|

市场调查报告书

商品编码

1939597

欧洲聚氯乙烯(PVC):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Polyvinyl Chloride (PVC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

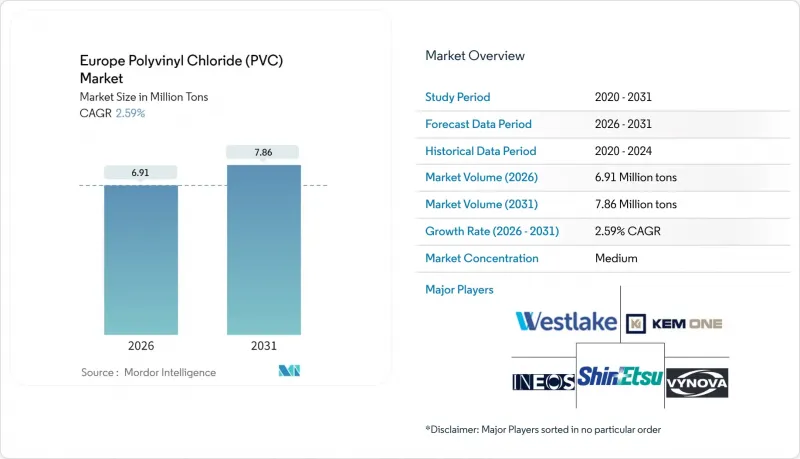

预计到 2026 年,欧洲聚氯乙烯(PVC) 市场规模将达到 691 万吨。

预计到 2025 年,这一数字将增加至 674 万吨,预计到 2031 年将达到 786 万吨,2026 年至 2031 年的年复合成长率(CAGR)为 2.59%。

对管道、型材和管件的强劲需求,以及住宅的逐步復苏,支撑了近期销售成长。 REACH法规的压力持续加速钙锌稳定剂的应用,而持续的基础设施投资则降低了转型成本。节能维修专案、电网升级和水资源管理计划支撑了结构性需求,而循环经济的必要性则加速了对再生和生物基PVC的投资。由于一体化生产商利用规模经济、自有原料和专有技术来抵销合规成本,市场竞争强度仍然适中。

欧洲聚氯乙烯(PVC)市场趋势与展望

建设产业需求不断成长

欧洲住宅短缺和建筑老化导致持续的维修需求,进而推动了对PVC窗框和墙板的需求。以热塑性嵌件加强的PVC窗框可将隔热性能提高12-13%,并更符合欧盟节能标准,进一步巩固了硬质PVC在维修计划中的应用。成员国的復苏基金优先用于土木工程支出,而蓄水排水系统则展现了PVC在农业基础设施的功能性和成本优势。利率稳定和材料价格正常化提高了北欧市场计划的可行性,而财政限制继续限制南欧的成长。整体而言,预计中期内对PVC管材和型材的需求将呈现均衡成长。

自动车产业からの需要増加

电动车的普及正在重塑汽车内装组件的规格,并扩大阻燃柔性PVC在汽车线束和地板材料的应用。预计到2025年初,德国汽车产量将年增3%,这将推动当地混炼厂树脂用量的成长。生物基PVC在整个生产过程中可减少58%的二氧化碳排放,同时维持拉伸强度和耐热性。这使得汽车製造商无需重新设计平台即可实现其环境、社会和治理(ESG)目标。以德国、法国和义大利北部为中心的成长中心促进了物流优化和准时制供应模式的实施。一级供应商正在将数位化品管工具与材料创新相结合,以减少边角料废弃物并缩短生产週期。

零售商加速禁用PVC食品包装

西欧大型超级市场正逐步淘汰PVC托盘和包装膜,迫使加工商转向使用整体式PET和纸基替代品。即将推出的包装废弃物法规将对PFAS和BPA施加更多限制,使传统PVC配方的合规性更加复杂。虽然药品泡壳包装不受此限制,但高需求生鲜食品产业的即时替代正在萎缩欧洲PVC市场对软包装的需求。品牌所有者的采购政策会向上游扩散,迫使混料商对替代树脂进行认证,并为对阻隔性要求极高的特定应用开发可回收的PVC混合物。东欧市场在实施禁令方面进展缓慢,虽然暂时缓解了这个问题,但也预示着最终将在全部区域进行过渡。

细分市场分析

2025年,硬质PVC将占欧洲PVC市场60.42%的份额,并将继续在建筑和供水管网的管道、型材和配件领域占据主导地位。低烟PVC虽然基数较小,但预计成长最为显着,到2031年复合年增长率将达到3.73%,主要得益于公共交通、隧道和公共集会场所计划对消防法规的要求。软质PVC的需求趋势呈现两极化:医用导管领域对生物增塑透明PVC的需求不断增长,预计将抵消食品包装薄膜需求的下降。氯化PVC正加速进入工业热水管道领域,当地生产设施的建立有助于降低进口关税和物流成本。

由于需求模式成熟,运转率稳定在80%左右,产能扩张仍较为温和。挤出製造商专注于透过模头升级和在线连续测量系统来产量比率,而不是投资新的资本设备。产品组合的柔软性是加工商的竞争优势,他们需要在满足化工视镜等硬质透明产品的订单和市政管道合约的大宗订单之间灵活切换。因此,欧洲PVC市场在稳定、高需求的硬质产品需求和低烟氯化聚氯乙烯(CPVC)等特种应用领域不断增长的细分市场之间保持着平衡。

到2025年,钙锌体系将占稳定剂消费量的42.55%,这清楚地显示了欧盟铅含量法规实施后市场格局的转变。预计到2031年,这些稳定剂产品将以3.47%的复合年增长率成长,成为欧洲PVC市场添加剂价值成长的主要驱动力。目前,铅基稳定剂主要在临时豁免条件下用于回收的硬质材料流中,而锡基系统则主要应用于高温丝材涂层这一小众市场。钡锌和液态混合金属稳定剂主要供应特殊板材压延工艺,但随着下游绿色化学标准的日益普及,其供应量正在下降。

化学品供应商正在主要挤出厂附近扩建模块化混合设施,从而实现准时交货和更严格的配方控制。与型材製造商的联合认证专案正在加快生产线变更核准,缩短换算时间。稳定剂的转型凸显了法规要求如何重塑供应链,使拥有深厚研发实力和一体化物流的企业更具优势。

欧洲PVC市场报告按产品类型(硬质PVC、软质PVC、低烟PVC等)、稳定剂类型(钙基、铅基、锡基和有机锡基等)、应用(管道和配件、薄膜和片材、电线电缆等)、最终用户行业(建筑和施工、汽车、电气和电子等)以及地区(德国、法国、英国、义大利等)进行细分。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第3章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 建设产业からの需要増加

- 自动车产业からの需要増加

- 水利基础建设计划需求增加

- 医疗产业对医用级PVC的需求

- 在包装应用的使用日益增多

- 市场限制

- 零售商加速禁用PVC食品包装

- REACH法规对传统铅和锡稳定剂的限制日益收紧。

- 窗户型材领域生物基聚合物替代率不断提高

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 硬质PVC

- 透明硬质PVC

- 不透明硬质聚氯乙烯

- 软PVC

- 透明柔软PVC

- 非透明软质PVC

- 低烟PVC

- 氯乙烯

- 硬质PVC

- 安定剤タイプ别

- カルシウム系(Ca-Zn)

- 铅ベースPb

- スズ・有机スズ系(Sn)

- 钡基及其他(液态混合金属)

- 透过使用

- 管道和配件

- 薄膜和片材

- 电线电缆

- 瓶子

- プロファイル、ホース・チューブ

- 其他用途

- 按最终用户行业划分

- 建筑/施工

- 车

- 电気・电子产业

- 包装

- 鞋

- 卫生保健

- 其他终端用户产业

- 按地区

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 土耳其

- 其他欧洲地区

第6章 竞合情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Benvic Group

- Ercros SA

- Formosa Plastics Corporation

- Hanwa Solutions Chemical Division Corporation

- Industrie Generali SpA

- INEOS

- KEM ONE

- LG Chem

- Lukoil

- Oltchim SA

- Orbia

- Shin-Etsu Chemical Co. Ltd.

- SIBUR Holding PJSC

- Solvay

- Teknor Apex

- Vynova Group

- Westlake Corporation

第七章 市场机会与未来展望

Europe Polyvinyl Chloride Market size in 2026 is estimated at 6.91 million tons, growing from 2025 value of 6.74 million tons with 2031 projections showing 7.86 million tons, growing at 2.59% CAGR over 2026-2031.

Robust demand in pipes, profiles, and fittings, coupled with moderate recovery in residential construction, underpins near-term volume gains. Regulatory pressure from REACH continues to accelerate calcium-zinc stabilizer adoption, yet sustained infrastructure spending cushions transition costs. Energy-efficient renovation programs, electrical grid upgrades, and water-management projects anchor structural demand, while circular-economy mandates fast-track investment in recycling and bio-attributed PVC. Competitive intensity remains moderate as integrated producers leverage scale, captive feedstocks, and proprietary technology to offset compliance costs.

Europe Polyvinyl Chloride (PVC) Market Trends and Insights

Growing Demand from Construction Industry

The region's housing shortage and aging building stock keep renovation activity high, driving window-profile and siding volumes in the Europe PVC market. Thermal-performance gains of 12-13% in PVC frames reinforced with thermoplastic inserts improve compliance with EU energy-efficiency codes, further entrenching rigid PVC in retrofit projects. Member-state recovery funds earmark civil-works spending, with water-retention drainage systems illustrating PVC's functional and cost advantages in agricultural infrastructure. Stabilizing interest rates and normalized material prices enhance project viability across Northern markets, though fiscal constraints continue to cap growth in Southern Europe. The overall effect is a well-distributed, medium-term lift in PVC pipe and profile demand.

Increasing Demand from Automotive Industry

Electric-vehicle adoption is reshaping interior-component specifications, widening the aperture for flame-retardant flexible PVC in wire harnesses and floor coverings. German motor-vehicle output advanced 3% YoY in early 2025, boosting resin off-take from regional compounding plants. Bio-attributed PVC grades cut cradle-to-gate CO2 emissions by 58% while preserving tensile and thermal performance, enabling OEMs to meet ESG targets without platform redesign. Growth clusters around Germany, France, and northern Italy facilitate optimized logistics and just-in-sequence supply models. Tier-one suppliers are pairing digital quality-control tools with material innovations to eliminate trim waste and reduce cycle times.

Accelerating Retailer Bans on PVC Food Packaging

Large supermarket chains across Western Europe are phasing out PVC trays and cling films, pressuring converters to shift toward mono-material PET or paper-based formats. The forthcoming Packaging and Packaging Waste Regulation adds PFAS and BPA constraints, complicating compliance pathways for legacy PVC formulations. While pharmaceutical blister packs remain exempt, high-volume fresh-food segments experience immediate substitution, shaving flexible-film demand in the Europe PVC market. Brand-owner purchasing policies cascade upstream, compelling compounders to qualify alternative resins or develop recyclable PVC-blends for niche, barrier-critical applications. Eastern markets show lagged uptake of bans, offering temporary relief yet signaling an eventual region-wide transition.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand from Water Infrastructure Projects

- Healthcare Demand for Medical-Grade PVC

- Escalating REACH Restrictions on Legacy Lead and Tin Stabilizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid grades anchored 60.42% of the Europe PVC market share in 2025 as pipes, profiles, and fittings retain dominance across building and water-supply networks. Low-smoke PVC, although a smaller base, is set to clock the strongest 3.73% CAGR through 2031 on the back of fire-safety regulations in mass-transit, tunnel, and public-assembly projects. Flexible PVC volumes face mixed fortunes: demand for bio-plasticized clear grades in medical tubing offsets contraction in food-packaging films. Chlorinated PVC penetrates industrial hot-water lines, leveraging localized production to mitigate import tariffs and logistics costs.

Capacity additions stay disciplined as mature demand patterns stabilize operating rates around 80%. Extruders focus on die-head upgrades and inline-measurement systems to boost yields rather than greenfield expansions. Product-mix agility becomes a competitive differentiator as converters juggle rigid-clear orders for chemical-processing sight-glasses alongside bulk commitments for municipal pipe contracts. The Europe PVC market thus balances steady, high-volume rigid demand with specialty growth niches in low-smoke and CPVC segments.

Calcium-zinc solutions held 42.55% of stabilizer consumption in 2025, a clear signal of market pivot after the EU lead ban These packages are projected to expand at 3.47% CAGR to 2031, driving most additive-level value growth in the Europe PVC market. Lead-based stabilizers now persist mainly in recycled rigid streams under temporary derogations, while tin systems linger in heat-resistant wire-coating niches. Barium-zinc and liquid-mixed-metal formats supply specialty sheet calendaring but face volume erosion as unified green-chemistry criteria spread downstream.

Chemical suppliers scale modular blending facilities near major extrusion hubs, ensuring just-in-time deliveries and tighter formulation control. Collaborative qualification programs with profile manufacturers accelerate line-change approvals, compressing conversion timelines. The stabilizer shift underscores how regulatory imperatives reshape supply chains in favor of actors with R&D depth and integrated logistics.

The Europe PVC Market Report is Segmented by Product Type (Rigid PVC, Flexible PVC, Low-Smoke PVC, and More), Stabilizer Type (Calcium Based, Lead Based, Tin and Organotin Based, and More), Application (Pipes and Fittings, Films and Sheets, Wires and Cables, and More), End-User Industry (Building and Construction, Automotive, Electrical and Electronics, and More), and Geography (Germany, France, United Kingdom, Italy, and More).

List of Companies Covered in this Report:

- Benvic Group

- Ercros S.A.

- Formosa Plastics Corporation

- Hanwa Solutions Chemical Division Corporation

- Industrie Generali S.p.A.

- INEOS

- KEM ONE

- LG Chem

- Lukoil

- Oltchim SA

- Orbia

- Shin-Etsu Chemical Co. Ltd.

- SIBUR Holding PJSC

- Solvay

- Teknor Apex

- Vynova Group

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from construction industry

- 4.2.2 Increasing demand from automotive industry

- 4.2.3 Increasing demand from water infrastructure projects

- 4.2.4 Healthcare demand for medical-grade PVC

- 4.2.5 Rinsing Usage in Packaging Application

- 4.3 Market Restraints

- 4.3.1 Accelerating retailer bans on PVC food packaging

- 4.3.2 Escalating REACH restrictions on legacy lead and tin stabilizers

- 4.3.3 Rising bio-based polymer substitution in window-profile segment

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Rigid PVC

- 5.1.1.1 Clear Rigid PVC

- 5.1.1.2 Non-clear Rigid PVC

- 5.1.2 Flexible PVC

- 5.1.2.1 Clear Flexible PVC

- 5.1.2.2 Non-clear Flexible PVC

- 5.1.3 Low-smoke PVC

- 5.1.4 Chlorinated PVC

- 5.1.1 Rigid PVC

- 5.2 By Stabilizer Type

- 5.2.1 Calcium based (Ca-Zn)

- 5.2.2 Lead based Pb

- 5.2.3 Tin and Organotin based (Sn)

- 5.2.4 Barium-based and Others (Liquid Mixed Metals)

- 5.3 By Application

- 5.3.1 Pipes and Fittings

- 5.3.2 Films and Sheets

- 5.3.3 Wires and Cables

- 5.3.4 Bottles

- 5.3.5 Profiles, Hoses and Tubings

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Building and Construction

- 5.4.2 Automotive

- 5.4.3 Electrical and Electronics

- 5.4.4 Packaging

- 5.4.5 Footwear

- 5.4.6 Healthcare

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 United Kingdom

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Turkey

- 5.5.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Rankinh Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Benvic Group

- 6.4.2 Ercros S.A.

- 6.4.3 Formosa Plastics Corporation

- 6.4.4 Hanwa Solutions Chemical Division Corporation

- 6.4.5 Industrie Generali S.p.A.

- 6.4.6 INEOS

- 6.4.7 KEM ONE

- 6.4.8 LG Chem

- 6.4.9 Lukoil

- 6.4.10 Oltchim SA

- 6.4.11 Orbia

- 6.4.12 Shin-Etsu Chemical Co. Ltd.

- 6.4.13 SIBUR Holding PJSC

- 6.4.14 Solvay

- 6.4.15 Teknor Apex

- 6.4.16 Vynova Group

- 6.4.17 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 PVC Recycling and Circularity

- 7.2 Bio-based Stabilizer and Plasticizer Platforms

- 7.3 White-space and unmet-need assessment

全球压延聚氯乙烯柔性薄膜市场规模、份额、趋势及成长分析报告(2026-2034)

全球压延聚氯乙烯柔性薄膜市场规模、份额、趋势及成长分析报告(2026-2034) 2026年全球聚氯乙烯(PVC)捲帘百叶窗市场报告2026年全球PVC乳液市场报告2026年全球聚氯乙烯(PVC)市场报告

2026年全球聚氯乙烯(PVC)捲帘百叶窗市场报告2026年全球PVC乳液市场报告2026年全球聚氯乙烯(PVC)市场报告 PVC添加剂市场-全球产业规模、份额、趋势、机会及预测(按类型、製造流程、应用、地区及竞争格局划分,2021-2031年)聚氯乙烯市场-全球产业规模、份额、趋势、机会及预测(依产品类型、稳定剂类型、应用、终端用户产业、区域及竞争格局划分),2021-2031年

PVC添加剂市场-全球产业规模、份额、趋势、机会及预测(按类型、製造流程、应用、地区及竞争格局划分,2021-2031年)聚氯乙烯市场-全球产业规模、份额、趋势、机会及预测(依产品类型、稳定剂类型、应用、终端用户产业、区域及竞争格局划分),2021-2031年 按类型、形状、厚度、颜色、销售管道、应用程式和最终用户分類的硬质PVC板材市场,全球预测,2026-2032年特种PVC树脂市场:按类型、形态、技术、应用和终端用户产业划分,全球预测,2026-2032年环境保护添加剂市场按产品类型、应用和最终用途产业划分-2026-2032年全球预测

按类型、形状、厚度、颜色、销售管道、应用程式和最终用户分類的硬质PVC板材市场,全球预测,2026-2032年特种PVC树脂市场:按类型、形态、技术、应用和终端用户产业划分,全球预测,2026-2032年环境保护添加剂市场按产品类型、应用和最终用途产业划分-2026-2032年全球预测 北美聚氯乙烯(PVC):市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)

北美聚氯乙烯(PVC):市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)