|

市场调查报告书

商品编码

1851462

弹性体:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Elastomers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

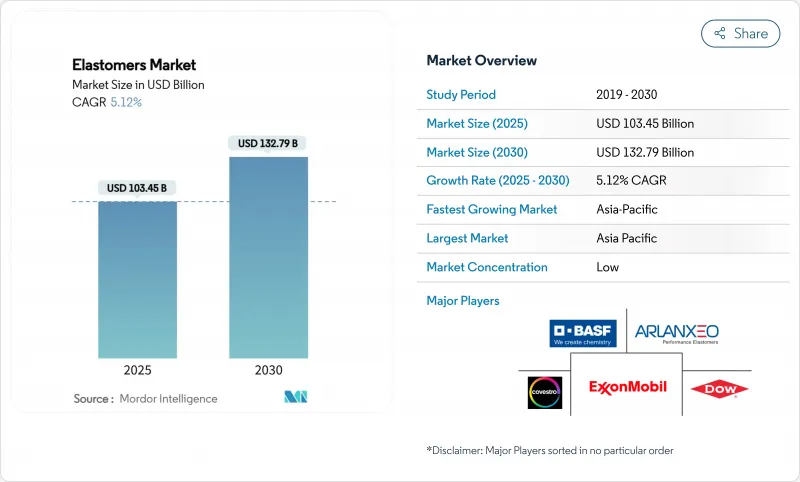

预计到 2025 年,弹性体市场规模将达到 1,034.5 亿美元,到 2030 年将达到 1,327.9 亿美元,在预测期(2025-2030 年)内,复合年增长率为 5.12%。

弹性体市场的成长轨迹与其能够实现更轻量化的汽车平台、延长电动车续航里程以及在不牺牲耐用性的前提下满足循环经济的需求密切相关。热塑性弹性体(TPE)正在取代传统橡胶,因为它们可以在标准塑胶设备上进行熔融加工,从而缩短生产週期并实现闭环再生料闭合迴路,降低废料率。亚太地区的快速都市化和对节能建筑的需求推动了建筑需求的持续成长。同时,医疗设备製造商正加速从PVC管材转向能够承受消毒的生物相容性TPE。

全球弹性体市场趋势与洞察

汽车减重和对电动车零件日益增长的需求

电动车製造商正利用先进的弹性体材料来减轻电池外壳、悬吊防尘罩和流体管路的重量,从而直接提升车辆续航里程。例如,Hytrel TPC LCF 等材料与传统聚合物相比,可减少 50% 的碳排放,并在低温衝击下保持柔韧性。商用车车主也对其重型电池组提出了同样的需求,推动了高温垫片和减振器等产品的多年研发项目。即使在全球轻型汽车销售低迷的年份,原始设备製造商 (OEM) 仍将研发预算转向轻量化密封解决方案,推动了弹性体市场的反週期成长。 Cooper Standard 的 Fortrex 平台凸显了这一趋势,与 EPDM 相比,其重量减轻了 53%,同时延长了使用寿命。充电站製造商也推动了对弹性体包覆成型部件的需求,因为这些部件必须能够承受快速充电过程中的热循环。

亚太地区的建筑和基础设施扩建

在中国、印度和东南亚的高层计划和大型交通走廊中,弹性体密封胶的使用确保了机芯、结构玻璃系统和防水膜即使在地震荷载作用下也能保持建筑围护结构的完整性。政府的绿建筑标准鼓励使用低挥发性有机化合物(VOC)和节能材料,使得高性能热塑性弹性体(TPE)和聚氨酯(PU)密封胶成为预设规格。科思创近期在台湾扩大了其浇注聚氨酯弹性体的产能,主要面向自动化工厂和风力发电机零件,从而增强了该地区的自给自足能力。智慧城市投资推动了对感测器外壳和空气品质监测器的需求成长,这些产品需要紫外线稳定的弹性体外壳。承包商倾向于选择本地配製的等级,以避免运输延误,这为全球供应商提供了与弹性体市场终端客户接轨的机会。

原油和原料价格波动

为了维持利润率,BASF等製造商对主要二醇类原料加收了每磅8-10美分的额外费用。供应紧张迫使加工商谨慎平衡库存,儘管一些加工商正在转向生物基原料,但供应量仍然有限。这种波动扰乱了预算,并可能导致资本支出推迟,从而抑制了弹性体市场的近期成长。

细分市场分析

热可塑性橡胶不仅占据了弹性体市场81.56%的份额,而且由于其闭合迴路再加工特性,有助于原始设备製造商(OEM)实现其回收目标,因此预计到2030年,其复合年增长率将达到5.35%,成为增长最快的弹性体材料。这种主导地位意味着,关键的汽车车窗密封件、线束护套和穿戴式装置正越来越多地使用热塑性弹性体(TPE)代替交联橡胶,以缩短成型週期。

热固性弹性体在温度超过 150°C 的应用领域已占据一席之地,例如涡轮增压器软管和油田封隔器。然而,即使在这些小众领域,将 TPE 外层与硫化芯材混合的混合型弹性体也能兼具耐化学性和可回收性。因此,研究投资主要集中在成核剂、嵌段共聚物设计和催化剂系统上,旨在将 TPE 的使用温度提高到 180°C 以上,同时又不影响其疲劳寿命。这些进展有望为弹性体市场带来额外收入,并帮助加工商履行回收义务。

此弹性体市场报告按产品类型(热可塑性橡胶和热固性弹性体)、终端用户行业(汽车及交通运输、电气及电子、医疗保健、工业机械及设备、其他)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲)进行细分。市场预测以美元计价。

区域分析

亚太地区以42.34%的市占率主导弹性体市场,年复合成长率达6.56%。中国仍然是关键参与者,为长三角Delta的高速铁路垫片、家用电器密封件和轮胎工厂供应弹性体。印度的国有工业工业也在推动对用于大型设备的减震支架的需求,而东南亚的电子产业丛集则在消耗用于智慧型手机和平板电脑的耐热包覆成型化合物。

北美透过轻型车辆、医疗设备和页岩气基础设施的整合供应链,为弹性体市场提供支援。针对国内电动车电池工厂的政策奖励,正在促进阻燃型TPE密封垫片的采购,这些垫片用于密封电池机壳。欧洲对永续性的重视,推动了经ISCC PLUS物料平衡系统检验的生物基EPDM和TPE混合物的应用。

南美洲、中东和非洲的基础设施投资正在稳步成长。巴西是世界第四大聚氨酯生产国,而墨西哥湾沿岸的能源计划需要耐酸性气体的弹性密封。儘管这些地区的绝对规模较小,但随着供应链日益本地化,它们具有长期的成长潜力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对更轻型汽车零件和电动车的需求不断增长

- 亚太地区的建筑和基础设施扩建

- 热可塑性橡胶(TPE)在柔性家用电器领域正迅速普及。

- 医用非PVC管材应用快速成长

- 循环利用、可回收热塑性塑胶(TPE)等级的出现

- 积层製造对弹性体长丝的需求

- 市场限制

- 原油和原料价格波动

- 加强对微塑胶和轮胎磨损的监管

- 高温下性能差异化的生物基弹性体

- 专门食品单体供应链集中度

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 热可塑性橡胶

- 热固性弹性体

- 按最终用户行业划分

- 汽车与运输

- 电气和电子

- 医疗保健

- 工业机械

- 消费品和鞋类

- 黏合剂、密封剂和被覆剂

- 其他(建筑和施工、航太和国防等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Ace Elastomer Co., Ltd.

- Arkema

- ARLANXEO

- Avient Corporation

- BASF

- Covestro AG

- DingZing Advanced Materials Co., Ltd.

- Dow

- Exxon Mobil Corporation

- Firestone Building Products Company

- HEXPOL AB

- Huntsman Corporation

- KRAIBURG TPE GmbH

- Kuraray Co., Ltd.

- Lion Elastomers Co., Ltd

- Mitsui Chemicals, Inc.

- Sirmax SpA

- Suzhou Austin Novel Materials Co., Ltd.

- Teknor Apex, Inc.

- Trinseo LLC

- UBE Corporation

- Wanhua Chemical Group Co., Ltd.

第七章 市场机会与未来展望

The Elastomers Market size is estimated at USD 103.45 billion in 2025, and is expected to reach USD 132.79 billion by 2030, at a CAGR of 5.12% during the forecast period (2025-2030).

The upward trajectory of the Elastomers market is tied to the material's ability to deliver weight reduction in automotive platforms, extend electric-vehicle range, and meet circular-economy expectations without sacrificing durability. Thermoplastic grades are displacing conventional rubbers because they melt-process on standard plastics equipment, cut cycle times, and enable closed-loop re-grind streams that lower scrap rates. Rapid urbanization in Asia Pacific and the push for energy-efficient buildings keep construction demand elevated, while medical device makers accelerate the shift away from PVC tubing toward biocompatible TPEs that survive sterilization.

Global Elastomers Market Trends and Insights

Growing Demand for Lightweighting and EV Parts in Automotive

Electric-vehicle makers rely on advanced elastomers to shave kilograms from battery housings, suspension boots, and fluid-handling lines, which directly boosts driving range. Materials such as Hytrel TPC LCF cut carbon footprints by 50% compared with incumbent polymers, yet keep flexibility under low-temperature shock. Commercial fleet owners echo the same need in heavy-duty packs, fueling multi-year programs for high-temperature gaskets and vibration isolators. Even in a year when global light-vehicle sales slipped, OEMs funneled research and development budgets toward lightweight sealing solutions, creating a counter-cyclical lift for the Elastomers market. Cooper Standard's Fortrex platform highlights the trend with a 53% mass reduction versus EPDM while extending service life. Charging-station manufacturers add to demand because elastomeric over-mold parts must tolerate thermal cycling during fast charging.

Expansion of Construction and Infrastructure in Asia-Pacific

High-rise projects and mega-transport corridors across China, India, and Southeast Asia use elastomeric sealants to enable movement joints, glazing systems, and waterproof membranes that maintain building envelope integrity under seismic loads. Government green-building codes reward the use of low-VOC, energy-saving materials, turning high-performance TPE and PU sealants into default specifications. Covestro's recent capacity ramp-up in Taiwan for cast polyurethane elastomers is aimed at equipment used in automated factories and wind-turbine components, reinforcing regional self-sufficiency. Smart-city investments generate incremental pulls from sensor housings and air-quality monitors that require UV-stable elastomer skins. Contractors favor locally compounded grades to avoid shipping delays, giving global suppliers a reason to co-locate with end-markets in the Elastomers market.

Volatile Crude Oil and Feedstock Prices

Producers such as BASF implemented 8-10 cents per pound surcharges on key diols to maintain margins. Tight supply obliges converters to balance inventories carefully, and some shift sourcing to bio-based feedstocks, although volumes remain limited. The volatility clouds budgeting and can postpone capital expenditure, dampening near-term expansion of the Elastomers market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Penetration of Thermoplastic Elastomers in Flexible Consumer Electronics

- Surge in Medical-Grade PVC-Free Tubing Applications

- Stricter Micro-Plastic and Tire-Wear Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoplastic elastomers not only own 81.56% share of the Elastomers market but also log the fastest 5.35% CAGR to 2030, thanks to closed-loop reprocessability that helps OEMs hit recycling targets. This dominance means every major automotive window seal, wire harness grommet, and wearable band increasingly relies on TPE, often replacing cross-linked rubber to shorten molding cycles.

Thermoset elastomers maintain footholds where temperatures exceed 150 °C, for instance, in turbocharger hoses and oil-field packers. Yet even in these niches, hybrid concepts mix TPE outer layers with vulcanized cores to marry chemical resistance with recyclability. Research investment, therefore, centers on nucleating agents, block-copolymer design, and catalyst systems that lift the service temperature of TPE beyond 180 °C without eroding fatigue life. Such advances are expected to channel additional revenue into the Elastomers market while helping processors meet take-back mandates.

The Elastomers Report is Segmented by Product Type (Thermoplastic Elastomers and Thermoset Elastomers), End-User Industry (Automotive and Transportation, Electrical and Electronics, Medical and Healthcare, Industrial Machinery and Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captures 42.34% of the Elastomers market and outpaces all other regions with a 6.56% CAGR. China remains the centerpiece, channeling elastomers into high-speed rail gaskets, appliance seals, and tire plants clustered along the Yangtze River Delta. India's state-sponsored industrial corridors likewise lift demand for vibration-dampening mounts used in capital equipment, while Southeast Asia's electronics clusters consume heat-resistant over-mold compounds for smartphones and tablets.

North America sustains the Elastomers market through its integrated supply chain for light vehicles, medical devices, and shale-gas infrastructure. Policy incentives for domestic EV battery plants intensify the procurement of flame-retardant TPE gaskets that seal cell enclosures. Europe pivots heavily toward sustainability, driving the adoption of bio-attributed EPDM and TPE blends verified under ISCC PLUS mass-balance systems.

South America, the Middle-East, and Africa post steady gains in infrastructure spending. Brazil's polyurethane output ranks fourth globally, while Gulf energy projects need sour-gas-resistant elastomer seals. Although smaller in absolute terms, these regions provide long-run upside as supply-chain localization continues.

- Ace Elastomer Co., Ltd.

- Arkema

- ARLANXEO

- Avient Corporation

- BASF

- Covestro AG

- DingZing Advanced Materials Co., Ltd.

- Dow

- Exxon Mobil Corporation

- Firestone Building Products Company

- HEXPOL AB

- Huntsman Corporation

- KRAIBURG TPE GmbH

- Kuraray Co., Ltd.

- Lion Elastomers Co., Ltd

- Mitsui Chemicals, Inc.

- Sirmax S.p.A

- Suzhou Austin Novel Materials Co., Ltd.

- Teknor Apex, Inc.

- Trinseo LLC

- UBE Corporation

- Wanhua Chemical Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for lightweighting and EV parts in automotive

- 4.2.2 Expansion of construction and infrastructure in Asia Pacific

- 4.2.3 Rapid penetration of Thermoplastic Elastomers (TPEs) in flexible consumer electronics

- 4.2.4 Surge in medical?grade PVC-free tubing applications

- 4.2.5 Emergence of recycling-compatible circular Thermoplastic Elastomers (TPE )grades

- 4.2.6 Additive manufacturing demand for elastomeric filaments

- 4.3 Market Restraints

- 4.3.1 Volatile crude oil and feedstock prices

- 4.3.2 Stricter micro-plastic and tire-wear regulations

- 4.3.3 Performance gap of bio-based elastomers at high-temperature

- 4.3.4 Supply-chain concentration of specialty monomers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Thermoplastic Elastomers

- 5.1.2 Thermoset Elastomers

- 5.2 By End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Electrical and Electronics

- 5.2.3 Medical and Healthcare

- 5.2.4 Industrial Machinery and Equipment

- 5.2.5 Consumer Goods and Footwear

- 5.2.6 Adhesives, Sealants and Coatings

- 5.2.7 Others (Building and Construction, Aerospace and Defense, etc)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ace Elastomer Co., Ltd.

- 6.4.2 Arkema

- 6.4.3 ARLANXEO

- 6.4.4 Avient Corporation

- 6.4.5 BASF

- 6.4.6 Covestro AG

- 6.4.7 DingZing Advanced Materials Co., Ltd.

- 6.4.8 Dow

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 Firestone Building Products Company

- 6.4.11 HEXPOL AB

- 6.4.12 Huntsman Corporation

- 6.4.13 KRAIBURG TPE GmbH

- 6.4.14 Kuraray Co., Ltd.

- 6.4.15 Lion Elastomers Co., Ltd

- 6.4.16 Mitsui Chemicals, Inc.

- 6.4.17 Sirmax S.p.A

- 6.4.18 Suzhou Austin Novel Materials Co., Ltd.

- 6.4.19 Teknor Apex, Inc.

- 6.4.20 Trinseo LLC

- 6.4.21 UBE Corporation

- 6.4.22 Wanhua Chemical Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Shifting Focus toward the Development of Bio-based Products

高温弹性体市场:2026-2032年全球市场预测(依弹性体类型、产品形式、加工技术、应用与最终用途产业划分)

高温弹性体市场:2026-2032年全球市场预测(依弹性体类型、产品形式、加工技术、应用与最终用途产业划分) 全球聚烯弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)

全球聚烯弹性体市场规模、份额、趋势和成长分析报告(2026-2034年) 弹性体市场分析及预测(至2035年):类型、产品、应用、技术、最终用户、形态、材料类型、组件、製程、安装类型2026-2034年全球阀门软座弹性体市场规模、份额、趋势和成长分析报告全球丁基弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)全球耐热弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)超弹性材料全球市场规模、份额、趋势和成长分析报告(2026-2034)

弹性体市场分析及预测(至2035年):类型、产品、应用、技术、最终用户、形态、材料类型、组件、製程、安装类型2026-2034年全球阀门软座弹性体市场规模、份额、趋势和成长分析报告全球丁基弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)全球耐热弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)超弹性材料全球市场规模、份额、趋势和成长分析报告(2026-2034) 弹性体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、热塑性塑胶、应用、地区和竞争格局划分,2021-2031年)工业热塑性聚氨酯弹性体市场按产品类型、硬度、加工製程、形状、应用和最终用途产业划分-2026-2032年全球预测

弹性体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、热塑性塑胶、应用、地区和竞争格局划分,2021-2031年)工业热塑性聚氨酯弹性体市场按产品类型、硬度、加工製程、形状、应用和最终用途产业划分-2026-2032年全球预测 高性能弹性体市场预测至2032年:按类型、加工方法、应用、最终用户和地区分類的全球分析

高性能弹性体市场预测至2032年:按类型、加工方法、应用、最终用户和地区分類的全球分析