|

市场调查报告书

商品编码

1851546

环氧树脂:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

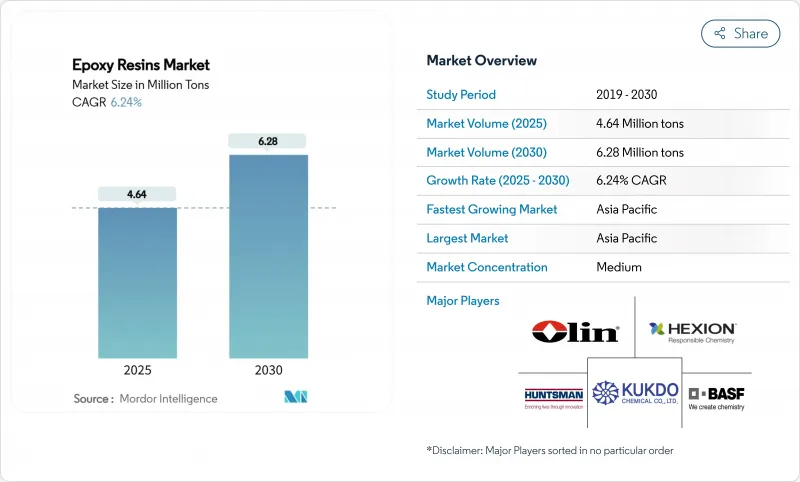

预计到 2025 年环氧树脂市场规模为 464 万吨,到 2030 年将达到 628 万吨,预测期(2025-2030 年)复合年增长率为 6.22%。

持续的需求源于该材料无与伦比的机械、化学和热性能,使其能够支援从风力发电机叶片到半导体封装等关键应用。随着对双酚A (BPA) 和挥发性有机化合物 (VOC) 的监管日益严格,以及水性、生物回收和低VOC化学品技术的进步,技术创新正在加速发展。新兴国家可再生能源基础设施的扩张、电气化趋势和基础设施支出为销售提供了积极的推动力,但不断上涨的贸易关税和植物来源价格的波动也为采购团队带来了短期不确定性。儘管环氧树脂市场集中度仍然不高,但可回收和生物基配方方面的突破性进展正在为成熟企业和新兴企业创造机会。

全球环氧树脂市场趋势与洞察

油漆和涂料需求不断成长

涂料将继续主导环氧树脂市场,预计到2024年将占60.15%的收入份额。东南亚和非洲的基础设施项目,以及依赖高阻隔阻隔性耐腐蚀涂料的船舶和包装等细分市场,将推动市场成长。 Westlake公司将于2025年推出EpoVIVE生物循环树脂,显示供应商正在努力平衡永续性和性能。量子点催化光化学技术将助力低VOC配方的普及,该技术无需使用昂贵的紫外线过滤剂即可提高树脂的耐光稳定性。 Amerlock 400等船用级系统可延长船舶的干船坞维修週期,并降低船队业者的全生命週期成本。预计到2030年,涂料的复合年增长率将达到6.51%,并将成为整个环氧树脂市场销售和技术创新的驱动力。

复合材料在风力发电机叶片中的应用

离岸风力发电的兴起、更大的转子直径以及碳-玻璃混合设计正在不断提升环氧树脂的性能阈值。全球风力发电理事会预测,新增产能将以每年8.8%的速度成长,以支撑树脂的长期需求。 TPI Composites的客户群将在2025年供应美国88%的陆上风力发电机叶片,这表明製程技术如何能够整合采购。西门子歌美飒已将可在弱酸性条件下脱粘的可回收环氧树脂叶片商业化,从而缓解了报废难题。利用机器学习优化叶片固化工艺,可进一步减少废弃物和能源消耗,巩固环氧树脂作为风力发电价值链首选基体材料的地位。

原物料价格波动

2024年上半年,中国双酚A(BPA)产能成长12.31%,达到每年548万吨,但运转率下降,区域价格较上季下跌4.6%。国都化工厂爆炸等事件导致BPA价格一度翻倍,下游化合物生产商面临利润风险。极端天气导致的不可抗力声明进一步加剧了供应的不确定性。因此,多家环氧树脂巨头正在建造专属式环氧氯丙烷和BPA装置,以确保原料供应并避免价格波动风险。

细分市场分析

作为风力涡轮机叶片和汽车复合材料的首选树脂,DGBEA树脂预计在2024年仍将占环氧树脂市场37.02%的份额。 DGBEA树脂以6.99%的复合年增长率持续成长,对市场扩张至关重要。然而,客户审核要求生产商证明其双酚A(BPA)来源可追溯且低碳。为此,欧洲、美国和日本的供应商正在试行物料平衡会计和生物回收原料,以维持DGBEA在环氧树脂市场的地位。

特种树脂填补了不同的性能空白。 DGBEF树脂具有低黏度,适用于船舶维护涂料;酚醛树脂则能抵抗炉衬中的热衝击。脂肪族环氧树脂具有建筑建筑幕墙所需的紫外线稳定性。缩水甘油胺体系在电子机壳中具有优异的金属黏合性。生物基树脂和环脂族树脂(归类为其他原料)预计到2030年将占据环氧树脂市场相当大的份额,因为闭合迴路回收和碳核算正受到股东的关注。

环氧树脂市场报告按原料(DGBEA(双酚A和ECH)、DGBEF(双酚F和ECH)、酚醛树脂(甲醛和苯酚)、脂肪族(脂肪醇)、缩水甘油胺(芳香胺和ECH)、其他)、应用(油漆和涂料、黏合剂和密封剂、复合材料、电气和ECH)以及其他地区(亚太)以及其他地区进行其他地区(亚太)

区域分析

亚太地区仍将是环氧树脂市场的主导区域,预计到2024年将占全球需求的48.19%,并有望在2030年前以6.44%的复合年增长率成长。中国树脂出口面临高达354.99%的美国反倾销税,迫使像DCM Shriram在印度投资1.25亿美元的待开发区建厂这样的企业,转向服务于地域更加多元化的基本客群。泰国和越南正在购买新的印刷电路板和风力涡轮机叶片生产能力,而日本和韩国则在推广用于半导体和离岸风电领域的高玻璃化转变温度(Tg)和可回收化学品。

北美将利用製造业回流、基础设施投资和可再生能源税额扣抵来缓解进口树脂流量的波动。 1.01%至547.76%不等的反补贴税将鼓励国内製造商运作暂停中的核子反应炉,并投资新的原料资产。加拿大风电开发商指定使用北极级环氧树脂体系,而墨西哥的汽车工业将推动对结构性黏着剂的需求。美国国家再生能源实验室(NREL)的植物来源环氧树脂研究凸显了该地区在永续性的领先地位。

欧洲正努力在严格的双酚A(BPA)法规与尖端研发之间寻求平衡。一家德国汽车零件製造商正与一家当地树脂製造商合作开发一种导热电磁相容(EMC)材料。英国离岸风力发电要求环氧底漆单桩的使用寿命达到25年,而法国核能产业则在推广耐辐射等级的材料。斯科特·巴德公司斥资3000万英镑在英国扩建产能,凸显了其在全球物流变化下对本地供应的承诺。在北欧,循环经济政策已经到位,一项欧盟资助的计画正在试验闭合迴路环氧树脂回收利用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 油漆和涂料需求不断成长

- 复合材料在风力发电机叶片中的应用

- 电气和电子产业需求不断成长

- 基础设施建设驱动的黏合剂需求成长

- 3D列印环氧光敏聚合物

- 市场限制

- 原物料价格波动

- 更严格的VOC和BPA法规

- 反倾销税扰乱贸易流动

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模及成长预测(价值及数量)

- 按原料

- DGBEA(双酚A和ECH)

- DGBEF(双酚F和ECH)

- 酚醛树脂(甲醛/苯酚)

- 脂肪族(脂肪醇)

- 缩水甘油胺(芳香胺和ECH)

- 其他原料(环脂族、生物基环氧树脂)

- 依实体形态

- 液体

- 坚硬的

- 解决方案

- 水性分散体

- 透过使用

- 油漆和涂料

- 黏合剂和密封剂

- 合成的

- 电气和电子

- 风力发电机

- 海洋

- 其他应用(建筑、用于 3D 列印的光敏聚合物等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Atul Ltd

- Bodo Moller Chemie GmbH

- Cardolite Corporation

- Chang Chun Group

- DIC Corporation

- Dow

- Grasim Industries Limited

- Hexion Inc.

- Huntsman International LLC

- Jiangsu Sanmu Group Co., Ltd.

- Kolon Industries

- Kukdo Chemical Co., Ltd

- Mitsui Chemicals, Inc.

- Nama

- Nan Ya Plastics Corporation

- Olin Corporation

- Robnor ResinLab Ltd,

- Sika AG

- Sinochem Holdings Corporation Ltd.

- Association for Chemical and Metallurgical Production(SPOLCHEMIE)

- Westlake Corporation

第七章 市场机会与未来展望

The Epoxy Resins Market size is estimated at 4.64 million tons in 2025, and is expected to reach 6.28 million tons by 2030, at a CAGR of 6.22% during the forecast period (2025-2030).

Sustained demand is rooted in the material's unmatched mechanical, chemical, and thermal performance that underpins critical uses ranging from wind-turbine blades to semiconductor packaging. Innovation is accelerating as stricter regulations on bisphenol A (BPA) and volatile organic compounds (VOCs) advance waterborne, bio-circular, and low-VOC chemistries. Expanding renewable-energy infrastructure, electrification trends, and infrastructure spending in emerging economies add positive volume momentum, while escalating trade duties and raw-material price swings present near-term uncertainties for procurement teams. The epoxy resins market remains moderately concentrated, yet breakthrough work on recyclable and plant-derived formulations is widening the opportunity set for both incumbents and specialist newcomers.

Global Epoxy Resins Market Trends and Insights

Increasing Demand from Paints and Coatings

Paints and coatings continued to dominate the epoxy resins market with a 60.15% revenue share in 2024. Growth is reinforced by infrastructure programs in Southeast Asia and Africa and by marine and packaging niches that depend on high-barrier, corrosion-resistant finishes. Westlake's 2025 launch of EpoVIVE bio-circular resins illustrates how suppliers are balancing sustainability with performance. The shift to low-VOC formulations is aided by quantum-dot-catalyzed photochemistry that improves sunlight stability without costly UV blockers Marine-grade systems such as Amerlock 400 lengthen dry-dock cycles, lowering total lifecycle cost for fleet operators.The resulting 6.51% CAGR to 2030 positions coatings as both volume and innovation anchors for the broader epoxy resins market.

Wind-Turbine Blade Composites Uptake

Growing offshore wind installations, larger rotor diameters, and hybrid carbon-glass designs are raising epoxy performance thresholds. The Global Wind Energy Council forecasts 8.8% annual growth in new capacity, which underpins long-run resin demand. TPI Composites' customer base supplied 88% of 2025 US onshore blades, underscoring how process know-how consolidates purchasing. Siemens Gamesa has already commercialized recyclable epoxy blades that de-bond under mild acidic conditions, easing end-of-life challenges. Machine-learning optimization of blade cure schedules further cuts waste and energy use, reinforcing epoxy's position as the matrix of choice in the wind energy value chain.

Raw-Material Price Volatility

China expanded BPA capacity by 12.31% in H1 2024 to 5.48 million t pa, yet utilization dipped and regional prices fell 4.6% quarter-on-quarter. Disruptions such as the Guodu Chemical plant explosion temporarily doubled BPA prices, exposing downstream formulators to margin risk. Force-majeure declarations following extreme weather events added further supply uncertainty. Several epoxy majors are therefore building captive epichlorohydrin and BPA units to secure feedstock and hedge volatility.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand from Electrical and Electronics

- Growing Infrastructure-Led Adhesive Demand

- Stricter VOC and BPA Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DGBEA resins retained 37.02% epoxy resins market share in 2024 as the workhorse grade for wind-energy blades and automotive composites. At a 6.99% CAGR they remain integral to market expansion, yet customer audits are pushing producers to demonstrate traceable, lower-carbon BPA supply. In response, Western and Japanese suppliers are piloting mass-balance accounting and bio-circulating feedstocks to preserve DGBEA's position in the epoxy resins market.

Specialty resins fill clear performance gaps. DGBEF offers lower viscosity for marine maintenance coatings, while novolac chemistries withstand thermal shock inside furnace linings. Aliphatic epoxies deliver UV stability essential for architectural facades. Glycidylamine versions provide superior metal adhesion in electronics housings. Bio-based and cycloaliphatic chemistries, grouped under other raw materials, are projected to be the fastest movers and could capture a measurable slice of the epoxy resins market by 2030 as closed-loop recycling and carbon accounting gain shareholder focus.

The Epoxy Resins Market Report is Segmented by Raw Material (DGBEA (Bisphenol A and ECH), DGBEF (Bisphenol F and ECH), Novolac (Formaldehyde and Phenols), Aliphatic (Aliphatic Alcohols), Glycidylamine (Aromatic Amines and ECH), and More), Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia-Pacific remained the epicenter of the epoxy resins market, securing 48.19% of 2024 demand and pointing to a 6.44% CAGR through 2030. China's resin exports face US anti-dumping duties as high as 354.99%, prompting ventures like DCM Shriram's USD 125 million Indian greenfield unit to serve a more regionally diversified customer base. Thailand and Vietnam capture fresh PCB and wind-blade capacity, while Japan and South Korea push ultra-high-Tg and recyclable chemistries for semiconductors and offshore wind applications.

North America leverages reshoring, infrastructure investment, and renewable-energy tax credits to buffer volatility in imported resin flows. Countervailing duties ranging from 1.01% to 547.76% spur domestic producers to reactivate idled reactors and invest in new feedstock assets. Canadian wind-farm developers specify Arctic-grade epoxy systems, and Mexico's automotive clusters accelerate demand for structural adhesives. NREL's plant-derived epoxy research underscores the region's sustainability leadership.

Europe balances stringent BPA rules with cutting-edge R&D. German automotive suppliers co-engineer thermally conductive EMCs with local resin formulators. The United Kingdom's offshore wind boom sustains 25-year service life requirements for epoxy-primed monopiles, and France's nuclear sector pushes radiation-resistant grades. Scott Bader's GBP 30 million UK capacity addition highlights commitments to local supply amid global logistics flux. The Nordic region, already well advanced in circular-economy policy, pilots closed-loop epoxy recycling trials under EU-funded programs.

- Atul Ltd

- Bodo Moller Chemie GmbH

- Cardolite Corporation

- Chang Chun Group

- DIC Corporation

- Dow

- Grasim Industries Limited

- Hexion Inc.

- Huntsman International LLC

- Jiangsu Sanmu Group Co., Ltd.

- Kolon Industries

- Kukdo Chemical Co., Ltd

- Mitsui Chemicals, Inc.

- Nama

- Nan Ya Plastics Corporation

- Olin Corporation

- Robnor ResinLab Ltd,

- Sika AG

- Sinochem Holdings Corporation Ltd.

- Association for Chemical and Metallurgical Production (SPOLCHEMIE)

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand from Paints and Coatings

- 4.2.2 Wind-Turbine Blade Composites Uptake

- 4.2.3 Increasing Demand from Electrical and Electronics

- 4.2.4 Growing Infrastructure-Led Adhesive Demand

- 4.2.5 3-D Printed Epoxy Photopolymers Adoption

- 4.3 Market Restraints

- 4.3.1 Raw-Material Price Volatility

- 4.3.2 Stricter VOC and BPA Regulations

- 4.3.3 Anti-Dumping Duties Disrupting Trade Flows

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Raw Material

- 5.1.1 DGBEA (Bisphenol A and ECH)

- 5.1.2 DGBEF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenol)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials (Cycloaliphatic, Bio-based Epoxies)

- 5.2 By Physical Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.2.3 Solution

- 5.2.4 Waterborne Dispersion

- 5.3 By Application

- 5.3.1 Paints and Coatings

- 5.3.2 Adhesives and Sealants

- 5.3.3 Composites

- 5.3.4 Electrical and Electronics

- 5.3.5 Wind Turbines

- 5.3.6 Marine

- 5.3.7 Other Applications (Construction, 3-D Printing Photopolymers, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%(/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Atul Ltd

- 6.4.2 Bodo Moller Chemie GmbH

- 6.4.3 Cardolite Corporation

- 6.4.4 Chang Chun Group

- 6.4.5 DIC Corporation

- 6.4.6 Dow

- 6.4.7 Grasim Industries Limited

- 6.4.8 Hexion Inc.

- 6.4.9 Huntsman International LLC

- 6.4.10 Jiangsu Sanmu Group Co., Ltd.

- 6.4.11 Kolon Industries

- 6.4.12 Kukdo Chemical Co., Ltd

- 6.4.13 Mitsui Chemicals, Inc.

- 6.4.14 Nama

- 6.4.15 Nan Ya Plastics Corporation

- 6.4.16 Olin Corporation

- 6.4.17 Robnor ResinLab Ltd,

- 6.4.18 Sika AG

- 6.4.19 Sinochem Holdings Corporation Ltd.

- 6.4.20 Association for Chemical and Metallurgical Production (SPOLCHEMIE)

- 6.4.21 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment