|

市场调查报告书

商品编码

1851387

合成润滑油:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Synthetic Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

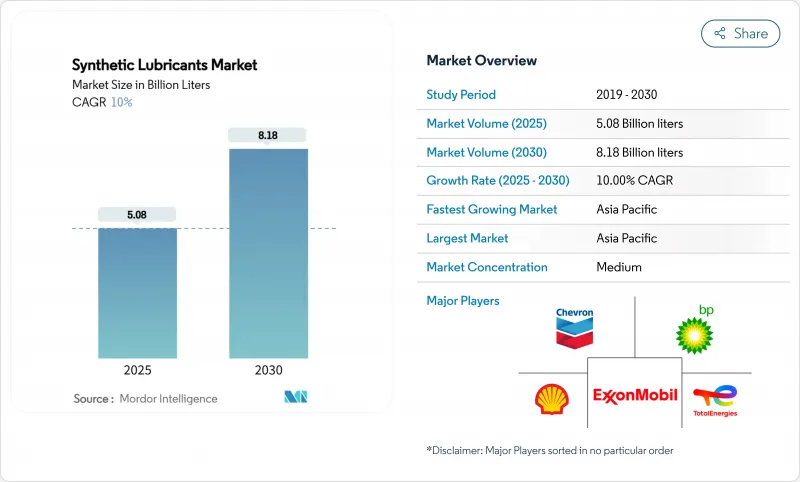

预计到 2025 年,合成润滑油市场规模将达到 50.8 亿公升,到 2030 年将达到 81.8 亿公升,在预测期(2025-2030 年)内复合年增长率将达到 10%。

低黏度机油需求不断增长、燃油经济性监管压力日益加大以及高性能润滑油在自动化生产线上的快速应用,是推动合成润滑油市场带来了正面影响。对茂金属聚环氧乙烷(PAO)产能的持续投资以及针对新的API和ACEA类别客製化产品的推出,正在增强供应安全并促进配方创新。同时,亚太地区在消费和成长方面均保持主导,这得益于中国庞大的製造地以及印度汽车保有量的復苏。

全球合成润滑油市场趋势及洞察

汽车售后市场对高性能合成机油的需求日益增长

随着API SQ标准于2025年3月生效,2024年及以后售后市场向全合成机油的转变已成定局。壳牌Helix Ultra系列填补了这个新类别,展现出卓越的动力保持能力和更佳的燃油经济性,促使服务中心推荐优质合成机油作为预设加註机油。市场偏好正迅速转向0W-20甚至0W-8黏度等级,因为更低的黏度可以改善冷启动时的燃油经济性。胜牌将于2024年底推出的优质全合成齿轮油,其磨损保护性能是传统产品的四倍,其溢价也符合客户在解释总体拥有成本时的预期。由于更严格的法规和消费者意识提升的提高,北美和欧洲仍然处于领先地位,但随着经销商网路强调延长换油週期,这股势头正蔓延至亚太地区的城市市场。

严格的排放气体和燃油经济法规

欧洲7号排放标准计画于2025年7月实施,而美国环保署(EPA)将于2026年发布更严格的重型车辆排放法规。这些法规强制要求使用黏度等级更低的润滑油,例如5W-20和0W-20,迫使润滑油配方商提高其抗氧化稳定性,以满足新一代柴油引擎65万英里(约105万公里)的长期使用要求。 ILSAC GF-7规范增加了低速早燃(LSPI)保护和正时链条磨损控制功能,这些功能难以用矿物油实现,因此合成基料必不可少。中国正在推动的国六排放标准和印度的Bharat Stage VII排放标准也朝着相似的阈值迈进,有效地将最严格的要求全球化。标准的统一化有利于跨国供应商,他们可以在全球部署同一种配方,从而缩短检验週期并提高规模经济效益。

合成润滑油的初始成本较高

全合成机油的零售价通常是矿物油的两到三倍,这一价格差异在对成本敏感的行业中仍然是一大障碍。在短週期使用情况下,延长换油週期的优势并不明显,这使得开发中国家的车队管理者难以证明其溢价的合理性。加德士的数据证实,在低于5000公里的保养间隔下,很难实现投资报酬率。然而,原油价格的上涨导致矿物油价格上涨速度超过合成油,缩小了两者之间的差距。同时,强调延长使用寿命的预测性维护工具逐渐降低商用车的吸引力。

细分市场分析

到2024年,机油将占合成合成润滑油市场34.58%的份额(按销量计),这主要得益于内燃机车庞大的装置量以及合成油优异的使用寿命。变速箱油和齿轮油仍是第二大品类,因为自动化生产线和风力发电机都需要在高负载下保持清洁运作。液压油受益于建设业和机器人技术的融合,可在宽广的温度范围内提供稳定的黏度。润滑脂在需要无滴漏润滑的领域仍然至关重要,例如航太产业的致动器和重型机械的接头。金属加工液虽然目前市占率较小,但随着精密加工和积层製造技术的成熟,其复合年增长率将达到11.15%,成为成长最快的品类。

此细分市场的前景受ILSAC GF-7和API SQ标准的影响。这项转变有利于能够延长换油週期、减少研讨会次数和废油处理的优质合成润滑油。此外,低雾、高闪点的金属加工液有助于降低工业事故的发生率,促使工厂转向合成酯类和PAG系统。综合来看,这些趋势必将推动非引擎用合成润滑油市场在2030年前保持稳定成长。

区域分析

预计到2024年,亚太地区将占全球合成润滑油市场份额的40.27%,复合年增长率(CAGR)为11.03%。中国先进製造业的復苏以及印度汽车销售两位数的成长,都支撑了该地区的消费。中国沿海地区新建的配方工厂,例如桂格霍顿公司计划于2026年投产的张家港工厂,显示供应商决心为高成长产业实现在地化供应。日本对高等级原厂润滑油的需求依然旺盛,而东南亚经济体则在扩大工业生产并拓展客户群。

北美地区销量位居第二,并持续保持技术领先地位。美国环保署 (EPA) 2026 年新规和美国石油学会 (API) 的产品线正推动配方师采用新一代添加剂化学品。美国凭藉其强大的丙烯基础设施,在高黏度聚环氧乙烷 (PAO) 供应方面也占据主导地位,但预计 2025 年年中丙烯供需将出现紧张,这可能会考验净利率。加拿大的油砂和采矿业以及墨西哥的汽车出口平台也构成了稳定的需求来源,这些地区依赖合成润滑油来确保运作和保固。

由于严格的环境法规和先进的OEM技术标准,欧洲保持其领先地位。欧盟7排放标准要求更低的黏度和更强的后处理相容性,这推动了酯类增强配方在轻型和重型车辆中的应用。北海离岸风电走廊和伊比利亚半岛新兴的可再生丛集需要能够耐受盐溶液腐蚀的终身变速箱油,从而扩大了高价值PAG和PAO混合油的选择范围。随着自动化投资的加速,东欧的工业基础正进一步实现需求多元化。中东和非洲(程度稍轻)也正在经历从矿物油到合成油的逐步转变,因为海湾地区的石化中心和南非的矿场在严酷的气候条件下追求更长的换油週期。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 汽车售后市场对高性能合成机油的需求日益增长

- 严格的排放气体和燃油经济法规

- 工业自动化的发展对先进的液压油和齿轮油提出了更高的要求。

- 航太和国防领域的快速扩张对合成涡轮机油的需求

- 离岸风力发电激增带动长效合成齿轮箱油需求成长

- 市场限制

- 与矿物油相比,初始成本较高。

- 由于电动车保有量增加,引擎机油需求下降。

- 聚α烯烃(PAO)原料供应的波动性;

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 机油

- 变速箱/齿轮油

- 油压

- 金属加工油

- 润滑脂

- 其他产品类型(通用工业油等)

- 基油

- 聚α烯烃(PAO)

- 酯

- 聚亚烷基二醇(PAG)

- 第三类/GTL衍生合成油

- 其他(烷基甲醇烷基化等)

- 最终用户

- 车

- 发电业务

- 重型机械

- 冶金与金属加工

- 其他终端用户产业(石油和天然气、海运、资料中心等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 印尼

- 泰国

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 北欧国家

- 土耳其

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Shell plc

- Exxon Mobil Corporation

- BP plc(Castrol)

- Chevron Corporation

- TotalEnergies

- Valvoline Global Operations(Saudi Aramco)

- China Petrochemical Corporation(Sinopec)

- PETRONAS Lubricants International

- FUCHS SE

- ENEOS Corporation

- Indian Oil Corporation Ltd

- AMSOIL Inc.

- Idemitsu Kosan Co.,Ltd.

- Gazpromneft-Lubricants Ltd.

- LUKOIL

- Phillips 66 Company

- Suncor Energy Inc.

- Quaker Chemical Corporation

- Repsol

- Motul

第七章 市场机会与未来展望

The Synthetic Lubricants Market size is estimated at 5.08 Billion liters in 2025, and is expected to reach 8.18 Billion liters by 2030, at a CAGR of 10% during the forecast period (2025-2030).

Rising demand for lower-viscosity engine oils, accelerated regulatory pressure on fuel economy, and the rapid adoption of high-performance fluids across automated manufacturing lines are the principal growth engines. The synthetic lubricants market is also benefiting from the introduction of the ILSAC GF-7 specification, effective March 2025, which compels automakers and service networks to shift toward advanced PAO and PAG-based formulations. Continuous investments in metallocene PAO capacity, together with product launches tuned for new API and ACEA categories, reinforce supply security and spur formulation innovation. Against this backdrop, Asia-Pacific maintains leadership on both consumption and growth, aided by China's large manufacturing base and India's recovering vehicle parc.

Global Synthetic Lubricants Market Trends and Insights

Increasing Usage of High-Performance Synthetic Engine Oils in the Automotive Aftermarket

The post-2024 aftermarket pivot toward full-synthetic engine oils became pronounced once the API SQ standard entered force in March 2025. Shell's Helix Ultra line, which satisfies the new category, demonstrates full power retention and better fuel economy, convincing service centers to recommend premium synthetics as default fills . Market preference is shifting rapidly to 0W-20 and even 0W-8 grades because lower viscosity improves fuel efficiency during cold starts. Valvoline's premium full-synthetic gear oils, launched late 2024, provide four-fold wear protection over conventional products and command price premiums that customers accept when total cost of ownership is explained. North America and Europe remain at the forefront thanks to higher regulatory stringency and consumer awareness, yet momentum is spreading to urban markets in Asia-Pacific as dealership networks highlight extended drain intervals.

Stringent Emission and Fuel-Economy Regulations

July 2025 marked the planned start of Euro 7, while EPA 2026 tightens heavy-duty requirements in the United States. These rules mandate lower-viscosity grades such as 5W-20 and 0W-20, forcing lubricant formulators to boost oxidation stability to satisfy extended service limits of 650,000 miles for next-generation diesel engines. The ILSAC GF-7 specification adds LSPI protection and timing chain wear control that mineral oils struggle to achieve, making synthetic base stocks indispensable. China's evolving China VI and India's Bharat Stage VII frameworks are converging toward similar thresholds, which effectively globalize the most stringent requirements. Harmonized standards benefit multinational suppliers that can deploy one formulation worldwide, cutting validation cycles and strengthening economies of scale.

Higher Upfront Cost of Synthetic Lubricants

Full-synthetic products often sell at prices two to three times those of mineral oils, a differential that remains a stumbling block in cost-sensitive segments. In short duty cycles the benefit of extended drains is muted, preventing fleet managers in developing economies from justifying the premium. Caltex data confirm that where service intervals sit below 5,000 km, ROI is difficult to secure. Rising crude prices, however, are lifting the cost base of mineral oils faster than synthetics, narrowing the gap. Meanwhile, predictive maintenance tools underscore lifetime savings, gradually eroding resistance among commercial fleets.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Industrial Automation Demanding Advanced Hydraulic & Gear Oils

- Rapid Expansion in Aerospace, Defense and Offshore Renewables Demanding Synthetic Turbine & Gearbox Oils

- Growing Electric-Vehicle Fleet

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engine oils captured 34.58% of the synthetic lubricants market in 2024 by volume, a position protected by the vast installed base of internal-combustion vehicles and the superior longevity synthetics deliver. Transmission and gear oils follow as the second-largest category because automated manufacturing lines and wind turbines both require high-load, clean-running formulations. Hydraulic fluids benefit from a construction upswing and robotics integration, supplying stable viscosity across wide temperature spreads. Greases remain indispensable in aerospace actuators and heavy machinery joints where drip-free lubrication is vital. Metalworking fluids, though holding a smaller volume share, advance at the fastest 11.15% CAGR as precision machining and additive manufacturing mature.

The segment outlook is shaped by ILSAC GF-7 and API SQ, both of which reduce permissible wear and LSPI occurrence. This shift favors premium synthetics that can sustain longer drains, reducing workshop visits, and oil disposal. Furthermore, metalworking fluids with low mist and high flash points mitigate occupational hazards, leading factories to migrate to synthetic ester-and-PAG systems. Together, these trends ensure that the synthetic lubricants market size for fluids beyond engine oils will expand steadily through 2030.

The Synthetic Lubricants Market Report Segments the Industry by Product Type (Engine Oils, Transmission and Gear Oils, Hydraulic Fluids, and More), by Base Oil (Polyalpha-Olefin (PAO), Esters, Polyalkylene Glycol (PAG), and More), by End User (Power Generation, Automotive, Heavy Equipment, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Liters).

Geography Analysis

Asia-Pacific held 40.27% of the synthetic lubricants market in 2024, with a 11.03% CAGR outlook. China's re-acceleration in advanced manufacturing, together with India's double-digit vehicle sales rebound, underpins regional consumption. New blending plants in coastal China, such as Quaker Houghton's Zhangjiagang facility scheduled for 2026, illustrate suppliers' determination to localize supply for high-growth sectors. Japan sustains demand for high-grade factory fills, while Southeast Asian economies ramp up industrial output, widening the customer base.

North America ranks second in volume and remains a technology bellwether. EPA 2026 rules and API's category pipeline push formulators into next-generation additive chemistry. The United States also dominates supply of high-viscosity PAO thanks to extensive propylene infrastructure, although propylene tightness predicted for mid-2025 could test margins. Canada's oil sands and mining fleets, plus Mexico's automotive export platforms, add stable demand pockets that rely on synthetic lubricants for uptime and warranty assurance.

Europe preserves its premium positioning through stringent environmental legislation and advanced OEM technical standards. Euro 7 compels lower viscosities and stronger aftertreatment compatibility, pushing adoption of ester-enhanced formulations in both light- and heavy-duty fleets. The North Sea offshore wind corridor and the Iberian Peninsula's emerging renewable clusters require fill-for-life gearbox oils that tolerate brine exposure, widening scope for high-value PAG and PAO blends. Eastern Europe's industrial base further diversifies demand as automation investments accelerate. The Middle East and Africa, while smaller, show a gradual shift from mineral to synthetic as Gulf petrochemical hubs and South African mines target longer drain intervals in harsh climates.

- Shell plc

- Exxon Mobil Corporation

- BP p.l.c. (Castrol)

- Chevron Corporation

- TotalEnergies

- Valvoline Global Operations (Saudi Aramco)

- China Petrochemical Corporation (Sinopec)

- PETRONAS Lubricants International

- FUCHS SE

- ENEOS Corporation

- Indian Oil Corporation Ltd

- AMSOIL Inc.

- Idemitsu Kosan Co.,Ltd.

- Gazpromneft-Lubricants Ltd.

- LUKOIL

- Phillips 66 Company

- Suncor Energy Inc.

- Quaker Chemical Corporation

- Repsol

- Motul

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Usage of High-Performance Synthetic Engine Oils in the Automotive Aftermarket

- 4.2.2 Stringent Emission & Fuel-Economy Regulations

- 4.2.3 Growth in Industrial Automation Demanding Advanced Hydraulic & Gear Oils

- 4.2.4 Rapid Expansion in Aerospace & Defence Requiring Synthetic Turbine Oils

- 4.2.5 Surge in Offshore Wind Installations Boosting Long-Drain Synthetic Gearbox Oils

- 4.3 Market Restraints

- 4.3.1 Higher Upfront Cost Versus Mineral Oils

- 4.3.2 Growing Electric-Vehicle Fleet Reducing Demand for Engine Oils

- 4.3.3 Volatility in Polyalphaolefin (PAO) Feed-Stock Supply

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Engine Oils

- 5.1.2 Transmission and Gear Oils

- 5.1.3 Hydraulic Fluids

- 5.1.4 Metalworking Fluids

- 5.1.5 Greases

- 5.1.6 Other Product Types (General Industrial Oils, etc.)

- 5.2 By Base Oil

- 5.2.1 Polyalpha-olefin (PAO)

- 5.2.2 Esters

- 5.2.3 Polyalkylene Glycol (PAG)

- 5.2.4 Group III / GTL-derived Synthetic

- 5.2.5 Others (Alkylated Naphthalene, etc.)

- 5.3 By End User

- 5.3.1 Automotive

- 5.3.2 Power Generation

- 5.3.3 Heavy Equipment

- 5.3.4 Metallurgy and Metalworking

- 5.3.5 Other End-user Industries (Oil and Gas, Marine, Data-centres, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Indonesia

- 5.4.1.7 Thailand

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Egypt

- 5.4.5.5 South Africa

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Shell plc

- 6.4.2 Exxon Mobil Corporation

- 6.4.3 BP p.l.c. (Castrol)

- 6.4.4 Chevron Corporation

- 6.4.5 TotalEnergies

- 6.4.6 Valvoline Global Operations (Saudi Aramco)

- 6.4.7 China Petrochemical Corporation (Sinopec)

- 6.4.8 PETRONAS Lubricants International

- 6.4.9 FUCHS SE

- 6.4.10 ENEOS Corporation

- 6.4.11 Indian Oil Corporation Ltd

- 6.4.12 AMSOIL Inc.

- 6.4.13 Idemitsu Kosan Co.,Ltd.

- 6.4.14 Gazpromneft-Lubricants Ltd.

- 6.4.15 LUKOIL

- 6.4.16 Phillips 66 Company

- 6.4.17 Suncor Energy Inc.

- 6.4.18 Quaker Chemical Corporation

- 6.4.19 Repsol

- 6.4.20 Motul

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Growing Adoption of Bio-lubricants