|

市场调查报告书

商品编码

1851335

胺类:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)Amines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

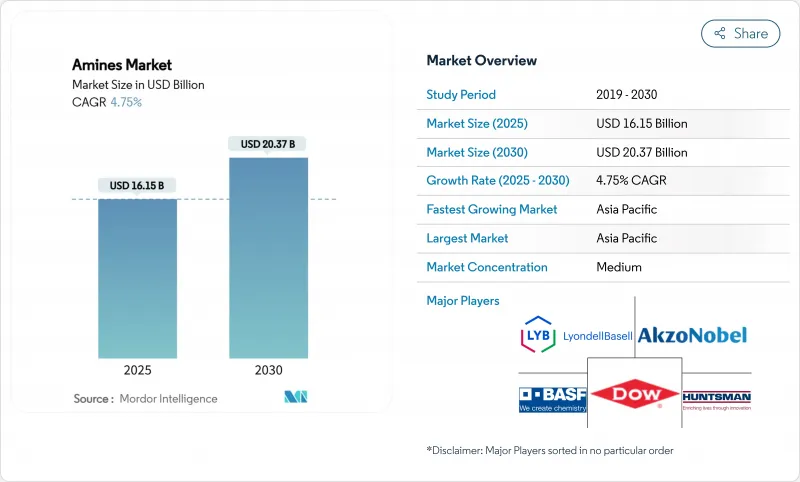

预计到 2025 年,胺类物质市场规模将达到 161.5 亿美元,到 2030 年将达到 203.7 亿美元,预测期(2025-2030 年)复合年增长率为 4.75%。

强劲的工业需求、有利于清洁化学品的日益严格的环境法规以及不断增长的高价值应用(例如碳捕获溶剂)项目,共同支撑了胺类市场的持续扩张。半导体製造领域的投资增加、大规模农业的现代化以及生物基个人护理界面活性剂的广泛应用,都为胺类市场带来了更大的规模和价值增长机会。生产商正透过提高能源效率和整合可再生原料来应对氨和乙烯价格的波动,同时遵守主要经济体新兴的挥发性有机化合物法规。领先的供应商也在加大对超高纯度电子级胺产能的投入,以满足下一代晶片对金属的严格要求,这凸显了胺类生产正从大宗商品生产向利润空间更大的特种解决方案的显着转变。

全球胺类市场趋势与洞察

亚洲个人护理产品配方师的需求激增

自2010年以来,胺基酸界面活性剂的市占率已超越传统硫酸盐界面活性剂,年均成长率高达18%。亚洲配方师凭藉麸胺酸和丙氨酸界面活性剂的温和性和生物降解性占据主导地位,这促使胺类界面活性剂生产商通过国际永续性和碳认证(ISCC-PLUS)拓展其生物基产品线。诺力昂(Nouryon)获得认证的绿色环氧乙烷和乙醇胺生产线,展现了工厂营运商如何调整产品组合,转向洁净标示配方。同时,多功能胺氧化物在洗髮精、沐浴露和家居用品领域也日益普及,因为生产商追求的是高发泡且温和的特性。随着中产阶级消费者越来越倾向于选择天然成分含量接近100%的产品,胺类界面活性剂市场有望进一步巩固其作为亚洲蓬勃发展的清洁美容生态系统关键推动者的地位。

新兴农业中心快速采用杀虫剂

亚太和南美洲的现代农业实践需要精准的化学投入,从而推动了对胺类农业化学盐和乳化剂的需求。采用可再生电力动力来源的新型分散式氨厂正在降低物流成本,并提高区域供应安全,尤其是在巴西和印度。 CF Industries 和 POET 的低碳氨肥初步试验展示了整合绿色氢能途径所带来的农艺和永续性优势。这些进展有助于提高用于除草剂、杀虫剂和种子处理剂的乙醇胺、烷基胺和脂族胺的长期市场需求。

转向非木质纸张和数位文件的转变

已开发国家办公用纸消费量的下降正在削弱对胺基纸浆漂白剂和纸张被覆剂的需求。为了缓解这种长期拖累,各公司正将销售量转移到成长更快的个人护理和建筑领域。BASF决定将其传统的胺类资产重新定位到特种化学品领域,凸显了该行业积极应对这一结构性变化的倡议。

细分市场分析

由于乙醇胺在气体脱硫剂、个人护理界面活性剂和腐蚀抑制剂等领域发挥至关重要的作用,预计到2024年,乙醇胺将占胺类市场总量的42.55%。天然气加工和三乙醇胺基水泥添加剂的稳定需求支撑着该市场强劲的基准,即便在碳捕获溶剂等领域出现了新的应用。此细分市场规模庞大,使得主要供应商能够充分利用成本优势和业务协同效应,涵盖从乙氧基化物到吗福林的整个衍生性商品链。相较之下,受电子、製药和先进复合材料等细分应用领域的推动,特种胺预计将在2030年之前以5.01%的复合年增长率实现最快成长。

生产商正在安装多功能反应器,以便在高纯度吗福林、二胺和手性胺中间体之间快速切换。赢创在南京的扩建计画正是这种向高附加价值分子转型的一个例证。同时,诸如钌/三磷酸催化剂等学术突破可望扩大特种胺的永续原料来源,该催化剂利用可再生原料即可实现90%的产率。乙醇胺规模化生产与特种胺市场成长之间的相互作用,为胺类市场长期的平衡发展轨迹提供了支撑。

区域分析

亚太地区继续保持其双重领先地位,2024年占全球销售额的38.91%,并预计到2030年将以5.88%的复合年增长率持续增长。中国4552万吨的氨产能巩固了该地区的原料优势。印度的特种化学品领军企业,包括Alkyl Amines和Balaji Amines,拥有20多家工厂,产品出口到100多个国家,充分发挥了其成本优势。台湾、韩国和中国当地半导体产业的扩张推动了对电子级胺的需求,而东南亚国协在医药、农业化学品和日用产品领域也实现了进一步成长。BASF计划投资100亿美元建设湛江一体化计划,该项目将完全使用可再生能源电力,这表明跨国公司正积极寻求把握该地区持续的成长潜力。

北美是一个成熟且具有重要战略意义的丛集,对整合碳捕获系统的蓝氨设施的投资不断增加。预计到2030年,美国的氨产能将成长四倍。这项扩张将保障国内化肥供应,并为乙醇胺和尿素衍生物提供本地原料。同时,加拿大丰富的水力资源使其成为低碳胺生产领域的有力竞争者,其产品面向国内和出口市场。

欧洲持续推动循环经济目标,推动生物基中间体和节能反应器的创新。诺力昂绿色环氧乙烷获得ISCC-PLUS认证,满足了欧洲对生态标籤界面活性剂的区域需求。欧盟委员会日益严格的VOC排放目标促使配方师以符合性能标准的高闪点衍生物取代传统的挥发性胺。中东和非洲受益于天然气原料的供应,尤其是在沙乌地阿拉伯和阿曼,这使得氨及其下游胺类产品的价格更具竞争力。在南美洲,大豆和玉米种植蓬勃发展,确保了巴西和阿根廷对除草剂胺盐的稳定需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲对个人护理配方师的需求激增

- 新兴农业中心农药的快速扩散

- 基础建设热潮刺激建筑化学品需求

- 用于尖端半导体工厂的电子级胺

- 现场绿色氢衍生先导计画

- 市场限制

- 转向非木质纸张和数位文件的转变

- 挥发性氨和乙烯原料定价

- 更严格的胺类挥发性有机化合物/气味法规

- 价值链分析

- 监管环境

- 技术展望

- 目前技术

- 沸石催化甲胺工艺

- 异丁烯的直接胺化

- 催化蒸馏

- EDC氨解

- 未来科技

- 目前技术

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 定价分析

- 生产分析

第五章 市场规模与成长预测

- 按类型

- 乙胺

- 烷基胺

- 脂肪胺

- 特种胺

- 乙醇胺

- 按最终用途行业划分

- 橡皮

- 个人保健产品

- 清洁产品

- 黏合剂、油漆、树脂

- 农业化学品

- 石油/石化

- 其他最终用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Air Products and Chemicals, Inc.

- Akzo Nobel NV

- Alkyl Amines Chemicals Limited

- Arkema

- BASF SE

- Celanese Corporation

- Clariant

- Daicel Corporation

- Dow

- Eastman Chemical Company

- Huntsman International LLC

- INEOS

- Invista

- Kemipex

- LyondellBasell Industries Holdings BV

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- NIPPON SHOKUBAI CO., LTD.

- SABIC

- Solvay

- Tosoh Corporation

第七章 市场机会与未来展望

The Amines Market size is estimated at USD 16.15 billion in 2025, and is expected to reach USD 20.37 billion by 2030, at a CAGR of 4.75% during the forecast period (2025-2030).

This sustained expansion is supported by resilient industrial demand, stricter environmental regulations that favor cleaner chemistries and a growing pipeline of high-value applications such as carbon-capture solvents. Rising investments in semiconductor fabrication, large-scale agricultural modernization and widespread adoption of bio-based personal-care surfactants are expanding both volume and value opportunities in the amines market. Producers are improving energy efficiency and integrating renewable feedstocks to manage volatile ammonia and ethylene prices while complying with emerging volatile organic compound limits across major economies. Leading suppliers are also channeling capital toward ultra-pure electronics-grade capacities to meet the stringent metal specifications required by next-generation chips, highlighting a visible shift from commodity production toward specialized solutions that offer superior margin potential.

Global Amines Market Trends and Insights

Surging Demand from Asian Personal-Care Formulators

Amino acid-based surfactants have outpaced traditional sulfate systems, recording 18% average annual growth since 2010. Asian formulators are mainstreaming glutamate and alaninate derivatives that offer low irritation and high biodegradability, forcing amine suppliers to expand bio-based lines with International Sustainability and Carbon Certification (ISCC-PLUS) credentials. Nouryon's certified production of green ethylene oxide and ethanolamines illustrates how plant operators are realigning portfolios toward clean-label formulations. In tandem, multifunctional amine oxides are gaining ground in shampoo, body-wash and household categories as manufacturers pursue high-foaming yet mild profiles. With middle-class consumers gravitating toward products boasting a natural-origin index approaching 100%, the amines market is set to deepen its role as a pivotal enabler of Asia's fast-growing clean-beauty ecosystem.

Rapid Pesticide Adoption in Emerging Agriculture Hubs

Modern farming practices in Asia Pacific and South America require precision chemical inputs, lifting demand for amine-based pesticide salts and emulsifiers. Novel decentralized ammonia plants powered by renewable electricity are lowering logistics costs and improving regional supply security, notably in Brazil and India. CF Industries and POET's pilot of low-carbon ammonia fertilizer demonstrates the agronomic and sustainability pay-off of integrating green hydrogen pathways. Such developments bolster long-term offtake for ethanolamines, alkylamines and fatty amines used in herbicides, insecticides and seed-treatment agents.

Shift to Wood-Free Paper & Digital Documentation

Declining office-paper consumption in developed economies is dampening demand for amine-based pulp bleaching agents and paper coatings. Companies are reallocating volumes toward faster-growing personal-care and construction segments to cushion the long-term drag. BASF's decision to reconfigure legacy amine assets toward specialty chemicals highlights the industry's proactive adjustment to this structural shift.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Boom Spurring Construction Chemicals

- Electronics-Grade Amines for Advanced Semiconductor Fabs

- Volatile Ammonia & Ethylene Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethanolamines captured 42.55% of the overall amines market in 2024, owing to their indispensable role in gas sweetening, personal-care surfactants and corrosion inhibitors. Steady demand from natural-gas treatment and triethanolamine-based cement additives underpins a robust baseline, even as newer uses in carbon-capture solvents emerge. The segment's scale gives leading suppliers cost leverage and operational synergies across derivative chains ranging from ethoxylates to morpholine. In contrast, specialty amines are projected to post the fastest 5.01% CAGR through 2030, propelled by niche applications in electronics, pharmaceuticals and advanced composites.

Producers are installing multipurpose reactors capable of quick changeovers between high-purity morpholines, diamines and chiral amine intermediates. Evonik's expansion in Nanjing exemplifies this pivot toward higher value-added molecules. Concurrently, academic breakthroughs such as ruthenium/triphos catalysts achieving 90% yields on renewable feedstocks promise to widen the sustainable feedstock pool for specialty grades. The interplay of scale in ethanolamines and growth in specialty amines underpins the balanced long-term trajectory of the amines market.

The Amines Market Report is Segmented by Type (Ethyleneamines, Alkylamines, Fatty Amines, Specialty Amines, Ethanolamines), End-Use Industry (Rubber, Personal Care Products, Cleaning Products, Adhesives/Paints/Resins, Agro-Chemicals, Oil/Petrochemicals, Other End-Uses), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained its dual leadership position, generating 38.91% of global revenue in 2024 and expanding at a 5.88% CAGR through 2030. China's 45.52 million t ammonia capacity anchors the region's raw-material advantage. India's specialty chemicals champions, including Alkyl Amines and Balaji Amines, operate more than 20 plants and export to over 100 countries, leveraging cost-competitive manufacturing. Semiconductor expansions across Taiwan, South Korea and mainland China are pushing demand for electronics-grade amines, while ASEAN nations add incremental growth through pharmaceuticals, agro chemicals and household products. BASF's planned USD 10 billion Zhanjiang Verbund project, powered entirely by renewable electricity, illustrates how multinationals intend to capture enduring regional upside.

North America represents a mature yet strategically vital cluster, with rising investments in blue ammonia facilities integrated with carbon-capture systems. The United States is expected to quadruple ammonia capacity by 2030. This expansion safeguards domestic fertilizer supply and provides a local feedstock base for ethanolamine and urea derivatives. Meanwhile, Canada's abundant hydropower positions it as a contender for low-carbon amine production targeting both domestic and export markets.

Europe continues to pursue circular-economy objectives, driving innovations in bio-based intermediates and energy-efficient reactors. Nouryon's ISCC-PLUS certification for green ethylene oxide supports regional demand for eco-labeled surfactants. The European Commission's stricter VOC targets are encouraging formulators to substitute conventional volatile amines with higher-flashpoint derivatives that meet performance criteria. The Middle East and Africa benefit from natural-gas feedstock availability, enabling competitively priced ammonia and downstream amine chains, especially in Saudi Arabia and Oman. South America's focus on soybean and corn cultivation assures steady consumption of herbicidal amine salts, with Brazil and Argentina leading uptake.

- Air Products and Chemicals, Inc.

- Akzo Nobel N.V.

- Alkyl Amines Chemicals Limited

- Arkema

- BASF SE

- Celanese Corporation

- Clariant

- Daicel Corporation

- Dow

- Eastman Chemical Company

- Huntsman International LLC

- INEOS

- Invista

- Kemipex

- LyondellBasell Industries Holdings B.V.

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- NIPPON SHOKUBAI CO., LTD.

- SABIC

- Solvay

- Tosoh Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from Asian personal-care formulators

- 4.2.2 Rapid pesticide adoption in emerging agriculture hubs

- 4.2.3 Infrastructure boom spurring construction chemicals

- 4.2.4 Electronics-grade amines for advanced semiconductor fabs

- 4.2.5 On-site green-hydrogen-derived amines pilots

- 4.3 Market Restraints

- 4.3.1 Shift to wood-free paper and digital documentation

- 4.3.2 Volatile ammonia and ethylene feedstock pricing

- 4.3.3 Stricter amine VOC/odor regulations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Current Technologies

- 4.6.1.1 Zeolite-catalyzed methylamine processes

- 4.6.1.2 Direct amination of isobutylene

- 4.6.1.3 Catalytic distillation

- 4.6.1.4 Ammonolysis of EDC

- 4.6.2 Upcoming Technologies

- 4.6.1 Current Technologies

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Price Analysis

- 4.9 Production Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Ethyleneamines

- 5.1.2 Alkylamines

- 5.1.3 Fatty Amines

- 5.1.4 Specialty Amines

- 5.1.5 Ethanolamines

- 5.2 By End-use Industry

- 5.2.1 Rubber

- 5.2.2 Personal Care Products

- 5.2.3 Cleaning Products

- 5.2.4 Adhesives, Paints and Resins

- 5.2.5 Agro-Chemicals

- 5.2.6 Oil and Petrochemicals

- 5.2.7 Other End-uses

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Air Products and Chemicals, Inc.

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Alkyl Amines Chemicals Limited

- 6.4.4 Arkema

- 6.4.5 BASF SE

- 6.4.6 Celanese Corporation

- 6.4.7 Clariant

- 6.4.8 Daicel Corporation

- 6.4.9 Dow

- 6.4.10 Eastman Chemical Company

- 6.4.11 Huntsman International LLC

- 6.4.12 INEOS

- 6.4.13 Invista

- 6.4.14 Kemipex

- 6.4.15 LyondellBasell Industries Holdings B.V.

- 6.4.16 MITSUBISHI GAS CHEMICAL COMPANY, INC

- 6.4.17 NIPPON SHOKUBAI CO., LTD.

- 6.4.18 SABIC

- 6.4.19 Solvay

- 6.4.20 Tosoh Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

二异丙基乙胺市场:依形态、等级、应用及通路-2026-2032年全球预测

二异丙基乙胺市场:依形态、等级、应用及通路-2026-2032年全球预测 烷基胺市场规模、份额和成长分析:按形态、烷基胺类型、最终用途、通路、地区和产业预测,2026-2033年

烷基胺市场规模、份额和成长分析:按形态、烷基胺类型、最终用途、通路、地区和产业预测,2026-2033年 2026年全球儿茶酚胺市场报告

2026年全球儿茶酚胺市场报告 对苯二异氰酸酯市场分析及预测(至2035年):按类型、产品、应用、技术、组件、最终用户、製程、材料类型、安装类型和解决方案划分

对苯二异氰酸酯市场分析及预测(至2035年):按类型、产品、应用、技术、组件、最终用户、製程、材料类型、安装类型和解决方案划分 全球胺类市场规模、份额、趋势及成长分析报告(2026-2034年)

全球胺类市场规模、份额、趋势及成长分析报告(2026-2034年) Piperazine市场-全球产业规模、份额、趋势、机会、预测:按原料、应用、区域和竞争对手划分,2021-2031年胺类市场 - 全球产业规模、份额、趋势、机会及预测(依产品、应用、地区及竞争格局划分,2021-2031年)

Piperazine市场-全球产业规模、份额、趋势、机会、预测:按原料、应用、区域和竞争对手划分,2021-2031年胺类市场 - 全球产业规模、份额、趋势、机会及预测(依产品、应用、地区及竞争格局划分,2021-2031年) 2026-2030年全球异丙胺市场水溶性咪唑啉市场按类型、剂型、应用和最终用户划分,全球预测(2026-2032)

2026-2030年全球异丙胺市场水溶性咪唑啉市场按类型、剂型、应用和最终用户划分,全球预测(2026-2032) 对苯二胺市场规模、份额和成长分析(按应用、纯度等级、最终用途产业、销售管道和地区划分)-2026-2033年产业预测

对苯二胺市场规模、份额和成长分析(按应用、纯度等级、最终用途产业、销售管道和地区划分)-2026-2033年产业预测