|

市场调查报告书

商品编码

1851292

亚太网路安全:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)APAC Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

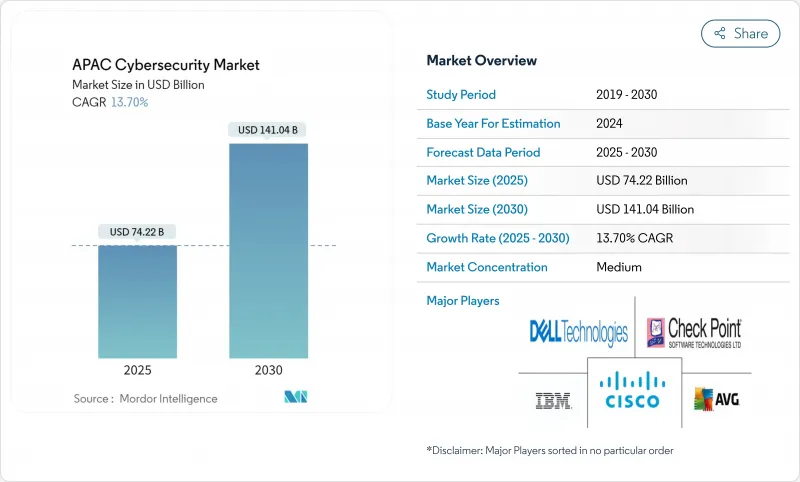

亚太地区网路安全市场预计到 2025 年将达到 742.2 亿美元,到 2030 年将达到 1,410.4 亿美元,年复合成长率为 13.7%。

这反映了各国政府对数位主权的推动以及企业向主动网路防御模式的转变。

国家级网路攻击日益增多、5G网路部署加速、数位支付诈骗激增以及人才长期短缺,正在改变预算优先事项。如今,竞争不再仅仅取决于产品功能,而是更取决于能否在法规环境分散的情况下,提供自主云架构、人工智慧主导的託管检测以及整合的IT和OT安全解决方案。对于那些能够将本地化威胁情报与可扩展的託管服务相结合的供应商而言,尤其是在缺乏内部安全专家的中端市场领域,机会比比皆是。

亚太网路安全市场趋势与洞察

亚太地区各国政府的资料主权要求推动了国内网路安全支出。

中国将于2025年生效的《网路资料安全管理条例》将要求资料处理必须在中国境内进行,并要求在中国营运的跨国公司实施独立的安全架构。新加坡的「网路安全基础认证」(Cyber Essentials)计画将政府合约与供应商认证挂钩,刺激了对本地供应商的需求。澳洲的REDSPICE倡议拨款20亿澳元用于为情报机构建立主权云,显示相关政策正在直接转化为网路安全方面的支出。为了维持市场准入,供应商正在将研发中心和安全营运中心(SOC)在地化,而本土专家则获得了合规方面的优势。

5G的推出为日本、韩国和印度的通讯业者带来了新的潜在网路威胁。

高吞吐量的5G架构引入了微切片和边缘运算节点,这些节点无法透过传统的边界防护工具进行保护。日本的《主动网路防御法》允许对针对通讯网路的网路威胁进行先发制人的干扰。韩国记录显示,2024年公共网路遭受了156万次骇客试验,其中80%的目标是5G和物联网终端。印度通讯业者报告称,57%的攻击导致服务降级,凸显了零信任和人工智慧主导分析的迫切需求。因此,市场对安全存取服务边际(SASE)平台和针对营运商环境最佳化的虚拟化防火墙的需求日益增长。

亚太新兴经济体网路安全人才严重短缺,推高服务成本。

该地区网路安全负责人缺口高达280万,限制了託管服务的扩充性,并导致薪资水平超出中小企业的预算。菲律宾仅有200名认证专家,而新加坡则有3000名,加剧了计划延误。越南已累计1亿美元用于人才发展计划,目标是在2025年前培养1000名专家和5000名工程师。 OT安全和云端架构领域的人才短缺最为严重,迫使企业外包相关功能或延迟部署,从而减少了可满足的需求。

细分市场分析

到2024年,解决方案收入将占总收入的57.6%,到2030年将以21.4%的复合年增长率增长,这主要得益于企业面临人才短缺,导致託管安全服务不断扩张。亚太网路安全市场青睐那些将全天候安全营运中心 (SOC) 监控、威胁调查和事件回应整合到基于结果的服务等级协定 (SLA) 中的供应商。 Ensign InfoSecurity 将成为2024年唯一跻身全球十大託管安全服务供应商 (MSSP) 行列的亚太地区公司,这标誌着该地区託管服务成熟度的提升。

内部分析师薪资的上涨,加上董事会层级对安全漏洞的课责,正促使大型企业与外部安全营运中心 (SOC) 共同管理其安全工具。人工智慧驱动的故障排查和自动化功能使託管安全服务提供者 (MSSP) 能够盈利服务中端市场客户,从而推动了此类服务的普及。因此,对基于平台的服务产品的投资正在加速成长,服务供应商正透过整合扩展灾难復原 (XDR)、安全营运自动化与回应 (SOAR) 和机器学习分析等技术来提升自身竞争力。

至2024年,本地部署的网路安全将占亚太地区网路安全市场份额的62.5%。同时,受远端办公政策和多重云端部署的推动,云端原生安全将以23.5%的复合年增长率成长。 HashiCorp的一项调查显示,70%的区域企业透过多重云端实现业务目标,90%的企业将安全视为关键成功因素。

为了保护跨云端服务供应商 (CSP) 和边缘节点的工作负载,各组织正在采用零信任网路和容器安全。儘管技能短缺仍然是一大挑战(31% 的组织表示其云端专业知识有限),但供应商正透过低程式码策略编配和託管 SASE 来应对这项挑战。因此,云端采用在绿地计画越来越受欢迎,而混合架构也正在成为传统系统迁移的途径。

亚太网路安全市场报告按解决方案、服务、部署类型(本地部署、云端部署)、最终用户垂直产业(银行、金融服务和保险、医疗保健、IT 和通讯、工业和国防、製造业、零售和电子商务、能源和公共产业、製造业、其他)、最终用户公司规模(中小企业、大型企业)和国家/地区对产业进行分类。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府资料主权要求推动亚太地区各国加大国内网路安全投资。

- 5G的推出为日本、韩国和印度的通讯业者带来了新的潜在网路威胁。

- 数位支付和电子商务诈骗激增推动东南亚安全投资

- 亚太地区主导对关键基础设施的攻击日益增多,推动了OT安全技术的普及应用。

- 中国和东协地区正经历一波中小企业迁移到云端的浪潮,因此需要保护其云端工作负载。

- 国家网路安全激励计划(例如,SG Cyber Safe、REDSPICE)正在推动市场成长

- 市场限制

- 亚太新兴经济体网路安全人才严重短缺,推高服务成本。

- 分散的区域合规体系阻碍了解决方案的标准化。

- 亚太地区中小企业对价格的高度敏感限制了先进解决方案的采用。

- 由于对安全硬体组件的出口限制,供应链中断

- 关键法规结构评估

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场区隔

- 报价

- 解决方案

- 应用程式安全

- 云端安全

- 资料安全

- 身分和存取管理

- 基础设施保护

- 综合风险管理

- 网路安全设备

- 端点安全

- 其他服务

- 服务

- 专业服务

- 託管服务

- 解决方案

- 透过部署模式

- 本地部署

- 云

- 按最终用户行业划分

- BFSI

- 卫生保健

- 资讯科技和电讯

- 工业与国防

- 製造业

- 零售与电子商务

- 能源与公共产业

- 製造业

- 其他的

- 按最终用户公司规模划分

- 中小企业

- 大公司

- 按国家/地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 新加坡

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Cisco Systems, Inc.

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Fortinet, Inc.

- Kaspersky Lab

- Broadcom, Inc.(Symantec Enterprise Division)

- BAE Systems plc

- NEC Corporation

- Infosys Limited

- Tata Consultancy Services Limited

- Darktrace plc

- Zscaler, Inc.

- CrowdStrike Holdings, Inc.

- F5, Inc.

- Sophos Ltd.

- Okta, Inc.

- SentinelOne, Inc.

- Rapid7, Inc.

- Imperva, Inc

第七章 市场机会与未来展望

The APAC cybersecurity market size reached USD 74.22 billion in 2025 and is forecast to expand at a 13.7% CAGR to USD 141.04 billion by 2030, reflecting governments' push for digital sovereignty and enterprises' shift toward proactive cyber-defense models.

Heightened state-sponsored attacks, accelerating 5G roll-outs, surging digital-payment fraud, and chronic talent shortages are reshaping budget priorities, while local data-protection rules are recasting procurement in favor of regionally domiciled vendors. Competition now hinges less on product features and more on the ability to deliver sovereign-cloud architectures, AI-driven managed detection, and integrated IT-OT security across fragmented regulatory environments. Opportunities abound for providers that combine localized threat intelligence with scalable managed services, especially in mid-market segments underserved by in-house security expertise.

APAC Cybersecurity Market Trends and Insights

Government Data-Sovereignty Mandates Accelerating Domestic Cybersecurity Spend Across APAC

China's Network Data Security Management Regulations taking effect in 2025 require in-country data processing and create separate security stacks for multinationals operating inside China. Singapore's refreshed Cyber Essentials program ties government contracts to vendor certification, driving local provider demand. Australia's REDSPICE initiative allocates AUD 2 billion to a sovereign cloud for the intelligence community, illustrating how policy translates directly into cybersecurity outlays. Vendors now localize R&D centers and SOCs to preserve market access, while homegrown specialists gain a compliance-driven edge.

5G Roll-Outs Creating New Network Threat Surfaces for Telcos in Japan, South Korea and India

High-throughput 5G architectures introduce micro-slicing and edge-compute nodes that traditional perimeter tools cannot secure. Japan's Active Cyber Defense law authorizes pre-emptive disruption of cyber threats targeting telecom networks. South Korea logged 1.56 million hacking attempts on public networks in 2024, 80% aimed at 5G and IoT endpoints. India's operators report that 57% of breaches result in service slowdowns, highlighting the urgency for zero-trust and AI-driven analytics. Consequently, demand is rising for secure access service edge (SASE) platforms and virtualized firewalls optimized for carrier environments.

Acute Cybersecurity Talent Shortage Inflating Service Costs in Emerging APAC Economies

The region accounts for 2.8 million unfilled cyber roles, restricting managed-service scalability and pushing salaries beyond SME budgets. The Philippines counts only 200 certified specialists versus Singapore's 3,000, amplifying project delays. Vietnam earmarked USD 100 million for workforce programs to train 1,000 experts and 5,000 engineers by 2025. Scarcity is most severe in OT security and cloud architecture, forcing enterprises to outsource functions or postpone deployments, dampening addressable demand.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Digital-Payment and E-Commerce Fraud Driving Security Investments in Southeast Asia

- Escalating State-Sponsored Attacks on APAC Critical Infrastructure Stimulating OT Security Adoption

- Fragmented Regional Compliance Regimes Complicating Solution Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained 57.6% revenue in 2024, yet managed security services are projected to expand 21.4% CAGR through 2030 as enterprises confront staffing gaps. The APAC cybersecurity market favors providers that bundle 24X7 SOC monitoring, threat hunting, and incident response under outcome-based SLAs. Ensign InfoSecurity became the only APAC firm to reach the global top-10 MSSP list in 2024, signaling the region's ascent in managed-service maturity.

Rising wages for in-house analysts, coupled with board-level accountability for breaches, push even large enterprises to co-manage security tools with external SOCs. AI-assisted triage and automation enable MSSPs to serve mid-market clients profitably, widening adoption. As a result, investment in platform-based service delivery is accelerating, with providers embedding XDR, SOAR, and machine-learning analytics to differentiate.

On-premise installations held 62.5% of APAC cybersecurity market share in 2024 because regulated sectors still favor physical control over data. Cloud-native security, however, is growing at 23.5% CAGR, propelled by remote-work mandates and multi-cloud adoption. A HashiCorp survey showed 70% of regional firms hit business targets via multi-cloud, with 90% rating security the defining success factor.

Organizations are embracing zero-trust networking and container security to protect workloads that span CSPs and edge nodes. Skills shortages remain a headwind-31% cite limited cloud expertise-but vendors counter with low-code policy orchestration and managed SASE offerings. Consequently, cloud deployments increasingly win green-field projects, while hybrid architectures emerge as a transition path for legacy systems.

The APAC Cybersecurity Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises), and Country.

List of Companies Covered in this Report:

- Cisco Systems, Inc.

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Fortinet, Inc.

- Kaspersky Lab

- Broadcom, Inc. (Symantec Enterprise Division)

- BAE Systems plc

- NEC Corporation

- Infosys Limited

- Tata Consultancy Services Limited

- Darktrace plc

- Zscaler, Inc.

- CrowdStrike Holdings, Inc.

- F5, Inc.

- Sophos Ltd.

- Okta, Inc.

- SentinelOne, Inc.

- Rapid7, Inc.

- Imperva, Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Data-Sovereignty Mandates Accelerating Domestic Cybersecurity Spend Across APAC

- 4.2.2 5G Roll-Outs Creating New Network Threat Surfaces for Telcos in Japan, South Korea and India

- 4.2.3 Surge in Digital Payments and E-commerce Fraud Driving Security Investments in Southeast Asia

- 4.2.4 Escalating State-Sponsored Attacks on APAC Critical Infrastructure Stimulating OT Security Adoption

- 4.2.5 SME Cloud Migration Wave Necessitating Cloud Workload Protection in China and ASEAN

- 4.2.6 National Cybersecurity Incentive Programs (e.g., SG Cyber Safe, REDSPICE) Catalyzing Market Growth

- 4.3 Market Restraints

- 4.3.1 Acute Cybersecurity Talent Shortage Inflating Service Costs in Emerging APAC Economies

- 4.3.2 Fragmented Regional Compliance Regimes Complicating Solution Standardization

- 4.3.3 High Price Sensitivity Among APAC SMEs Limiting Adoption of Advanced Solutions

- 4.3.4 Supply-Chain Disruptions from Export Controls on Security Hardware Components

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Manufacturing

- 5.3.9 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 Australia and New Zealand

- 5.5.6 Singapore

- 5.5.7 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Palo Alto Networks, Inc.

- 6.4.5 Check Point Software Technologies Ltd.

- 6.4.6 Fortinet, Inc.

- 6.4.7 Kaspersky Lab

- 6.4.8 Broadcom, Inc. (Symantec Enterprise Division)

- 6.4.9 BAE Systems plc

- 6.4.10 NEC Corporation

- 6.4.11 Infosys Limited

- 6.4.12 Tata Consultancy Services Limited

- 6.4.13 Darktrace plc

- 6.4.14 Zscaler, Inc.

- 6.4.15 CrowdStrike Holdings, Inc.

- 6.4.16 F5, Inc.

- 6.4.17 Sophos Ltd.

- 6.4.18 Okta, Inc.

- 6.4.19 SentinelOne, Inc.

- 6.4.20 Rapid7, Inc.

- 6.4.21 Imperva, Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

区块链网路安全市场分析与预测(2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案

区块链网路安全市场分析与预测(2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、解决方案 2032 年网路安全和资料隐私技术市场预测:按组件、安全类型、部署类型、技术、组织规模、最终用户和地区进行的全球分析安全态势管理市场机会、成长驱动因素、产业趋势分析及预测(2025-2034 年)

2032 年网路安全和资料隐私技术市场预测:按组件、安全类型、部署类型、技术、组织规模、最终用户和地区进行的全球分析安全态势管理市场机会、成长驱动因素、产业趋势分析及预测(2025-2034 年) 2025年全球建设产业网路安全市场报告2025年金融保全服务全球市场报告2025年海事网路安全全球市场报告2032 年金融服务网路安全市场预测:按安全类型、部署、解决方案、最终用户和地区进行的全球分析2025年旅游安全全球市场报告2025年全球银行网路安全市场报告2025年金融服务网路安全系统与服务全球市场报告

2025年全球建设产业网路安全市场报告2025年金融保全服务全球市场报告2025年海事网路安全全球市场报告2032 年金融服务网路安全市场预测:按安全类型、部署、解决方案、最终用户和地区进行的全球分析2025年旅游安全全球市场报告2025年全球银行网路安全市场报告2025年金融服务网路安全系统与服务全球市场报告