expand at a 27.85% CAGR. Governments in China, India and Southeast Asia champion national cloud programs while manufacturing digitalization piles new data into BDaaS pipelines. Local hyperscalers such as Alibaba Cloud and Tencent Cloud invest in cross-regional availability zones, removing latency penalties once tied to global providers. Japan and South Korea, early IoT adopters, now experiment with enterprise-grade GenAI built on regional data guardianship frameworks.

Latin America and the Middle East and Africa are earlier in the curve yet show promising absolute growth. Brazilian fintech firms and Mexican retailers shift workloads to BDaaS because capital budgets cannot support large self-hosted clusters. Gulf oil producers run hybrid BDaaS edge nodes on rigs for predictive maintenance, while African telecoms leverage consumption pricing to launch customer-analytics programs without front-loading capital. Collectively, these emerging markets contribute incremental revenue that broadens the global footprint of the big data as a service market.

- Amazon Web Services

- Microsoft

- Google Cloud

- IBM

- Oracle

- SAP

- Hewlett Packard Enterprise

- SAS Institute

- Accenture

- Teradata

- Cloudera

- Snowflake

- Databricks

- Dell Technologies

- Splunk

- Palantir

- Informatica

- Huawei Cloud

- Alibaba Cloud

- Tencent Cloud

- Wipro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud adoption and exploding data volumes

- 4.2.2 Cost-effective alternatives to on-prem big-data stacks

- 4.2.3 Generative-AI-ready analytics demand

- 4.2.4 Edge-to-cloud data fabrics for IoT-rich verticals

- 4.2.5 Data-localization rules fueling regional BDaaS nodes

- 4.2.6 FinOps-linked consumption pricing models

- 4.3 Market Restraints

- 4.3.1 Data privacy and cybersecurity risks

- 4.3.2 Legacy integration complexity

- 4.3.3 Carbon-footprint scrutiny on hyperscale DCs

- 4.3.4 Talent gap in FinOps and data engineering

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Model

- 5.1.1 Hadoop-as-a-Service (HaaS)

- 5.1.2 Analytics-as-a-Service (AaaS)

- 5.1.3 Data Platform-as-a-Service (DPaaS)

- 5.2 By Deployment

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By End User Industry

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Retail and E-commerce

- 5.3.5 Manufacturing

- 5.3.6 Energy and Power

- 5.3.7 Government and Public Sector

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 ASEAN

- 5.4.4.6 Rest of Asia Pacific

- 5.4.5 Middle East

- 5.4.5.1 GCC

- 5.4.5.2 Turkey

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Microsoft

- 6.4.3 Google Cloud

- 6.4.4 IBM

- 6.4.5 Oracle

- 6.4.6 SAP

- 6.4.7 Hewlett Packard Enterprise

- 6.4.8 SAS Institute

- 6.4.9 Accenture

- 6.4.10 Teradata

- 6.4.11 Cloudera

- 6.4.12 Snowflake

- 6.4.13 Databricks

- 6.4.14 Dell Technologies

- 6.4.15 Splunk

- 6.4.16 Palantir

- 6.4.17 Informatica

- 6.4.18 Huawei Cloud

- 6.4.19 Alibaba Cloud

- 6.4.20 Tencent Cloud

- 6.4.21 Wipro

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

巨量资料即服务市场:依服务类型、部署模式、组织规模及产业划分-2026年至2032年全球预测

巨量资料即服务市场:依服务类型、部署模式、组织规模及产业划分-2026年至2032年全球预测 2026年全球巨量资料软体即服务市场报告巨量资料即服务 (BDaaS) 全球市场报告 2026

2026年全球巨量资料软体即服务市场报告巨量资料即服务 (BDaaS) 全球市场报告 2026 BDaaS市场分析及至2035年预测:依类型、产品、服务、技术、组件、应用、部署、最终用户及解决方案划分巨量资料即服务 (BDaaS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

BDaaS市场分析及至2035年预测:依类型、产品、服务、技术、组件、应用、部署、最终用户及解决方案划分巨量资料即服务 (BDaaS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 大数据即服务 (BDaaS) 市场规模、份额、趋势和预测(按解决方案、部署模式、平台类型、组织规模、垂直行业和地区划分),2026-2034 年

大数据即服务 (BDaaS) 市场规模、份额、趋势和预测(按解决方案、部署模式、平台类型、组织规模、垂直行业和地区划分),2026-2034 年 巨量资料即服务市场-全球产业规模、份额、趋势、机会、预测(依解决方案类型、部署模式、组织规模、产业垂直领域、地区和竞争格局划分,2021-2031)

巨量资料即服务市场-全球产业规模、份额、趋势、机会、预测(依解决方案类型、部署模式、组织规模、产业垂直领域、地区和竞争格局划分,2021-2031) 巨量资料即服务(BaaS) 市场规模、份额和成长分析(按组件、组织规模、部署类型、垂直产业和地区划分)-2026-2033 年产业预测

巨量资料即服务(BaaS) 市场规模、份额和成长分析(按组件、组织规模、部署类型、垂直产业和地区划分)-2026-2033 年产业预测 2025-2029 年全球大数据即服务 (BDaaS) 市场

2025-2029 年全球大数据即服务 (BDaaS) 市场 大数据即服务 (BDaaS) 市场:预测(2025-2030 年)

大数据即服务 (BDaaS) 市场:预测(2025-2030 年)