|

市场调查报告书

商品编码

1851436

云端迁移:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Cloud Migration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

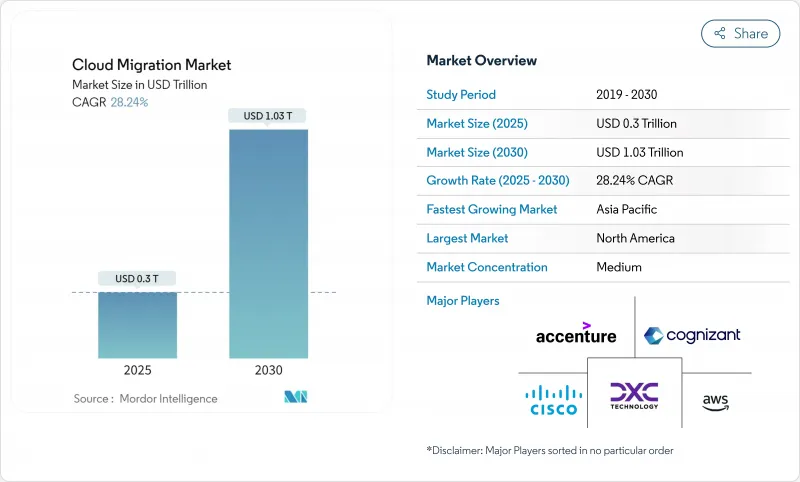

预计到 2025 年,云端迁移市场规模将达到 3,000 亿美元,到 2030 年将达到 1.03 兆美元,年复合成长率为 28.24%。

这种快速成长反映了企业正从资本密集的本地资产转向可扩展的云端环境,从而实现更快的创新週期和更好的成本控制。推动这一趋势的因素包括:生成式人工智慧工作负载的加速发展、混合云策略的扩展以及日益严格的范围 3 碳排放报告要求(这些要求有利于云端原生架构)。儘管公有云仍保持领先地位,但随着企业努力平衡效能、合规性和成本优化目标,混合云模式正在兴起。大型企业的云端采用率仍然很高,但随着自动化迁移工具链降低技术门槛,中小企业正在缩小差距。按行业划分,银行、金融服务和保险 (BFSI) 以及医疗保健行业的云端采用率正在加速增长,而超大规模云端服务提供商和垂直领域专家则在对供应商锁定和退出费用的担忧下,继续扩展其服务组合。

全球云端迁移市场趋势与洞察

经济高效且扩充性的云端部署优势

将工作负载迁移到云端后,企业营运成本节省了 20-30%,这主要得益于无需进行资本密集的硬体更新週期,以及按需合理配置资源。 Infomart 的 B2B 平台迁移到 Oracle 云端基础架构后,资料中心成本降低了 38%,同时提升了效能弹性。灵活的资源配置使企业能够应对突如其来的需求高峰,而无需像实体资料中心环境那样经历 6-12 个月的采购延迟。从基础设施维护中节省下来的预算越来越多地被用于推动创新倡议,从而提升竞争力。这些累积效益使得成本合理化策略成为预期复合年增长率影响最大的因素。

远距办公和自备设备办公(BYOD)的普及率正在上升

随着混合办公模式的普及,企业正强制将协作套件、身分服务和安全管理迁移到云端,以确保无论使用者身处何地或使用何种设备,都能获得一致的使用者体验。最近的一项调查显示,89% 的 IT 领导者计划在 2025 年增加云端支出,以支援分散式团队。自带装置办公室 (BYOD) 让边界安全更加复杂,促使企业转向更容易以云端原生方式实施的零信任架构。因此,企业正日益重视安全存取服务边缘、端点管理和即时分析层,以确保员工随时随地都能有效率地运作。这一趋势将在不久的将来对计划流程产生重大影响,尤其是在北美和欧洲地区。

资料安全和监管合规风险

欧洲企业难以将《一般资料保护规则》(GDPR) 与公共云端服务模式协调,而全球金融机构则疲于应对重迭的司法管辖区规则,这些规则很少明确规定云端资料流。责任共用模式往往模糊了加密、日誌和事件回应的课责。在某些情况下,主权云端要求迫使企业为本地化容量支付额外费用或维护本地基础设施,从而延长了迁移时间。这些因素几乎限制了所有行业的成长,尤其是在医疗保健、银行和政府部门。

细分市场分析

混合部署成长最快,年复合成长率高达 18.7%,企业在满足本地部署的低延迟需求和公共云端的标准优势之间寻求平衡。公共云端目前仍占据 55.4% 的市场份额,这主要得益于超大规模云端供应商成熟的安全态势。边缘云端整合将运算资源更靠近用户,同时保持弹性后端分析连接,未来的架构将支援将多个执行节点整合到单一工作流程中。能够编配工作负载跨节点部署的迁移专家仍供不应求。

企业不再将部署视为非此即彼的选择。金融机构将交易引擎部署在私有丛集上以实现亚毫秒延迟,同时将监管报告任务卸载到成本效益更高的公共储存桶中。医疗机构在本地处理影像数据,并将匿名化后的数据集路由到云端的AI管道。正是这些细緻入微的部署方案解释了为何混合部署方案在云端迁移市场中持续扩大其市场份额。

到2024年,大型企业将占据云端迁移市场62%的份额,这反映了它们多年期的转型预算和全球布局。然而,中小企业将呈现18%的复合年增长率,这主要得益于打包式迁移工具链的普及,这些工具链能够缩短设定时间并降低专业知识门槛。云端服务供应商目前正在对其产品进行细分,例如为财富500强客户提供深度咨询服务,为中小企业提供标准化的模板,从而在不损害净利率的前提下扩大其服务范围。

中小企业倾向于选择SaaS替代方案和託管服务,以避免组建成本高昂的内部营运团队。相反,大型企业通常会在数十个业务部门内进行渐进式架构重构,并由卓越中心提供支持,这些中心负责制定管治和安全蓝图。这种差异迫使服务供应商采取不同的市场策略,以适应不同客户群的预算週期和合规要求。

区域分析

到2024年,北美将占全球云端支出的37.8%,这主要得益于早期采用者专注于人工智慧优化和多重云端成本管治。美国凭藉联邦政府的云端计画(例如83亿美元的现代化预算)处于领先地位,而加拿大和墨西哥则利用网路骨干网路的改进来加速云端采用。在全部区域,企业正在整合预测性工作负载部署引擎,以优化消费模型并控制出口费用,从而巩固北美作为云端迁移市场核心参与者的地位。

亚太地区预计到2030年将以18.5%的复合年增长率成长,这主要得益于各国数位转型基金和对超大规模资料中心的投资。微软已累计29亿美元在日本扩建资料中心,显示对日本云端运算发展前景充满信心。预计到2028年,印度的云端运算市场规模将达到255亿美元,这反映出银行、金融服务和保险(BFSI)、零售、政府等行业的广泛现代化。中国本土云端服务供应商凭藉客製化的自主服务,在数据本地化规则的支持下,持续扩大市场份额。该地区多元化的监管环境造就了混合云端和多重云端架构的复杂局面,企业在迁移过程中必须应对这些挑战。

欧洲正经历稳定成长与严格的资料主权法规并存的局面。德国和英国仍然是最大的采用者,而法国和西班牙则支持赋能本土供应商的主权云端框架。 GDPR 的实施要求所有计划都必须进行细緻的驻留映射和加密管治。因此,混合策略正成为主流,将敏感工作负载保留在国内,并利用可扩展的区域节点执行分析和人工智慧任务。这种动态将使欧洲的迁移模式在整个预测期内始终与合规优先的架构保持一致。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 经济高效且扩充性的云端部署优势

- 远距办公和自备设备办公(BYOD)的普及

- 政府数位转型基金

- 混合/多重云端策略的兴起

- 重构以加速生成式人工智慧工作负载

- 范围 3彙报以推进碳意识转型

- 市场限制

- 资料安全和监管合规风险

- 传统应用程式的复杂性和互通性

- 云端出口费用上涨如何影响整体拥有成本

- 主权云端指令可能导致供应商锁定

- 价值/供应链分析

- 监管环境

- 技术展望

- 宏观经济因素的影响

- 投资分析

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依部署类型

- 公有云

- 私有云端

- 混合云

- 多重云端

- 按公司规模

- 中小企业

- 大公司

- 按服务类型

- Infrastructure-as-a-Service(IaaS)

- Platform-as-a-Service(PaaS)

- Software-as-a-Service(SaaS)

- 透过迁移方法

- 迁移和重新託管

- 平台重构

- 重构/重新架构

- 替代方案(SaaS 替代方案)

- 按最终用户行业划分

- 银行、金融服务和保险(BFSI)

- 医疗保健和生命科学

- 零售与电子商务

- 政府/公共部门

- 资讯科技/通讯

- 製造业

- 能源与公共产业

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 非洲

- 南非

- 奈及利亚

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Accenture plc

- Amazon Web Services Inc.

- Cisco Systems Inc.

- Cognizant Technology Solutions Corporation

- DXC Technology Company

- Evolve IP LLC

- Google LLC

- International Business Machines Corporation(IBM)

- Microsoft Corporation

- Oracle Corporation

- Rackspace Technology Inc.

- Flexera Software LLC(RightScale)

- Tech Mahindra Limited

- VMware Inc.

- WSM International LLC

- Infosys Limited

- HCL Technologies Limited

- Capgemini SE

- Atos SE

- Fujitsu Limited

- Alibaba Cloud(Alibaba Group Holding Limited)

- Kyndryl Holdings Inc.

- Tata Consultancy Services Limited

- NTT Data Corporation

第七章 市场机会与未来展望

The cloud migration market size stands at USD 0.30 trillion in 2025 and is on track to reach USD 1.03 trillion by 2030, expanding at a 28.24% CAGR.

This rapid upside reflects how enterprises are shifting from capital-intensive on-premises assets toward scalable cloud environments that permit faster innovation cycles and superior cost control. Momentum is fueled by generative-AI workload acceleration, expanding hybrid strategies, and mounting Scope-3 carbon-reporting obligations that favor cloud-native architectures. Public cloud keeps its leadership position, yet hybrid patterns are gaining ground as firms work to balance performance with compliance and cost-optimization goals. Large enterprises remain the biggest spenders, but small and medium enterprises (SMEs) are closing the gap as automated migration toolchains lower technical barriers. Across industries, Banking, Financial Services and Insurance (BFSI) and Healthcare are pacing adoption, while hyperscale providers and niche specialists continue to broaden service portfolios amid vendor-lock-in and egress-fee concerns.

Global Cloud Migration Market Trends and Insights

Cost-efficiency and Scalability Advantages of Cloud Adoption

Enterprises continue to realize 20-30% operational-expenditure savings after moving workloads to the cloud, primarily by eliminating capital-intensive hardware refresh cycles and right-sizing resources on demand. Infomart's business-to-business platform migration to Oracle Cloud Infrastructure cut data-center costs by 38% while boosting performance flexibility. Elastic resource provisioning now allows organizations to handle unexpected demand spikes without the six-to-twelve-month procurement delays common in physical data-center environments. Budget freed from infrastructure upkeep is increasingly redirected toward innovation initiatives that sharpen competitive differentiation. These cumulative benefits give cost-rationalization strategies the highest positive impact on the forecast CAGR.

Rising Remote-work & BYOD Penetration

Hybrid work models have solidified, prompting organizations to migrate collaboration suites, identity services and security controls to the cloud to guarantee consistent user experiences across locations and devices. A recent survey shows 89% of IT leaders intend to raise cloud spending in 2025 to support distributed teams. BYOD complicates perimeter security, steering enterprises toward zero-trust architectures that are easier to enforce in cloud-native form. Consequently, migrations increasingly encompass secure access service edge, endpoint management and real-time analytics layers that maintain workforce productivity from any location. This trend exerts a strong, near-term pull on project pipelines, particularly in North America and Europe.

Data-security and Regulatory-compliance Risks

European firms struggle to reconcile General Data Protection Regulation (GDPR) stipulations with public-cloud service models, while global financial institutions juggle overlapping jurisdictional rules that rarely address cloud data flows explicitly. The shared-responsibility model often blurs accountability for encryption, logging and incident response. In some cases, sovereign-cloud requirements force organizations to pay premiums for localized capacity or retain on-premises infrastructure, extending migration timelines. These factors temper growth across nearly every industry, especially healthcare, banking and government.

Other drivers and restraints analyzed in the detailed report include:

- Government Digital-transformation Funding

- Proliferation of Hybrid / Multi-cloud Strategies

- Legacy-application Complexity and Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are the fastest riser, advancing at an 18.7% CAGR as enterprises balance low-latency on-premises demands with public-cloud scale. Public cloud still holds 55.4% cloud migration market share due to the mature security posture of hyperscale providers. Edge-cloud integrations now push compute closer to the user while maintaining elastic backend analytics connectivity, signaling that future architectures will combine multiple execution venues within a single workflow. Migration specialists able to orchestrate workload placement across these nodes remain in high demand.

Enterprises no longer view deployment as a binary choice. Financial institutions position trading engines on private clusters for sub-millisecond latency while offloading regulatory reporting to cost-efficient public buckets. Healthcare groups process imaging data on-site, then route anonymized sets to AI pipelines in the cloud. These nuanced blueprints underline why hybrid options will keep expanding their footprint within the cloud migration market.

Large enterprises accounted for 62% of cloud migration market size in 2024, reflecting multi-year transformation budgets and global rollouts. Yet SMEs exhibit an 18% CAGR, propelled by packaged migration toolchains that cut setup time and lower expertise thresholds. Cloud providers now segment offerings-white-glove consulting for Fortune 500 clients versus prescriptive templates for smaller firms-thereby widening addressable demand without eroding margins.

SMEs gravitate toward SaaS replacements and managed services to avoid staffing expensive in-house operations teams. Conversely, large entities pursue phased re-architecting across dozens of business units, often underpinned by center-of-excellence teams that codify governance and security blueprints. This bifurcation requires service vendors to maintain differentiated go-to-market motions tailored to each cohort's budget cycles and compliance obligations.

The Cloud Migration Market Report is Segmented by Deployment Type (Public Cloud, Private Cloud, Hybrid Cloud, Multi-Cloud), Enterprise Size (Small and Medium Enterprises, Large Enterprises), Service Type (IaaS, Paas, Saas), Migration Approach (Lift-And-Shift, Re-Platform, Refactor/Re-architect, Replace), End-User Vertical (BFSI, Healthcare, Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 37.8% of 2024 spend, anchored by early adopters that now focus on AI optimization and multi-cloud cost governance. The United States leads through federal cloud programs such as the USD 8.3 billion modernization budget, while Canada and Mexico leverage improved network backbones to accelerate adoption. Across the region, organizations are integrating predictive workload placement engines to refine consumption models and curb egress charges, reinforcing North America's position at the core of the cloud migration market.

Asia-Pacific is projected to post an 18.5% CAGR to 2030, propelled by state-level digital-transformation funds and hyperscaler investments. Microsoft earmarked USD 2.9 billion for data-center expansion in Japan, demonstrating confidence in Japan's cloud trajectory. India is on course for a USD 25.5 billion cloud sector by 2028, reflecting widespread modernization across BFSI, retail and government. China's domestic providers, supported by data-localization rules, continue to grow market share via tailored sovereign offerings. The region's diverse regulatory landscape shapes a patchwork of hybrid and multi-cloud designs that migration firms must navigate.

Europe pairs steady growth with stringent data-sovereignty controls. Germany and the United Kingdom remain the largest adopters, yet France and Spain are championing sovereign-cloud frameworks that bolster domestic vendors. GDPR enforcement compels meticulous residency mapping and encryption governance across every project. Consequently, hybrid strategies dominate, allowing sensitive workloads to stay on national soil while analytics and AI tasks harness scalable regional nodes. This dynamic will keep Europe's migration profile firmly tied to compliance-first architectures throughout the forecast period.

- Accenture plc

- Amazon Web Services Inc.

- Cisco Systems Inc.

- Cognizant Technology Solutions Corporation

- DXC Technology Company

- Evolve IP LLC

- Google LLC

- International Business Machines Corporation (IBM)

- Microsoft Corporation

- Oracle Corporation

- Rackspace Technology Inc.

- Flexera Software LLC (RightScale)

- Tech Mahindra Limited

- VMware Inc.

- WSM International LLC

- Infosys Limited

- HCL Technologies Limited

- Capgemini SE

- Atos SE

- Fujitsu Limited

- Alibaba Cloud (Alibaba Group Holding Limited)

- Kyndryl Holdings Inc.

- Tata Consultancy Services Limited

- NTT Data Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-efficiency and scalability advantages of cloud adoption

- 4.2.2 Rising remote-work and BYOD penetration

- 4.2.3 Government digital-transformation funding

- 4.2.4 Proliferation of hybrid / multi-cloud strategies

- 4.2.5 Generative-AI workload acceleration of refactoring

- 4.2.6 Scope-3 reporting pushes carbon-aware migrations

- 4.3 Market Restraints

- 4.3.1 Data-security and regulatory-compliance risks

- 4.3.2 Legacy-application complexity and interoperability

- 4.3.3 Escalating cloud-egress fees impact TCO

- 4.3.4 Vendor lock-in fears amid sovereign-cloud mandates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macro-Economic Factors

- 4.8 Investment Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.1.4 Multi-Cloud

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Service Type

- 5.3.1 Infrastructure-as-a-Service (IaaS)

- 5.3.2 Platform-as-a-Service (PaaS)

- 5.3.3 Software-as-a-Service (SaaS)

- 5.4 By Migration Approach

- 5.4.1 Lift-and-Shift (Re-hosting)

- 5.4.2 Re-platform

- 5.4.3 Refactor / Re-architect

- 5.4.4 Replace (SaaS Substitution)

- 5.5 By End-user Vertical

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Retail and E-commerce

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecommunication

- 5.5.6 Manufacturing

- 5.5.7 Energy and Utilities

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Amazon Web Services Inc.

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Cognizant Technology Solutions Corporation

- 6.4.5 DXC Technology Company

- 6.4.6 Evolve IP LLC

- 6.4.7 Google LLC

- 6.4.8 International Business Machines Corporation (IBM)

- 6.4.9 Microsoft Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 Rackspace Technology Inc.

- 6.4.12 Flexera Software LLC (RightScale)

- 6.4.13 Tech Mahindra Limited

- 6.4.14 VMware Inc.

- 6.4.15 WSM International LLC

- 6.4.16 Infosys Limited

- 6.4.17 HCL Technologies Limited

- 6.4.18 Capgemini SE

- 6.4.19 Atos SE

- 6.4.20 Fujitsu Limited

- 6.4.21 Alibaba Cloud (Alibaba Group Holding Limited)

- 6.4.22 Kyndryl Holdings Inc.

- 6.4.23 Tata Consultancy Services Limited

- 6.4.24 NTT Data Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

云端迁移服务市场分析与预测(至 2034 年):类型、产品、服务、技术、元件、应用程式、部署、最终用户、解决方案和模式

云端迁移服务市场分析与预测(至 2034 年):类型、产品、服务、技术、元件、应用程式、部署、最终用户、解决方案和模式 云端迁移服务市场规模、份额、趋势和预测(按服务类型、企业规模、部署模式、应用程式、行业垂直和地区),2025 年至 2033 年

云端迁移服务市场规模、份额、趋势和预测(按服务类型、企业规模、部署模式、应用程式、行业垂直和地区),2025 年至 2033 年 云端迁移服务市场:按服务类型、迁移类型、部署模式、垂直产业、公司规模和服务供应商- 全球预测,2025-2032持续智慧市场:按组件、部署、用途、最终用户功能、垂直行业和组织规模划分 - 全球预测 2025-2032

云端迁移服务市场:按服务类型、迁移类型、部署模式、垂直产业、公司规模和服务供应商- 全球预测,2025-2032持续智慧市场:按组件、部署、用途、最终用户功能、垂直行业和组织规模划分 - 全球预测 2025-2032 2025年全球云端迁移服务市场报告

2025年全球云端迁移服务市场报告 2025-2029 年全球云端迁移服务市场

2025-2029 年全球云端迁移服务市场 云端迁移服务市场规模、份额、成长分析(按平台类型、按部署、按公司规模、按最终用户、按地区)- 产业预测 2025-2032

云端迁移服务市场规模、份额、成长分析(按平台类型、按部署、按公司规模、按最终用户、按地区)- 产业预测 2025-2032 文件迁移软体市场-按产品类型、应用、地区、预测的全球市场规模2026 年至 2032 年按部署类型、垂直产业和地区分類的云端迁移市场

文件迁移软体市场-按产品类型、应用、地区、预测的全球市场规模2026 年至 2032 年按部署类型、垂直产业和地区分類的云端迁移市场 全球云端迁移服务市场按组件、部署、公司规模、最终用途产业和地区划分

全球云端迁移服务市场按组件、部署、公司规模、最终用途产业和地区划分