|

市场调查报告书

商品编码

1851297

手势姿态辨识:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Gesture Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

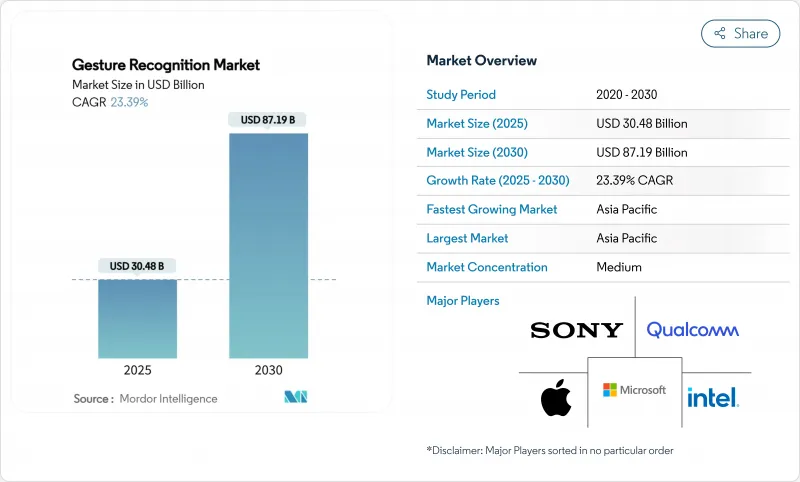

手势姿态辨识市场规模预计到 2025 年将达到 304.8 亿美元,到 2030 年将达到 871.9 亿美元,预测期内(2025-2030 年)复合年增长率为 23.39%。

这种持续增长反映了先进毫米波雷达、多区域飞行时间 (ToF) 感测器和边缘人工智慧演算法的融合,从而在智慧型手机、汽车、医疗设备和工业设备中实现响应迅速、低延迟的人机互动介面。高阶行动装置中感测器出货量的加速成长、汽车安全系统监管压力以及医疗保健领域对感染控制的需求,都在刺激着市场需求。同时,手势姿态辨识市场正经历价值重心从以硬体为中心的解决方案向软体和人工智慧堆迭的转变,这些堆迭能够实现互动个性化、减少误报并延长设备寿命。诸如美国《晶片和影像辨识法案》(CHIPS Act) 和欧洲《晶片和影像辨识法案》(CHIPS Act) 等区域性製造激励措施,正在重塑供应链,并为本地零件製造创造新的成本优势。随着这些因素的汇聚,垂直整合感测器、软体和云端协作层的产业参与企业预计将在手势姿态辨识市场获得不成比例的回报。

全球手势姿态辨识市场趋势与洞察

毫米波和飞行时间感测器在亚洲旗舰智慧型手机中越来越普及

亚洲行动电话厂商目前正将STMicroelectronics的VL53L7CX等多区域ToF模组整合到手机中,以实现毫米级深度精度,且不受环境光影响,即使在光线不足的情况下也能可靠地进行空中指令输入。 Ceva的MotionEngine Hex韧体整合了惯性和雷达数据,可实现对使用者介面的空间控制。随着ToF晶片组在大批量生产中的单价降至1美元以下,手势控制正从高端差异化功能转变为手势姿态辨识市场的标配功能。

汽车製造商采用车载手势抬头显示器以满足欧洲新车安全评鑑协会(Euro NCAP)的规定

2024年7月生效的「高级驾驶员分心警告」法规要求汽车製造商降低驾驶员的认知负荷,这推动了基于摄影机的手势识别系统在欧洲车型中的快速整合。 BMW7系列车型获得L2/L3级认证,标誌着该技术已具备商业性化条件;奥迪的3D驾驶座介面则展示了透过在主机顶部挥动手掌即可选择多模态资讯娱乐系统。能够保证回应时间在150毫秒以内且误报率低于3%的供应商有望赢得专案奖项,从而进一步巩固手势姿态辨识市场的成长动能。

在热带地区,基于视觉的系统在阳光下会出现较高的误报率。

以摄影机为中心的演算法难以在明亮的背景下识别手的轮廓,导致户外自助服务终端和叫车等应用程式中的错误率飙升。研究表明,基于雷达的替代方案无论光照强度如何,都能保持90%以上的照度,这迫使系统设计人员在手势姿态辨识市场中采用多感测器融合技术。

细分市场分析

到2024年,非接触式解决方案将占总收入的58.2%,反映出终端市场对卫生、驾驶安全和身临其境型娱乐的重视。到2030年,非接触式细分市场将以24.4%的年复合成长率成长,超过整体手势姿态辨识市场,这主要得益于飞行时间(ToF)、毫米波雷达和超音波阵列等材料成本的降低。相较之下,电容式控制在对成本敏感的消费性电子设备中仍然重要,但其年复合成长率仍处于个位数。京瓷的深度感测器在10公分范围内实现了100微米的分辨率,可用于需要手术级精度的机器人拾取放置和整形外科矫正工具。向环境互动的稳定转变表明,非接触式模式最终将比其依赖接触的领先占据更大的市场份额。

非接触式技术的兴起正在改变供应商格局。过去将晶片产品商品化的感测器供应商,如今开始将人工智慧韧体、数据模型和开发者入口网站捆绑销售,从中赚取硬体利润,并收取持续的授权费用。这种重新捆绑销售模式符合原始设备製造商 (OEM) 对现场可无线升级效能提升的需求,从而支援手势姿态辨识市场大规模采用非接触式技术所需的可扩展经济模式。

到2024年,硬体将占手势姿态辨识市场规模的71.5%,这主要受镜头、雷达前端和微控制器等固有成本的影响。然而,能够实现情境感知、使用者自适应和协作学习的软体平台预计将以23.7%的复合年增长率成长,比硬体成长高出350个基点以上。英飞凌的DEEPCRAFT Ready Models提供针对常见手势的预训练神经网络,可将整合时间缩短40%,从而提升公司在价值链上的地位。同时,Imagimob基于视觉化图的机器学习工具可将模型开发週期缩短至数小时,让中端OEM厂商也能轻鬆进行AI最佳化。

收入结构的转变为服务捆绑创造了机会,包括预测性维护、云端基础分析以及透过手势识别实现的应用程式内数位购买。能够编配晶片、韧体和生命週期服务的供应商预计将在手势姿态辨识市场中占据有利地位,因为总体拥有成本 (TCO) 将超过组件价格。

区域分析

亚太地区的领先地位得益于垂直整合的供应链、政府资金支持以及庞大的早期用户装置量。该地区的行动电话品牌每10-12个月就会推出新款旗舰机型,每款机型都配备高解析度ToF阵列,从而扩大了感测器供应商的手势姿态辨识市场。日本企业集团正在将基于XR技术的技能转移平台应用于汽车焊接和半导体微影术,这进一步推动了对高精度手势辨识模型的需求。韩国的晶圆生产能力确保了零件供应的连续性,而印度智慧电视的普及则让中等收入家庭也能使用非接触式遥控器,从而扩大了收入金字塔。

在北美,手术室和诊断中心正利用医疗保健领域的支出优势来提高单位收入。采用悬浮式显示器的医院报告称,交叉感染事件显着减少,降低了再入院罚款,并提高了手势介面的投资回报率。汽车原始设备製造商 (OEM) 正在整合基于手势的驾驶员监控和驾驶感测器磨损率监测系统,以符合 2024 年后联邦政府关于分心驾驶的指导方针。

欧洲在监管方面发挥引领作用,Euro NCAP 指令强制要求车辆配备分心驾驶缓解技术,并加速在豪华车和大众市场车型中推广应用。德国供应商正与国内汽车製造商合作开发手势控制模组,儘管硬体采购全球化,但仍巩固了区域价值获取。同时,海湾合作委员会 (GCC) 国家正在推进人工智慧主权倡议,为配备非接触式使用者介面的公共服务亭提供资金,这使得中东地区相比其现有基础而言,展现出显着的成长前景。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 毫米波和飞行时间(ToF)感测器在亚洲旗舰智慧型手机中越来越受欢迎。

- 汽车製造商采用车载手势抬头显示器以符合欧洲新车安全评估协会(Euro NCAP)关于防止驾驶员分心的规定

- 美国和德国的医院要求使用非接触式人机互动系统,以降低手术室的医院感染风险。

- 整合到 XR 穿戴式装置中,可实现 6 自由度控制,用于工业培训(日本)

- 在价格暴跌的市场中,智慧型电视厂商为了脱颖而出,会将手势遥控器与电视遥控器捆绑销售。

- 政府智慧城市拨款促进公共资讯亭手势使用者介面部署(海湾合作委员会)

- 市场限制

- 在热带地区,基于视觉的系统在阳光下假阳性率较高

- 缺乏开放的互通性标准会增加原始设备製造商的整合成本。

- 在10奈米以下製程的移动SoC中,「始终开启」手势唤醒词会消耗大量电量。

- GDPR下车载影片分析的资料隐私合规性障碍

- 监理展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过技术

- 基于触摸的手势姿态辨识

- 2D多点触控面板

- 电容式和电阻式感测器

- 非接触式手势姿态辨识

- 基于二维摄影机的

- 3D深度和飞行时间

- 超音波和毫米波雷达

- 基于触摸的手势姿态辨识

- 按组件

- 硬体(感测器、控制器、SoC)

- 软体(机器学习演算法、SDK、中介软体)

- 透过手势类型

- 线上动态手势

- 离线静态手势

- 通过认证

- 生物辨识技术(脸部、虹膜、手掌)

- 非生物特征测量(运动、姿势)

- 按最终用户行业划分

- 消费性电子产品

- 智慧型手机和平板电脑

- 智慧电视和机上盒

- 扩增实境/虚拟实境和穿戴式设备

- 车

- 驾驶员监控和资讯娱乐

- 航太/国防

- 卫生保健

- 手术室及诊断室

- 游戏与娱乐

- 工业机器人

- 其他行业

- 消费性电子产品

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 纽西兰,澳大利亚

- 亚太其他地区

- 中东和非洲

- 海湾合作委员会(沙乌地阿拉伯、阿联酋、卡达)

- 土耳其

- 南非

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Intel Corporation

- Qualcomm Technologies Inc.

- Apple Inc.

- Microsoft Corp.

- Sony Group Corp.

- Google LLC

- Meta Platforms Inc.

- Ultraleap Ltd.

- Microchip Technology Inc.

- Infineon Technologies AG

- Synaptics Inc.

- Elliptic Laboratories AS

- GestureTek Inc.

- Cognitec Systems GmbH

- Eyesight Technologies Ltd.

- PointGrab Ltd.

- Omron Corporation

- Jabil Inc.

- Leap Motion

第七章 市场机会与未来展望

The Gesture Recognition Market size is estimated at USD 30.48 billion in 2025, and is expected to reach USD 87.19 billion by 2030, at a CAGR of 23.39% during the forecast period (2025-2030).

This sustained expansion reflects the convergence of advanced millimeter-wave radar, multizone Time-of-Flight (ToF) sensors, and edge-AI algorithms that together enable responsive, low-latency human-machine interfaces across smartphones, vehicles, medical devices, and industrial equipment. Accelerating sensor shipments in premium handsets, regulatory pressure on automotive safety systems, and infection-control imperatives in healthcare are jointly stimulating volume demand. At the same time, the gesture recognition market is witnessing a value shift from hardware-centric solutions toward software and AI stacks that personalize interactions, reduce false positives, and extend device longevity. Regional manufacturing incentives most notably the CHIPS Act in the United States and the European Chips Act are reshaping supply chains and creating new cost advantages for local component production. As these drivers converge, industry participants that integrate vertically across sensor, software, and cloud orchestration layers are positioned to capture disproportionate returns within the gesture recognition market.

Global Gesture Recognition Market Trends and Insights

Proliferation of mm-wave and ToF sensors in flagship smartphones across Asia

Asia-based handset OEMs now embed multizone ToF modules such as STMicroelectronics' VL53L7CX to deliver millimeter-level depth accuracy without ambient-light restrictions, enabling reliable mid-air command input even under harsh illumination. The deployment extends to smart-TV handsets through Ceva's MotionEngine Hex firmware, which integrates inertial and radar data to deliver spatial control of user interfaces. As the cost of ToF chipsets falls below USD 1 per unit in volume lots, gesture control is transitioning from a premium differentiator to a default feature in the gesture recognition market.

Automaker adoption of in-cabin gesture HUDs to meet Euro NCAP mandates

The July 2024 Advanced Driver Distraction Warning regulation obliges OEMs to mitigate cognitive load, propelling rapid integration of camera-based gesture hubs in European models. BMW's Level 2/3 certification on the 7 Series demonstrates commercial readiness, while Audi's 3-D cockpit interface showcases multi-modal infotainment selection using above-console hand sweeps. Suppliers that can guarantee sub-150 ms response times and <3% false-trigger rates stand to win program awards, reinforcing the growth trajectory of the gesture recognition market.

High false-positive rates in sunlight for vision-based systems in tropical regions

Camera-centric algorithms struggle to resolve hand contours against high-lux backgrounds, driving error spikes in outdoor kiosks and ride-hailing vehicles. Research indicates radar-based alternatives maintain >90% precision independent of illumination, prompting system designers to adopt multi-sensor fusion in the gesture recognition market.

Other drivers and restraints analyzed in the detailed report include:

- Hospital demand for touch-free HMI to cut HAI risks in surgical suites

- Integration into XR wearables to unlock 6-DoF control for industrial training

- Absence of open interoperability standards inflating OEM integration cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Touchless solutions generated 58.2% of 2024 revenue, reflecting end-market emphasis on hygiene, driver safety, and immersive entertainment. The touchless sub-segment will compound at 24.4% through 2030, outpacing the broader gesture recognition market as ToF, mm-wave radar, and ultrasonic arrays reduce bill-of-materials cost. In contrast, capacitive touch-based controls retain relevance in cost-sensitive consumer devices, yet their CAGR trails at single-digits. Kyocera's depth sensor demonstrates 100 µm resolution within 10 cm, enabling robotic pick-and-place and orthopedic alignment tools that demand surgical-grade accuracy. The steady migration toward ambient interaction implies touchless modalities will ultimately hold a greater gesture recognition market share than their contact-dependent predecessors.

Touchless expansion is altering supplier power dynamics. Sensor vendors that historically commoditized silicon are now bundling AI firmware, data models, and developer portals, capturing recurring license fees on top of hardware margins. This re-bundling aligns with OEM priorities for field-upgradable over-the-air performance improvements and supports the scalable economics required for high-volume touchless adoption within the gesture recognition market.

Hardware contributed 71.5% of gesture recognition market size in 2024, driven by the intrinsic cost of lenses, radar front-ends, and MCUs. However, software platforms that deliver contextual awareness, user adaptation, and federated learning are forecast at a 23.7% CAGR-more than 350 bps above hardware growth. Infineon's DEEPCRAFT Ready Models supply pre-trained neural networks for common gestures, cutting integration time by 40% and repositioning the firm higher on the value curve. Meanwhile, Imagimob's visual graph-based ML tooling compresses model-development cycles to hours, democratizing AI optimization for mid-tier OEMs.

The revenue mix shift creates opportunities for service bundling: predictive maintenance, cloud-based analytics, and in-app monetization through gesture-initiated digital purchases. Suppliers able to orchestrate silicon, firmware, and lifecycle services are poised to command loyalty in the gesture recognition market as total cost of ownership eclipses component price considerations.

Gesture Recognition Market Report is Segmented by Technology (Touch-Based Gesture Recognition, Touchless Gesture Recognition), Component (Hardware, Software), Gesture Type (Online Dynamic Gestures, Offline Static Gestures), Authentication (Biometric, Non-Biometric), End-User Industry (Consumer Electronics, Automotive, Aerospace and Defense and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific's dominance rests on vertically integrated supply chains, supportive government funding, and an immense installed base of early-adopter consumers. Regional handset brands release new flagship lines every 10-12 months, each iteration embedding higher-resolution ToF arrays, thereby expanding the gesture recognition market size for sensor vendors. Japanese conglomerates employ XR-based skill-transfer platforms in automotive welding and semiconductor lithography, reinforcing demand for high-precision gesture models. South Korea's wafer capacity secures component continuity, while India's smart-TV expansion introduces touchless remotes into middle-income households, broadening the revenue pyramid.

North America leverages healthcare spending power for surgical suites and diagnostic centers, generating premium revenue per unit. Hospitals adopting mid-air displays report significant reductions in cross-contamination incidents, translating into lower readmission penalties and bolstering ROI for gesture interfaces. Automotive OEMs integrate gesture-based driver monitoring to comply with post-2024 federal guidelines on distracted driving, pushing incremental sensor attach rates.

Europe acts as a regulatory pacesetter. Euro NCAP directives mandate distraction-mitigation technologies, accelerating deployment across both luxury and mass-market vehicle classes. German suppliers co-develop gesture modules with domestic automakers, cementing regional value capture despite globalized hardware sourcing. Meanwhile, GCC nations pursue AI sovereignty initiatives that fund public-service kiosks with touchless UIs, giving the Middle East an outsized growth profile relative to its current base.

- Intel Corporation

- Qualcomm Technologies Inc.

- Apple Inc.

- Microsoft Corp.

- Sony Group Corp.

- Google LLC

- Meta Platforms Inc.

- Ultraleap Ltd.

- Microchip Technology Inc.

- Infineon Technologies AG

- Synaptics Inc.

- Elliptic Laboratories AS

- GestureTek Inc.

- Cognitec Systems GmbH

- Eyesight Technologies Ltd.

- PointGrab Ltd.

- Omron Corporation

- Jabil Inc.

- Leap Motion

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of mm-wave and ToF sensors in flagship smartphones across Asia

- 4.2.2 Automaker adoption of in-cabin gesture HUDs to meet Euro NCAP distraction mandates

- 4.2.3 Hospital demand for touch-free HMI to cut HAI risks in surgical suites (US and Germany)

- 4.2.4 Integration into XR wearables to unlock 6-DoF control for industrial training (Japan)

- 4.2.5 Smart-TV vendors bundling air-gesture remotes to differentiate in price-eroding market

- 4.2.6 Government smart-city grants driving public-kiosk gesture UI roll-outs (GCC)

- 4.3 Market Restraints

- 4.3.1 High false-positive rates in sunlight for vision-based systems in tropical regions

- 4.3.2 Absence of open interoperability standards inflating OEM integration cost

- 4.3.3 "Always-on" gesture wake-word draining battery in sub-10 nm mobile SoCs

- 4.3.4 Data-privacy compliance hurdles for in-cabin video analytics under GDPR

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Touch-based Gesture Recognition

- 5.1.1.1 2-D Multi-touch Panels

- 5.1.1.2 Capacitive and Resistive Sensors

- 5.1.2 Touchless Gesture Recognition

- 5.1.2.1 2-D Camera-based

- 5.1.2.2 3-D Depth and ToF

- 5.1.2.3 Ultrasonic and mm-wave Radar

- 5.1.1 Touch-based Gesture Recognition

- 5.2 By Component

- 5.2.1 Hardware (Sensors, Controllers, SoCs)

- 5.2.2 Software (ML Algorithms, SDKs, Middleware)

- 5.3 By Gesture Type

- 5.3.1 Online Dynamic Gestures

- 5.3.2 Offline Static Gestures

- 5.4 By Authentication

- 5.4.1 Biometric (Face, Iris, Palm-vein)

- 5.4.2 Non-biometric (Motion, Pose)

- 5.5 By End-user Industry

- 5.5.1 Consumer Electronics

- 5.5.1.1 Smartphones and Tablets

- 5.5.1.2 Smart-TV and Set-top Boxes

- 5.5.1.3 AR/VR and Wearables

- 5.5.2 Automotive

- 5.5.2.1 Driver Monitoring and Infotainment

- 5.5.3 Aerospace and Defense

- 5.5.4 Healthcare

- 5.5.4.1 Surgical and Diagnostic Rooms

- 5.5.5 Gaming and Entertainment

- 5.5.6 Industrial and Robotics

- 5.5.7 Other Industries

- 5.5.1 Consumer Electronics

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 New Zealand and Australia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.6.5.2 Turkey

- 5.6.5.3 South Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Qualcomm Technologies Inc.

- 6.4.3 Apple Inc.

- 6.4.4 Microsoft Corp.

- 6.4.5 Sony Group Corp.

- 6.4.6 Google LLC

- 6.4.7 Meta Platforms Inc.

- 6.4.8 Ultraleap Ltd.

- 6.4.9 Microchip Technology Inc.

- 6.4.10 Infineon Technologies AG

- 6.4.11 Synaptics Inc.

- 6.4.12 Elliptic Laboratories AS

- 6.4.13 GestureTek Inc.

- 6.4.14 Cognitec Systems GmbH

- 6.4.15 Eyesight Technologies Ltd.

- 6.4.16 PointGrab Ltd.

- 6.4.17 Omron Corporation

- 6.4.18 Jabil Inc.

- 6.4.19 Leap Motion

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

手势姿态辨识市场机会、成长要素、产业趋势分析及2026年至2035年预测

手势姿态辨识市场机会、成长要素、产业趋势分析及2026年至2035年预测 全球手势姿态辨识市场规模、份额、趋势和成长分析报告(2026-2034)

全球手势姿态辨识市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球桌面和可携式个人电脑(PC)手势姿态辨识技术市场报告

2026年全球桌面和可携式个人电脑(PC)手势姿态辨识技术市场报告 汽车手势姿态辨识市场-全球产业规模、份额、趋势、机会及预测(依技术、应用、区域及竞争格局划分,2021-2031年)

汽车手势姿态辨识市场-全球产业规模、份额、趋势、机会及预测(依技术、应用、区域及竞争格局划分,2021-2031年) 手势姿态辨识市场规模、份额和成长分析(按组件、技术、类型、认证方法、最终用途和地区划分)-2026-2033年产业预测

手势姿态辨识市场规模、份额和成长分析(按组件、技术、类型、认证方法、最终用途和地区划分)-2026-2033年产业预测 汽车手势姿态辨识市场规模、份额和成长分析(按类型、产品类型、分销管道、应用、技术、产品和地区划分)—产业预测(2026-2033 年)

汽车手势姿态辨识市场规模、份额和成长分析(按类型、产品类型、分销管道、应用、技术、产品和地区划分)—产业预测(2026-2033 年) 全球石墨烯电子产品市场:预测(至2032年)-按材料类型、製造方法、应用、最终用户和地区分類的分析

全球石墨烯电子产品市场:预测(至2032年)-按材料类型、製造方法、应用、最终用户和地区分類的分析 手势姿态辨识市场(按技术、产品、部署模式、应用和最终用户划分)—全球预测 2025-20322032 年基于二维材料的电子市场预测:按产品类型、材料类型、製造技术、应用和地区进行的全球分析

手势姿态辨识市场(按技术、产品、部署模式、应用和最终用户划分)—全球预测 2025-20322032 年基于二维材料的电子市场预测:按产品类型、材料类型、製造技术、应用和地区进行的全球分析 手势辨识市场规模、份额、趋势及预测(依技术、最终用途产业及地区),2025 年至 2033 年

手势辨识市场规模、份额、趋势及预测(依技术、最终用途产业及地区),2025 年至 2033 年