|

市场调查报告书

商品编码

1851610

区块链即服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Blockchain-as-a-Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

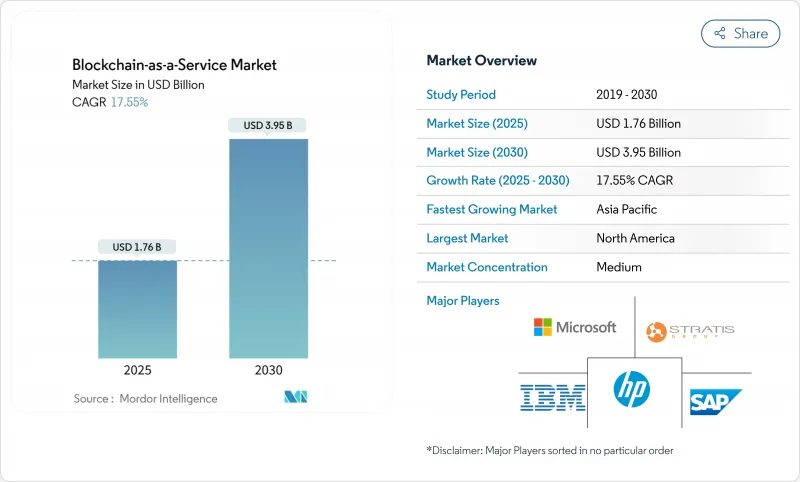

预计到 2025 年,区块链即服务市场规模将达到 17.6 亿美元,到 2030 年将达到 39.5 亿美元,在此期间的复合年增长率将达到 17.55%。

随着企业从小型概念验证转向生产部署,区块链即服务(BaaS)市场正蓬勃发展,这得益于监管环境的日益清晰以及云端服务供应商将分散式帐本工具整合到更广泛的基础设施组合中。各国央行的数位货币试点项目,尤其是国际清算银行的mBridge计划,正在创造企业级区块链平台的下游需求。云端超大规模资料中心业者提供的配套服务降低了采购摩擦,而欧盟加密资产市场监管条例等法规结构也为企业支出提供了依据。北美地区的沙盒计划和亚太地区政府资助的代币化计划进一步加速了区块链的普及。同时,人才短缺和通讯协定层面互通性方面的不足仍然是需要关注的问题,并可能限制近期的成长。

全球区块链即服务市场趋势与洞察

受监管产业对防篡改资料完整性的需求日益增长

为了满足严格的审核追踪和证明要求,医疗保健、金融和製药业正在越来越多地采用区块链技术。 Change Healthcare 的 Hyperledger Fabric 实现方案每天已处理约 5,000 万笔交易,并储存不可窜改的日誌。追踪药品来源的欧洲药品法规也在推动类似的应用。金融机构透过在监管机构根据《药品和资讯合规法案》(MiCA) 认定为可信的区块链上记录监管数据,从而减轻了合规工作量。区块链即服务 (BaaS) 市场被定位为合规赋能工具,尤其是在审核越来越倾向于使用不可篡改的记录而非传统资料库的情况下。因此,随着已开发国家每推出一项新的数据整合政策,市场对区块链的需求将持续成长。

云端超大规模营运商正在将 BaaS 捆绑到其更广泛的 X 即服务堆迭中。

微软正在将区块链、人工智慧和物联网整合到 Azure 中,使客户能够透过熟悉的入口网站和现有合约启用帐本。亚马逊云端服务和Google云端也纷纷效仿,Kaleido 与 Azure 的合作提供了 500 多个预先建置 API,可轻鬆整合到企业工具中。这种捆绑式服务缩短了采购週期,尤其对那些缺乏深厚密码学专业知识的中型企业而言更是如此,并且使营运成本保持可变性而非资本密集。这种打包策略使所有管理云端工作负载的客户都能了解区块链即服务市场,从而使采用区块链即服务成为一个渐进式而非变革性的决策。

标准碎片化和通讯协定互通性差距

儘管IEEE和ISO仍在製定相关框架,但由于缺乏通用的即插即用标准,企业不得不客製化建造跨链连接器。 Sensor 日誌的研究表明,此类架构会增加复杂性并暴露新的攻击面。这阻碍了跨国公司跨境推广试点项目,从而减缓了区块链即服务市场累积数量的成长。在主导性的互通性通讯协定成熟之前,供应商必须将蓝图资源投入到建构自身桥樑。

细分市场分析

到2024年,平台即服务(PaaS)将构成比收入的38.0%,这主要得益于其整合开发环境和可配置性,这些优势吸引了大型企业。同时,託管服务预计将以19.98%的复合年增长率(CAGR)实现最快成长。这主要源自于企业对承包营运、安全性修补程式和全天候执行时间运作的需求,而无需自行运行节点。大型跨国公司的财务团队已表示,迁移到託管帐簿以实现跨境流动性后,西门子银行帐户减少了一半,每年节省了2000万美元。咨询和实施工作对于连接传统ERP系统和满足特定行业(例如金融和医疗保健行业)的法规要求仍然至关重要。

企业在需要对共识设定进行精细控制但又倾向于云端收费时,也会采用基础设施即服务 (IaaS)。同时,软体即法规(SaaS)套件正在开放抽象智慧合约编译的 API,降低了小型开发者的入门门槛。此外,日益严格的合规性要求使得不可篡改的审核追踪成为预设要求,这促使即使是风险规避型的董事会也核准订阅。这种持续的需求正在支撑区块链即服务 (BaaS) 市场在待开发区和现有棕地配置的成长。

到2024年,公共云端将占据区块链即服务(BaaS)市场63.0%的份额,因为超大规模云端服务商能够提供弹性扩展和高服务等级协定(SLA)。混合云将以22.10%的复合年增长率成长,因为金融机构和製药公司为了遵守《居住通讯法》(MiCA)及类似政策规定的资料驻留要求,会将敏感资料保留在本地。混合拓扑结构透过将生产链置于防火墙后,同时利用公有云建置开发沙箱,从而加快迭代速度。

当资料主权或敏感工作负载限制外部基础设施的使用时,私有私有云端便成为首选。欧盟新推出的营运弹性规则进一步推动了应急计画的製定,并使混合架构更具吸引力。因此,我们在区块链即服务市场中持续看到架构的多样性。企业为了因应成本审核和新的合规要求,正在不同环境之间迁移工作负载,这确保了对编配工具的长期需求。

区块链即服务市场报告按组件(平台即服务 (PaaS)、基础设施即服务 (IaaS)、其他)、部署模式(公共云端、私有云端、其他)、组织规模(大型企业、中小企业)、应用(智能合约、支付、其他)、最终用户垂直行业(IT 和通讯、製造业、其他)和地区进行细分。

区域分析

北美地区继续保持主导地位,预计到2024年将占据区块链即服务市场41.0%的份额,这主要得益于大型创业融资,例如由高盛和Citadel主导的Digital Asset 1.35亿美元融资。总部位于美国的超大规模云端服务供应商正在将帐本工具整合到其主流云端产品中,使现有客户能够快速上线。儘管一些州已推出监管沙盒以加速试点项目,但全国各地政策的碎片化仍然造成了合规性的不确定性,并延缓了跨州推广的进程。

亚太地区以18.69%的复合年增长率实现了最快增长。新加坡和香港政府支持的央行数位货币(CBDC)和代币化计划正在创造显着的成功案例,吸引银行和金融科技公司入驻商业平台。日本、韩国和中国的製造地正利用亚洲内部贸易走廊,将区块链应用于供应链和永续性报告等领域。大学的区块链实验室正在扩大区域人才储备,有助于缓解其他地区普遍存在的开发者短缺问题。

欧洲将受益于MiCA的统一规则,该规则将于2024年12月全面生效。汽车、奢侈品和食品公司将部署成熟可靠的解决方案,以满足监管机构和消费者的需求,例如雷诺的XCEED供应链系统。欧洲中央银行倡导数位资产市场一体化,这将促使各银行采用分散式帐本基础设施来实现后勤部门现代化,并维持短期合约交易。中东和非洲的新兴市场正在尝试将区块链应用于普惠金融和碳信用登记,但由于技术能力有限,其整体应用仍处于起步阶段。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 受监管产业对防篡改资料完整性的需求日益增长

- 云端超大规模营运商将 BaaS 打包到更广泛的 XaaS 服务堆迭中

- 关于代币化和稳定币的监管清晰度正在逐步提高。

- 中央银行沙盒计画购买BaaS后端

- 新冠疫情后企业级区块链试点计画激增

- 利用区块链永续性帐本进行范围 3排放审核(非正式审计)

- 市场限制

- 标准碎片化和通讯协定互通性差距

- 分散式帐本工程人才短缺

- 关于智能合约可执行性的法律原则尚不明确。

- 云端成本上涨使概念验证预算受到密切关注(儘管并未引起太多关注)。

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按组件

- 平台即服务 (PaaS)

- 基础设施即服务 (IaaS)

- 软体即服务 (SaaS) SDK 和 API

- 咨询及实施服务

- 託管/营运服务

- 按部署模式

- 公共云端

- 私有云端

- 混合云

- 按组织规模

- 大公司

- 小型企业

- 透过使用

- 智能合约

- 供应链可追溯性

- 数位身分和KYC

- 沉淀

- 管治、风险与合规

- 其他的

- 按行业

- 银行、金融服务和保险(BFSI)

- 医疗保健和生命科学

- 资讯科技和电信

- 零售与电子商务

- 製造业

- 能源与公共产业

- 政府/公共部门

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 海湾合作委员会(沙乌地阿拉伯、阿联酋、卡达等)

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Microsoft Corporation

- Amazon Web Services(AWS)

- Oracle Corporation

- SAP SE

- Hewlett-Packard Enterprise

- Huawei Technologies Co. Ltd.

- Alibaba Cloud

- Tencent Cloud

- R3

- ConsenSys

- Blockstream Inc.

- Stratis Group Ltd.

- PayStand Inc.

- Kaleido

- Guardtime

- Dragonchain Inc.

- Bitfury Group

- LeewayHertz

- Wipro Limited

- Accenture plc

- Infosys Limited

- NTT DATA

- LG CNS

- Tech Mahindra

第七章 市场机会与未来展望

The Blockchain-as-a-Service market size reached USD 1.76 billion in 2025 and is projected to climb to USD 3.95 billion by 2030, registering a 17.55% CAGR over the period.

The Blockchain-as-a-Service market is gaining momentum as enterprises move from small-scale proofs of concept toward production deployments, spurred by clearer regulations and cloud providers that embed distributed-ledger tools within broader infrastructure bundles. Central-bank digital-currency pilots, especially the Bank for International Settlements' mBridge project, are generating downstream demand for enterprise blockchain platforms. Cloud hyperscalers' bundled offerings reduce procurement friction, while regulatory frameworks such as the European Union's Markets in Crypto-Assets regulation legitimize enterprise spending. North American sandbox programs and Asia Pacific's state-funded tokenization initiatives further accelerate uptake. At the same time, ongoing talent shortages and protocol-level interoperability gaps remain watchpoints that could temper short-term growth.

Global Blockchain-as-a-Service Market Trends and Insights

Rising demand for tamper-proof data integrity across regulated industries

Health, finance, and pharmaceuticals increasingly adopt blockchain to meet stringent audit-trail and provenance mandates. Change Healthcare's Hyperledger Fabric deployment already processes about 50 million daily transactions while preserving immutable logs. European pharmaceutical rules that track medicine provenance drive similar uptake. Financial institutions cut compliance workloads by recording regulatory data on chains that regulators deem trustworthy under MiCA. These sector mandates position the Blockchain-as-a-Service market as a compliance enabler, particularly as auditors begin to prefer immutable records over traditional databases. Demand, therefore, scales with every new data-integrity policy in advanced economies.

Cloud hyperscalers bundling BaaS into broader X-as-a-Service stacks

Microsoft integrates blockchain, AI, and IoT on Azure, letting clients activate ledgers through familiar portals and existing contracts. Amazon Web Services and Google Cloud follow, while Kaleido's Azure tie-up offers more than 500 pre-built APIs that snap into enterprise tools. Bundling cuts procurement cycles, especially for mid-market firms without deep cryptography skills, and keeps operating costs variable instead of capital-intensive. This packaging strategy keeps the Blockchain-as-a-Service market visible to every customer managing cloud workloads, making adoption an incremental, rather than transformative, decision.

Fragmented standards and protocol interoperability gaps

IEEE and ISO continue to draft frameworks, yet no universal plug-and-play standard exists, forcing enterprises to custom-build cross-chain connectors iso.org. Sensors-journal research shows such architectures add complexity and new attack surfaces. Multinationals therefore hesitate to scale pilots across borders, which slows cumulative contract flow into the Blockchain-as-a-Service market. Until dominant interoperability protocols mature, vendors must allocate road-map resources to proprietary bridges that elevate costs and lengthen implementation timelines.

Other drivers and restraints analyzed in the detailed report include:

- Gradual regulatory clarity on tokenization and stablecoins

- Central-bank sandbox programs sourcing BaaS back-ends

- Talent shortage in distributed-ledger engineering

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform-as-a-Service contributed 38.0% revenue in 2024, underpinned by integrated development environments and configurability that attract large corporations. Managed Services, however, grows fastest at 19.98% CAGR as organizations seek turnkey operations, security patching and 24/7 uptime without running nodes themselves. Large multinational treasury teams cite tangible savings; Siemens cut bank accounts by half and saved USD 20 million each year after migrating to managed ledgers for cross-border liquidity. Consulting and implementation work remains essential to bridge legacy ERP systems and to meet sector-specific regulations in finance and healthcare.

Enterprises also adopt Infrastructure-as-a-Service when they need granular control over consensus settings yet still prefer cloud billing. Meanwhile, software-as-a-service toolkits expose APIs that abstract smart-contract compilation, lowering entry barriers for small developers. Rising compliance workloads make immutable audit trails a default requirement, so even risk-averse boards now approve subscriptions. This persistent demand anchors the Blockchain-as-a-Service market across both greenfield and brownfield deployments.

Public Cloud captured 63.0% of the Blockchain-as-a-Service market share in 2024 because hyperscalers provide elasticity and high service-level agreements. Still, Hybrid Cloud is on track for a 22.10% CAGR as financial institutions and pharmaceutical firms hold sensitive data on-premises to satisfy residency laws under MiCA and similar policies. Hybrid topologies keep production chains behind firewalls while using public cloud for development sandboxes, which speeds iteration.

Private Cloud persists where data sovereignty or classified workloads prohibit any external infrastructure. The European Union's new operational-resilience rules further motivate contingency planning, making hybrid designs attractive. As a result, the Blockchain-as-a-Service market sees consistent architectural diversity: enterprises swap workloads between environments in response to cost audits or new compliance directives, ensuring long-run demand for orchestration tools.

The Blockchain As A Service Market Report is Segmented by Component (Platform-As-A-Service (PaaS), Infrastructure-As-A-Service (IaaS), and More), Deployment Model (Public Cloud, Private Cloud, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), Application (Smart Contracts, Payments and Settlement, and More), End-User Vertical (IT and Telecom, Manufacturing, and More), and Geography.

Geography Analysis

North America continued to dominate in 2024 with a 41.0% Blockchain-as-a-Service market share, buoyed by deep venture funding such as Digital Asset's USD 135 million round led by Goldman Sachs and Citadel. US-based hyperscalers integrate ledger tools into mainstream cloud menus, allowing quick uptakes among existing clients. Regulatory sandboxes in several states accelerate production pilots, though nationwide policy fragmentation still injects compliance uncertainty that slows multi-state rollouts.

Asia Pacific records the steepest growth at an 18.69% CAGR. Government-backed CBDC and tokenization projects in Singapore and Hong Kong create visible proof points, drawing banks and fintechs onto commercial platforms. Manufacturing hubs across Japan, South Korea and China deploy blockchains for supply-chain and sustainability reporting use cases, leveraging intra-Asia trade corridors. Regional talent pools expand through university blockchain labs, helping offset developer shortages seen elsewhere.

Europe benefits from MiCA's uniform rules that became fully effective in December 2024. Automotive, luxury and food companies implement provenance solutions to satisfy regulators and consumers, exemplified by Renault's XCEED supply-chain systeM. The European Central Bank's advocacy for digital-assets market integration encourages banks to modernize back offices with distributed-ledger infrastructure, sustaining near-term contract flow. Emerging markets in the Middle East and Africa experiment with blockchain for financial inclusion and carbon credit registries, yet overall adoption remains nascent due to limited technical capacity.

- IBM Corporation

- Microsoft Corporation

- Amazon Web Services (AWS)

- Oracle Corporation

- SAP SE

- Hewlett-Packard Enterprise

- Huawei Technologies Co. Ltd.

- Alibaba Cloud

- Tencent Cloud

- R3

- ConsenSys

- Blockstream Inc.

- Stratis Group Ltd.

- PayStand Inc.

- Kaleido

- Guardtime

- Dragonchain Inc.

- Bitfury Group

- LeewayHertz

- Wipro Limited

- Accenture plc

- Infosys Limited

- NTT DATA

- LG CNS

- Tech Mahindra

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for tamper-proof data integrity across regulated industries

- 4.2.2 Cloud hyperscalers bundling BaaS into broader X-as-a-Service stacks

- 4.2.3 Gradual regulatory clarity on tokenization and stablecoins

- 4.2.4 Central-bank sandbox programs sourcing BaaS back-ends

- 4.2.5 Explosion of enterprise-grade blockchain pilots post-COVID-19

- 4.2.6 Scope-3 emissions auditing via blockchain sustainability ledgers (under-radar)

- 4.3 Market Restraints

- 4.3.1 Fragmented standards and protocol interoperability gaps

- 4.3.2 Talent shortage in distributed-ledger engineering

- 4.3.3 Uncertain jurisprudence on smart-contract enforceability

- 4.3.4 Rising cloud spend scrutiny dampening POC budgets (under-radar)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform-as-a-Service (PaaS)

- 5.1.2 Infrastructure-as-a-Service (IaaS)

- 5.1.3 Software-as-a-Service (SaaS) SDKs and APIs

- 5.1.4 Consulting and Implementation Services

- 5.1.5 Managed/Operations Services

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Smart Contracts

- 5.4.2 Supply-Chain Traceability

- 5.4.3 Digital Identity and KYC

- 5.4.4 Payments and Settlement

- 5.4.5 Governance, Risk and Compliance

- 5.4.6 Others

- 5.5 By End-User Vertical

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 IT and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Manufacturing

- 5.5.6 Energy and Utilities

- 5.5.7 Government and Public Sector

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Netherlands

- 5.6.3.7 Russia

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC (Saudi Arabia, UAE, Qatar, etc.)

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Amazon Web Services (AWS)

- 6.4.4 Oracle Corporation

- 6.4.5 SAP SE

- 6.4.6 Hewlett-Packard Enterprise

- 6.4.7 Huawei Technologies Co. Ltd.

- 6.4.8 Alibaba Cloud

- 6.4.9 Tencent Cloud

- 6.4.10 R3

- 6.4.11 ConsenSys

- 6.4.12 Blockstream Inc.

- 6.4.13 Stratis Group Ltd.

- 6.4.14 PayStand Inc.

- 6.4.15 Kaleido

- 6.4.16 Guardtime

- 6.4.17 Dragonchain Inc.

- 6.4.18 Bitfury Group

- 6.4.19 LeewayHertz

- 6.4.20 Wipro Limited

- 6.4.21 Accenture plc

- 6.4.22 Infosys Limited

- 6.4.23 NTT DATA

- 6.4.24 LG CNS

- 6.4.25 Tech Mahindra

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

区块链即服务市场(按组件、组织规模、部署模式、应用和最终用户产业划分)—全球预测,2025 年至 2032 年

区块链即服务市场(按组件、组织规模、部署模式、应用和最终用户产业划分)—全球预测,2025 年至 2032 年 2032 年区块链即服务(BaaS) 市场预测:按组件、部署模型、应用、最终用户和地区进行的全球分析

2032 年区块链即服务(BaaS) 市场预测:按组件、部署模型、应用、最终用户和地区进行的全球分析 2025年全球区块链服务市场报告

2025年全球区块链服务市场报告 区块链即服务市场规模、份额及成长分析(按产品、组织规模、应用、垂直领域和地区)-2025 年至 2032 年产业预测2025年全球区块链即服务市场报告

区块链即服务市场规模、份额及成长分析(按产品、组织规模、应用、垂直领域和地区)-2025 年至 2032 年产业预测2025年全球区块链即服务市场报告 BaaS(区块链即服务)的全球市场,2024-2028

BaaS(区块链即服务)的全球市场,2024-2028 全球区块链即服务市场规模研究(按组织规模、应用、垂直和区域预测 2022-2032)

全球区块链即服务市场规模研究(按组织规模、应用、垂直和区域预测 2022-2032) BaaS(区块链即服务)市场:按组件、按业务应用、按行业、按地区,2024-2031 年

BaaS(区块链即服务)市场:按组件、按业务应用、按行业、按地区,2024-2031 年 区块链即服务市场 - 按组件、最终用户垂直、按地区、按竞争细分的全球行业规模、份额、趋势、机会和预测,2019-2029FBaaS(区块链即服务)市场 - 2024 年至 2029 年预测

区块链即服务市场 - 按组件、最终用户垂直、按地区、按竞争细分的全球行业规模、份额、趋势、机会和预测,2019-2029FBaaS(区块链即服务)市场 - 2024 年至 2029 年预测