|

市场调查报告书

商品编码

1939103

汽车涂料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

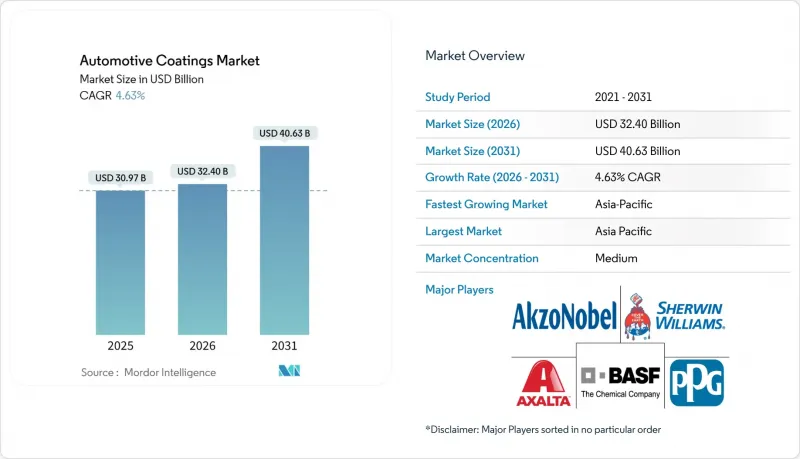

2025年汽车涂料市场价值为296亿美元,预计到2031年将达到388.2亿美元,高于2026年的309.7亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.62%。

全球汽车生产的復苏、向低VOC配方的转变以及电动车(EV)产量的激增,都支撑着不断增长的需求。然而,原物料价格的波动和日益严格的溶剂法规正给利润率带来压力。供应商正在加速采用水性涂料和粉末涂料系统,以在满足即将出台的排放法规的同时,保持与原厂配套(OEM)产品相同的耐久性。 OEM涂装车间的数位化,包括在线连续固化、机器人检测和基于云端的配色,在提高生产效率的同时,也提高了技术准入门槛。同时,市场分散仍在持续,中型区域供应商与有能力投资大规模永续性和自动化项目的跨国公司展开激烈的市场份额争夺。

全球汽车涂料市场趋势与洞察

全球汽车产量復苏并扩张

预计到2024年,北美轻型车产量将达到1,550万辆,延续成长势头,并支撑工厂对车身外部和底盘涂料的需求。轻型卡车目前占每月销量的84%,推动了高端耐刮透明涂层的消费。在中国,产能的提升和出口的强劲势头支撑着稳定的涂料需求,但区域产能过剩的担忧也开始显现。疫情造成的衝击过后,全球汽车製造商已恢復了可预测的采购计划,使供应商能够优化批量生产和物流。随着汽车製造商在追求品牌专属美学的同时满足耐久标准,对先进涂装自动化和差异化涂装技术的投资也日益凸显。

为符合VOC法规,过渡到水性和粉末涂料系统。

加州严格的VOC排放上限将于2025年生效,欧盟绿色交易的推进正在加速溶剂型涂料的重新配方。水性底涂层在大型汽车修理厂的渗透率已达64%,证明了商业性可行性。BASF的Glaslit 100系列产品就是一个典型的例子,这是一款高效低VOC产品,已被1000多家碰撞维修中心采用。粉末涂料在轮毂、引擎室和电动车电池外壳等领域的市场份额不断增长,这主要得益于雷射固化炉的广泛应用,雷射固化炉可降低50%的能耗。拥有丰富树脂和颜料产品组合的供应商正透过在更严格的法规出台前迅速引导客户转向粉末涂料,从而获得先发优势。

严格限制溶剂和异氰酸酯的暴露

美国职业安全与健康管理局 (OSHA) 的重点监督计画加强了对喷漆房的检查,强制要求提高通风量并个人防护设备,以降低异氰酸酯相关气喘和皮肤炎的风险。小规模的汽车修补企业面临着因遵守法规而产生的巨额资金成本,或者被迫转型使用低异氰酸酯化学品,这可能会牺牲性能。底漆和透明涂层配方生产商正在将不含聚脲的替代品推向市场,但由于耐久性标准仍在不断检验,这些替代品的推广应用仍然持谨慎态度。

细分市场分析

到2025年,丙烯酸涂料将占汽车涂料市场需求的48.10%,凭藉其成本效益和均衡的耐候性,巩固其市场地位。聚氨酯涂料到2031年将以5.00%的复合年增长率成长,满足对优质透明涂层和柔性基材的需求,尤其适用于对耐刮擦性能要求极高的豪华运动型多用途车(SUV)和电动车(EV)。随着新型脂肪族二异氰酸酯化学品符合严格的黄变测试标准,预计北美OEM生产线中的聚氨酯汽车涂料市场规模将显着扩大。环氧树脂将继续在阴极电涂装这一细分市场占据主导地位,因为防腐蚀至关重要;同时,生物基混合技术正在欧洲OEM主导的概念项目中崭露头角。

聚氨酯的需求成长主要受产品使用寿命延长的推动,这促使人们对其耐用性提出更高要求。然而,美国职业安全与健康管理局 (OSHA) 对异氰酸酯处理的监管日益严格,促使企业投资建造封闭式混合单元和机器人喷涂室。科思创等供应商目前提供含 33% 回收碳的聚氨酯,显示符合原始设备製造商 (OEM) 的永续性目标。丙烯酸化学品製造商则积极研发新一代交联剂,以提高耐腐蚀性,同时不增加挥发性有机化合物 (VOC) 的含量。竞争优势越来越依赖兼具机械韧性和低温固化性能的专利组合,从而满足能源使用法规和轻质基材的要求。

溶剂型涂料凭藉其优异的流动性和显色性,在金属漆和珠光漆的涂装中仍将占据70.20%的市场份额。然而,随着全球VOC排放上限的日益严格,汽车涂料市场正明显转向其他技术。水性涂料目前在欧盟OEM底涂层线中占据主导地位,日本OEM厂商如马自达已实现了15克/平方米的行业最低VOC排放。粉末涂料虽然目前仍占少数,但随着节能型雷射固化隧道在电动车零件生产线上的普及,预计其复合成长率将最高。

在监管区域,水性修补漆已占据汽车涂料市场60%以上的份额,因为汽车修理厂需要遵守环保许可规定。树脂乳化和闪蒸控制的技术突破消除了水性漆与溶剂型底漆的性能差距。一级供应商正利用模组化树脂结构实现快速配方调整,以应对新法规对挥发性有机化合物(VOC)和有害空气污染物(HAPS)排放限量的日益严格,从而保护客户免受法规週期中期合规方面的意外情况。

区域分析

到2025年,亚太地区将占全球收入的58.40%,这主要得益于中国崛起为净出口国以及在主导地位。印尼百万吨级涂料厂和越南快速发展的供应商园区等产能扩张项目,支撑着该地区6.05%的复合年增长率预测。本地整车製造商正与跨国配方商合作,在保持与溶剂型涂料外观一致性的同时,实现水性树脂的在地化生产。政府对新能源汽车的支持措施也进一步推动了对电池专用功能涂料的需求。

预计2024年北美轻型汽车产量将成长9.6%,产能紧张的工厂通常会运作运转,从而为涂料定价创造有利条件。美国农业部(USDA)的BioPreferred法规以及美国环保署(EPA)计划收紧对全氟烷基物质(PFAS)的限制,正在推动无氟面漆的快速认证,并迫使供应商加快研发步伐。随着加拿大和墨西哥的企业遵守美国法规,低VOC系统的汽车涂料市场份额预计将会扩大。

欧洲对碳中和的重视促使原始设备製造商(OEM)安装100%再生能源的喷漆车间和溶剂回收焚化炉。二氧化钛反倾销税推高了成本结构,但干式洗涤喷漆室和封闭回路型污泥回收技术的广泛应用在一定程度上抵消了成本增加。包括波兰和匈牙利在内的东欧丛集的崛起,提供了低工资的组装,但也要求供应商为一级喷漆模组建立准时制生产中心。

在南美洲,由于南方共同市场关税的降低,汽车製造商正加快向巴西和阿根廷转移新型SUV平台,从而增加了整车厂的涂料消耗量。然而,汇率波动迫使涂料製造商采用与美元挂钩的合约。儘管中东和非洲地区仍处于发展中,但预计未来前景光明,沙乌地阿拉伯的「2030愿景」旨在促进国内汽车生产,并扩大涂料生产设施以供应出口市场。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球汽车产量復苏并扩张

- 为符合VOC法规,正在过渡到水性和粉末系统。

- 对电动车专用涂层(用于电池温度控管)的需求不断增长

- 成熟市场的碰撞维修量復苏

- 原始设备製造商采用数位配色和在线连续固化技术

- 市场限制

- 严格限制溶剂和异氰酸酯的暴露

- 石化原料价格波动

- 电动滑板平台减少了喷漆面积

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依树脂类型

- 聚氨酯

- 环氧树脂

- 丙烯酸纤维

- 其他的

- 透过技术

- 溶剂型

- 水溶液

- 粉末

- 透过涂层

- 电着底漆

- 底漆

- 底涂层

- 透明涂层

- 透过使用

- OEM

- 翻新

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 印尼

- 马来西亚

- 泰国

- 其他东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Akzo Nobel NV

- Asian Paints PPG Pvt., Ltd.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Cabot Corporation

- Eastman Chemical Company

- Hempel A/S

- HMG Paints Limited

- Jotun

- Kansai Nerolac Paints Limited

- KCC Corporation

- Nippon Paint Holdings Co., Ltd.

- Parker Hannifin Corp

- PPG Industries Inc.

- RPM International Inc.

- Shanghai Kinlita Chemical Co., Ltd.

- The Sherwin-Williams Company

第七章 市场机会与未来展望

The Automotive Coatings Market was valued at USD 29.60 billion in 2025 and estimated to grow from USD 30.97 billion in 2026 to reach USD 38.82 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

The rebound in global vehicle production, the pivot toward low-Volatile Organic Compound (VOC) formulations, and surging electric-vehicle (EV) output underpin demand expansion, even as raw-material price swings and tightening solvent regulations constrain margins. Suppliers are accelerating launches of water-borne and powder systems that comply with imminent emissions caps while still delivering Original Equipment Manufacturer (OEM)-level durability. OEM paint-shop digitalization spanning inline curing, robotic inspection, and cloud-based color matching is raising throughput and widening technical barriers to entry. Meanwhile, fragmentation persists as regional midsized suppliers vie for share against multinationals that can fund large-scale sustainability and automation programs.

Global Automotive Coatings Market Trends and Insights

Growing Global Vehicle Production Rebound

North American light-vehicle output reached 15.5 Million units in 2024 and continues rising, sustaining factory demand for exterior and under-body coatings. Light trucks now represent 84% of monthly sales, propelling the consumption of premium, scratch-resistant clear coats. In China, capacity additions and export momentum reinforce steady coating volumes, even as localized overcapacity looms. Automakers worldwide reinstate predictable sourcing schedules after pandemic disruptions, enabling suppliers to optimize batch production and logistics. Parallel investments in advanced paint-shop automation and differentiated finishes surfaced as OEMs seek brand-distinctive aesthetics while meeting durability standards .

Shift Toward Water-borne & Powder Systems to Meet VOC Caps

The 2025 enforcement of stricter VOC ceilings in California and forthcoming EU Green Deal measures are accelerating reformulation of solvent-borne systems. Leading body shops already report 64% penetration of water-borne basecoats, validating commercial viability. BASF's Glasurit 100 Line exemplifies high-efficiency, low-VOC products now used by more than 1,000 collision centers. Powder coatings are gaining share in wheels, under-hood parts, and EV battery casings, helped by laser-curing ovens that cut energy use by 50%. Suppliers with broad resin and pigment portfolios are fastest to convert customers, establishing early-mover advantages before regulations tighten further.

Stringent Solvent & Isocyanate Exposure Limits

Occupational Safety and Health Administration (OSHA)'s National Emphasis Program intensifies inspections of paint booths, mandating enhanced ventilation and personal protective equipment to mitigate asthma and dermatitis risks from isocyanates . Small refinishing operations face steep capital costs for compliant spray booths or must migrate to low-isocyanate chemistries that may sacrifice performance. Primer and clear-coat formulators commercialize polyurea-free variants, although adoption remains cautious while durability benchmarks are validated.

Other drivers and restraints analyzed in the detailed report include:

- Rising EV-specific Coating Demand for Battery Thermal Management

- Recovery of Collision-repair Volumes in Mature Markets

- Volatile Petrochemical-based Raw-material Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, acrylics supplied 48.10% of the Automotive Coatings market demand, cementing their status owing to cost-efficiency and balanced weatherability. Polyurethane formulations, advancing at a 5.00% CAGR to 2031, fulfill premium clear-coat and flexible-substrate needs, especially on luxury Sports Utility Vehicles (SUVs) and EVs requiring superior scratch resistance. The automotive coatings market size for polyurethane systems is expected to widen notably in North American OEM lines as new aliphatic diisocyanate chemistries meet stricter yellowing tests. Epoxy resins continue niche dominance in cathodic e-coats where corrosion protection is critical, while bio-based hybrids are emerging in concept programs led by European OEMs.

The polyurethane push is amplified by longer ownership cycles driving demand for durability, though OSHA scrutiny around isocyanate handling is prompting investment in closed-mixing cells and robot-spray enclosures. Suppliers such as Covestro now offer 33% renewable-carbon polyurethanes, illustrating alignment with OEM sustainability targets. Acrylic chemists are responding with next-generation crosslinkers that improve mar resistance without raising VOC levels. Competitive advantage increasingly hinges on patent portfolios that combine mechanical robustness with low-temperature cure profiles, addressing both energy-use mandates and lightweight-substrate requirements.

Solvent-borne finishes still held 70.20% revenue in 2025, propelled by superior flow and color depth demanded on metallic and pearlescent shades. Yet the automotive coatings market is unmistakably tilting toward alternatives as global VOC ceilings narrow. Water-borne systems now dominate EU OEM base-coat lines, with Japanese OEMs such as Mazda achieving industry-low emissions of 15 g VOC/m2. Powder coatings, while presently a minority, post the highest compound growth as energy-efficient laser-cure tunnels become standard on EV component lines.

The automotive coatings market share for water-borne refinish lines has surpassed 60% in regulated regions as body shops align with environmental permits. Technological breakthroughs in resin emulsification and flash-off control have closed the performance gap with solvent-borne primers. Tier-one suppliers leverage modular resin architectures, enabling fast reformulation when each new rule tightens permissible VOCs or HAPS (hazardous air pollutants), insulating customers from mid-cycle compliance surprises.

The Automotive Coatings Market Report is Segmented by Resin Type (Polyurethane, Epoxy, Acrylic, and Others), Technology (Solvent-Borne, Water-Borne, and Powder), Coating Layer (E-Coat, Primer, Base Coat, and Clear Coat), Application (OEM and Refinish), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 58.40% of global 2025 revenue, buoyed by China's ascent as a net exporter and leadership in EV output. Capacity additions such as Indonesia's million-ton paint plant and Vietnam's fast-growing supplier parks underpin a 6.05% regional CAGR forecast. Local OEMs collaborate with multinational formulators to localize water-borne resins while preserving appearance parity with solvent benchmarks. Government stimulus on new-energy vehicles further amplifies demand for battery-specific functional coatings.

North America, with light-vehicle builds rising 9.6% in 2024, exhibits that constrained capacity plants regularly exceed rated throughput, creating favorable pricing for coatings. Stringent United States Department of Agriculture (USDA) BioPreferred and upcoming Environmental Protection Agency (EPA) per- and polyfluoroalkyl substances (PFAS) rules spur rapid qualification of fluorine-free top coats, compelling suppliers to accelerate R&D. The automotive coatings market share of low-VOC systems is poised to expand as Canadian and Mexican operations align with United States regulations.

Europe's focus on carbon neutrality pushes OEMs toward 100% renewable-electric paint shops and solvent-capture incinerators. Anti-dumping duties on titanium dioxide elevate cost structures, but wide adoption of dry-scrubber booths and closed-loop sludge recycling partially offsets outlays. Eastern European cluster growth, including Poland and Hungary offers lower-wage assembly yet requires suppliers to establish just-in-sequence hubs for tier-one paint modules.

South America benefits from Mercosur tariff reductions that encourage automakers to allocate new SUV platforms to Brazil and Argentina, lifting OEM-paint consumption. Nonetheless, currency volatility prompts formulators to adopt US-dollar-pegged contracts. Middle East & Africa remains nascent but shows promise as Saudi Arabia's Vision 2030 sparks domestic vehicle production and related coating capacity build-outs targeting export markets.

- Akzo Nobel N.V.

- Asian Paints PPG Pvt., Ltd.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Cabot Corporation

- Eastman Chemical Company

- Hempel A/S

- HMG Paints Limited

- Jotun

- Kansai Nerolac Paints Limited

- KCC Corporation

- Nippon Paint Holdings Co., Ltd.

- Parker Hannifin Corp

- PPG Industries Inc.

- RPM International Inc.

- Shanghai Kinlita Chemical Co., Ltd.

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Global Vehicle Production Rebound

- 4.2.2 Shift Toward Water-borne & Powder Systems to Meet VOC Caps

- 4.2.3 Rising EV-specific Coating Demand for Battery Thermal Management

- 4.2.4 Recovery of Collision-repair Volumes in Mature Markets

- 4.2.5 OEM Adoption of Digital Color-matching & Inline Curing

- 4.3 Market Restraints

- 4.3.1 Stringent Solvent & Isocyanate Exposure Limits

- 4.3.2 Volatile Petrochemical-based Raw-material Pricing

- 4.3.3 EV Skateboard Platforms Reducing Painted Surface Area

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Others

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Powder

- 5.3 By Coating Layer

- 5.3.1 E-coat

- 5.3.2 Primer

- 5.3.3 Base Coat

- 5.3.4 Clear Coat

- 5.4 By Application

- 5.4.1 OEM

- 5.4.2 Refinish

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Australia and New Zealand

- 5.5.1.6 Indonesia

- 5.5.1.7 Malaysia

- 5.5.1.8 Thailand

- 5.5.1.9 Rest of ASEAN

- 5.5.1.10 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Egypt

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Asian Paints PPG Pvt., Ltd.

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF

- 6.4.5 Beckers Group

- 6.4.6 Cabot Corporation

- 6.4.7 Eastman Chemical Company

- 6.4.8 Hempel A/S

- 6.4.9 HMG Paints Limited

- 6.4.10 Jotun

- 6.4.11 Kansai Nerolac Paints Limited

- 6.4.12 KCC Corporation

- 6.4.13 Nippon Paint Holdings Co., Ltd.

- 6.4.14 Parker Hannifin Corp

- 6.4.15 PPG Industries Inc.

- 6.4.16 RPM International Inc.

- 6.4.17 Shanghai Kinlita Chemical Co., Ltd.

- 6.4.18 The Sherwin-Williams Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Self-Cleaning Coating Technology

日本汽车涂料市场规模、份额、趋势及预测(按树脂类型、技术、分层、应用和地区划分),2026-2034年

日本汽车涂料市场规模、份额、趋势及预测(按树脂类型、技术、分层、应用和地区划分),2026-2034年 2026年全球汽车涂料市场报告

2026年全球汽车涂料市场报告 汽车底盘涂料市场按产品类型、技术、性能类型、应用方法、车辆类型、分销管道和最终用户划分-2026-2032年全球预测汽车底盘防锈涂料市场(按涂层类型、应用技术、动力类型、涂层技术、价格等级、车辆类型、最终用户和分销管道划分),全球预测,2026-2032年汽车涂料颜料市场(按颜料类型、树脂类型、涂料形式、颜色、车辆类型和应用划分)-2026-2032年全球预测汽车照明光学模具市场按类型、材质、型腔、应用和最终用户划分-2026-2032年全球预测汽车玻璃涂层市场:按类型、固化技术、应用方法、车辆类型、最终用户和销售管道划分-2026-2032年全球预测环保水性涂料市场:依树脂类型、涂料类型、价格范围、技术、应用、通路和最终用途产业划分-2026-2032年全球预测

汽车底盘涂料市场按产品类型、技术、性能类型、应用方法、车辆类型、分销管道和最终用户划分-2026-2032年全球预测汽车底盘防锈涂料市场(按涂层类型、应用技术、动力类型、涂层技术、价格等级、车辆类型、最终用户和分销管道划分),全球预测,2026-2032年汽车涂料颜料市场(按颜料类型、树脂类型、涂料形式、颜色、车辆类型和应用划分)-2026-2032年全球预测汽车照明光学模具市场按类型、材质、型腔、应用和最终用户划分-2026-2032年全球预测汽车玻璃涂层市场:按类型、固化技术、应用方法、车辆类型、最终用户和销售管道划分-2026-2032年全球预测环保水性涂料市场:依树脂类型、涂料类型、价格范围、技术、应用、通路和最终用途产业划分-2026-2032年全球预测 欧洲汽车涂料市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)

欧洲汽车涂料市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年) 全球环保涂料及化学品市场预测(至2032年):依产品种类、原料、技术、应用及地区划分

全球环保涂料及化学品市场预测(至2032年):依产品种类、原料、技术、应用及地区划分