|

市场调查报告书

商品编码

1851463

工业涂料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Industrial Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

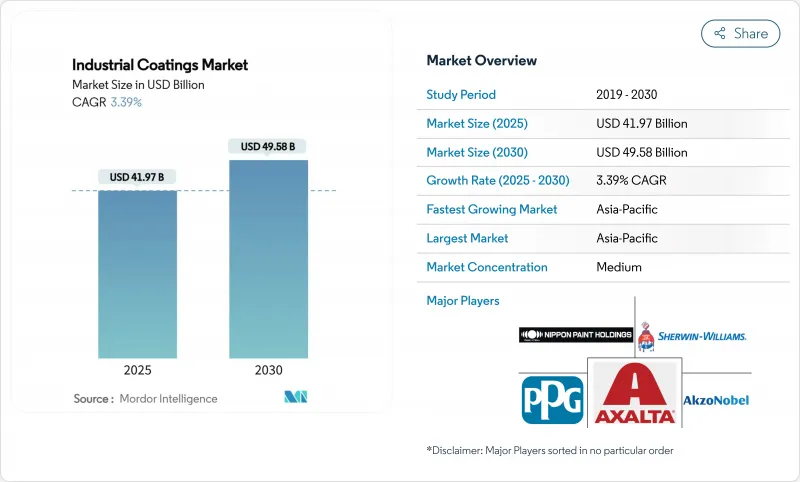

预计到 2025 年,工业涂料市场规模将达到 419.7 亿美元,到 2030 年将达到 495.8 亿美元,预测期(2025-2030 年)复合年增长率为 3.39%。

这项市场成长动能主要得益于奈米技术的加速应用,奈米技术在提升涂料性能的同时还能减少材料用量;此外,永续的水性涂料和粉末涂料技术也迅速取代溶剂型产品。亚太地区将在2024年占据51%的市场份额,这主要得益于中国和印度的大规模基础设施投资以及製造业的成长。环氧树脂因其优异的耐化学性和黏合性,已成为能源、基础设施和重工业等高性能应用领域不可或缺的材料,预计将以6%的复合年增长率成长,占据31%的市场份额。在全球范围内,日益严格的挥发性有机化合物(VOC)法规正促使製造商加速研发低VOC和零VOC化学品。同时,随着主要供应商收购专业公司以扩大其区域覆盖范围和技术实力,产业整合也在加速进行。

全球工业涂料市场趋势与洞察

防护涂层需求不断成长:防蚀驱动创新

随着资产所有者将耐久性和生命週期成本管理置于优先地位,防护涂层变得至关重要。例如,NEI 公司的 NANOMYTE TC-3001 等产品可在极少维护的情况下提供长达 15 年的耐腐蚀性,使营运商能够推迟资本密集的更换。下游炼油厂、化工厂和海上平台越来越多地指定使用多层环氧树脂和富锌体系,这些体系既能提供屏障保护,又能提供阴极保护。将感测器整合到这些涂层中,正在将维护策略从被动检测转向预测分析,从而在确保安全的同时减少非计划性停机时间。同时,各国政府正在强制要求公共基础设施拥有更长的使用寿命,这推动了对能够抵御沿海盐度、除冰盐和工业污染物的下一代解决方案的需求。这些动态共同强化了市场动态,促使研究重点转向在不增加膜厚或固化时间的情况下延长涂层寿命。

在石油和天然气产业不断拓展的应用:针对严苛条件量身订做的解决方案

深水和高温油井的限制限制了传统涂料的应用,促使人们致力于研发混合化学涂料,将环氧酚醛树脂与陶瓷和硅酮组分相结合,以增强其对碳氢化合物和超过150 度C高温的耐受性。 PPG的专有系统可在单一整合方案中保护海底管线免受酸性气体的侵蚀,同时为上部结构提供膨胀型防火保护。涂料设计也在不断发展,以承受大规模二氧化碳捕集与储存(CCS)计划中预期的高压二氧化碳流。中东地区的本地供应商正在获得这些先进技术的许可,以满足该地区快速成长的钻井专案需求,但严格的认证通讯协定意味着产品推广週期较长。随着产业投资于数位孪生技术以保护资产,具有嵌入式远端状态监测功能的涂料在油气产业的工业涂料市场中变得越来越普遍,并具有重要的战略意义。

溶剂型涂料对环境的有害影响:监管压力加速转型

在美国和欧洲经济区,针对挥发性有机化合物 (VOC) 的新法规已经出台,收紧了工业涂装车间的排放,迫使操作人员安装减排设备或改用低溶剂替代品。因此,水性涂料和粉末涂料的市场需求日益增长,即使是小面积涂料也是如此。供应商维修现有分散生产线而非新建溶剂型设施,这表明他们对生命週期成本进行了审慎的考量,并相信环境合规支出将显着转向替代化学品。随着参与企业凭藉永续性资质赢得多年供应合同,这进一步强化了反馈机制,使得符合监管要求成为市场准入的先决条件,而非竞争优势。

细分市场分析

预计到2024年,环氧涂料将占工业涂料市场31%的份额,而聚氨酯涂料的复合年增长率将达到5.02%,显着高于整个行业的平均水平。聚氨酯涂料的领先地位归功于其卓越的附着力、耐化学性和与多种基材的相容性,使其在炼油厂、污水厂和加工厂等场所得到广泛应用。奈米二氧化硅改质环氧树脂正在兴起,它不仅具有优异的耐磨性,还能维持低VOC含量,满足了监管机构对更环保解决方案的需求。相较之下,聚氨酯树脂的市场份额正在逐步扩大,尤其是在对紫外线稳定性和柔韧性要求较高的室外应用领域,例如风力发电机塔架和铁路车辆。丙烯酸乳化。

环氧树脂供应商正增加研发投入,以缩短重涂週期,并满足日益加快的计划进度。耐湿无溶剂酚醛环氧树脂在海上平台上的应用日益广泛,有效减少了因天气原因造成的延误。同时,埃洛石奈米管增强技术在不改变配方黏度的前提下,显着提升了涂料的耐盐雾性能,吸引了致力于实现30年使用寿命目标的管道业主。总而言之,这些技术进步巩固了工业涂料市场对环氧树脂化学在关键服务运作中的依赖,同时也为聚氨酯和丙烯酸工业创新者在更具挑战性的环境中提供了新的商机。

在工业涂料市场,溶剂型涂料预计到2024年将保持37%的市场份额,而水性涂料由于其在不同气候带的优异性能,将实现4.89%的复合年增长率。然而,随着承包商逐渐适应更低的溶剂含量、更少的异味以及更安全的使用要求,水性涂料目前在维护性重涂领域占据了更大的份额。预计到2030年,随着欧洲和北美更严格的VOC法规过渡期的结束,水性涂料在重型设备工业涂料市场的份额将进一步增长。无溶剂粉末涂料持续快速成长,广泛应用于农业机械和家用电器的外表面。宣伟公司的Powdura ECO系列产品在不牺牲耐腐蚀性的前提下,融入了再生聚对苯二甲酸乙二醇酯(rPET),展现了永续创新,与品牌所有者对循环经济的承诺相契合。

紫外光固化涂料可即时施工,并可减少高达95%的烘箱能耗,因此在地板、电子机壳和金属包装等领域越来越受欢迎。然而,视线限制和基板温度敏感度限制了其在复杂几何形状中的应用。在更广泛的工业涂料市场中,资产所有者优先考虑的是总应用成本、性能和法规合规性,这促使许多企业采用混合方法,将水性底漆与溶剂型或聚氨酯面漆混合,以实现性能平衡。在预测期内,配方师可望改善无胺促进剂和快干醇酸乳液,从而进一步推动水性涂料在工业涂料市场的成长。

区域分析

预计到2024年,亚太地区将占据工业涂料市场51%的份额,并在2030年之前以4.31%的复合年增长率成长。中国正大力投资石化综合体和电动车製造,而印度的国家基础建设也推动了公路、机场和铁路涂料的需求。跨国供应商正在推进本地化生产,以规避关税并缩短前置作业时间,越南和泰国最近成立的合资企业便是例证,该合资企业将树脂聚合和麵漆调配集中在同一厂房内进行。

在北美,销售量成长放缓,但随着资产所有者转向高端、高固含量技术,销售额却显着提升。 PPG以5.5亿美元的价格出售了美国和加拿大的建筑涂料业务,使经营团队能够将资金重新部署到其工业涂料产品组合中,包括采用机器人技术的粉末生产线。加拿大的脱碳蓝图也鼓励使用低挥发性有机化合物(VOC)和可再生电力进行生产。

在严格的挥发性有机化合物(VOC)法规和雄心勃勃的气候中和目标的推动下,欧洲仍然是技术领域的领导者。BASF决定将其位于德国和荷兰的主要涂料工厂全部采用再生能源,每年可减少11,000吨二氧化碳排放,从而增强其对寻求减少范围3排放的原始设备製造商(OEM)的价值提案。该地区也正在见证以非食用油料作物为原料的生物基醇酸树脂的早期商业化,儘管工业客户要求在广泛应用之前进行严格的耐久性检验。

儘管中东和非洲的市场份额较小,但其成长速度却最高,这主要得益于沙乌地阿拉伯NEOM等大型企划对先进金属和混凝土防护系统的需求。当地配方商正与跨国技术合作伙伴携手,以满足高盐度、高紫外线沙漠环境中严苛的防火防腐蚀要求。以巴西为首的南美洲正受益于石化投资和持续的都市化,儘管宏观经济的不确定性限制了公共部门的资本支出。在全部区域,知识转移计画和本地培训计画正在提升施工人员的技能水平,而这正是充分发挥现代工业涂料性能潜力的关键因素。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对防护涂料的需求不断增长

- 在石油和天然气产业中不断扩展的应用

- 基础设施建设和都市化

- 电力和海事领域的需求不断增长

- 人们对美感价值重要性的认识日益增强

- 市场限制

- 溶剂型涂料对环境的有害影响

- 原物料价格波动

- 替代涂料产品的供应情况

- 价值链分析

- 监理展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依树脂类型

- 环氧树脂

- 聚氨酯

- 丙烯酸纤维

- 聚酯纤维

- 其他树脂(醇酸树脂、氟树脂、乙烯基酯树脂)

- 透过技术

- 溶剂型

- 水溶液

- 粉末

- 紫外线技术

- 按最终用途行业划分

- 一般工业

- 保护涂层

- 石油和天然气

- 矿业

- 电力

- 基础设施

- 其他保护涂层

- 按基础材料

- 金属

- 具体的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 澳洲

- 纽西兰

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- 3M

- AkzoNobel NV

- Arkema

- Asian Paints

- Axalta Coating Systems

- BASF SE

- Beckers Group

- Chugoku Marine Paints Ltd.

- Daikin Industries Ltd.

- Hempel A/S

- Henkel AG & Co. KGaA

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- OC Oerlikon Management AG

- PPG Industries, Inc.

- RPM International Inc.

- Rust-Oleum Corporation

- Sika AG

- The Sherwin-Williams Company

- Tikkurila

- Wacker Chemie AG

第七章 市场机会与未来展望

The Industrial Coatings Market size is estimated at USD 41.97 billion in 2025, and is expected to reach USD 49.58 billion by 2030, at a CAGR of 3.39% during the forecast period (2025-2030).

The market's momentum is shaped by the accelerating adoption of nanotechnology, which improves coating performance while reducing material usage, and by a rapid substitution of solvent-borne products with sustainable water-borne and powder technologies. Asia-Pacific leads with a 51% share in 2024, powered by extensive infrastructure investments and manufacturing growth in China and India. Epoxy resins dominate with a 31% share, advancing at a 6% CAGR on account of their superior chemical resistance and adhesion properties, making them indispensable in high-performance applications across energy, infrastructure, and heavy industry. Regulatory mandates on volatile organic compounds (VOCs) are tightening globally, prompting manufacturers to accelerate innovation in low- and zero-VOC chemistries and thereby creating fresh opportunities for producers equipped with green technologies. Meanwhile, consolidation is accelerating as leading suppliers acquire specialized firms to bolster regional reach and technology depth, even as more than 20 sizable competitors maintain a fragmented landscape.

Global Industrial Coatings Market Trends and Insights

Rising Demand for Protective Coatings: Corrosion Mitigation Drives Innovation

Protective coatings have become pivotal as asset owners prioritize durability and lifecycle cost control. Products such as NEI Corporation's NANOMYTE TC-3001 offer up to 15 years of corrosion resistance with minimal maintenance, enabling operators to defer capital-intensive replacements. Downstream oil refineries, chemical plants, and offshore platforms increasingly specify multi-layer epoxy and zinc-rich systems that deliver both barrier and cathodic protection. The integration of embedded sensors within these coatings is shifting maintenance strategies from reactive inspections to predictive analytics, cutting unexpected downtime while preserving safety. Concurrently, governments are mandating longer service lives for public infrastructure, a requirement that boosts demand for next-generation solutions able to withstand coastal salinity, de-icing salts, and industrial pollutants. Collectively, these dynamics reinforce the industrial coatings market's focus on research that extends coating lifespan without increasing film thickness or curing time.

Increasing Applications in Oil and Gas Industry: Specialized Solutions for Extreme Conditions

Deep-water and high-temperature wells challenge conventional coatings, driving innovation toward hybrid chemistries that combine epoxy phenolics with ceramic or silicone components for enhanced resistance to hydrocarbons and temperatures exceeding 150 °C. PPG's purpose-built systems guard subsea pipelines from sour gas, while offering intumescent fire protection on topside structures in one integrated scheme. Coating designs are also evolving to tolerate high-pressure carbon dioxide streams expected in large-scale carbon capture and storage (CCS) projects. Localized suppliers in the Middle East are licensing these advanced technologies to meet rapidly expanding regional drilling programs, although stringent qualification protocols lengthen product adoption cycles. As the industry invests in digital twins for asset integrity, coatings compatible with remote condition-monitoring embedment stand to gain further traction, reinforcing the oil and gas sector's strategic importance to the industrial coatings market.

Harmful Environmental Impact of Solvent-borne Coating: Regulatory Pressure Accelerates Transition

Fresh limits on volatile organic compounds (VOC) in the United States and the European Economic Area have tightened allowable emissions for industrial paint shops, forcing operators to install abatement equipment or switch to low-solvent alternatives. Water-borne and powder varieties are therefore capturing incremental Industrial Coatings market size even when total painted surface area expands only modestly. Suppliers that retrofit existing dispersion lines instead of constructing new solvent facilities illustrate a calculated response to lifetime cost, signaling confidence that environmental compliance spending will tilt decisively toward alternative chemistries. As early movers win multi-year supply contracts on sustainability credentials, they reinforce a feedback loop that makes regulatory alignment a prerequisite for market entry rather than a competitive bonus.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Development & Urbanization: Driving Demand for Durable Solutions

- Sustainability-Driven Shift Toward Low-VOC Technologies: Regulatory Pressure Accelerates Transition

- Fluctuating Raw Material Prices: Supply Chain Vulnerabilities Impact Market Dynamics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy coatings represented 31% of the industrial coatings market in 2024, while polyurethane is projected to grow at a 5.02% CAGR, firmly outpacing the overall industry. Their leadership stems from exceptional adhesion, chemical resistance, and compatibility with a broad spectrum of substrates, enabling widespread adoption in refineries, wastewater plants, and fabrication workshops. Hybrid nano-silica-modified epoxies are emerging, delivering superior abrasion resistance while maintaining low VOC levels, which satisfies regulatory calls for greener solutions. In contrast, polyurethane resins are gradually taking share in exterior segments where UV stability and flexibility are critical, particularly in wind-turbine towers and railcars. Acrylics retain an important niche in light-duty equipment due to fast dry-to-touch times and low cost, and recent capital investments such as Lubrizol's USD 20 million expansion in North Carolina signal continued growth potential in water-borne acrylic emulsions.

Epoxy suppliers intensify R&D to shorten recoat windows and meet rapid project schedules, a top procurement criterion for contractors seeking to finish multiple passes in a single shift. Solvent-free novolac epoxies that tolerate moisture during cure are gaining momentum on offshore platforms, reducing weather-related delays. Meanwhile, halloysite-nanotube enhancements deliver double-digit improvements in salt-spray performance without altering formulation viscosity, attracting pipeline owners committed to 30-year service targets. Collectively, these advances strengthen the industrial coatings market's reliance on epoxy chemistries for critical-service duties, while opening incremental opportunities for polyurethane and acrylic innovators in less aggressive environments within the industrial coatings industry.

Solvent-borne coatings retained a 37% share of the industrial coatings market in 2024, while water-borne posting a resilient 4.89% CAGR thanks to their proven performance across diverse climatic zones. However, water-borne products now capture a growing share of maintenance repaints as contractors adapt to lower solvent levels, odor reduction, and safer handling requirements. The industrial coatings market share for water-borne technologies on heavy machinery is expected to rise by 2030 as phase-in periods for tightened VOC limits expire in Europe and North America. Powder coatings, free of solvents, remain the fastest-growing platform, adding capacity for agricultural equipment and appliance exteriors. Sherwin-Williams' Powdura ECO line integrates recycled polyethylene terephthalate (rPET) without sacrificing corrosion resistance, illustrating sustainable innovation that resonates with brand owners' circular-economy commitments.

UV-curable coatings, which provide instant throughput and slash oven-energy use by up to 95%, are penetrating wood flooring, electronics housings, and metal packaging segments. Nevertheless, their line-of-sight limitation and substrate temperature sensitivity restrain adoption in complex geometries. In the broader industrial coatings market, asset owners weigh total applied cost, performance, and regulatory compliance, leading many to adopt hybrid schemes that blend water-borne primers with solvent-borne or polyurethane topcoats for balanced properties. Over the forecast horizon, formulators are expected to refine amine-free accelerators and fast-dry alkyd emulsions to unlock further water-borne growth within the industrial coatings market.

The Industrial Coatings Market Report Segments the Industry by Resin Type (Epoxy, Polyurethane, and More), Technology (Solvent-Borne, Water-Borne, and More), End-Use Industry (General Industrial, and Protective Coatings), Substrate (Metal and Concrete), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific secured a 51% share of the industrial coatings market in 2024 and is poised to grow at a 4.31% CAGR through 2030. China commands heavy investment in petrochemical complexes and electric-vehicle manufacturing, while India's National Infrastructure Pipeline underwrites coatings demand for highways, airports, and railways. Multinational suppliers localize production to avoid tariffs and reduce lead times, evidenced by recent joint ventures in Vietnam and Thailand that integrate resin polymerization and finished-paint blending under one roof.

North America exhibits modest volume growth but strong value expansion as asset owners shift to premium, high-solids technologies. PPG's divestment of its U.S. and Canadian architectural coatings unit for USD 550 million allows management to redeploy capital toward its industrial coatings portfolio, including robotics-enabled powder lines. Infrastructure law outlays accelerate demand for bridge and pipeline coatings across the United States, while Canada's decarbonization roadmap incentivizes the adoption of low-VOC, renewable-electricity-based production.

Europe remains a technology leader, driven by strict VOC limits and ambitious climate-neutrality targets. BASF's decision to power key German and Dutch coating plants entirely with renewable electricity eliminates 11,000 tons of CO2 annually and strengthens its value-proposition for OEMs pursuing Scope 3 emission reductions. The region is also seeing early commercialization of bio-based alkyds sourced from non-food oil crops, though industrial customers demand rigorous durability validation before widespread adoption.

The Middle East & Africa, while owning a smaller share, records some of the highest growth rates as mega-projects such as Saudi Arabia's NEOM drive demand for advanced metal and concrete protective systems. Local formulators align with multinational technology partners to meet stringent fire- and corrosion-protection specifications required for high-salinity, high-UV desert environments. South America, led by Brazil, benefits from petrochemical investments and continued urbanization, though macroeconomic uncertainty tempers public-sector capital spending. Across these developing regions, knowledge transfer initiatives and localized training programs bolster applicator proficiency, a critical factor in realizing the full performance potential of modern industrial coatings.

- 3M

- AkzoNobel N.V.

- Arkema

- Asian Paints

- Axalta Coating Systems

- BASF SE

- Beckers Group

- Chugoku Marine Paints Ltd.

- Daikin Industries Ltd.

- Hempel A/S

- Henkel AG & Co. KGaA

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- OC Oerlikon Management AG

- PPG Industries, Inc.

- RPM International Inc.

- Rust-Oleum Corporation

- Sika AG

- The Sherwin-Williams Company

- Tikkurila

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Protective Coatings

- 4.2.2 Increasing Applications in Oil and Gas Industry

- 4.2.3 Infrastructure Development and Urbanization

- 4.2.4 Growing Demand in Power and Marine Sectors

- 4.2.5 Rising Awareness of the Importance of Aesthetic Value

- 4.3 Market Restraints

- 4.3.1 Harmful Environmental Impact Of Solvent-borne Coating

- 4.3.2 Fluctuating Raw Material Prices

- 4.3.3 Availability of Alternative Coating Products

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Polyester

- 5.1.5 Other Resins (Alkyd, Fluoropolymer, Vinyl Ester)

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Powder

- 5.2.4 UV Technology

- 5.3 By End-use Industry

- 5.3.1 General Industrial

- 5.3.2 Protective Coatings

- 5.3.2.1 Oil and Gas

- 5.3.2.2 Mining

- 5.3.2.3 Power

- 5.3.2.4 Infrastructure

- 5.3.2.5 Other Protective Coatings

- 5.4 By Substrate

- 5.4.1 Metal

- 5.4.2 Concrete

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Australia

- 5.5.1.7 New Zealand

- 5.5.1.8 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 AkzoNobel N.V.

- 6.4.3 Arkema

- 6.4.4 Asian Paints

- 6.4.5 Axalta Coating Systems

- 6.4.6 BASF SE

- 6.4.7 Beckers Group

- 6.4.8 Chugoku Marine Paints Ltd.

- 6.4.9 Daikin Industries Ltd.

- 6.4.10 Hempel A/S

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Jotun

- 6.4.13 Kansai Paint Co., Ltd.

- 6.4.14 Nippon Paint Holdings Co., Ltd.

- 6.4.15 OC Oerlikon Management AG

- 6.4.16 PPG Industries, Inc.

- 6.4.17 RPM International Inc.

- 6.4.18 Rust-Oleum Corporation

- 6.4.19 Sika AG

- 6.4.20 The Sherwin-Williams Company

- 6.4.21 Tikkurila

- 6.4.22 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 Technological Advancements in Coating Formulations

- 7.2 White-space and Unmet-need Assessment

工业维护涂料市场按产品类型、技术、最终用户、应用和销售管道划分-2025-2032 年全球预测涂装设备市场:依设备类型、技术类型、涂料、应用类型和组件划分-2025-2032年全球预测工业被覆剂市场(按树脂类型、技术、功能、应用和分销管道)—2025-2030 年全球预测

工业维护涂料市场按产品类型、技术、最终用户、应用和销售管道划分-2025-2032 年全球预测涂装设备市场:依设备类型、技术类型、涂料、应用类型和组件划分-2025-2032年全球预测工业被覆剂市场(按树脂类型、技术、功能、应用和分销管道)—2025-2030 年全球预测 全球工业维护与涂料市场

全球工业维护与涂料市场 2025年涂装设备全球市场报告

2025年涂装设备全球市场报告 工业涂料市场分析:需求、地区、应用及2034年预测报告

工业涂料市场分析:需求、地区、应用及2034年预测报告 工业被覆剂市场:按功能、技术、树脂类型、最终用途行业和地区分類的全球市场 - 预测至 2030 年

工业被覆剂市场:按功能、技术、树脂类型、最终用途行业和地区分類的全球市场 - 预测至 2030 年 2025-2029年全球工业被覆剂市场全球风能涂料市场

2025-2029年全球工业被覆剂市场全球风能涂料市场 日本工业涂料市场报告(按产品类型、技术、最终用户和地区)2025-2033

日本工业涂料市场报告(按产品类型、技术、最终用户和地区)2025-2033