|

市场调查报告书

商品编码

1851343

4K显示解析度:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030年)4K Display Resolution - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

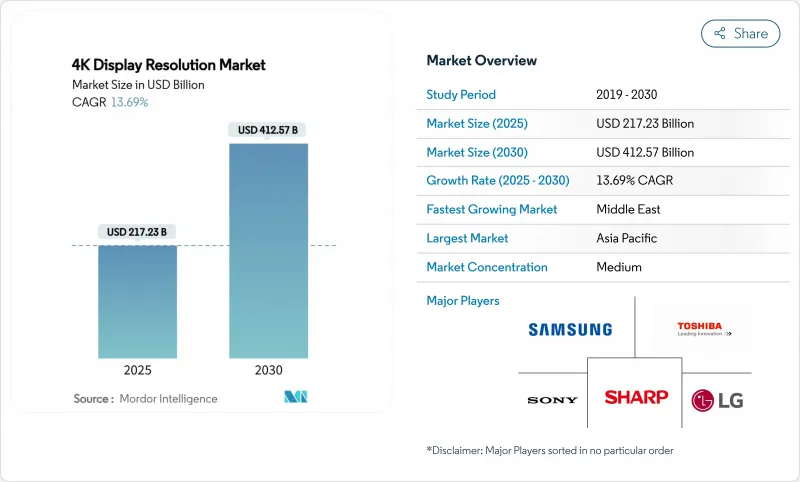

预计到 2025 年,4K 显示解析度市场价值将达到 2,172.3 亿美元,到 2030 年将达到 4,125.7 亿美元,年复合成长率为 13.69%。

面板成本的快速下降、原生4K串流内容的丰富供应以及不断扩展的企业应用场景,正推动这项技术从高端定位走向大众普及。亚太地区的製造能力维持了平均售价的低位,而该地区的消费者也明显偏好大萤幕。混合办公模式和身临其境型游戏的需求推动了产品更新换代的加速,促使各大品牌推出更多专业化型号。同时,晶片组供应链风险以及欧洲不断变化的能源效率法规,迫使供应商实现组件采购多元化,并加快低功耗背光技术的研发。

全球4K显示解析度市场趋势与洞察

北美地区OTT主导的4K串流媒体迅速普及

到2024年,串流媒体平台将以4K解析度提供超过60%的新内容,这将大大推动家庭升级,促使更多用户选择相容4K的萤幕。 Wi-Fi 7提供的更高频宽(支援高达46 Gbps的资料速率)消除了先前限制4K普及的瓶颈。日本正在推广毫米波频谱,目标是在2027年前建成5万个基地台,这将进一步提升网路容量,惠及跨国内容供应商。因此,电视和显示器的更换週期正在加快,串流媒体服务商也正围绕HDR效能和广色域来製定其功能蓝图。那些将面板发布与热门大片首映同步的品牌,在关键的销售季度到来之前,吸引了许多早期用户的注意。

中国和韩国的面板补贴和产能扩张

政府激励措施降低了新建液晶显示器(LCD)和量子点发光二极管(QD-OLED)生产线的资本成本,使得京东方科技(BOE Technology)和三星显示器(Samsung Display)等公司能够以高产运作运作其工厂。三星显示器计划在2025年将其QD-OLED显示器面板的出货量提高50%,达到143万片,这为其OEM合作伙伴更新高阶产品线提供了空间。这些投资带来的规模经济将支持在50-65英寸主流尺寸市场中保持价格竞争力,而mini-LED背光产量比率的降低将推动其在中阶机型中的应用。补贴主导的产量激增已经渗透到全球供应链,降低了下游组装商的材料成本。

HDMI 2.1晶片组短缺(2024-2025年)

主要晶圆代工厂晶圆出货量的限制导致HDMI 2.1重定时器和开关IC的供应不足,从而延缓了旗舰级游戏显示器和高阶电视的大规模出货。海迈科技(Himax Technologies)报告称,其2024年82.9%的收入将来自显示器驱动IC,这表明该公司对单一元件市场的依赖性较高。供应商已将稀缺晶片组转移到利润较高的型号上,导致中端SKU出现暂时性缺货。这种短缺也加速了DisplayPort 2.1的普及,例如微星(MSI)的新款QD-OLED显示器就采用了该接口,这表明即使供应恢復正常,接口多样化仍具有长期发展潜力。

细分市场分析

预计在4K显示器解析度市场中,游戏显示器将以最快的速度成长,2025年至2030年的复合年增长率(CAGR)将达到14.1%。三星在2024年保持了21.0%的全球市场份额,并在OLED细分市场占据了34.6%的份额,凭藉QD-OLED技术的兴起获得了先发优势。该细分市场蓬勃发展得益于高规格的电竞赞助、频繁的产品更新以及NVIDIA GeForce RTX 4090等高性能GPU的协同效应,这些GPU能够实现稳定的4K/144Hz游戏体验。显示器品牌正在透过更高的峰值亮度、双层OLED面板和DisplayPort 2.1介面等方式升级规格,以区分高阶产品。由于发烧友更注重反应时间、HDR对比和色彩还原,因此游戏显示器的盈利仍然高于主流电视。

智慧型电视将继续保持领先地位,预计到2024年将占据68%的市场份额,这主要得益于丰富的4K串流内容库和不断下降的物料清单成本。随着混合办公模式对广视角和高像素密度的需求日益增长,企业电视墙和数位指示牌萤幕的重要性也随之提升。医疗显示器开闢了一片利润丰厚的市场,例如SONY的LMD-32M1MD等4K手术显示器已达到VESA HDR1000标准,可用于手术室。原生4K解析度的智慧型手机和平板电脑由于功耗抵消了其行动优势,因此其应用范围仅限于创意类应用。总体而言,消费者对更丰富的娱乐体验和更有效率的办公室协作的需求正在推动4K显示解析度市场各个细分领域的成长。

OLED面板预计将以16.7%的复合年增长率成长,成为4K显示解析度市场中成长最快的产品。三星显示器计画在2025年出货143万块QD-OLED显示器面板,显示产能扩张正在推动OLED应用范围的拓展,使其超越旗舰电视的范畴。卓越的对比度、像素级调光和双OLED堆迭技术的引入,如今已应用于游戏显示器,从而推高了平均售价。 LG将于2025年推出的G5电视,配备165Hz原生更新率和微透镜阵列光学系统,凸显了OLED研发的持续推进。

由于模具数量庞大、供应链成熟以及在中阶产品中具有成本竞争力,LCD技术预计在2024年仍将维持71%的市场份额。 Mini-LED背光技术增加了局部调光和高亮度功能,以更低的成本缩小了与OLED的性能差距。SONY的HDR1000手术监视器展示了Mini-LED在专业垂直市场的影响力。正如海信的136吋显示器所证明的那样,在製造产量比率提高之前,Micro-LED的应用将仅限于超大尺寸规格。多种面板类型的共存将使游戏、指示牌和医疗保健等各种应用能够在不断增长的4K显示解析度市场中实现成本、亮度和使用寿命的最佳平衡。

区域分析

亚太地区巩固了其作为全球最大4K显示分辨率市场的地位,预计2024年将占全球收入的46%。中国的补贴政策促进了产能的快速扩张,而韩国在OLED领域的领先地位则为全球提供了高利润面板。日本设定了2027年安装5万个毫米波基地台的目标,旨在加强该地区的网路骨干,以支援4K串流媒体的广泛应用。随着平均售价下降和可支配收入增加,印度和东南亚进入了4K应用的新阶段,释放了尚未开发的市场潜力。

预计中东地区2025年至2030年的复合年增长率将达到13.6%,位居全球之首。海湾合作委员会(GCC)企业正在部署4K电视墙以增强混合协作,从而推动了对小像素间距LED组件的需求。SONY中东和非洲公司报告称,其销售额显着成长,并计划在2025年底前推出INZONE M9 4K显示器。目前,该地区20%的电视销售额已来自线上通路,迫使各大品牌优化其电商物流。

北美成熟的4K装置量持续成长,这主要得益于OTT内容的快速普及和游戏显示器强劲的升级换代週期。医疗机构扩大了4K诊断套件的应用,拓展了一个利润丰厚且受价格竞争影响较小的市场区隔。在欧洲,注重科技的消费者开始青睐更大尺寸的OLED电视,而更严格的环保设计标准则提高了65吋以上面板的合规成本,促使供应商转向节能的Mini-LED设计。拉丁美洲和非洲仍是新兴市场。儘管宽频普及率的提高预示着未来成长潜力,但撒哈拉以南非洲部分地区有限的4K广播频谱限制了其发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 北美地区OTT主导的4K串流媒体迅速普及

- 中国和韩国的面板补贴和产能扩张

- 欧洲电竞市场对4K/144Hz游戏显示器的需求

- 美国和日本对4K手术和诊断显示器的应用

- 混合工作LED电视墙引领波湾合作理事会国家企业采用

- 台湾製造的迷你LED灯可产生50-65英吋的产量比率

- 市场限制

- 2024-2025年HDMI 2.1晶片组短缺

- 欧盟生态设计规则提高了65吋电视的合规成本

- 撒哈拉以南非洲地区4K广播频谱有限

- 日本和韩国的高阶8K影片蚕食现象

- 生态系分析

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 智慧型电视

- 监视器

- 智慧型手机

- 药片

- 笔记型电脑

- 数位电子看板/电视墙

- 投影萤幕

- 头戴式显示器(HMD)

- 医疗显示器

- 其他的

- 透过面板技术

- LCD显示幕(IPS/VA/TN)

- 有机发光二极体

- 迷你LED

- 微型LED

- 其他的

- 按萤幕尺寸

- 32英吋或更小

- 32-49 英寸

- 50-65英寸

- 66-84英寸

- 84吋或以上

- 按最终用户行业划分

- 家用电器(家用)

- 游戏和电竞场馆

- 商业与教育

- 零售和广告

- 媒体与娱乐製作

- 卫生保健

- 航太/国防

- 其他的

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家(丹麦、瑞典、挪威、芬兰)

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 东南亚

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略倡议与发展

- 市占率分析

- 公司简介

- Samsung Electronics Co. Ltd

- LG Display Co. Ltd

- BOE Technology Group Co. Ltd

- TCL Technology(CSOT)

- Sony Group Corporation

- Toshiba Corporation

- Panasonic Holdings Corporation

- Sharp Corporation

- Hisense Group

- Koninklijke Philips NV

- Innolux Corporation

- AU Optronics Corp.

- Dell Technologies Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Vizio Inc.

- Skyworth Group Ltd

- Barco NV

- Eizo Corporation

- ViewSonic Corporation

- BenQ Corporation

第七章 市场机会与未来展望

The 4K display resolution market size is estimated at USD 217.23 billion in 2025 and is forecast to reach USD 412.57 billion by 2030, advancing at a 13.69% CAGR.

Fast-declining panel costs, a richer supply of native 4K streaming content, and expanding corporate use cases are allowing the technology to move from premium positioning into mass adoption. Asia Pacific's manufacturing scale keeps average selling prices low while the region's consumers display a marked preference for larger screens. Hybrid-work demand and immersive gaming are further tightening refresh cycles, encouraging brands to launch increasingly specialized models. At the same time, supply chain risks around chipsets and evolving energy-efficiency rules in Europe urge vendors to diversify component sourcing and accelerate R&D in low-power backlighting.

Global 4K Display Resolution Market Trends and Insights

Rapid OTT-led Uptake of 4K Streaming in North America

Streaming platforms delivered more than 60% of their new content in 4K during 2024, setting a stronger pull for compatible screens in household upgrades. Bandwidth gains from Wi-Fi 7, which supports data rates up to 46 Gbit/s, remove the previous bottlenecks that limited mainstream 4K adoption. Millimeter-wave rollouts, with Japan targeting 50,000 base stations by 2027, add further capacity that benefits cross-border content providers. The result is a steeper replacement cycle for television sets and monitors, with streaming services shaping feature roadmaps around HDR performance and wider color gamuts. Brands that synchronize panel launches with blockbuster content premieres are capturing early-adopter interest ahead of key sales quarters.

Panel Subsidies and Capacity Expansion in China and South Korea

Government incentives trimmed capital costs for new LCD and QD-OLED lines, enabling firms such as BOE Technology and Samsung Display to run plants at high utilization. Samsung Display plans to raise QD-OLED monitor panel shipments by 50% to 1.43 million units in 2025, giving OEM partners more scope to refresh premium catalogs. Economies of scale flowing from these investments support competitive pricing in the 50-65" mainstream sweet spot, while yield-driven cost erosion in Mini-LED backlights widens adoption in mid-tier models. The subsidy-induced volume surge is already filtering through global supply chains, lowering bill-of-materials outlays for downstream assemblers.

HDMI 2.1 Chipset Shortages 2024-25

Constrained wafer starts at leading foundries have a limited supply of HDMI 2.1 retimer and switch ICs, delaying volume shipments of flagship gaming monitors and high-end TVs. Himax Technologies reported that 82.9% of 2024 revenue came from display driver ICs, underscoring dependence on a narrow component pool. Vendors redirected scarce chipsets to models with higher gross margins, creating temporary stockouts in mid-tier SKUs. The scarcity also accelerated DisplayPort 2.1 adoption, as seen in MSI's new QD-OLED monitor, signaling possible long-term interface diversification even after supply normalizes.

Other drivers and restraints analyzed in the detailed report include:

- Esports Demand for 4K/144 Hz Gaming Monitors in Europe

- Adoption of 4K Surgical and Diagnostic Displays in U.S. and Japan

- EU Eco-design Rules Raising Compliance Costs for >65" TVs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gaming monitors accounted for a 14.1% CAGR forecast between 2025 and 2030, the fastest trajectory within the 4K display resolution market. Samsung upheld a 21.0% global share in 2024, while its 34.6% slice of the OLED sub-segment confirmed a first-mover advantage in emerging QD-OLED stacks. The segment thrives on esports sponsorship visibility, frequent model refreshes, and the synergy with powerful GPUs such as NVIDIA GeForce RTX 4090 that unlocked stable 4K/144 Hz gameplay. Monitor brands elevate specifications with higher peak brightness, tandem OLED layers, and DisplayPort 2.1 input to differentiate premium SKUs. Profitability remains thicker than mainstream TVs because enthusiast buyers value response time, HDR contrast, and color coverage.

Smart TVs preserved leadership with a 68% revenue share in 2024, supported by wide 4K streaming content libraries and falling BOM costs. Corporate video walls and digital signage screens gained importance as hybrid-work hubs required wide viewing angles and high pixel density. Medical displays formed a high-margin niche, with 4K surgical monitors like Sony's LMD-32M1MD achieving VESA HDR1000 compliance for operating theaters. Smartphones and tablets with native 4K remain limited to creator-focused uses because energy draw offsets mobile benefits. Overall, consumer appetite for richer entertainment and workplace collaboration sustains multi-segment momentum within the 4K display resolution market.

OLED panels are projected to expand at a 16.7% CAGR, the swiftest run in the 4K display resolution market. Samsung Display's plan to ship 1.43 million QD-OLED monitor panels in 2025 exemplifies the capacity scaling that propels wider use beyond flagship TVs. Superior contrast, pixel-level dimming, and the introduction of tandem OLED stacks now reach gaming monitors, encouraging ASP premiums. LG's 2025 G5 TV, with a 165 Hz native refresh and Micro Lens Array optics, underscores the continued pace of OLED R&D.

LCD technology retained 71% share in 2024 because of vast installed tooling, mature supply chains, and cost competitiveness for mid-range sets. Mini-LED backlighting adds local dimming and higher luminance, bridging performance gaps with OLED at a lower cost. Sony's HDR1000-rated surgical monitor demonstrates Mini-LED influence in specialty verticals. Micro-LED remains confined to ultra-large formats, evidenced by Hisense's 136-inch showpiece, until manufacturing yields improve. The coexistence of multiple panel types ensures that each application - gaming, signage, healthcare - receives an optimal balance of cost, brightness, and longevity within the expanding 4K display resolution market.

The 4K Display Resolution Market Report is Segmented by Product Type (Smart TV, Monitor, Smartphone, Tablet, and More), Panel Technology (LCD, OLED, Mini-LED, and Micro-LED), Screen Size (Sub 32 Inch, 32-49 Inch, 50-65 Inch, 66-84 Inch, and Above 85 Inch), End-User Vertical (Consumer Electronics, Gaming and Esports Venues, Business and Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 46% of 2024 revenue, cementing its position as the largest territory in the 4K display resolution market. China's subsidies enabled swift capacity ramps, while South Korea's OLED leadership supplied high-margin panels globally. Japan's goal of installing 50,000 millimeter-wave bases by 2027 reinforces the regional network backbone supporting 4K streaming uptake. India and Southeast Asia entered a new adoption phase as falling ASPs aligned with rising discretionary income, unlocking large untapped volumes.

The Middle East is forecast to post the highest CAGR at 13.6% between 2025 and 2030. GCC corporations rolled out 4K video walls to enhance hybrid collaboration, boosting demand for fine-pixel-pitch LED assemblies. Sony Middle East and Africa reported notable sales gains and aims to release the INZONE M9 4K monitor within 2025, reflecting the region's appetite for premium displays. Online channels have already captured 20% of regional TV sales, prompting brands to fine-tune e-commerce logistics.

North America's mature installed base still grew on the back of fast OTT content adoption and a robust gaming monitor upgrade cycle. Healthcare institutions expanded to 4K diagnostic suites, widening a lucrative sub-segment less exposed to price wars. Europe faced a dual narrative: tech-savvy consumers embraced larger OLED sets while stricter Eco-design norms raised compliance costs for panels over 65", nudging suppliers toward energy-efficient Mini-LED designs. Latin America and Africa remained emergent frontiers; limited 4K broadcast spectrum in parts of Sub-Saharan Africa tempered growth, though rising broadband coverage signals future upside.

- Samsung Electronics Co. Ltd

- LG Display Co. Ltd

- BOE Technology Group Co. Ltd

- TCL Technology (CSOT)

- Sony Group Corporation

- Toshiba Corporation

- Panasonic Holdings Corporation

- Sharp Corporation

- Hisense Group

- Koninklijke Philips N.V.

- Innolux Corporation

- AU Optronics Corp.

- Dell Technologies Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Vizio Inc.

- Skyworth Group Ltd

- Barco NV

- Eizo Corporation

- ViewSonic Corporation

- BenQ Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid OTT?led Uptake of 4K Streaming in North America

- 4.2.2 Panel Subsidies and capacity Expansion in China and South Korea

- 4.2.3 Esports Demand for 4K/144 Hz Gaming Monitors in Europe

- 4.2.4 Adoption of 4K Surgical and Diagnostic Displays in United States and Japan

- 4.2.5 Hybrid-Work LED Videowalls Driving Gulf Cooperation Council Countries Corporate Installations

- 4.2.6 Mini-LED Yield-Driven Price Erosion in Taiwan-made 50-65? Panels

- 4.3 Market Restraints

- 4.3.1 HDMI 2.1 Chipset Shortages 2024-25

- 4.3.2 EU Ecodesign Rules Raising Compliance Costs for Above 65? TVs

- 4.3.3 Limited 4K Broadcast Spectrum in Sub-Saharan Africa

- 4.3.4 Premium 8K Cannibalisation in Japan and South Korea

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Smart TV

- 5.1.2 Monitor

- 5.1.3 Smartphone

- 5.1.4 Tablet

- 5.1.5 Laptop

- 5.1.6 Digital Signage/Videowall

- 5.1.7 Projection Screen

- 5.1.8 Head-Mounted Display (HMD)

- 5.1.9 Medical Display

- 5.1.10 Others

- 5.2 By Panel Technology

- 5.2.1 LCD (IPS/VA/TN)

- 5.2.2 OLED

- 5.2.3 Mini-LED

- 5.2.4 Micro-LED

- 5.2.5 Others

- 5.3 By Screen Size

- 5.3.1 Below 32 inch

- 5.3.2 32-49 inch

- 5.3.3 50-65 inch

- 5.3.4 66-84 inch

- 5.3.5 Above 84 inch

- 5.4 By End-user Vertical

- 5.4.1 Consumer Electronics (Household)

- 5.4.2 Gaming and Esports Venues

- 5.4.3 Business and Education

- 5.4.4 Retail and Advertisement

- 5.4.5 Media and Entertainment Production

- 5.4.6 Healthcare

- 5.4.7 Aerospace and Defence

- 5.4.8 Others

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Gulf Cooperation Council Countries

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co. Ltd

- 6.4.2 LG Display Co. Ltd

- 6.4.3 BOE Technology Group Co. Ltd

- 6.4.4 TCL Technology (CSOT)

- 6.4.5 Sony Group Corporation

- 6.4.6 Toshiba Corporation

- 6.4.7 Panasonic Holdings Corporation

- 6.4.8 Sharp Corporation

- 6.4.9 Hisense Group

- 6.4.10 Koninklijke Philips N.V.

- 6.4.11 Innolux Corporation

- 6.4.12 AU Optronics Corp.

- 6.4.13 Dell Technologies Inc.

- 6.4.14 ASUSTeK Computer Inc.

- 6.4.15 Acer Inc.

- 6.4.16 Vizio Inc.

- 6.4.17 Skyworth Group Ltd

- 6.4.18 Barco NV

- 6.4.19 Eizo Corporation

- 6.4.20 ViewSonic Corporation

- 6.4.21 BenQ Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

超高清环境光防反射萤幕市场(按产品类型、应用、最终用户和分销管道划分),全球预测(2026-2032年)

超高清环境光防反射萤幕市场(按产品类型、应用、最终用户和分销管道划分),全球预测(2026-2032年) 2026年全球4K超短焦雷射电视投影机市场报告4K 超高清 USB 网路摄影机市场:按感测器类型、价格范围、连接类型、影格速率、自动对焦支援、应用、最终用户和分销管道划分 - 全球预测 2026-2032 年

2026年全球4K超短焦雷射电视投影机市场报告4K 超高清 USB 网路摄影机市场:按感测器类型、价格范围、连接类型、影格速率、自动对焦支援、应用、最终用户和分销管道划分 - 全球预测 2026-2032 年 4K显示器市场规模、份额和成长分析(按产品类型、解析度、技术、最终用户、分销管道和地区划分)-产业预测(2026-2033年)

4K显示器市场规模、份额和成长分析(按产品类型、解析度、技术、最终用户、分销管道和地区划分)-产业预测(2026-2033年) 超高清4K面板市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

超高清4K面板市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 4K 显示解析度市场报告,按产品类型(显示器、智慧电视、智慧型手机等)、最终用户(航太和国防、商业和教育、娱乐和媒体、零售和广告等)和地区划分,2025 年至 2033 年4K 显示解析度市场 - 按产品(摄影机、数位相机、智慧电视、显示器、智慧型手机和平板电脑)、按解析度、按应用和预测,2024 年至 2032 年

4K 显示解析度市场报告,按产品类型(显示器、智慧电视、智慧型手机等)、最终用户(航太和国防、商业和教育、娱乐和媒体、零售和广告等)和地区划分,2025 年至 2033 年4K 显示解析度市场 - 按产品(摄影机、数位相机、智慧电视、显示器、智慧型手机和平板电脑)、按解析度、按应用和预测,2024 年至 2032 年