|

市场调查报告书

商品编码

1851596

石墨:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Graphite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

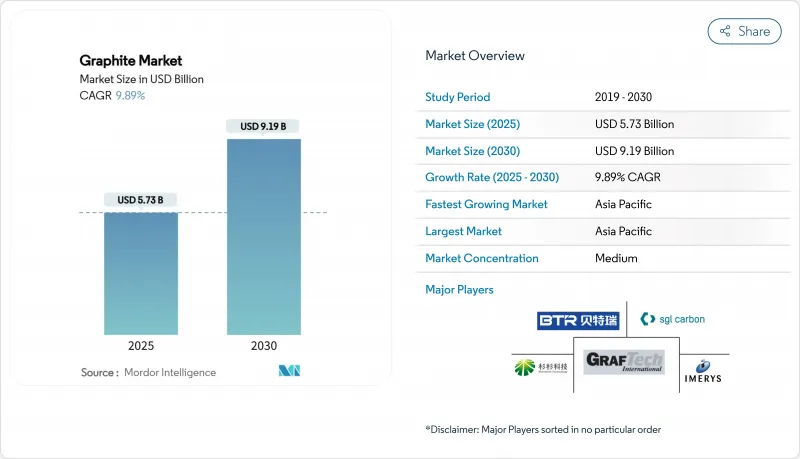

预计到 2025 年石墨市场规模为 57.3 亿美元,到 2030 年将达到 91.9 亿美元,预测期(2025-2030 年)复合年增长率为 9.89%。

强劲的电池需求、钢铁製造业的结构性转变以及关键材料供应链在地化努力的加强,共同推动了这一发展趋势。石墨产业正经历从大宗商品产业向战略性材料产业的重大转型,为交通运输、电力和重工业的脱碳转型提供支援。亚太地区自然资源的集中以及北美和欧洲的政策奖励,正在推动对采矿、加工和回收资产的新投资。同时,不断上涨的资本成本和日益严格的环境法规促使合资企业在确保负责任采购的同时分散风险。合约期限的延长是推动这一趋势的新兴因素,如今承购协议的期限通常为10年或更长。

全球石墨市场趋势与洞察

锂离子电池产业需求不断成长

目前,电池製造商占据石墨市场最大份额,该细分市场年复合成长率超过17%,显示未来十年将持续加速成长。电动车品牌间日益激烈的价格竞争加剧了阳极的成本敏感性,并使天然石墨更具偏好,其每吨价格比合成石墨低数千美元。这是因为合成石墨的生产需要3000°C的高温,而天然石墨的提炼温度通常低于1800°C。近期的竞标数据显示,汽车製造商愿意接受首圈效率略有下降,以换取天然材料更优的ESG(环境、社会和治理)表现。

亚洲和中东钢铁产量不断成长

为减少排放而转向电弧炉(EAF)显着推动了对高功率石墨电极的需求。随着机械和汽车应用在钢铁消费量中所占份额的不断增加,对电极耐久性和导电性的需求也随之增长。电极纯度、出钢间隔时间和炉子整体能源效率之间存在直接联繫,因此电极供应商可以透过证明其产品硫氮含量低来获得溢价。

严格的环境法规

碳定价法规和范围 3 揭露框架鼓励生产商采用再生能源,并试行美国能源局开发的低温催化石墨化技术。

细分市场分析

儘管合成石墨目前占据主导地位(预计到2024年将占58.09%的市场份额),但天然石墨的市场份额正在迅速增长。诸如碱烧结合微波加热等新型纯化工艺,如今已能生产出纯度高达99.95%的天然石墨,缩小了以往的性能差距。由此可见,OEM采购平台中出现的生命週期评估数据正促使采购策略向天然石墨倾斜,即便其直接电池能量密度略低。

生物质衍生合成石墨引发了人们对供应安全的担忧,因为它可能减少对开采的天然石墨和石油针状焦的依赖。先驱性研究证实,木质素基前驱体可产生层间距适合锂离子嵌入的紊乱层状碳。由此得出一个新的推论:天然鳞片石墨和生物石墨的双重筹资策略正逐渐成为应对地缘政治动盪和碳价上涨的有效对冲手段。

区域分析

目前,亚太地区的石墨市占率为55.42%,年复合成长率超过11%,成长最快。中国的领先地位归功于丛集将片状石墨矿、精炼生产线和球化厂整合到单一物流走廊。一种新兴理论认为,印尼和马来西亚等东南亚国协正效法中国的丛集模式,吸引中游加工企业,希望在价值链中打造新的节点。

北美正从依赖进口的消费群向新兴的生产市场转型,这得益于《通货膨胀削减法案》的税额扣抵(该政策可报销合格阳极组件成本的10%)。欧洲石墨产业的发展更受监管导向而非资源供应的影响。电池中强制性的最低再生材料基准值将促使超级工厂与回收商签订多年供应协议。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 锂离子电池产业需求不断成长

- 亚洲和中东钢铁产量不断成长

- 加强打造以循环为导向的社会

- 电子产业对导电石墨的需求日益增长

- 来自航太和国防工业的需求不断增长

- 市场限制

- 严格的环境法规

- 优质天然石墨供应有限

- 原物料价格波动

- 价值链分析

- 监理与环境展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 天然石墨

- 合成石墨

- 透过使用

- 电极

- 耐火材料、铸造厂及铸造厂

- 电池

- 润滑油

- 其他用途(散热材料、摩擦材料、煞车衬等)

- 按最终用户行业划分

- 冶金

- 电子元件

- 车

- 其他产业(能源、航太和国防等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Asbury Carbons

- BTR New Material Group Co., Ltd.

- GrafTech International

- Graphit Kropfmuhl GmbH

- Imerys

- Mason Resources Inc.

- Mersen

- Nippon Kokuen Group

- Northern Graphite

- POCO

- Resonac Holdings Corporation

- SGL Carbon

- Shanghai Shanshan Technology Co., Ltd.

- Syrah Resources Limited

- Tokai Carbon Co., Ltd.

- Triton Minerals Limited

第七章 市场机会与未来展望

The Graphite Market size is estimated at USD 5.73 billion in 2025, and is expected to reach USD 9.19 billion by 2030, at a CAGR of 9.89% during the forecast period (2025-2030).

Robust battery demand, structural shifts in steelmaking, and intensifying efforts to localize critical-material supply chains collectively underpin this trajectory. The graphite industry is experiencing a decisive shift from a bulk commodity sector to a strategic materials arena supporting decarbonization across mobility, power, and heavy industry. Natural-resource concentration in Asia-Pacific and policy incentives in North America and Europe are catalyzing new investment in mining, processing, and recycling assets. Simultaneously, the rising cost of capital and stricter environmental scrutiny are encouraging joint ventures that spread risk while ensuring responsible sourcing. A fresh inference that emerges is that contract structures are lengthening off-take agreements now regularly span 10-plus years, signaling buyers' willingness to lock in feedstock security even at higher prices.

Global Graphite Market Trends and Insights

Augmenting Demand from the Lithium-ion Battery Industry

Battery manufacturers now account for the single largest slice of the graphite market share, and the segment's 17%-plus CAGR indicates sustained acceleration through the decade. Intensifying price competition among electric-vehicle (EV) brands magnifies the cost sensitivity of anodes, tilting preference toward natural graphite that offers a multithousand-dollar per-tonne advantage over synthetic alternatives. This cost gradient is widening as energy prices rise, because synthetic production requires temperatures of 3,000 °C, whereas natural purification usually runs below 1,800 °C. One inference observable from recent tender data is that automakers are accepting slightly lower first-cycle efficiency in exchange for natural graphite's better ESG profile, illustrating how carbon-footprint metrics have become commercially material.

Increase in Steel Production in Asia and the Middle East

The shift toward electric-arc furnaces (EAF) for emissions abatement is materially lifting demand for ultra-high-power graphite electrodes. Machinery and automotive applications now drive a larger share of steel consumption, implicitly elevating electrode durability and conductivity requirements. A fresh inference is that electrode suppliers can certify lower sulfur and nitrogen contents, secure premium price realizations because EAF operators see a direct link between electrode purity, tap-to-tap time, and overall furnace energy efficiency.

Stringent Environmental Regulations

Carbon-pricing regimes and Scope-3 disclosure frameworks are prompting producers to adopt renewable power and to pilot low-temperature catalytic graphitization developed by the U.S. Department of Energy, which halves energy use and compresses production cycles from weeks to hours.

Other drivers and restraints analyzed in the detailed report include:

- Increase in Natural Graphite Recycling Initiatives

- Growing Demand from the Electronics Industry

- Limited Availability of High-Quality Natural Graphite

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural graphite is rapidly gaining market share despite synthetic graphite's current dominance at 58.09% of the market in 2024. Fresh purification processes such as caustic baking combined with microwave heating now deliver 99.95% purity, closing the historical performance gap. A clear inference is that life-cycle-assessment data, which now feature in OEM purchasing dashboards, are tipping procurement policies in favor of natural graphite even when immediate cell-level energy density is marginally lower.

Supply-security concerns amplify interest in biomass-derived synthetic graphite, which could reduce dependence on mined natural graphite and petroleum needle-coke routes. Pilot studies confirm that lignin-based precursors yield turbostratic carbon with an interlayer spacing conducive to lithium intercalation. The fresh inference is that dual-sourcing strategies, natural flake plus bio-graphite, are surfacing as an attractive hedge against geopolitical disruption and carbon-price escalation.

The Graphite Market Report Segments the Industry by Type (Natural Graphite and Synthetic Graphite), Application (Electrodes, Refractories, Casting, and Foundries, Batteries, Lubricants, and Other Applications), End-User Industry (Metallurgy, Electronic, Automotive, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific currently captures 55.42% graphite market share and registers the fastest regional CAGR at above 11%. China's dominance stems from integrated clusters that combine flake-graphite mines, purification lines, and spheronization plants into a single logistics corridor. A fresh inference is that ASEAN nations such as Indonesia and Malaysia are courting mid-stream processors, hoping to replicate China's cluster model and thus create alternative nodes in the value chain.

North America is transitioning from an import-dependent consumer base to an emerging producer, helped by the Inflation Reduction Act's tax credits that reimburse 10% of qualified anode-component costs. Europe's graphite industry is shaped by regulatory leadership rather than resource endowment. Mandatory minimum recycled-content thresholds in batteries are pushing gigafactories to sign multi-year supply contracts with recyclers.

- Asbury Carbons

- BTR New Material Group Co., Ltd.

- GrafTech International

- Graphit Kropfmuhl GmbH

- Imerys

- Mason Resources Inc.

- Mersen

- Nippon Kokuen Group

- Northern Graphite

- POCO

- Resonac Holdings Corporation

- SGL Carbon

- Shanghai Shanshan Technology Co., Ltd.

- Syrah Resources Limited

- Tokai Carbon Co., Ltd.

- Triton Minerals Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Augmenting Demand from the Lithium-ion Battery Industry

- 4.2.2 Increase in Steel Production in Asia and the Middle East

- 4.2.3 Increase in Natural Graphite Recycling Initiatives

- 4.2.4 Growing Demand for Conductive Graphite from Electronics Industry

- 4.2.5 Increasing Demand from Aerospace and Defense Industry

- 4.3 Market Restraints

- 4.3.1 Stringent Environmental Regulations

- 4.3.2 Limited Availability of High-Quality Natural Graphite

- 4.3.3 Fluctuation in Raw Material Prices

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Environmental Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Natural Graphite

- 5.1.2 Synthetic Graphite

- 5.2 By Application

- 5.2.1 Electrodes

- 5.2.2 Refractories, Casting and Foundries

- 5.2.3 Batteries

- 5.2.4 Lubricants

- 5.2.5 Other Applications (Thermal Management Materials, Friction Products and Brake Linings,etc.)

- 5.3 By End-user Industry

- 5.3.1 Metallurgy

- 5.3.2 Electronic

- 5.3.3 Automotive

- 5.3.4 Other Industries (Energy, Aerospace and Defence, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asbury Carbons

- 6.4.2 BTR New Material Group Co., Ltd.

- 6.4.3 GrafTech International

- 6.4.4 Graphit Kropfmuhl GmbH

- 6.4.5 Imerys

- 6.4.6 Mason Resources Inc.

- 6.4.7 Mersen

- 6.4.8 Nippon Kokuen Group

- 6.4.9 Northern Graphite

- 6.4.10 POCO

- 6.4.11 Resonac Holdings Corporation

- 6.4.12 SGL Carbon

- 6.4.13 Shanghai Shanshan Technology Co., Ltd.

- 6.4.14 Syrah Resources Limited

- 6.4.15 Tokai Carbon Co., Ltd.

- 6.4.16 Triton Minerals Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Applications of Graphite in Green Technologies

- 7.3 Increasing Graphene Demand and Nuclear Energy

高纯度石墨市场按应用、类型、形态和纯度等级划分,全球预测(2026-2032年)

高纯度石墨市场按应用、类型、形态和纯度等级划分,全球预测(2026-2032年) 特种石墨:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

特种石墨:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本石墨市场规模、份额、趋势和预测:按类型、应用、最终用途行业和地区划分,2026-2034年

日本石墨市场规模、份额、趋势和预测:按类型、应用、最终用途行业和地区划分,2026-2034年 2026年全球石墨市场报告2026年全球热解石墨市场报告2026年全球等向性挤压石墨市场报告2026年全球等向性石墨市场报告2026年全球等静压石墨市场报告2026年全球铺路砖市场报告LED用碳化硅基座市场:按材料类型、晶圆尺寸、封装结构、沉积过程、应用和最终用户类型划分,全球预测,2026-2032年

2026年全球石墨市场报告2026年全球热解石墨市场报告2026年全球等向性挤压石墨市场报告2026年全球等向性石墨市场报告2026年全球等静压石墨市场报告2026年全球铺路砖市场报告LED用碳化硅基座市场:按材料类型、晶圆尺寸、封装结构、沉积过程、应用和最终用户类型划分,全球预测,2026-2032年