|

市场调查报告书

商品编码

1851585

威胁情报保全服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Threat Intelligence Security Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

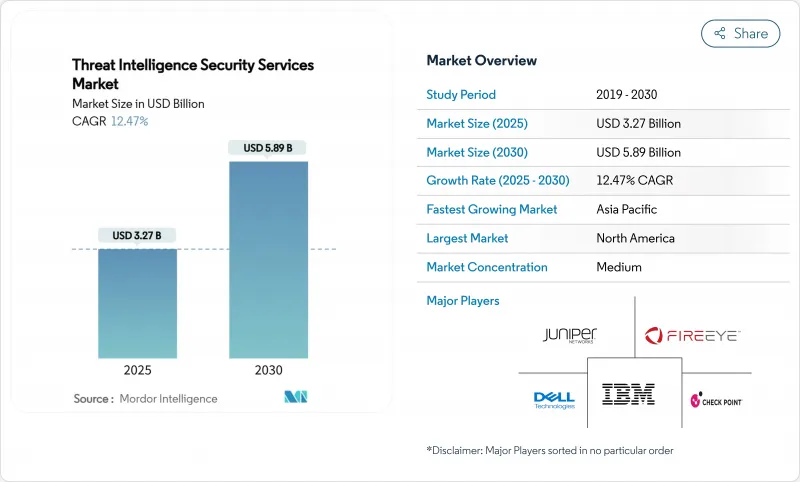

预计到 2025 年,威胁情报保全服务市场规模将达到 32.7 亿美元,到 2030 年将达到 58.9 亿美元,在此期间的复合年增长率为 12.47%。

市场扩张反映了安全策略从被动的边界防御转向持续威胁搜寻、风险暴露管理和预测分析的重大转变。主导宣传活动的加剧、云端安全事件激增65%以及主要司法管辖区强制执行的资料外洩通知,都在推动对即时、情境化威胁资料的需求。平台融合(以零信任和扩展检测与回应 (XDR) 的部署为代表)进一步加速了相关投资,因为安全团队正在寻求整合的可见性和自动化回应。同时,应用程式介面 (API) 攻击面的指数级增长以及由生成式人工智慧 (AI) 代码助理带来的内部风险,迫使企业重新评估其风险态势,从而推动了蓬勃发展的威胁情报保全服务市场。

全球威胁情报保全服务市场趋势与洞察

国家支持的高级威胁防护(APT)宣传活动的迅速扩张

像Volt Typhoon和Salt Typhoon这样的国家级组织正加强对关键基础设施的攻击力度,这促使各机构优先考虑战术性情报和事件前归因能力。网路安全与基础设施安全局(CISA)在2024年发布了3,368份勒索软体预警通知,证实了复杂入侵尝试的数量之多。如今的攻击不再局限于间谍活动,还包括破坏性的预先部署,因此需要持续监控和专门的威胁搜寻。伊朗攻击者同时将目标对准医疗保健和金融服务业,这使得威胁情报成为各行业的战略要务。这些趋势正在加速对託管侦测、增强型恶意软体分析和情境归因服务的投资。

云端工作负载激增,API攻击也随之浮现。

向云端迁移扩大了攻击面,企业在多重云端环境中运行数千个 API。 API 中断是 2024 年报告的大多数云端安全漏洞的罪魁祸首,暴露出东西向流量的可见性不足。传统的网路监控缺乏对短暂工作负载的上下文讯息,这加速了云端原生威胁情报的普及,后者能够即时映射依赖关係。微服务架构进一步增加了资产清单的复杂性,使得企业更加依赖自动化发现和持续风险评分。因此,针对无伺服器和容器环境客製化的云端交付分析引擎和风险管理模组的需求持续成长。

一级威胁猎人和分析师短缺

对深度取证和恶意软体逆向工程的需求远远超过了供给。掌握国家级对手的策略需要多年的训练,然而安全团队却面临人员削减和薪资上涨的双重困境。这种缺口正在推动行业整合,因为小型供应商难以招揽专家,而客户则寻求託管式检测和回应的承包服务。如今,服务提供者需要实现日常故障排查的自动化,并将稀缺的专业知识解放出来,用于更高价值的任务,这导致人们对人工智慧辅助分析模组的兴趣日益浓厚。

细分市场分析

云端部署目前已占据威胁情报保全服务市场58%的份额。预计到2030年,该细分市场将以18.20%的复合年增长率成长,从而提升云端原生分析引擎的重要性。弹性运算分散式储存使服务供应商无需客户侧硬体即可处理PB级遥测Petabyte,这对于到2030年威胁情报安全服务市场规模达到58.9亿美元至关重要。虽然在需要本地资料处理的主权云端和国防环境中,本地部署仍然存在,但目前的开发蓝图优先考虑混合连接器而非独立设备。

混合部署模式在受监管企业中日益普及,这些企业利用云端技术扩展规模,但出于合规性考虑,仍将某些资料集保留在国内。由于传统感测器缺乏容器流量的上下文讯息,以 API 为中心的攻击向量在云端环境中尤其容易受到攻击。 Palo Alto Networks 报告称,其与人工智慧相关的年度经常性收入超过 2 亿美元,年增 4 倍,这表明市场对云端交付的机器学习模组有着强劲的需求。因此,儘管云端优势已成定局,但供应商必须解决延迟、加密和本地化等问题,才能加速云端技术的进一步普及。

预计到2024年,託管式侦测与回应(MDR)将占据威胁情报保全服务市场56%的份额,年增长率预计为18.55%。企业青睐MDR,因为它融合了技术、远端检测和专家经验,能够在不增加员工负担的情况下缩短平均侦测时间。 MDR业务的快速成长表明,威胁情报保全服务市场正致力于以结果为导向的交付。专业服务对于成熟度评估、框架设计和持续威胁暴露管理部署仍然至关重要。

订阅资讯流虽然已形成商品化基础,但正逐渐演变为包含攻击者画像和风险评分等丰富上下文资讯的软体包。 Fortinet累计,其 2025 年第一季安全营运年度经常性收入 (ARR) 为 4.345 亿美元,年成长 30.3%,这表明整合式託管侦测与编配(MDR) 和编排功能正在蓬勃发展。在工具整合日益加剧的背景下,那些将精心策划的遥测数据与自动化隔离工作流程相结合的供应商正在建立具有竞争力的差异化优势。

威胁情报保全服务市场按部署类型(云端、本地部署)、服务类型(託管侦测与回应、专业/咨询服务、其他)、组织规模(大型企业、中小企业)、最终用户产业(银行和金融服务、医疗保健、其他)以及地区进行细分。市场预测以美元计价。

区域分析

北美地区占全球收入的38%,这得益于美国2025年275亿美元的网路安全预算。该预算包括向美国网路安全和基础设施安全局(CISA)提供的30亿美元津贴,用于扩展资讯共用网路。零信任的高普及率、活跃的资金筹措以及云端原生供应商生态系统,都巩固了该地区的领先地位。联邦行政命令14028号强制政府机构将威胁情报整合到安全运作中,相关产业也正在效法供应链保障模式。加拿大正在与美国的资讯揭露标准接轨,墨西哥金融监管机构正在将事件报告范围扩大到金融科技领域,增加了新的需求来源。

亚太地区预计将以18.90%的复合年增长率快速成长,成为全球成长最快的地区。随着政府专案加强国内安全管理,中国网路安全市场预计在2029年达到236.6亿美元。日本的战略文件呼吁将国内网路安全收入提高三倍,并将国家预算增加50%,这将推动对产业级威胁情报的需求。印度正在快速数位化,CERT-IN(印度电脑紧急应变小组)强制要求即时报告特定事件,并鼓励采用相关服务。澳洲斥资5.86亿澳元的网路弹性计画正在推动对託管情报的需求,区域电讯也正在投资远端检测交换。

在NIS2指令和区域资料保护法规的推动下,欧洲保持稳定成长。德国预计到2025年将在网路安全方面投入超过100亿欧元,以保护工业自动化系统免受破坏。英国累计6亿英镑,并计划在2035年将GDP的5%用于国家安全,这将为供应商提供更清晰的长期发展前景。资料主权要求将促进区域安全营运中心的发展,这些中心能够在国家边界内处理遥测数据,这将使拥有居住感知云端架构和多语言分析师支援的供应商受益。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 国家主导的APT宣传活动激增

- 云端工作负载的激增与 API 攻击面

- CISO平台零信任与XDR

- 强制违规通知法(美国、欧盟、亚太地区)

- 利用 GEN-AI 代码助手降低内部风险

- 采用 CTEM* 进行连续控制验证

- 市场限制

- 一级威胁猎人和分析师短缺

- 中小企业预算压缩

- 跨境远端检测共用面临的资料主权障碍

- 虚假TI讯息流导致的警报疲劳

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争的激烈程度

第五章 市场规模与成长预测

- 透过部署模式

- 云

- 本地部署

- 按服务类型

- 託管侦测与回应

- 专业/咨询

- 订阅资料馈送

- 按组织规模

- 大公司

- 小型企业

- 按最终用户行业划分

- 银行和金融服务

- 卫生保健

- 资讯科技和电讯

- 零售与电子商务

- 生命科学/製药

- 政府和国防部

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Google LLC(Mandiant)

- Recorded Future Inc.

- CrowdStrike Holdings Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- International Business Machines Corporation

- Palo Alto Networks Inc.

- Dell Technologies Inc.

- Check Point Software Technologies Ltd.

- Trellix LLC(McAfee Enterprise)

- Broadcom Inc.(Symantec)

- LogRhythm Inc.

- Juniper Networks Inc.

- F-Secure Corporation

- LookingGlass Cyber Solutions Inc.

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Trend Micro Incorporated

- Elastic NV(Security)

- Kaspersky Lab JSC

第七章 市场机会与未来展望

The threat intelligence security services market size stands at USD 3.27 billion in 2025 and is forecast to reach USD 5.89 billion by 2030, advancing at a 12.47% CAGR over the period.

The expansion reflects a decisive shift from reactive perimeter defense toward continuous threat hunting, exposure management, and predictive analytics. Escalating state-sponsored campaigns, a 65% rise in cloud security incidents, and mandatory breach-notification laws across major jurisdictions are amplifying demand for real-time, contextual threat data. Platform convergence, led by zero-trust and Extended Detection and Response (XDR) rollouts, is further accelerating investment as security teams seek unified visibility and automated response. At the same time, the proliferation of application programming interface attack surfaces and insider risks arising from generative AI code assistants have prompted organizations to reassess risk postures, energizing the threat intelligence security services market.

Global Threat Intelligence Security Services Market Trends and Insights

Rapid Escalation in State-Sponsored APT Campaigns

Nation-state groups such as Volt Typhoon and Salt Typhoon have intensified operations against critical infrastructure, prompting organizations to prioritize tactical intelligence and pre-incident attribution capabilities. The Cybersecurity and Infrastructure Security Agency issued 3,368 pre-ransomware notifications in 2024, underscoring the volume of advanced intrusion attempts. Attacks now go beyond espionage to include destructive pre-positioning, which demands continuous monitoring and specialized hunting. Iranian actors are simultaneously targeting healthcare and financial services, turning threat intelligence into a strategic imperative across sectors. These developments have accelerated spending on managed detection, enriched malware analysis, and contextual attribution services.

Proliferation of Cloud Workloads & API Attack-Surface

Cloud migration has multiplied attack entry points, with organizations operating thousands of APIs across multi-cloud settings. API failures contributed to a majority of cloud breaches reported in 2024, revealing visibility gaps in east-west traffic. Traditional network monitoring lacks context for ephemeral workloads, fuelling adoption of cloud-native threat intelligence that can map dependencies in real time. Microservices architectures further complicate asset inventories, increasing reliance on automated discovery and continuous risk scoring. The outcome is sustained momentum for cloud-delivered analytics engines and exposure management modules tailored to serverless and container environments.

Shortage of Tier-1 Threat-Hunters & Analysts

Demand for deep forensics and malware reverse-engineering outpaces supply. Years of training are needed to master nation-state adversary tactics, yet security teams face attrition and wage inflation. The gap is driving consolidation as smaller vendors struggle to retain experts, and clients turn to Managed Detection and Response for turnkey coverage. Providers must now automate routine triage to free scarce specialists for higher-value pursuits, heightening interest in AI-assisted analysis modules.

Other drivers and restraints analyzed in the detailed report include:

- Zero-Trust & XDR Platformisation by CISOs

- Mandatory Breach-Notification Laws

- Budget Compression in SME Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment already commands 58% of the threat intelligence security services market share. The segment is projected to expand at an 18.20% CAGR through 2030, reinforcing the centrality of cloud-native analytics engines. Elastic compute and distributed storage enable providers to process petabytes of telemetry without customer-side hardware, which is critical as threat intelligence security services market size grows to USD 5.89 billion in 2030. On-premises deployments persist in sovereign cloud and defense contexts that require local data processing, although development roadmaps now prioritize hybrid connectors rather than standalone appliances.

Hybrid adoption is rising among regulated firms that embrace the cloud for scale yet retain select data sets in country for compliance. API-centric attack vectors accentuate cloud resonance since traditional sensors lack context for container traffic. Palo Alto Networks reported AI-centric Annual Recurring Revenue above USD 200 million with 4x year-over-year growth, validating appetite for cloud-delivered machine learning modules. Cloud superiority is therefore entrenched, but vendors must address latency, encryption, and locality factors to accelerate further penetration.

Managed Detection and Response own 56% of the threat intelligence security services market share as of 2024 and are forecast to grow 18.55% annually. Enterprises favour MDR because it fuses technology, telemetry, and human expertise, reducing mean time to detect without staffing burdens. The surge in MDR contracts underlines how the threat intelligence security services market pivots toward outcome-based delivery. Professional services remain vital for maturity assessments, framework design, and Continuous Threat Exposure Management rollouts.

Subscription feeds form a commodity base but are evolving toward context-rich packages with actor profiling and risk scoring. Fortinet posted Security Operations ARR of USD 434.5 million in Q1 2025, up 30.3% year on year, signalling that integrated MDR plus orchestration gains momentum. Vendors blending curated telemetry with automated containment workflows are building defensible differentiation as tool consolidation continues.

Threat Intelligence Security Services Market Segmented by Deployment Mode (Cloud, On-Premises), Service Type (Managed Detection & Response, Professional/Consulting and More), Organization Size (Large Enterprises, Small & Medium Enterprises), End-User Industry (Banking & Financial Services, Healthcare and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controls 38% of global revenue, supported by the United States' USD 27.5 billion cybersecurity allocation for 2025, which includes USD 3 billion for CISA grants that expand intelligence sharing networks. High adoption of zero-trust, robust venture funding, and an ecosystem of cloud-native vendors sustain regional leadership. Federal Executive Order 14028 compels government agencies to integrate threat intelligence into security operations, and adjacent industries replicate the model for supply-chain assurance. Canada is harmonizing with U.S. disclosure norms, while Mexico's financial regulator extends incident reporting to fintech, adding new demand vectors.

Asia-Pacific is projected to grow at an 18.90% CAGR, the fastest worldwide. China's cybersecurity market is on track to reach USD 23.66 billion by 2029 as government programs enforce in-country security controls. Japan's strategic documents call for tripling domestic cybersecurity sales and boosting national budgets by 50%, which elevates appetite for industry-grade threat intelligence. India continues rapid digitization; its CERT-IN directives oblige real-time reporting for specified incidents, driving service uptake. Australia's AUD 586 million cyber resilience package underpins managed intelligence demand, and regional telecom providers are investing in cross-border telemetry exchanges.

Europe maintains steady growth propelled by the NIS2 directive and local data protection mandates. Germany expects cybersecurity spending beyond €10 billion in 2025 to shield industrial automation from sabotage. The United Kingdom earmarked an extra £600 million for intelligence agencies and plans to devote 5% of GDP to national security by 2035 reinforce long-term visibility for vendors. Data-sovereignty requirements stimulate growth of regional security operations centers capable of processing telemetry within national borders. Providers offering residency-aware cloud fabrics and multilingual analyst support are therefore preferred.

- Google LLC (Mandiant)

- Recorded Future Inc.

- CrowdStrike Holdings Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- International Business Machines Corporation

- Palo Alto Networks Inc.

- Dell Technologies Inc.

- Check Point Software Technologies Ltd.

- Trellix LLC (McAfee Enterprise)

- Broadcom Inc. (Symantec)

- LogRhythm Inc.

- Juniper Networks Inc.

- F-Secure Corporation

- LookingGlass Cyber Solutions Inc.

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Trend Micro Incorporated

- Elastic N.V. (Security)

- Kaspersky Lab JSC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid escalation in state-sponsored APT campaigns

- 4.2.2 Proliferation of cloud workloads and API attack-surface

- 4.2.3 Zero-trust and XDR platformisation by CISOs

- 4.2.4 Mandatory breach-notification laws (US, EU, APAC)

- 4.2.5 Insider-risk from Gen-AI code-assistants (under-radar)

- 4.2.6 Adoption of CTEM* for continuous controls validation (under-radar)

- 4.3 Market Restraints

- 4.3.1 Shortage of Tier-1 threat-hunters and analysts

- 4.3.2 Budget compression in SME segment

- 4.3.3 Data-sovereignty barriers to cross-border telemetry sharing (under-radar)

- 4.3.4 Adversary abuse of spoofed TI feeds causing alert fatigue (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Service Type

- 5.2.1 Managed Detection and Response

- 5.2.2 Professional / Consulting

- 5.2.3 Subscription Data-feeds

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Banking and Financial Services

- 5.4.2 Healthcare

- 5.4.3 IT and Telecom

- 5.4.4 Retail and e-Commerce

- 5.4.5 Life Sciences / Pharma

- 5.4.6 Government and Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Google LLC (Mandiant)

- 6.4.2 Recorded Future Inc.

- 6.4.3 CrowdStrike Holdings Inc.

- 6.4.4 Fortinet Inc.

- 6.4.5 Cisco Systems Inc.

- 6.4.6 International Business Machines Corporation

- 6.4.7 Palo Alto Networks Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Check Point Software Technologies Ltd.

- 6.4.10 Trellix LLC (McAfee Enterprise)

- 6.4.11 Broadcom Inc. (Symantec)

- 6.4.12 LogRhythm Inc.

- 6.4.13 Juniper Networks Inc.

- 6.4.14 F-Secure Corporation

- 6.4.15 LookingGlass Cyber Solutions Inc.

- 6.4.16 Rapid7 Inc.

- 6.4.17 Arctic Wolf Networks Inc.

- 6.4.18 Trend Micro Incorporated

- 6.4.19 Elastic N.V. (Security)

- 6.4.20 Kaspersky Lab JSC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

威胁狩猎市场:按组件、服务类型、技术、部署模式、组织规模和产业划分-2026年至2032年全球市场预测

威胁狩猎市场:按组件、服务类型、技术、部署模式、组织规模和产业划分-2026年至2032年全球市场预测 2026年全球网路威胁情报市场报告

2026年全球网路威胁情报市场报告 网路威胁情报订阅市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署模式、最终用户和解决方案划分

网路威胁情报订阅市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署模式、最终用户和解决方案划分 内部威胁防护市场 - 全球产业规模、份额、趋势、机会及预测(按解决方案、部署方式、公司规模、产业垂直领域、地区和竞争格局划分,2021-2031 年)威胁狩猎市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署模式、组织规模、产业垂直领域、威胁类型、地区和竞争格局划分,2021-2031 年)按服务类型、部署模式、组织规模和行业分類的託管威胁狩猎服务市场 - 全球预测,2026-2032 年

内部威胁防护市场 - 全球产业规模、份额、趋势、机会及预测(按解决方案、部署方式、公司规模、产业垂直领域、地区和竞争格局划分,2021-2031 年)威胁狩猎市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署模式、组织规模、产业垂直领域、威胁类型、地区和竞争格局划分,2021-2031 年)按服务类型、部署模式、组织规模和行业分類的託管威胁狩猎服务市场 - 全球预测,2026-2032 年 网路威胁情报市场预测至2032年:按情报类型、组件、部署模式、应用、最终用户和地区分類的全球分析

网路威胁情报市场预测至2032年:按情报类型、组件、部署模式、应用、最终用户和地区分類的全球分析 全球威胁搜寻市场

全球威胁搜寻市场 2025-2029年全球网路威胁情报市场

2025-2029年全球网路威胁情报市场 网路威胁情报市场(按类型和地区)

网路威胁情报市场(按类型和地区)