|

市场调查报告书

商品编码

1851351

变频器:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Variable Frequency Drives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

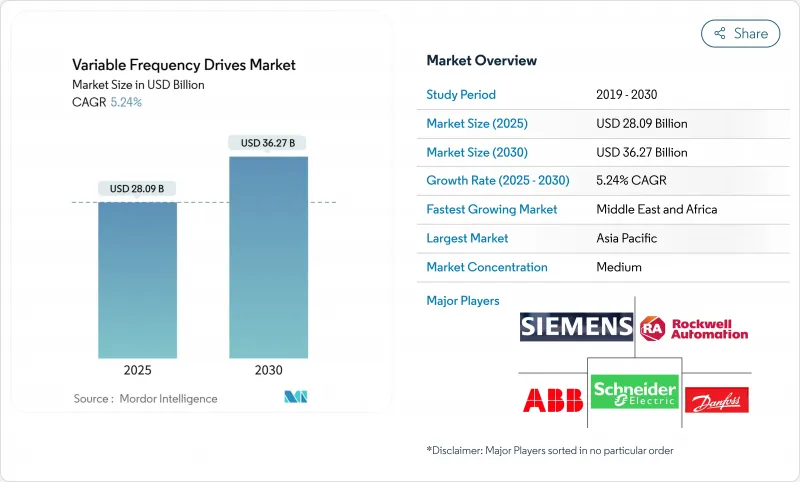

全球变频器市场预计到 2025 年将达到 280.9 亿美元,到 2030 年将达到 362.7 亿美元,年复合成长率为 5.24%。

对马达级能效的强劲政策压力、节能带来的快速回报以及向数位化生产线的转型,正稳步扩大变频器的应用范围。即使在资本支出週期趋紧的情况下,市场需求仍然强劲,因为变频器维修能够立即降低高耗能工厂的电力成本。采矿和金属行业的中压升级计划、中东地区的海水淡化厂建设以及商业建筑中暖通空调(HVAC)能源效率的强制性要求,都为变频器的应用提供了更多机会。将乙太网路、网路安全安全功能和碳化硅开关元件整合到产品组合中的供应商,保护了利润率并确保了业务收益。碳化硅/氮化镓晶片短缺和不断上涨的电磁干扰合规成本带来的不利因素抑制了变频器的出货量成长,但并未阻碍多年来持续的能源效率投资。

全球变频器市场趋势与洞察

寻求马达级能耗优化的数位原民製程装置

数位化工厂依靠现代变频器 (VFD) 内部的预测分析功能,根据生产计划和即时电价调整马达负载。例如,罗克韦尔自动化的 PowerFlex 755TS 平台整合了边缘分析功能,可在降低多条马达生产线能耗的同时减少停机时间。半导体製造和製药工厂率先采用了这项技术,因为产量比率取决于精确的速度控制和不间断的服务连接。

暖通空调和水系统强制性可变扭矩效率规则

能源效率法规使得在泵浦和空气调节机中整合变频器成为一项不容商榷的措施。美国能源局2028年发布的《循环泵浦规则》强制要求使用电子换向马达和先进的驱动器。为此,特灵等原始设备製造商已与丹佛斯签订了多年采购协议,以确保符合规定的变频器供应。

690V以上电压的电磁干扰/谐波合规成本不断上升

随着监管机构收紧 IEEE 519 标准对 690V 以上电压等级的限制,与电磁干扰和谐波失真相关的合规成本飙升。中压计划需要使用更大容量的电抗器、多脉衝变压器和屏蔽电缆,这增加了材料、试运行和工程成本,可能导致已安装驱动器的成本增加 15% 甚至更多。小型製造商受到的影响尤其严重,因为它们必须将设计和认证成本分摊到较少的出货量上,这可能会阻碍新进入者,并加速行业整合。

细分市场分析

1 kV 以下的低压变频器仍是中小型工厂输送机、搅拌机和暖通空调风扇控制的主要设备。到 2024 年,低压变频器将占据 62.4% 的市场份额,从而支撑变频驱动器市场的发展。经济高效的安装、丰富的整合商经验和广泛的供应商资源使其保持了市场份额。同时,钢铁厂和地下矿场的扩建项目促使采购转向 1-6 kV 的解决方案,推动中压变频器市场以 6.8% 的复合年增长率成长。升级到 995 V 电网的矿场选择专用变频器来减少电缆敷设并提高电压稳定性。

预计到2030年,中压变频驱动市场规模将达到104亿美元,这得益于可再生能源併网推动了电网规范对谐波抑制的要求。供应商积极响应,推出了耐电弧机壳和模组化主动前端设计,将总谐波失真控制在3%以下。 6千伏特以上的高压产品主要面向水泵和轧延等特定计划,但由于价格高且安装复杂,其应用受到限制。

功率低于 20 kW 的超紧凑型驱动器实现了最高的复合年增长率 (CAGR),达到 7.2%,这主要得益于工厂采用分散式控制技术,将小型马达整合到自主移动机器人和智慧建筑子系统中。此外,随着配备丰富感测器的暖通空调分区控制系统和食品加工送料器的应用,此类驱动器的出货量也随之成长。低功率(20-200 kW)型号预计仍将贡献 2024 年 40.3% 的收入,对于化学和水源产业的离心式帮浦和轴流风机至关重要。

开发商提高了散热器容量并改用碳化硅二极管,从而提高了环境温度高于 60°C 时的工作极限,这在沙漠太阳能领域是一项差异化优势。虽然高功率级(600 kW 以上)变频驱动器的市场份额不足 5%,但每笔销售都透过长期服务合约带来了可观的售后收入,其中包括对功率模组继电器和谐波滤波器的审核。

变频器市场报告按电压类型(低压、中压、高压)、功率等级(微、低、中、高)、驱动类型(交流变频器、直流驱动器、伺服/向量驱动器、其他)、应用(泵、风扇、鼓风机、其他)、最终用户行业(基础设施和建筑、食品和饮料加工、其他)以及地区(北美、南美、其他)地区进行细分。

区域分析

亚太地区持续保持领先地位,占2024年销售额的46.3%,这主要得益于中国自动化家电工厂的发展以及印度鼓励电机节能维修的生产关联奖励计划。像威驰这样的本土企业透过捆绑云端闸道和持续监控服务,扩大了出口销售,增强了其在该地区的成本竞争力。东南亚国协的政府补贴计画和强制性IE3马达政策维持了基准需求,而台湾和韩国的半导体工厂的伺服驱动器订单也出现了成长。

中东和非洲地区复合年增长率预计最高,达到7.3%,主要得益于海水淡化管道和铜矿带电气化改造对高抗衝击性重型中压驱动器的需求。 ACCIONA在舒盖格3期计画的里程碑凸显了水安全的重要性,并促成了数兆瓦级水泵驱动合约的签订。资金紧张的非洲公共产业金融机构的资金,为大量采用变频驱动器的水处理升级项目提供资金,从而扩大了区域订单。

随着北美和欧洲老旧设备接近使用寿命终点,能源效率法规日益严格,设备的更新换代週期也稳定加速。公用事业公司的回扣计划和企业环境、社会及公司治理(ESG)目标加速了设备的普及,尤其是在电价上涨与积极的脱碳目标一致的情况下。一家欧洲粉末冶金厂采用了主动式前端驱动器来满足谐波排放法规的要求,而美国中西部的一家化工厂则利用天然气价格波动,透过预测性变频器(VFD)演算法来调整马达负载。网路安全要求的提高虽然延长了竞标评估週期,但最终却提升了提供修补程式管理和安全认证更新服务的供应商的业务收益。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 数位原民流程工厂需要马达级能量优化。

- 暖通空调和水系统强制性可变扭矩效率规则

- 低延迟乙太网路马达在工业4.0改装的广泛应用

- 海水淡化和水资源再利用基础设施的快速发展(主要在中东地区)

- 地下矿业车辆的电气化

- 与通货膨胀挂钩的电费加快了变频器改造的投资维修。

- 市场限制

- 690V以上等级设备的EMI/谐波抑制措施成本不断上涨

- 开发中国家公共产业的资本投资受限

- 网路加固成本减缓了传统硬碟的更新换代週期。

- 电力电子级SiC/GaN晶片持续短缺

- 宏观经济因素的影响

- 投资分析

- 价值链分析

- 监管环境

- 技术概览

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按电压类型

- 低电压(低于1千伏特)

- 中压(1-6千伏特)

- 高压(6千伏以上)

- 按额定输出功率(kW)

- 微型(少于 20)

- 低(20-200)

- 中(200-600)

- 高(超过 600)

- 按驱动类型

- 交流变频器

- 直流驱动器

- 伺服/向量驱动器

- 多级和矩阵驱动器

- 透过使用

- 泵浦

- 风扇和鼓风机

- 压缩机

- 输送带

- 暖通空调系统

- 挤出机和混合机

- 按最终用户行业划分

- 基础设施和建筑物

- 食品和饮料加工

- 能源与发电

- 石油、天然气和石化

- 采矿和金属

- 纸浆和造纸

- 用水和污水

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Danfoss A/S

- Rockwell Automation Inc.

- Mitsubishi Electric Corporation

- Yaskawa Electric Corporation

- Fuji Electric Co. Ltd.

- Eaton Corporation plc

- WEG Industries SA

- Nidec Corporation

- Toshiba Corporation

- Hitachi Ltd.

- Johnson Controls International plc

- Inovance Technology Co. Ltd.

- Delta Electronics Inc.

- Emerson Electric Co.

- LS Electric Co. Ltd.

- SEW-Eurodrive GmbH & Co KG

- Veichi Electric Co. Ltd.

- Control Techniques(Nidec)

- HARS Drives Co. Ltd.

- Vacon(Part of Danfoss)

- Parker Hannifin-SSD Drives

- Kollmorgen Corporation

- Bonfiglioli Riduttori SpA

第七章 市场机会与未来展望

The global variable frequency drives market size was valued at USD 28.09 billion in 2025 and is forecast to reach USD 36.27 billion by 2030, advancing at a 5.24% CAGR.

Strong policy pressure for motor-level efficiency, fast paybacks from energy savings, and the migration toward digitalized production lines have steadily widened the adoption base. Demand remained resilient even as capital-spending cycles tightened, because VFD retrofits deliver immediate electricity cost relief in energy-intensive plants. Medium-voltage upgrade projects in mining and metals, desalination build-outs in the Middle East, and HVAC efficiency mandates in commercial buildings collectively broadened the addressable opportunity. Suppliers that embedded Ethernet, cybersecurity features, and silicon-carbide switching devices into their portfolios protected margins and unlocked service revenues. Headwinds tied to SiC/GaN chip shortages and higher electromagnetic-interference compliance costs slightly tempered shipment growth yet did not derail the multiyear efficiency investment trend.

Global Variable Frequency Drives Market Trends and Insights

Digital-native process plants demanding motor-level energy optimisation

Digitally designed plants relied on predictive analytics inside modern VFDs to align motor load with production schedules and real-time electricity prices. Rockwell Automation's PowerFlex 755TS platform, for example, bundled edge analytics and delivered downtime cuts while trimming energy usage across multi-motor lines. Semiconductor fabrication and pharmaceutical facilities led adoption because yield depends on precise speed control and uninterrupted service connectivity.

Mandatory variable-torque efficiency rules in HVAC and water verticals

Efficiency legislation made VFD integration non-negotiable in pumps and air-handling units. The U.S. Department of Energy's 2028 circulator-pump rule in effect required electronically commutated motors paired with sophisticated drives. In anticipation, OEMs such as Trane locked multi-year purchase agreements with Danfoss to guarantee compliant VFD supply.

Rising EMI/harmonics compliance costs above 690 V

Compliance costs linked to electromagnetic interference and harmonic distortion rose sharply after regulators tightened IEEE 519 limits for installations above 690 V. Medium-voltage projects now require oversized reactors, multi-pulse transformers, and shielded cable runs, adding material, commissioning, and engineering expenses that can raise installed drive cost by more than 15%. Smaller manufacturers are disproportionately affected because the design and certification overhead must be spread across lower shipment volumes, which can deter new entrants and accelerate consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Surge in low-latency Ethernet-enabled motors for Industry 4.0 retrofits

- Rapid build-out of desalination and water-reuse infrastructure

- Persistent shortage of power-electronics-grade SiC/GaN chips

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-voltage units below 1 kV remained the workhorse, controlling conveyors, mixers, and HVAC fans across small and mid-sized plants. In 2024 they captured 62.4% revenue, anchoring the variable frequency drives market. Cost-effective installation, plentiful integrator expertise, and abundant supplier catalogs sustained share. Parallelly, brownfield expansions in steel mills and underground mines shifted procurement toward 1-6 kV solutions, propelling the medium-voltage tier at a 6.8% CAGR. Mines upgrading to 995 V grids selected purpose-built drives to limit cable runs and improve voltage stability.

The variable frequency drives market size for medium-voltage equipment is forecast to reach USD 10.4 billion by 2030, benefiting from renewable energy in-feed, which heightens grid-code requirements for harmonic mitigation. Vendors responded with arc-resistant enclosures and modular active-front-end designs that cut total harmonic distortion below 3%. High-voltage products above 6 kV served niche hydro-pumping and rolling-mill projects; their uptake stayed limited by premium price tags and installation complexity.

Micro drives under 20 kW delivered the highest 7.2% CAGR as factories embraced distributed control, embedding small motors in autonomous mobile robots and smart building subsystems. Volume shipments climbed in tandem with sensor-rich HVAC zoning and food-processing feeders. Low-power (20-200 kW) models still underpinned 40.3% of 2024 revenue, proving indispensable to centrifugal pumps and axial fans across chemical and water utilities.

Developers enlarged heat-sink capacity and switched to SiC diodes to lift ambient operating limits beyond 60 °C, a critical differentiator in desert solar fields. The variable frequency drives market share for high-power classes above 600 kW remained below 5%, yet each sale generated sizable aftermarket revenue streams through long-term service agreements covering power-module relays and harmonic filter audits.

The Variable Frequency Drives Market Report is Segmented by Voltage Type (Low Voltage, Medium Voltage, High Voltage), Power Rating (Micro, Low, Medium, High), Drive Type (AC Drives, DC Drives, Servo/Vector Drives, and More), Application (Pumps, Fans and Blowers, and More), End-User Industry (Infrastructure and Buildings, Food and Beverage Processing, and More), and Geography (North America, South America, and More).

Geography Analysis

Asia-Pacific maintained leadership with 46.3% 2024 revenue, underpinned by China's automated appliance plants and India's production-linked incentive schemes that encouraged motor-efficiency retrofits. Local champions such as VEICHI scaled export sales by bundling cloud gateways for continuous monitoring, reinforcing regional cost competitiveness. Government rebate programs and mandatory IE3 motor policies in several ASEAN states sustained baseline demand, while semiconductor fabs in Taiwan and South Korea accelerated servo-drive orders.

The Middle East and Africa posted the highest 7.3% CAGR outlook as sovereign desalination pipelines and copper-belt mining electrification demanded rugged medium-voltage drives with high ingress protection. ACCIONA's Shuqaiq 3 milestone highlighted how water-security imperatives generate multi-megawatt pump-drive contracts. African utilities, though capital-constrained, tapped development-finance institutions to fund VFD-rich water-treatment upgrades, amplifying regional order books.

North America and Europe delivered steady replacement-cycle growth as older installations approached end-of-life and as stricter efficiency codes compelled upgrades. Utility rebate schemes and corporate ESG targets hastened adoption, especially where tariff escalation aligned with aggressive decarbonisation goals. European powder-metallurgy plants opted for active-front-end drives to meet harmonic quotas, while US Midwest chemical plants exploited natural-gas price volatility by modulating motor load with predictive VFD algorithms. Cyber-security hardening requirements extended bid evaluation timelines, yet ultimately enlarged service revenue for vendors offering patch-management and security-certificate renewal packages.

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Danfoss A/S

- Rockwell Automation Inc.

- Mitsubishi Electric Corporation

- Yaskawa Electric Corporation

- Fuji Electric Co. Ltd.

- Eaton Corporation plc

- WEG Industries S.A.

- Nidec Corporation

- Toshiba Corporation

- Hitachi Ltd.

- Johnson Controls International plc

- Inovance Technology Co. Ltd.

- Delta Electronics Inc.

- Emerson Electric Co.

- LS Electric Co. Ltd.

- SEW-Eurodrive GmbH & Co KG

- Veichi Electric Co. Ltd.

- Control Techniques (Nidec)

- HARS Drives Co. Ltd.

- Vacon (Part of Danfoss)

- Parker Hannifin - SSD Drives

- Kollmorgen Corporation

- Bonfiglioli Riduttori S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital-native process plants demanding motor-level energy-optimisation

- 4.2.2 Mandatory variable torque efficiency rules in HVAC and water verticals

- 4.2.3 Surge in low-latency, Ethernet-enabled motors for Industry 4.0 retrofits

- 4.2.4 Rapid build-out of desalination and water-reuse infrastructure (Middle-East focus)

- 4.2.5 Electrification of underground mining fleets

- 4.2.6 Inflation-linked electricity tariffs accelerating ROI on VFD retrofits

- 4.3 Market Restraints

- 4.3.1 Rising EMI / harmonics compliance costs above 690 V class

- 4.3.2 Cap-ex squeeze in developing-world utilities

- 4.3.3 Cyber-hardening spend delaying refresh cycles of legacy drives

- 4.3.4 Persistent shortage of power-electronics grade SiC/GaN chips

- 4.4 Impact of Macroeconomic Factors

- 4.5 Investment Analysis

- 4.6 Value Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technology Snapshot

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Voltage Type

- 5.1.1 Low Voltage (<1 kV)

- 5.1.2 Medium Voltage (1-6 kV)

- 5.1.3 High Voltage (>6 kV)

- 5.2 By Power Rating (kW)

- 5.2.1 Micro (<20)

- 5.2.2 Low (20-200)

- 5.2.3 Medium (200-600)

- 5.2.4 High (>600)

- 5.3 By Drive Type

- 5.3.1 AC Drives

- 5.3.2 DC Drives

- 5.3.3 Servo / Vector Drives

- 5.3.4 Multilevel and Matrix Drives

- 5.4 By Application

- 5.4.1 Pumps

- 5.4.2 Fans and Blowers

- 5.4.3 Compressors

- 5.4.4 Conveyors

- 5.4.5 HVAC Systems

- 5.4.6 Extruders and Mixers

- 5.5 By End-user Industry

- 5.5.1 Infrastructure and Buildings

- 5.5.2 Food and Beverage Processing

- 5.5.3 Energy and Power Generation

- 5.5.4 Oil, Gas and Petrochemicals

- 5.5.5 Mining and Metals

- 5.5.6 Pulp and Paper

- 5.5.7 Water and Wastewater

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Danfoss A/S

- 6.4.5 Rockwell Automation Inc.

- 6.4.6 Mitsubishi Electric Corporation

- 6.4.7 Yaskawa Electric Corporation

- 6.4.8 Fuji Electric Co. Ltd.

- 6.4.9 Eaton Corporation plc

- 6.4.10 WEG Industries S.A.

- 6.4.11 Nidec Corporation

- 6.4.12 Toshiba Corporation

- 6.4.13 Hitachi Ltd.

- 6.4.14 Johnson Controls International plc

- 6.4.15 Inovance Technology Co. Ltd.

- 6.4.16 Delta Electronics Inc.

- 6.4.17 Emerson Electric Co.

- 6.4.18 LS Electric Co. Ltd.

- 6.4.19 SEW-Eurodrive GmbH & Co KG

- 6.4.20 Veichi Electric Co. Ltd.

- 6.4.21 Control Techniques (Nidec)

- 6.4.22 HARS Drives Co. Ltd.

- 6.4.23 Vacon (Part of Danfoss)

- 6.4.24 Parker Hannifin - SSD Drives

- 6.4.25 Kollmorgen Corporation

- 6.4.26 Bonfiglioli Riduttori S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

隧道钻掘机变频驱动装置(VFD逆变器)市场:2026-2032年全球预测,依输出范围、电压等级、隧道钻掘机类型、冷却方式、应用领域及安装方式划分塔式起重机变频驱动装置市场:依起重机类型、额定功率、控制类型、安装类型和应用划分-全球预测,2026-2032年隧道钻掘机变频驱动装置市场:按类型、额定功率、应用和最终用户划分,全球预测,2026-2032年

隧道钻掘机变频驱动装置(VFD逆变器)市场:2026-2032年全球预测,依输出范围、电压等级、隧道钻掘机类型、冷却方式、应用领域及安装方式划分塔式起重机变频驱动装置市场:依起重机类型、额定功率、控制类型、安装类型和应用划分-全球预测,2026-2032年隧道钻掘机变频驱动装置市场:按类型、额定功率、应用和最终用户划分,全球预测,2026-2032年 变频驱动马达市场规模、份额及成长分析:依产品类型、电压、应用、功率范围、最终用户及地区划分-2026-2033年产业预测

变频驱动马达市场规模、份额及成长分析:依产品类型、电压、应用、功率范围、最终用户及地区划分-2026-2033年产业预测 2026年全球驱动装置市场报告

2026年全球驱动装置市场报告 变频器市场-全球产业规模、份额、趋势、机会与预测:按类型、最终用户、功率范围、电压、应用、地区和竞争格局划分,2021-2031年

变频器市场-全球产业规模、份额、趋势、机会与预测:按类型、最终用户、功率范围、电压、应用、地区和竞争格局划分,2021-2031年 日本驱动装置市场按产品类型、功率范围、应用、最终用途和地区划分,2026-2034年

日本驱动装置市场按产品类型、功率范围、应用、最终用途和地区划分,2026-2034年 驱动装置(VFD)市场规模、份额和成长分析(按产品类型、功率范围、电压类型、应用、最终用户和地区划分)-2026-2033年产业预测

驱动装置(VFD)市场规模、份额和成长分析(按产品类型、功率范围、电压类型、应用、最终用户和地区划分)-2026-2033年产业预测 HVAC变频驱动器市场规模、份额和成长分析(按类型、功率范围、应用和地区划分)-2026-2033年产业预测

HVAC变频驱动器市场规模、份额和成长分析(按类型、功率范围、应用和地区划分)-2026-2033年产业预测 变频器市场 - 全球预测 2025-2030

变频器市场 - 全球预测 2025-2030