|

市场调查报告书

商品编码

1851369

工业控制系统:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Industrial Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

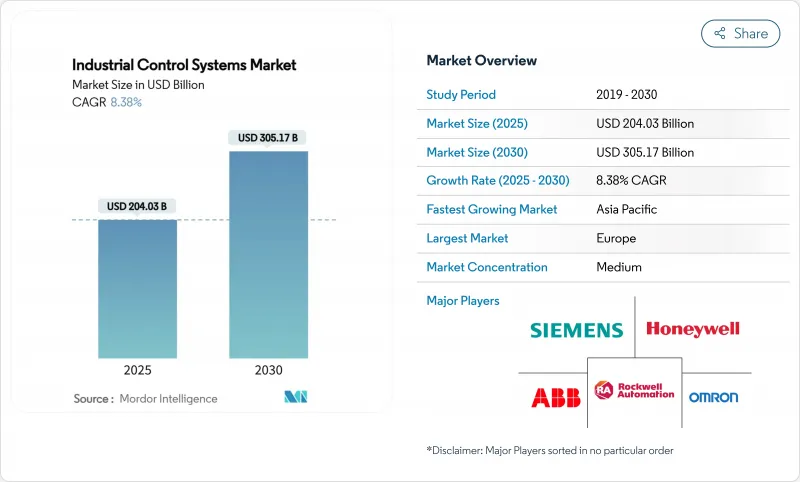

预计到 2025 年,工业控制系统市场规模将达到 2,040.3 亿美元,到 2030 年将达到 3,051.7 亿美元,年复合成长率为 8.38%。

工业4.0加速数位化、网路安全要求以及开放式、厂商中立架构日益增长的吸引力,正将自动化从提升效率的附加附加元件转变为营运的基石。 2024年半导体产业的低迷加剧了供应链风险,凸显了软体定义控制平台(将功能与专用硬体分离)的价值;同时,欧洲和北美政府的激励措施扩大了维修计划的资金池。随着製造商在不放弃低延迟製程控制的前提下寻求大规模分析,云端、边缘和本地部署正在并存。尤其是在电子和生命科学等高精度领域,能够将可互通的硬体与人工智慧软体和整合安全功能相结合的供应商正在获得竞争优势。

全球工业控制系统市场趋势与洞察

利用工业4.0加速工厂整体自动化

製造商正将自动化从孤立的生产线扩展到整合营运、工程和业务数据的企业级网路。诸如西门子 SINUMERIK ONE 等支援人工智慧的边缘节点,现在可以直接在工具机现场执行预测性维护和自适应进给速度控制,从而缩短决策延迟。更广泛的连接性创造了复合价值,这也解释了为什么儘管面临宏观经济逆风,到 2025 年营运技术 (OT) 预算平均仍将成长 30%。因此,可互通的产品正在超越专有单点产品,重塑市场竞争动态。

更加重视工业安全和功能安全合规性

工业法规正朝着安全完整性(IEC 61508/61511)和网路安全韧性(IEC 62443)的双重目标靠拢。经过认证的安全PLC和安全通讯协定至关重要,因为像西门子SIBERprotect这样的工具可以在几毫秒内隔离风险资产,同时保持安全迴路的完整性。随着CISA针对2024年OT漏洞发布了24项建议,买家现在将网路安全资质纳入资本规划,这推动工业控制系统市场向提供原生整合功能的供应商靠拢。

熟练的OT/ICS工程师短缺

德勤预测,到2033年,美国製造业将有190万个工作失业,其中许多人需要具备IT和OT混合技能。因此,供应商正寻求透过将託管服务与低程式码配置捆绑在一起来降低部署难度。

细分市场分析

儘管SCADA平台在2024年将占据工业控制系统市场28.7%的份额,但其集中式控制方式正受到边缘PLC的挑战,后者预计到2030年将以11.46%的复合年增长率增长。微型AI晶片的涌现使得PLC能够在本地处理状态监测和品质检测工作负载,从而减少资料回程传输和网路拥塞。在石油天然气和化学工业,分散式控制系统仍用于管理连续流程,但客户正在传统DCS之上迭加预测演算法,以延长资产寿命。人机介面正在演变为决策支援主机,并整合AR扩增实境技术以进行现场故障排除。随着电网营运商寻求更快的故障隔离,智慧电子设备在公用事业领域越来越受欢迎。对于这些应用场景,提供开放API的供应商在工业控制系统市场备受青睐,这使得工厂管理人员能够在不被特定供应商锁定的情况下组合使用最佳组件。

预计到2025年,SCADA仍将为工业控制系统市场贡献585亿美元,届时,能够融合分析功能并维持监控层完整性的容器化微服务将主导升级週期。同时,一项离散製造业的试点计画表明,边缘PLC集群可将计划外停机时间减少高达20%,从而加快投资回报率。能够协调集中式和分散式架构生命週期服务的供应商预计将获得不成比例的市场份额。

随着工厂追求整体设备效率 (OEE) 和无需计划维护,资产性能管理将在 2024 年贡献 23.6% 的收入。展望未来,受勒索软体攻击 OT 资产日益猖獗的推动,网路安全套件预计将以 12.75% 的复合年增长率 (CAGR) 超越所有其他类别。整合漏洞扫描、零信任分段和安全 PLC 加固功能的产品在製药公司等风险规避型产业中越来越受欢迎。製造执行系统 (MES) 现在将品质分析与电子批次记录 (EBR) 结合,产品生命週期管理 (PLM) 工具与数位孪生技术连接,从而连接设计和製造。 ERP 供应商正在透过 REST API 公开 OT 资料模型,以支援需求主导的计画演算法。因此,工业控制系统市场正倾向于编配跨域资料的平台,而不是单一模组。

预计到2030年,工业控制系统市场规模将超过140亿美元,工业网路平台正吸引创业投资资金,并促使现有供应商收购特定领域的专业公司。擅长协调应用效能管理(APM)、製造执行系统(MES)和网路层的供应商,正将自身定位为数位转型蓝图的端到端推动者。

区域分析

2024年,欧洲将占全球销售额的28.5%,严格的功能安全法规和永续性要求推动了对高效自动化技术的重视。诸如Manufacturing-X之类的资金筹措计划正在拨款1.5亿欧元(1.61亿美元)用于优先考虑数据主权的计划,这使本土供应商获得了先发优势。资本计划越来越多地将碳足迹仪錶板与欧盟绿色新政的报告要求捆绑在一起。东欧产业丛集为西方原始设备製造商提供了近岸产能,刺激了对中阶控制设备的需求成长。

亚太地区将以10.24%的复合年增长率成长,受益于电子产品、电动车电池和可再生组件的大规模产能扩张。中国的人口结构变化和薪资上涨将加速工厂自动化进程,而东南亚国家将利用税收优惠吸引回流计划。国内PLC和机器人供应商正在扩大市场份额,而跨国巨头则继续在高端安全和运动解决方案领域保持主导地位。以中国《关键资讯基础设施法》为首的政府网路安全法规,正促使买家转向检验的安全相关产品,并影响采购候选名单的发展。

北美将透过製造业倡议和《CHIPS法案》2亿美元的数位双胞胎孪生计画维持成长动能。美国墨西哥湾沿岸的能源转型支出正在催生开放式製程自动化的需求,以用于维修天然气、氢气和碳捕获与封存(CCS)设施。加拿大NGen的3500万美元永续製造挑战计画正在推动中小企业采用模组化控制套件。美国网路安全和基础设施安全局(CISA)加强的网路安全要求正在改善采购规范,优先考虑拥有IEC 62443认证的供应商。总而言之,这些趋势正在推动工业控制系统市场持续实现区域多元化成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 工业4.0的部署将加速工厂范围内的自动化进程。

- 更加重视工业安全和功能安全合规性

- 对即时、数据主导的大规模客製化的需求激增

- 政府对智慧工厂维修的奖励

- 开放式流程自动化(O-PAS)架构尚未引起广泛关注

- 转型为「OT即服务」边缘平台(鲜为人知)

- 市场限制

- 熟练的OT/ICS工程师短缺

- 高额资本投入和较长的投资回收期

- 半导体前置作业时间波动(在不为人知的情况下)扰乱了控制器供应。

- 旧有系统整合复杂性(鲜为人知)

- 价值链分析

- 监管环境

- 技术展望

- 主要宏观经济趋势的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 评估市场宏观经济趋势

第五章 市场规模与成长预测

- 透过营运技术

- 监控与数据采集(SCADA)

- 分散式控制系统(DCS)

- 可程式逻辑控制器(PLC)

- 智慧电子设备(IED)

- 人机介面(HMI)

- 其他系统

- 透过软体

- 资产绩效管理(APM)

- 产品生命週期管理(PLM)

- 製造执行系统(MES)

- 企业资源规划(ERP)

- 工业网路安全平台

- 其他软体

- 透过部署模式

- 本地部署

- 云端基础的

- 边缘/混合

- 按最终用户行业划分

- 石油和天然气

- 化工/石油化工

- 电力与公用事业

- 饮食

- 汽车和运输设备

- 生命科学

- 用水和污水

- 金属和采矿

- 纸浆和造纸

- 电子和半导体

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Siemens AG

- ABB Ltd.

- Rockwell Automation Inc.

- Schneider Electric SE

- Honeywell International Inc.

- Emerson Electric Co.

- Yokogawa Electric Corporation

- Mitsubishi Electric Corporation

- Omron Corporation

- GE Digital(General Electric Co.)

- Bosch Rexroth AG

- Phoenix Contact GmbH

- Beckhoff Automation GmbH

- Hitachi Ltd.

- Delta Electronics Inc.

- Advantech Co., Ltd.

- Johnson Controls International plc

- Fortinet Inc.(ICS-cybersecurity)

- Palo Alto Networks Inc.(ICS-cybersecurity)

- ICS-Secure LLC

第七章 市场机会与未来展望

The industrial control systems market size stood at USD 204.03 billion in 2025 and is projected to reach USD 305.17 billion by 2030, advancing at an 8.38% CAGR.

Accelerated digitalization under Industry 4.0, mounting cybersecurity obligations, and the growing appeal of open, vendor-neutral architectures are reinforcing automation as an operational cornerstone rather than an efficiency add-on. Heightened supply-chain risk during the 2024 semiconductor squeeze underscored the value of software-defined control platforms that detach functionality from dedicated hardware, while government incentives in Europe and North America widened the capital pool for retrofit projects. Cloud, edge, and on-premise deployments now coexist as manufacturers seek analytics at scale without surrendering low-latency process control. Competitive positioning increasingly favors vendors that combine interoperable hardware with AI-enabled software and integrated security, especially in high-precision sectors such as electronics and life sciences.

Global Industrial Control Systems Market Trends and Insights

Industry 4.0 Roll-outs Accelerating Plant-wide Automation

Manufacturers are extending automation from isolated lines to enterprise-wide networks that merge operational, engineering, and business data. AI-ready edge nodes such as Siemens SINUMERIK ONE now execute predictive maintenance and adaptive feed-rate control directly on the machine floor, shrinking decision latency. Broader connectivity generates compound value, which explains why average OT budgets grew 30% in 2025 despite macro headwinds. As a result, interoperable offerings are edging out proprietary point products, reshaping competitive dynamics across the industrial control systems market.

Growing Emphasis on Industrial Safety and Functional-Safety Compliance

Industrial regulations are converging around dual mandates of safety integrity (IEC 61508/61511) and cybersecurity resilience (IEC 62443). Tools such as Siemens SIBERprotect isolate compromised assets within milliseconds while keeping safety loops intact, making certified safety PLCs and secure communication protocols indispensable. With CISA releasing 24 advisories on OT vulnerabilities in 2024, buyers now factor cyber-safety credentials into capital planning, nudging the industrial control systems market toward vendors that offer natively integrated capabilities.

Shortage of Skilled OT/ICS Engineers

Deloitte estimates 1.9 million US manufacturing roles may go unfilled by 2033, many requiring hybrid IT-OT skills. Scarcity inflates labor costs and prolongs commissioning cycles, prompting vendors to bundle managed services and low-code configuration to soften onboarding friction.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Demand for Real-time Data-driven Mass-customisation

- Government Incentives for Smart-factory Retrofits

- High Capex and Long Pay-back Periods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SCADA platforms retained a 28.7% slice of the industrial control systems market in 2024, yet their centralized approach is being contested by edge-enabled PLCs that are posting 11.46% CAGR through 2030. The influx of micro-AI chips allows PLCs to process condition-monitoring and quality-inspection workloads locally, reducing data backhaul and network congestion. In oil & gas and chemicals, Distributed Control Systems still govern continuous processes, but customers are layering predictive algorithms over legacy DCS to extend asset life. Human-Machine Interfaces have evolved into decision-support consoles incorporating AR overlays for on-the-spot troubleshooting. Intelligent Electronic Devices are gaining traction in utilities as grid operators pursue faster fault isolation. Across these use cases, the industrial control systems market rewards suppliers that embed open APIs, enabling plant managers to mix best-of-breed components without vendor lock-in.

With SCADA still contributing USD 58.5 billion to industrial control systems market size in 2025, upgrade cycles center on container-based micro-services that keep supervisory layers intact while injecting analytics. Meanwhile, pilot programs in discrete manufacturing show edge PLC clusters trimming unplanned downtime by up to 20%, accelerating payback. Vendors able to harmonize lifecycle services for both centralized and distributed architectures are expected to capture disproportionate share.

Asset Performance Management generated 23.6% of 2024 revenue as plants chase overall equipment effectiveness and schedule-free maintenance. Looking ahead, cybersecurity suites are set to outpace all other categories at 12.75% CAGR, a reaction to increased ransomware targeting OT assets. Integrated offerings that fuse vulnerability scanning, zero-trust segmentation, and safety-PLC hardening resonate with risk-averse sectors such as pharmaceuticals. Manufacturing Execution Systems now bundle quality analytics and electronic batch records, while Product Lifecycle Management tools couple with digital twins to bridge design and production. ERP vendors are exposing OT data models via REST APIs, feeding demand-driven planning algorithms. The industrial control systems market is therefore tilting toward platforms that orchestrate cross-domain data rather than discrete modules.

Industrial cyber platforms, forecast to exceed USD 14 billion in industrial control systems market size by 2030, are attracting venture funding and prompting established vendors to buy niche specialists. Suppliers competent in synchronizing APM, MES, and cyber layers position themselves as single-throat-to-choke partners for digital transformation roadmaps.

The Global Industrial Control Systems Market Report is Segmented by Operational Technology (SCADA, DCS, PLC, and More), Software (APM, PLM, MES, ERP, and More), Deployment Mode (On-Premise, Cloud-Based, Edge/Hybrid), End-User Industry (Oil and Gas, Chemical and Petrochemical, Power and Utilities, Food and Beverages, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe steers 28.5% of 2024 revenue, driven by rigorous functional-safety statutes and sustainability mandates that reward high-efficiency automation. Funding schemes such as Manufacturing-X distribute EUR 150 million (USD 161 million) to projects that emphasize data sovereignty, giving domestic vendors an early-mover edge. Capital projects increasingly bundle carbon-footprint dashboards, aligning with the EU's Green Deal reporting. Eastern European clusters act as near-shore capacity for Western OEMs, stimulating incremental demand for mid-tier control gear.

Asia-Pacific, advancing at 10.24% CAGR, benefits from large-scale capacity expansions in electronics, EV batteries, and renewable components. China's demographic headwinds and wage inflation accelerate factory automation, while Southeast Asian nations leverage tax incentives to lure reshoring projects. Domestic PLC and robot suppliers are gaining share, but multinational incumbents retain dominance in high-end safety and motion solutions. Government cyber rules, notably China's Critical Information Infrastructure law, push buyers toward products with verifiable security lineage, shaping procurement shortlists.

North America sustains momentum through reshoring initiatives and the CHIPS Act's USD 200 million digital-twin program. Energy transition spending in the US Gulf Coast is spawning demand for open-process automation to retrofit LNG, hydrogen, and CCS facilities. Canada's NGen USD 35 million sustainable manufacturing challenge propels SME adoption of modular control kits. Heightened cyber directives from CISA elevate procurement specifications, giving advantage to suppliers with IEC 62443 certifications. Collectively, these trends keep the industrial control systems market on a diversified regional growth footing.

- Siemens AG

- ABB Ltd.

- Rockwell Automation Inc.

- Schneider Electric SE

- Honeywell International Inc.

- Emerson Electric Co.

- Yokogawa Electric Corporation

- Mitsubishi Electric Corporation

- Omron Corporation

- GE Digital (General Electric Co.)

- Bosch Rexroth AG

- Phoenix Contact GmbH

- Beckhoff Automation GmbH

- Hitachi Ltd.

- Delta Electronics Inc.

- Advantech Co., Ltd.

- Johnson Controls International plc

- Fortinet Inc. (ICS-cybersecurity)

- Palo Alto Networks Inc. (ICS-cybersecurity)

- ICS-Secure LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0 roll-outs accelerating plant-wide automation

- 4.2.2 Growing emphasis on industrial safety and functional-safety compliance

- 4.2.3 Surge in demand for real-time data-driven mass-customisation

- 4.2.4 Government incentives for smart-factory retrofits

- 4.2.5 Open Process Automation (O-PAS) architecture gaining traction (under-the-radar)

- 4.2.6 Shift to "OT-as-a-Service" edge platforms (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled OT/ICS engineers

- 4.3.2 High capex and long pay-back periods

- 4.3.3 Semiconductor lead-time volatility disrupting controller supply (under-the-radar)

- 4.3.4 Legacy-system integration complexity (under-the-radar)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Key Macroeconomic Trends

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Operational Technology

- 5.1.1 Supervisory Control and Data Acquisition (SCADA)

- 5.1.2 Distributed Control System (DCS)

- 5.1.3 Programmable Logic Controller (PLC)

- 5.1.4 Intelligent Electronic Devices (IED)

- 5.1.5 Human-Machine Interface (HMI)

- 5.1.6 Other Systems

- 5.2 By Software

- 5.2.1 Asset Performance Management (APM)

- 5.2.2 Product Lifecycle Management (PLM)

- 5.2.3 Manufacturing Execution System (MES)

- 5.2.4 Enterprise Resource Planning (ERP)

- 5.2.5 Industrial Cyber-security Platforms

- 5.2.6 Other Software

- 5.3 By Deployment Mode

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.3.3 Edge / Hybrid

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Power and Utilities

- 5.4.4 Food and Beverages

- 5.4.5 Automotive and Transportation

- 5.4.6 Life Sciences

- 5.4.7 Water and Wastewater

- 5.4.8 Metal and Mining

- 5.4.9 Pulp and Paper

- 5.4.10 Electronics and Semiconductor

- 5.4.11 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 ABB Ltd.

- 6.4.3 Rockwell Automation Inc.

- 6.4.4 Schneider Electric SE

- 6.4.5 Honeywell International Inc.

- 6.4.6 Emerson Electric Co.

- 6.4.7 Yokogawa Electric Corporation

- 6.4.8 Mitsubishi Electric Corporation

- 6.4.9 Omron Corporation

- 6.4.10 GE Digital (General Electric Co.)

- 6.4.11 Bosch Rexroth AG

- 6.4.12 Phoenix Contact GmbH

- 6.4.13 Beckhoff Automation GmbH

- 6.4.14 Hitachi Ltd.

- 6.4.15 Delta Electronics Inc.

- 6.4.16 Advantech Co., Ltd.

- 6.4.17 Johnson Controls International plc

- 6.4.18 Fortinet Inc. (ICS-cybersecurity)

- 6.4.19 Palo Alto Networks Inc. (ICS-cybersecurity)

- 6.4.20 ICS-Secure LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

工业共生平台市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户及解决方案划分

工业共生平台市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户及解决方案划分 2026年全球工业控制市场报告

2026年全球工业控制市场报告 PLC控制器市场按类型、组件、产业、通讯协定、应用和程式语言划分,全球预测,2026-2032年基于云端的自动化控制系统市场:按最终用户、组件、系统类型、技术、公司规模和产品/服务划分,全球预测,2026-2032年

PLC控制器市场按类型、组件、产业、通讯协定、应用和程式语言划分,全球预测,2026-2032年基于云端的自动化控制系统市场:按最终用户、组件、系统类型、技术、公司规模和产品/服务划分,全球预测,2026-2032年 工业製程製造控制市场:依技术、硬体及软体、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

工业製程製造控制市场:依技术、硬体及软体、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测 工业控制系统市场规模、份额和成长分析(按组件、技术、最终用途和地区划分)-2026年至2033年产业预测

工业控制系统市场规模、份额和成长分析(按组件、技术、最终用途和地区划分)-2026年至2033年产业预测 工业计数器市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测2025年全球田径圈市场报告

工业计数器市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测2025年全球田径圈市场报告 云端基础工业控制系统市场预测至2032年:按组件、控制系统类型、部署模式、最终用户和地区分類的全球分析工业共生市场预测至2032年:按类型、共生模式、技术、应用、最终用户和地区分類的全球分析

云端基础工业控制系统市场预测至2032年:按组件、控制系统类型、部署模式、最终用户和地区分類的全球分析工业共生市场预测至2032年:按类型、共生模式、技术、应用、最终用户和地区分類的全球分析