|

市场调查报告书

商品编码

1851261

电动汽车电池系统:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Battery Systems For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

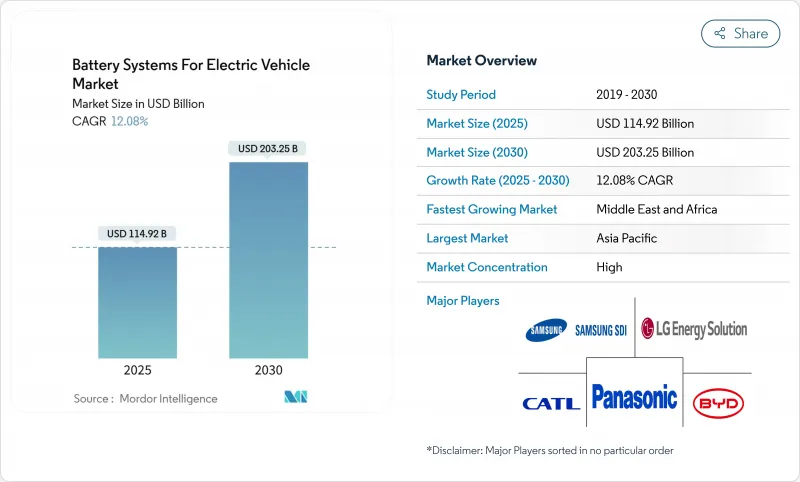

预计到 2025 年,电动车电池系统市场规模将达到 1,149.2 亿美元,到 2030 年将扩大到 2,032.5 亿美元,复合年增长率为 12.08%。

北美和欧洲的奖励主导推广目标、锂离子电池化学成本的快速下降以及亚洲、北美和欧洲垂直整合的超级工厂的部署,都为这一扩张提供了支撑。固态电池技术的突破也为市场带来益处,这些突破有望提高能量密度和安全性;同时,结合锂离子、钠离子和电容器的多化学电池组提供了更大的设计灵活性。儘管美国和欧盟的监管框架收紧了在地化含量限制,但中国製造商仍利用磷酸锂铁的成本优势来扩大市场份额,竞争仍然激烈。供应链分化、热失控召回事件以及关键矿物价格波动等因素虽然会抑制市场前景,但不会阻碍其持续成长的动能。

全球电动汽车电池系统市场趋势与洞察

政府奖励和零排放强制规定

法律规范透过设定电力传动系统的最低销量来加速需求成长。美国为符合条件的车辆提供高达7500美元的税额扣抵,并逐年提高国产车辆的零件含量门槛。加州的「先进清洁汽车II」(Advanced Clean Car II)法规要求汽车製造商在2025年实现22%的零排放汽车销量,并在2035年实现100%的零排放汽车销量。英国强制要求到2030年电动车销量占比达到80%,而加拿大则力争在2035年实现100%的电动车销量。由于违规将面临巨额罚款,大多数汽车製造商都签订了多年期的电池回收协议,从而为电池製造商提供了销售量保障和现金流可见度。

锂离子电池成本下降和能量密度提高

由于学习曲线效应和材料替代,成本持续下降。多家领先的电池製造商的目标是将电池组成本从2024年的每千瓦时118美元降至2026年的每千瓦时60美元以下。富硅负极可提高能量密度,使比容量提升25%至50%,而磷酸锂铁透过先进的涂层技术提高了体积能量密度。成本的快速下降扩大了目标市场,涵盖入门级乘用车、摩托车和对成本敏感的商用车。

关键矿产的供应和价格波动

专注于上游精炼会使製造商面临地缘政治风险。中国精炼了全球80%的磷酸锂铁正极材料,而钴的主要产地只有一个国家。预计到2030年,锂的需求将增加五倍,但矿场核准的延误意味着价格波动正在挤压电池製造商的净利率。多元化措施需要数年才能见效,这增加了对关键供应商的依赖,并降低了价格的透明度。

细分市场分析

到2024年,锂离子电池技术将占据电动车电池系统市场94.12%的份额,并将在2030年之前保持销量领先地位。电池组层面的快速创新正推动能量密度迈向300Wh/kg迈进,同时将成本降至60美元/kWh以下。该领域的製造生态系统涵盖材料、电芯规格和回收流程,从而增强了规模优势,并降低了新车製造商的准入门槛。

固态电池将以39.92%的复合年增长率(CAGR)实现最高增长,这主要得益于陶瓷隔膜能够抑制枝晶生长,并将1000次循环后的容量损失限制在5%以内。其卓越的储能能力使其能够实现紧凑的电池组设计,从而释放车内空间并减轻车辆重量,这对于高性能和远距车型至关重要。固态电池的商业性化取决于自动化烧结和高压层压生产线的成熟,这些生产线预计将在本十年后半段将生产成本降低到与传统锂离子电池持平的水平。

到2024年,镍锰钴电池将占据电动车电池系统市场规模的61.38%,并在对续航里程要求极高的高阶乘用车和轻型卡车领域占据主导地位。持续降低钴含量和采用富锰配方有助于减少价格上涨和道德采购的风险。

磷酸锂铁因其安全性高、原料供应充足且成本低廉而迅速普及,在廉价型轿车和重型商用车领域均有应用。钠离子电池以44.16%的复合年增长率成长,可在低至-40°C的温度下工作,并能承受频繁的快速充电循环。其近乎零锂含量降低了价格风险,并有助于在锂蕴藏量匮乏的地区利用国内资源。钠离子和锂离子混合电池组在保持性能的同时优化了成本,并且随着能量密度达到200Wh/kg,它们构成了一种可以作为过渡到完全钠离子电池架构的方案。

区域分析

由于从矿物加工到电池组装和整车製造的稳定供应链,亚太地区将在2024年维持64.32%的电动车电池系统市场份额。光是中国一国就将在2030年前推动显着成长,这主要得益于强劲的国内需求和出口激增,尤其是对东南亚和拉丁美洲的出口。日本将推进固体研究,而韩国将转向高锰化学以重振竞争力。协调一致的政府奖励和基础建设支出将继续加强区域生态系统。

北美将成为第二大市场,《通膨削减法案》将向清洁能源领域注入3,690亿美元资金,提高关键矿产资源基准值,并打造一系列强劲的新型超级工厂和中游炼油计划。同样,在绿色新政协议和欧洲电池联盟的推动下,欧洲正以9.40%的复合年增长率稳步发展。策略自主将推动由公私合营企业资助的在地化正极材料生产和电池组装。德国正主导一项研究伙伴关係,以推动富硅负极材料的发展,而西班牙和法国则专注于大众市场的磷酸锂铁。

中东和非洲地区正经历最高的成长,复合年增长率达15.74%。沙乌地阿拉伯将投资60亿美元建造一座综合电池产业园区,以实现经济多元化并确保下游汽车製造业的发展。阿联酋的目标是到2035年达到25%的电动车普及率,并沿着酋长国间高速公路建造充电走廊。加纳、摩洛哥和卢安达的早期计划正受益于发展援助机构提供的优惠资金筹措和技术援助,这为非洲大陆两轮车和轻型商用车的区域电气化奠定了基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府奖励和零排放强制规定

- 锂离子电池成本下降和能量密度提高

- OEM超级工厂建设及供货协议

- 扩大快速充电网络

- Vehicle-to-Grid计画将电池货币化

- 与电池健康分析相关的保险折扣

- 市场限制

- 关键矿产的供应和价格波动

- 热失控召回和安全意识

- 贸易壁垒和本地化含量限制扰乱供应链

- LFP/Na离子化学回收经济性的不确定性

- 价值/供应链分析

- 监管环境

- 技术展望

- 电池製造能力分析

- 电池回收和二次利用分析

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依电池类型

- 锂离子

- 镍氢化物

- 铅酸电池

- 超级电容器

- 固态及其他

- 电池化学

- NMC

- NCA

- LFP

- LMO

- 钠离子和新兴物质

- 按车辆类型

- 搭乘用车

- 商用车辆

- 透过推进技术

- 电池电动车(BEV)

- 插电式混合动力汽车(PHEV)

- 混合动力电动车(HEV)

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 泰国

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 南非

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Contemporary Amperex Technology Co., Limited.(CATL)

- BYD Co. Ltd.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- AESC Group Ltd.

- CALB

- Gotion High-tech Co., Ltd.

- EVE Energy Co., Ltd.

- Farasis Energy Europe GmbH

- Northvolt AB

- ProLogium Technology Co., Ltd

- QuantumScape Battery, Inc.

- Solid Power Inc.

- StoreDot

- SES AI Corp.

- Hitachi Energy Ltd.

- Johnson Controls International plc

第七章 市场机会与未来展望

The battery systems for electric vehicles market stands at USD 114.92 billion in 2025 and is forecast to climb to USD 203.25 billion by 2030, reflecting a 12.08% CAGR by 2030.

Incentive-driven adoption targets in North America and Europe, rapid cost declines in lithium-ion chemistry, and vertically integrated gigafactory roll-outs across Asia, North America, and Europe underpin this expansion. The market also benefits from solid-state break-throughs that promise higher energy density and safety, while multi-chemistry packs combining lithium-ion with sodium-ion or ultracapacitors widen design flexibility. Competitive intensity remains high as Chinese producers use lithium iron phosphate cost advantages to win share, even as regulatory frameworks in the United States and the European Union tighten local-content demands. Supply-chain bifurcation, thermal-runaway recalls, and critical-mineral volatility temper the outlook but do not derail the secular growth trajectory.

Global Battery Systems For Electric Vehicle Market Trends and Insights

Government Incentives and Zero-Emission Mandates

Regulatory frameworks accelerate demand by anchoring minimum sales volumes for electric drivetrains. The United States offers tax credits up to USD 7,500 per qualifying vehicle and escalates domestic-content thresholds each year. California's Advanced Clean Cars II rule obliges automakers to reach 22% zero-emission sales in 2025 and 100% by 2035. The United Kingdom mandates 80% electric sales by 2030, while Canada targets 100% by 2035. Because non-compliance triggers sizable penalties, most vehicle makers lock in multi-year battery offtake contracts, providing cell manufacturers with volume security and cash-flow visibility.

Declining Li-ion Costs and Energy Density Gains

Learning-curve effects and materials substitution continue to drive cost trajectories downward. Several top-tier cell makers aim to push pack costs below USD 60 per kWh by 2026, versus USD 118 per kWh in 2024. Energy density climbs through silicon-rich anodes that raise specific capacity by 25-50%, while lithium iron phosphate improves volumetric density with refined cathode coatings. Rapid cost declines widen the total addressable market into entry-level passenger cars, two-wheelers, and cost-sensitive commercial fleets.

Critical-Mineral Supply and Price Volatility

Concentration in upstream refining exposes manufacturers to geopolitical risk. China refines 80% of global lithium iron phosphate cathode material, while one country produces the majority of cobalt. Demand for lithium is expected to grow five-fold by 2030, yet mine approvals lag, forcing price swings that compress cell-maker margins. Diversification efforts require several years to materialize, extending dependence on dominant suppliers and undermining price visibility.

Other drivers and restraints analyzed in the detailed report include:

- OEM Giga-factory Build-outs and Supply Pacts

- Fast-charging Network Expansion

- Thermal-Runaway Recalls and Safety Perception

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion technology held 94.12% of the battery systems for electric vehicles market share in 2024 and remains the volume leader through 2030. Rapid pack-level innovation drives gravimetric densities toward 300 Wh/kg while trimming cost below USD 60 per kWh. The segment's entrenched manufacturing ecosystem spans materials, cell formats, and recycling streams, reinforcing scale advantages and lowering entry barriers for new vehicle OEMs.

Solid-state cells record the highest 39.92% CAGR, propelled by ceramic separators that curb dendrite growth and cut capacity fade to 5% after 1,000 cycles. Their superior energy storage enables compact pack designs that free cabin space and trim curb weight, key factors in high-performance or extended-range models. Commercial readiness hinges on automated sintering and high-pressure lamination lines that slash production cost to parity with conventional lithium-ion by the late decade.

Nickel manganese cobalt chemistry accounted for 61.38% of the battery systems for the electric vehicles market size in 2024, anchoring its position in premium passenger cars and light trucks that demand maximum range. Continuous cobalt-content reduction and manganese-rich formulations cut exposure to price spikes and ethical sourcing concerns.

Lithium iron phosphate rises sharply on the back of robust safety, abundant raw material supply, and lower cost, attracting budget segments and heavy-duty commercial vehicles. Sodium-ion cells, growing at 44.16% CAGR, unlock cold-temperature operation down to -40 °C and tolerate frequent fast-charge cycles. Their near-zero lithium content buffers price risk and allows domestic resource utilization in regions lacking lithium reserves. Hybrid packs combining sodium-ion and lithium-ion optimize cost while maintaining performance, creating an architecture bridge toward full sodium-ion transition once density reaches 200 Wh/kg.

The Battery Systems for Electric Vehicles Market Report is Segmented by Battery Type (Lithium-Ion, Nickel-Metal Hydride, and More), Battery Chemistry (NMC, NCA, LFP, and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Propulsion Technology (Battery Electric Vehicle (BEV), Plug-In Hybrid Electric Vehicle (PHEV), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific maintained 64.32% share of the battery systems for electric vehicles market in 2024, anchored by an integrated supply chain that stretches from mineral processing through cell assembly to vehicle manufacturing. China alone supports a significant growth through 2030 as domestic demand remains strong and exports surge, particularly to Southeast Asia and Latin America. Japan advances solid-state research while Korea pivots toward high-manganese chemistries to regain competitiveness. Government incentive alignment and coordinated infrastructure spending continue to reinforce the regional ecosystem.

North America registers the second-largest market, the Inflation Reduction Act channels USD 369 billion in clean-energy funding and sets escalating critical-mineral thresholds, creating a robust pipeline of new gigafactories and mid-stream refining projects. Similarly, Europe advances at 9.40% CAGR on the back of its Green Deal policies and the European Battery Alliance. Strategic autonomy drives localized cathode production and cell assembly funded by public-private joint ventures. Germany leads research partnerships that push silicon-rich anodes, whereas Spain and France focus on mass-market lithium iron phosphate.

The Middle East & Africa region posts the highest regional growth at 15.74% CAGR. Saudi Arabia invests USD 6 billion in an integrated battery complex to diversify its economy and secure downstream automotive manufacturing. The United Arab Emirates targets 25% electric vehicle penetration by 2035, anchoring charging-corridor build-outs along inter-emirate highways. Early-stage projects in Ghana, Morocco, and Rwanda benefit from concessional finance and development-agency technical assistance, positioning the continent for localized two-wheeler and light-commercial electrification.

- Contemporary Amperex Technology Co., Limited. (CATL)

- BYD Co. Ltd.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- AESC Group Ltd.

- CALB

- Gotion High-tech Co., Ltd.

- EVE Energy Co., Ltd.

- Farasis Energy Europe GmbH

- Northvolt AB

- ProLogium Technology Co., Ltd

- QuantumScape Battery, Inc.

- Solid Power Inc.

- StoreDot

- SES AI Corp.

- Hitachi Energy Ltd.

- Johnson Controls International plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Govt incentives and zero-emission mandates

- 4.2.2 Declining Li-ion costs and energy density gains

- 4.2.3 OEM giga-factory build-outs and supply pacts

- 4.2.4 Fast-charging network expansion

- 4.2.5 Vehicle-to-grid programs monetizing batteries

- 4.2.6 Insurance discounts linked to battery-health analytics

- 4.3 Market Restraints

- 4.3.1 Critical-mineral supply and price volatility

- 4.3.2 Thermal-runaway recalls and safety perception

- 4.3.3 Trade barriers and local-content rules disrupting supply chains

- 4.3.4 Uncertain recycling economics for LFP / Na-ion chemistries

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Battery Manufacturing Capacity Analysis

- 4.8 Battery Recycling and Second-Life Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Nickel-metal-hydride

- 5.1.3 Lead-acid

- 5.1.4 Ultracapacitors

- 5.1.5 Solid-state and others

- 5.2 By Battery Chemistry

- 5.2.1 NMC

- 5.2.2 NCA

- 5.2.3 LFP

- 5.2.4 LMO

- 5.2.5 Sodium-ion and emerging

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Propulsion Technology

- 5.4.1 Battery Electric Vehicle (BEV)

- 5.4.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.4.3 Hybrid Electric Vehicle (HEV)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Thailand

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Contemporary Amperex Technology Co., Limited. (CATL)

- 6.4.2 BYD Co. Ltd.

- 6.4.3 LG Energy Solution Ltd.

- 6.4.4 Panasonic Holdings Corporation

- 6.4.5 Samsung SDI Co., Ltd.

- 6.4.6 SK On Co., Ltd.

- 6.4.7 AESC Group Ltd.

- 6.4.8 CALB

- 6.4.9 Gotion High-tech Co., Ltd.

- 6.4.10 EVE Energy Co., Ltd.

- 6.4.11 Farasis Energy Europe GmbH

- 6.4.12 Northvolt AB

- 6.4.13 ProLogium Technology Co., Ltd

- 6.4.14 QuantumScape Battery, Inc.

- 6.4.15 Solid Power Inc.

- 6.4.16 StoreDot

- 6.4.17 SES AI Corp.

- 6.4.18 Hitachi Energy Ltd.

- 6.4.19 Johnson Controls International plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球和中国电动汽车电池和材料:技术、趋势和市场预测

全球和中国电动汽车电池和材料:技术、趋势和市场预测 日本电动车电池市场规模、份额、趋势及预测(按电池类型、驱动系统、车辆类型和地区划分,2026-2034年)

日本电动车电池市场规模、份额、趋势及预测(按电池类型、驱动系统、车辆类型和地区划分,2026-2034年) 2026年全球电动汽车电池市场报告

2026年全球电动汽车电池市场报告 电动车电池市场 - 全球产业规模、份额、趋势、竞争格局、机会及预测(按车辆类型、动力方式、电池类型、电池容量、需求类别、地区和竞争格局划分,2021-2031年)电动车电池系统市场-全球产业规模、份额、趋势、机会、预测:按电池类型、车辆类型、地区和竞争格局划分,2021-2031年

电动车电池市场 - 全球产业规模、份额、趋势、竞争格局、机会及预测(按车辆类型、动力方式、电池类型、电池容量、需求类别、地区和竞争格局划分,2021-2031年)电动车电池系统市场-全球产业规模、份额、趋势、机会、预测:按电池类型、车辆类型、地区和竞争格局划分,2021-2031年 2026-2030年全球电动Scooter电池市场

2026-2030年全球电动Scooter电池市场 锂离子电池用炭黑:全球市占率及排名、总收入及需求预测(2025-2031年)汽车锂离子电池用炭黑:全球市占率及排名、总收入及需求预测(2025-2031年)

锂离子电池用炭黑:全球市占率及排名、总收入及需求预测(2025-2031年)汽车锂离子电池用炭黑:全球市占率及排名、总收入及需求预测(2025-2031年) 电动汽车电池市场(按电池类型、充电容量、电池格式、推进类型、车辆类型和分销管道划分)—2025-2032 年全球预测电动车电池市场(按最终用途、应用、电池容量、电池外形规格和电池化学成分)—2025-2032 年全球预测

电动汽车电池市场(按电池类型、充电容量、电池格式、推进类型、车辆类型和分销管道划分)—2025-2032 年全球预测电动车电池市场(按最终用途、应用、电池容量、电池外形规格和电池化学成分)—2025-2032 年全球预测