|

市场调查报告书

商品编码

1851253

柠檬酸:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)Citric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

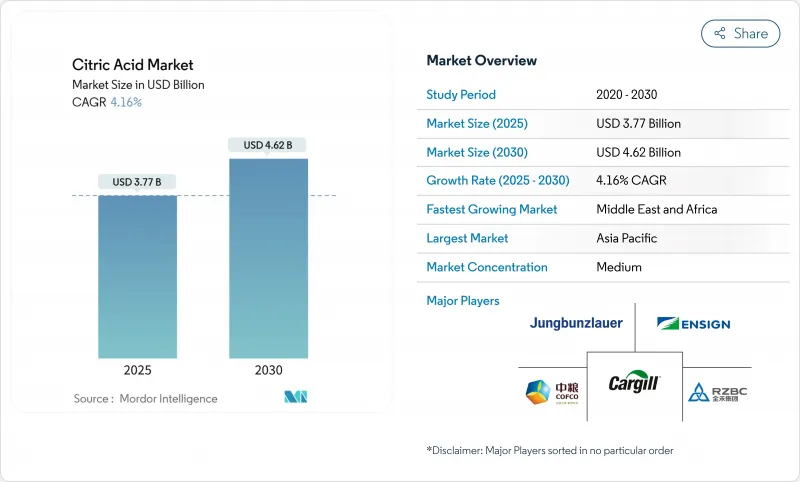

预计到 2025 年,柠檬酸市场规模将达到 37.7 亿美元,到 2030 年将成长至 46.2 亿美元,复合年增长率高达 4.16%。

消费者对洁净标示产品的偏好日益增长、生物技术工艺的进步以及柠檬酸在食品饮料、製药和清洁产品等行业的应用日益多元化,是推动市场成长的主要因素。监管政策的进一步明确,包括美国授予的GRAS认证和欧盟的量子饱和度核准,持续降低市场进入门槛,促进市场准入并鼓励新参与企业。然而,对中国进口产品征收反倾销税正在重塑全球筹资策略,并促使製造商将产能转移到中国以外地区,以降低供应链风险。此外,供应链的垂直整合以及节能发酵技术的创新正在提高生产效率和成本效益。便利饮料、可生物降解清洁液、发泡药品和其他新兴应用领域对柠檬酸的需求不断增长,进一步拓宽了市场范围。这些因素支撑着柠檬酸市场的成长潜力及其适应不断变化的监管、技术和消费者主导趋势的能力。

全球柠檬酸市场趋势与洞察

消费者越来越倾向于在碳酸饮料中使用天然酸味剂

随着饮料业转向天然酸味剂,柠檬酸的需求量激增,这主要得益于洁净标示产品的推广。柠檬酸已在巴西获得批准,成为食品添加剂,相关法规为211/2023号规范。该法规规定了饮料中柠檬酸的典型添加量,介于0.1%至0.3%之间,为生产商提供了亟需的指南。这项明确的监管规定不仅消除了配方的不确定性,也使品牌能够宣称其产品具有天然防腐剂的功效。此举与消费者日益增长的对成分透明度和简化的期望相契合。柠檬酸的重要性不仅限于其作为天然酸味剂的主要作用。它还具有pH调节剂和防腐剂的功能,使生产商能够在简化成分配方的同时提高产品稳定性。这项策略与产业遵守监管标准并满足消费者对洁净标示产品需求的整体目标一致。此外,领先的饮料生产商目前倾向于使用药用级柠檬酸,这凸显了品质稳定性和市场合规性的重要性。对经过认证的高品质柠檬酸日益增长的需求,不仅为经过认证的供应商提供了溢价,而且还激发了市场上的竞争和创新精神。

即饮饮料对柠檬酸的需求不断成长

即饮饮料市场正经历强劲成长,显着推动了柠檬酸在各种应用领域的需求。柠檬酸因其多功能特性而成为关键成分,这些特性包括增强风味、稳定色泽和延长保质期,对于保持产品品质和吸引力至关重要。新兴市场的都市化进程加速了便利消费习惯的普及,为即饮饮料创造了巨大的成长机会。柠檬酸作为一种保色剂,在果味饮料中尤其重要,因为它直接影响视觉吸引力、消费者偏好以及在竞争激烈的市场中实现品牌差异化。此外,发酵技术的进步彻底改变了生产能力。製造商目前采用工程改造的黑曲菌株,使柠檬酸浓度超过174 g/L。这些技术创新提高了生产效率,降低了营运成本,并增强了供应链的可靠性。因此,供应商能够更好地满足不断增长的需求,同时保持价格竞争力,从而促进市场扩张,尤其是在对价格敏感的新兴细分市场。

新兴国家原物料价格波动

原料成本的波动给整个柠檬酸供应链带来了巨大的利润压力,尤其是玉米、甘蔗糖蜜和其他碳水化合物等发酵基材。这种波动在新兴市场尤其显着,因为这些地区的农产品价格极易受到外部因素的影响,例如难以预测的天气、政策改革、地缘政治紧张局势和基础设施不足。除了投入成本上涨之外,製造商还面临外汇波动和物流成本上升的挑战,这进一步加剧了成本管理的复杂性,并迫使他们采用复杂的避险策略。然而,基材利用技术的进步为缓解这些挑战提供了一个有希望的途径。近期研究表明,利用甘蔗渣、乳清和其他产品流等农业废弃物成功生产柠檬酸是可行的。这些技术创新提供了经济高效且环境友善的替代方案,不仅可以减少对大宗商品市场的依赖,而且符合永续性目标,并增强柠檬酸供应链的韧性。

细分市场分析

无水柠檬酸在2024年仍占据市场主导地位,市占率高达55.35%。这主要归功于其优异的稳定性、较长的保质期以及完善的供应链体系,使其能够满足多种终端用途的需求。其晶体结构确保了品质的稳定性,使其成为食品和製药生产商的热门选择。工业应用也青睐无水柠檬酸,因为它溶解速率可预测,并且在製剂过程中不易受水分影响。然而,随着加工效率日益重要,市场格局逐渐转变。例如,荣邦茨劳尔(Jungbunzlauer)的CITROCOAT N等可直接压片的柠檬酸产品,在製药片剂生产领域越来越受欢迎。这些产品透过提高片剂硬度、缩短加工时间以及改善特定应用中的性能,满足了行业需求。

液态柠檬酸製剂市场正经历强劲成长,预计到2030年将以6.82%的复合年增长率成长。这一成长主要得益于製造商日益重视营运效率和成本优化。液态製剂无需溶解步骤,可在自动化生产系统中实现精确的剂量控制,从而简化生产流程。这一趋势在饮料行业尤其明显,液态柠檬酸可无缝整合到糖浆製备过程中,降低粉末处理带来的污染风险。此外,储存和运输技术的进步也缓解了传统的稳定性问题,使液态柠檬酸更具可行性。这些进步推动了液态柠檬酸在以往以无水柠檬酸为主的应用领域中广泛应用,并在整个预测期内保持持续成长。

柠檬酸市场报告按形态(无水和液体)、应用领域(食品饮料、医药、个人护理和化妆品及其他)、等级(医药级、食品级、工业级)以及地区(北美、南美、欧洲、亚太、中东和非洲)对行业进行分类。各细分市场的市场规模及预测均以美元计价。

区域分析

到2024年,亚太地区的市占率将达到37.74%,这主要得益于中国强大的生产能力以及食品加工和工业领域国内需求的激增。该地区的优势包括完善的发酵基础设施、具有竞争力的生产成本以及便捷获取玉米和甘蔗等关键原料。然而,贸易摩擦和反倾销措施正在改变该地区的格局。印度、泰国和其他东南亚国家正在扩大产能,以满足国内和出口需求。日本先进的製药和食品加工业提供了良好的市场前景,而澳洲快速成长的食品饮料产业也将促进区域消费。

中东和非洲地区值得关注,预计到2030年将以7.43%的复合年增长率成长。这一增长主要得益于沙乌地阿拉伯和阿联酋等国蓬勃发展的食品加工业和基础设施投资。该地区各国政府为加强粮食安全和实现产业多元化所采取的倡议,正在为柠檬酸创造新的需求中心。 NEOM与Liberation Labs合作建立精密发酵设施,凸显了该地区在先进生物製造领域的雄心。同时,北美和欧洲凭藉其成熟的食品和製药行业,提供了稳定的需求,但市场饱和和监管不一致限制了其成长速度。

欧洲凭藉在食品、饮料和个人护理领域的强劲需求,以及严格的品质标准和完善的加工设施,保持着稳固的市场地位。北美市场正经历稳定成长,这主要得益于即饮饮料、方便食品和药品产业的快速扩张。该地区的消费者将柠檬酸用作天然防腐剂和增味剂,并且越来越倾向于选择洁净标示的配料。南美洲,尤其是巴西和阿根廷等国家,由于食品加工业的扩张和消费者对包装食品日益增长的偏好,也实现了成长。南美洲的生产商拥有丰富的柠檬酸生产原料,为其提供了双重优势,降低了对进口的依赖。欧洲、北美和南美洲有利于天然添加剂的法律规范进一步提升了柠檬酸的市场潜力,为全球巨头和本土企业都创造了机会。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 消费者越来越倾向于在碳酸饮料中使用天然酸味剂

- 即饮饮料对柠檬酸的需求不断成长

- 发泡药物的使用日益增多

- 加强对工业清洁剂中可生物降解螯合剂的监管

- 糖果甜点中减少糖分的需求日益增长

- 生产流程创新可提高产量比率并降低成本。

- 市场限制

- 新兴国家原物料价格波动

- 提高对中国柠檬酸的反倾销税

- 来自其他酸味剂的竞争。

- 季节性变化影响柑橘类水果的供应。

- 供应链分析

- 监理展望

- 波特五力模型

- 新进入者的威胁

- 买方/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按形式

- 无水

- 液体

- 透过使用

- 饮食

- 麵包店

- 糖果甜点

- 乳製品

- 饮料

- 咸味小吃

- 其他食品和饮料

- 製药

- 个人护理和化妆品

- 清洁剂和家用清洁剂

- 其他的

- 饮食

- 按年级

- 医药级

- 食品级

- 工业级

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 智利

- 秘鲁

- 其他南美洲

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 荷兰

- 波兰

- 比利时

- 瑞典

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 印尼

- 韩国

- 泰国

- 新加坡

- 亚太其他地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 摩洛哥

- 土耳其

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市场排名分析

- 公司简介

- Shandong Ensign Industry Co., Ltd.

- Jungbunzlauer Suisse AG

- COFCO Corporation

- RZBC Group Co., Ltd.

- TTCA Co., Ltd.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Gadot Biochemical Industries Ltd.

- Foodchem International Corporation

- Merck KGaA

- Hawkins, Inc.

- Citrique Belge NV

- BBCA Group(Anhui BBCA)

- FUSO Chemical Co., Ltd.

- Wang Pharmaceuticals and Chemicals

- Hemadri Chemicals

- Vinipul Inorganics India Pvt. Ltd

- Arihant Chemicals

- Anmol Chemicals Private Limited

- Innova Corporate

第七章 市场机会与未来展望

The Citric Acid market size is anticipated to be USD 3.77 billion in 2025, and is projected to grow to USD 4.62 billion by 2030, registering a steady CAGR of 4.16%.

The rising consumer preference for clean-label products, advancements in biotechnology processes, and the increasing diversification of applications across industries such as food and beverages, pharmaceuticals, and cleaning products primarily drive this growth. Regulatory clarity, including the GRAS status in the United States and quantum satis approval in the European Union, continues to lower entry barriers, fostering market accessibility and encouraging participation from new players. However, the imposition of anti-dumping duties on Chinese imports is reshaping global sourcing strategies, prompting manufacturers to expand production capacities in regions outside China to mitigate supply chain risks. Additionally, vertical integration across the supply chain and innovations in energy-efficient fermentation technologies are improving production efficiency and cost-effectiveness. The growing demand for citric acid in convenience beverages, biodegradable cleaning solutions, effervescent pharmaceuticals, and other emerging applications is further broadening its market scope. These factors collectively underscore the market's strong growth potential and its ability to adapt to evolving regulatory, technological, and consumer-driven trends.

Global Citric Acid Market Trends and Insights

Growing Consumer Shift to Natural Acidulants in Carbonated Soft Drinks

As the beverage industry pivots towards natural acidulants, citric acid is witnessing a surge in demand, largely fueled by a commitment to clean-label product reformulations. In Brazil, regulatory shifts have bolstered this momentum, with citric acid receiving the green light as an additive under Normative Instruction 211/2023. This regulation delineates typical dosages for beverages, set between 0.1% and 0.3%, offering manufacturers much-needed guidance. Such regulatory clarity not only dispels formulation uncertainties but also empowers brands to flaunt their natural preservation credentials. This move resonates with a growing consumer appetite for transparency and simplicity in ingredient lists. Citric acid's significance transcends its primary role as a natural acidulant. Its added functions as a pH regulator and preservative allow manufacturers to enhance product stability while streamlining ingredient formulations. This strategy dovetails with the industry's overarching objectives: adhering to regulatory benchmarks and aligning with consumer demands for clean-label offerings. Moreover, top-tier beverage manufacturers are now gravitating towards pharmaceutical-grade citric acid, underscoring the importance of consistent quality and market compliance. This heightened demand for certified, high-quality citric acid not only paves the way for premium pricing for certified suppliers but also ignites a spirit of competition and innovation in the market.

Increasing Demand for Citric Acid in Ready-to-drink Beverages

The ready-to-drink beverage market is experiencing robust growth, significantly driving the demand for citric acid across various applications. Citric acid is a key ingredient due to its multifunctional properties, including flavor enhancement, color stabilization, and shelf-life extension, which are critical for maintaining product quality and appeal. The increasing urbanization in emerging markets has accelerated the adoption of convenience-driven consumption habits, creating substantial growth opportunities for ready-to-drink beverages. In fruit-based beverages, citric acid's role as a color retention agent is particularly vital, as it directly influences visual appeal, consumer preferences, and brand differentiation in a competitive market. Additionally, advancements in fermentation technology have transformed production capabilities. Manufacturers are now employing engineered Aspergillus niger strains, achieving citric acid titers exceeding 174 g/L, a significant improvement over traditional methods. These innovations have enhanced production efficiency, reduced operational costs, and improved supply chain reliability. As a result, suppliers are well-positioned to meet the rising demand while maintaining competitive pricing, fostering market expansion, particularly in price-sensitive and emerging segments.

Price Volatility of Raw Materials in Emerging Countries

Fluctuations in raw material costs are exerting considerable margin pressures across the citric acid supply chain, with fermentation substrates such as corn, sugarcane molasses, and other carbohydrate sources being particularly impacted. This volatility is most evident in emerging markets, where agricultural commodity prices are highly susceptible to external factors, including unpredictable weather conditions, policy reforms, geopolitical tensions, and infrastructure deficiencies. Beyond the rising input costs, manufacturers are also grappling with currency fluctuations and increasing logistics expenses, which further complicate cost management and necessitate the adoption of sophisticated hedging strategies. However, advancements in substrate utilization technologies are providing a promising avenue for mitigation. Recent research highlights the successful production of citric acid from agricultural waste streams, such as sugarcane bagasse, cheese whey, and other by-products. These innovations not only reduce dependence on primary commodity markets but also align with sustainability goals, offering a cost-effective and environmentally friendly alternative that strengthens the resilience of the citric acid supply chain.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption in Effervescent Pharmaceuticals

- Rise in Regulatory Push for Biodegradable Chelating Agents in Industrial Cleaners

- Rise in Anti-dumping Duties on Chinese Citric Acid

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, anhydrous citric acid continues to dominate the market with a 55.35% share, attributed to its superior stability, extended shelf life, and well-established supply chain infrastructure supporting diverse end-use applications. Its crystalline structure ensures consistent quality, making it a preferred choice for food manufacturers and pharmaceutical companies. Industrial applications also favor anhydrous forms due to their predictable dissolution rates and reduced moisture-related challenges during formulation processes. However, the market is gradually shifting as processing efficiency becomes a critical factor. Direct compressible citric acid variants, such as Jungbunzlauer's CITROCOAT N, are gaining traction in pharmaceutical tableting. These variants address industry needs by offering improved tablet hardness, faster processing times, and enhanced performance in specific applications.

Liquid citric acid formulations are witnessing robust growth, with a projected CAGR of 6.82% through 2030. This growth is driven by manufacturers' increasing focus on operational efficiency and cost optimization. The liquid form eliminates the need for dissolution steps, enabling precise dosing control in automated production systems and streamlining manufacturing processes. This trend is particularly prominent in the beverage industry, where liquid citric acid integrates seamlessly with syrup preparation processes, reducing contamination risks associated with powder handling. Additionally, advancements in storage and transportation technologies have mitigated traditional stability concerns, further enhancing the viability of liquid forms. These improvements are expanding the adoption of liquid citric acid in applications that were previously dominated by anhydrous variants, positioning the segment for sustained growth in the forecast period.

The Citric Acid Market Report Segments the Industry by Form (Anhydrous and Liquid); by Application (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, and More); by Grade (Pharmaceutical Grade, Food Grade, and Industrial Grade); and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). For Each Segment, The Market Sizing and Forecasts Have Been Based On Values in USD.

Geography Analysis

In 2024, Asia-Pacific commands a 37.74% market share, largely due to China's robust production capabilities and its surging domestic appetite in food processing and industrial sectors. The region's advantages include a well-established fermentation infrastructure, competitive production costs, and close access to vital raw materials like corn and sugarcane derivatives. Yet, trade tensions and anti-dumping measures are altering the regional landscape. Countries like India, Thailand, and other Southeast Asian nations are ramping up production capacities to cater to both local and export demands. Japan's sophisticated pharmaceutical and food processing sectors present lucrative market prospects, while Australia's burgeoning beverage industry bolsters regional consumption.

Middle East and Africa is the region to watch, boasting a 7.43% CAGR through 2030. This growth is largely attributed to the burgeoning food processing sectors and infrastructural investments in nations such as Saudi Arabia and the UAE. Government initiatives in the region, aimed at bolstering food security and diversifying industries, are birthing new demand hubs for citric acid. NEOM's collaboration with Liberation Labs to set up precision fermentation facilities underscores the region's ambition in advanced biomanufacturing. Meanwhile, North America and Europe, with their entrenched food and pharmaceutical sectors, offer stable demand, albeit with tempered growth rates due to market saturation and regulatory consistency.

Europe, with its robust demand from the food, beverage, and personal care sectors, remains a stable player, bolstered by stringent quality standards and established processing facilities. North America's growth is steady, driven by a surge in ready-to-drink beverages, convenience foods, and pharmaceuticals. Consumers here increasingly lean towards clean-label ingredients, using citric acid as a natural preservative and flavor enhancer. South America, particularly in nations like Brazil and Argentina, is on the rise, thanks to its expanding food processing sectors and a growing appetite for packaged foods. South American manufacturers enjoy the dual advantage of abundant agricultural feedstocks for citric acid production and a reduced reliance on imports. Across Europe, North America, and South America, regulatory frameworks that favor natural additives further enhance citric acid's market potential, presenting opportunities for both global giants and local players.

- Shandong Ensign Industry Co., Ltd.

- Jungbunzlauer Suisse AG

- COFCO Corporation

- RZBC Group Co., Ltd.

- TTCA Co., Ltd.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Gadot Biochemical Industries Ltd.

- Foodchem International Corporation

- Merck KGaA

- Hawkins, Inc.

- Citrique Belge NV

- BBCA Group (Anhui BBCA)

- FUSO Chemical Co., Ltd.

- Wang Pharmaceuticals and Chemicals

- Hemadri Chemicals

- Vinipul Inorganics India Pvt. Ltd

- Arihant Chemicals

- Anmol Chemicals Private Limited

- Innova Corporate

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing consumer shift to natural acidulants in carbonated soft drinks

- 4.2.2 Increasing demand for citric acid in ready-to-drink beverages

- 4.2.3 Rising adoption in effervescent pharmaceuticals

- 4.2.4 Rise in regulatory push for biodegradable chelating agents in industrial cleaners

- 4.2.5 Increasing need for sugar-reduction reformulation in confectionery

- 4.2.6 Innovations in production processes are improving yield and reducing costs.

- 4.3 Market Restraints

- 4.3.1 Price volatility of raw materials in emerging countries

- 4.3.2 Rise in anti-dumping duties on chinese citric acid

- 4.3.3 Competition from alternative acidulants.

- 4.3.4 Seasonal variations impacting citrus fruit availability.

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form

- 5.1.1 Anhydrous

- 5.1.2 Liquid

- 5.2 By Application

- 5.2.1 Food and Beverage

- 5.2.1.1 Bakery

- 5.2.1.2 Confectionery

- 5.2.1.3 Dairy

- 5.2.1.4 Beverages

- 5.2.1.5 Savory and Snacks

- 5.2.1.6 Other Foods and Beverages

- 5.2.2 Pharmaceuticals

- 5.2.3 Personal Care and Cosmetics

- 5.2.4 Detergents and Household Cleaners

- 5.2.5 Others

- 5.2.1 Food and Beverage

- 5.3 By Grade

- 5.3.1 Pharmaceutical Grade

- 5.3.2 Food Grade

- 5.3.3 Industrial Grade

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Colombia

- 5.4.2.4 Chile

- 5.4.2.5 Peru

- 5.4.2.6 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Netherlands

- 5.4.3.6 Poland

- 5.4.3.7 Belgium

- 5.4.3.8 Sweden

- 5.4.3.9 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Indonesia

- 5.4.4.6 South Korea

- 5.4.4.7 Thailand

- 5.4.4.8 Singapore

- 5.4.4.9 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Shandong Ensign Industry Co., Ltd.

- 6.4.2 Jungbunzlauer Suisse AG

- 6.4.3 COFCO Corporation

- 6.4.4 RZBC Group Co., Ltd.

- 6.4.5 TTCA Co., Ltd.

- 6.4.6 Archer Daniels Midland Company

- 6.4.7 Cargill, Incorporated

- 6.4.8 Gadot Biochemical Industries Ltd.

- 6.4.9 Foodchem International Corporation

- 6.4.10 Merck KGaA

- 6.4.11 Hawkins, Inc.

- 6.4.12 Citrique Belge NV

- 6.4.13 BBCA Group (Anhui BBCA)

- 6.4.14 FUSO Chemical Co., Ltd.

- 6.4.15 Wang Pharmaceuticals and Chemicals

- 6.4.16 Hemadri Chemicals

- 6.4.17 Vinipul Inorganics India Pvt. Ltd

- 6.4.18 Arihant Chemicals

- 6.4.19 Anmol Chemicals Private Limited

- 6.4.20 Innova Corporate

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

日本柠檬酸市场报告(按形态(无水、液体)、应用(食品饮料、家用洗涤剂和清洁剂、药品及其他)和地区划分,2026-2034年)

日本柠檬酸市场报告(按形态(无水、液体)、应用(食品饮料、家用洗涤剂和清洁剂、药品及其他)和地区划分,2026-2034年) 柠檬酸市场规模、份额及成长分析(依形态、应用、功能、等级及地区划分)-2026-2033年产业预测

柠檬酸市场规模、份额及成长分析(依形态、应用、功能、等级及地区划分)-2026-2033年产业预测 伊康酸市场(依等级、形式、通路和应用)-2025-2032 年全球预测柠檬酸市场(按来源、等级、形式、应用和分销管道)—2025-2032 年全球预测柠檬酸盐市场按产品类型、供应来源、形态、等级、应用、最终用途产业和分销管道划分-2025-2032年全球预测

伊康酸市场(依等级、形式、通路和应用)-2025-2032 年全球预测柠檬酸市场(按来源、等级、形式、应用和分销管道)—2025-2032 年全球预测柠檬酸盐市场按产品类型、供应来源、形态、等级、应用、最终用途产业和分销管道划分-2025-2032年全球预测 衣康酸市场-全球产业规模、份额、趋势、机会及预测,依衍生物、应用、区域及竞争细分,2020-2030 年预测

衣康酸市场-全球产业规模、份额、趋势、机会及预测,依衍生物、应用、区域及竞争细分,2020-2030 年预测 柠檬酸的全球市场:各终端用户业界,各地区,机会,预测,2018年~2032年

柠檬酸的全球市场:各终端用户业界,各地区,机会,预测,2018年~2032年 全球柠檬酸市场需求及预测分析(2018-2034)

全球柠檬酸市场需求及预测分析(2018-2034) 柠檬酸市场:按等级、最终用途行业、应用和地区划分柠檬酸市场报告,按应用(食品和饮料、家用洗涤剂和清洁剂、药品和其他)、形式(无水、液体)和地区划分,2025 年至 2033 年

柠檬酸市场:按等级、最终用途行业、应用和地区划分柠檬酸市场报告,按应用(食品和饮料、家用洗涤剂和清洁剂、药品和其他)、形式(无水、液体)和地区划分,2025 年至 2033 年