|

市场调查报告书

商品编码

1851637

小型风力发电机:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Small Wind Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

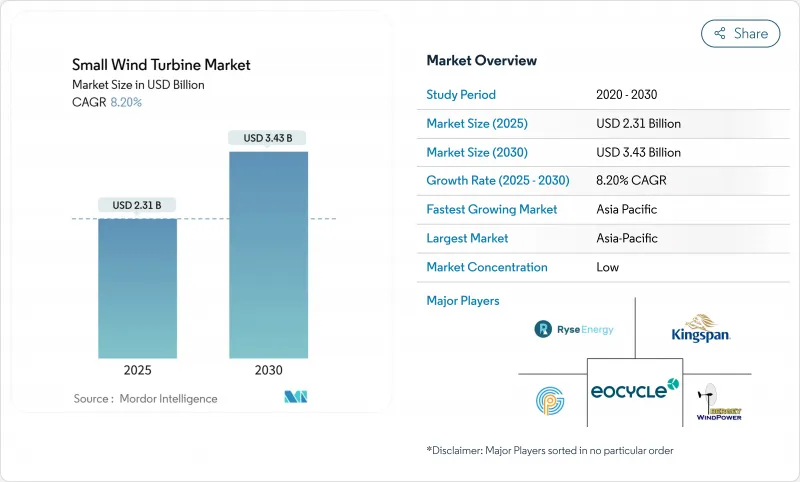

预计到 2025 年,小型风力发电机市场价值为 23.1 亿美元,到 2030 年将达到 34.3 亿美元,预测期(2025-2030 年)复合年增长率为 8.20%。

成长的驱动力来自政策奖励、垂直轴技术的进步以及在电讯、农业和分散式能源系统中日益增长的应用。北美、欧盟和亚洲的公共资助计画正在加速其普及,而机器学习驱动的涡轮机优化降低了全生命週期能源成本并提高了可靠性。企业购电协议正在推动併网计划的需求,而风光互补系统正在扩大风力资源不稳定地区的市场规模。在10千瓦以下的细分市场,与屋顶太阳能的成本竞争仍然是一个限制因素,但效率的提高和新的安装法规正在缩小这一差距。

全球小型风力发电机市场趋势与洞察

加勒比海偏远离岛快速通电

离岛的电力公司正在用包含小型风力发电机的混合可再生微电网取代柴油发电系统。各国政府和多边贷款机构正在争取优惠融资,以降低计划前期成本并提高开发商的参与度。提供耐腐蚀涂层和模组化物流方案的涡轮机供应商正在该市场中获得竞争优势。每个站点的平均装置容量仍低于50千瓦,产品系列从0千瓦到20千瓦不等。稳定的信风支持超过35%的发电容量,与纯太阳能发电方案相比,缩短了投资回收期。岛屿电气化计画采用基于绩效的收费系统,奖励高运转率,这凸显了整合到新型涡轮机的数位监控平台的价值。

美国农村能源补贴推动了5千瓦以下风力涡轮机的需求

美国农村能源计画(Rural Energy for America Program)已拨款1.8亿美元,用于支持农场和农村小型企业的小型风力发电系统,该计划将持续到2025年。津贴最高可涵盖50%的资本成本,在平均风速超过6公尺/秒的地区,投资可在六年内回收成本。国家可再生能源实验室(NREL)的竞争性改善项目(Competitive Improvement 计划)透过资助原型认证和获取第三方融资,弥补了以往的融资缺口。该计画的目标是涵盖400多个农场,到2027年将微型风力发电系统的累积装置容量增加25兆瓦。将风力涡轮机与谷仓屋顶太阳能板结合,可以帮助种植者抵消白天的尖峰负载和晚间灌溉需求。根据该计划获得UL 6141认证的製造商有资格获得联邦政府的优先采购。

欧洲都市区基于高度的区域划分法规

在许多历史街区,地方政府高度限制规定风力涡轮机轮毂高度不得超过10米,这限制了发电产量。不同的要求通常需要进行阴影闪烁和视觉评估,从而延长了计划工期。噪音测量法规依赖模型而非经验数据,这推高了工程成本。由于管辖权分散,相邻市政当局对同一计划的规定各不相同,这阻碍了开发商在整个城市范围内扩张。欧盟风能一揽子计画指南呼吁协调统一,但地方文物保护组织仍拥有否决权。供应商已推出可安装在女儿墙下的短桅杆垂直轴风力涡轮机设计,但扫掠面积的减少降低了年度发电量。

细分市场分析

由于动态成熟且供应链成熟,水平轴风力发电机组预计在2024年仍将占68%的市场份额。该细分市场在大型农场改造和农村住宅风力发电机更换领域占据主导地位。製造商正将2-20kW的机型标准化,以满足美国农业部和印度通讯业者的竞标要求,从而实现规模经济。垂直轴小型风力发电机组的市场规模预计将从较低的基数快速成长,年复合成长率将达到14%,超过水平轴风力发电机组。垂直轴风力发电机在屋顶和街道电线杆附近的湍流风环境中表现出色,其全方位叶片能够捕捉多方向的阵风。透过遗传学习演算法调整桨距角,可将功率係数提高至多0.45,使其更接近贝茨极限基准。较少的活动部件使得地面齿轮箱的安装成为可能,从而减少了30%的维护车辆出勤次数,加速了其在商业车队中的应用。

垂直轴风力发电机供应商与建筑幕墙工程师合作,将风力发电机整合到幕墙中,满足了欧盟的创新技术配额要求。反向旋转的萨沃纽斯/达里厄斯混合转子最大限度地减少了扭矩波动,并在5米距离处实现了35分贝以内的声学特征。东京大学的现场测试证实,即使在颱风般的强风下,轴承寿命也能达到15年,从而消除了人们对耐久性的担忧。开发人员透过建构租赁协议,将服务和回收义务捆绑在一起,满足了中国和欧盟的循环经济法规。垂直轴风力发电机定位为补充而非颠覆性技术,能够实现混合阵列,从而平衡整个场地的能源输出。

2024年,0-5kW微型风力发电机将占小型风力发电机市场46%的份额,这主要得益于政府补贴在农场、小屋和路边感测器等场所的安装。儘管由于电子产品的商品化,平均售价较去年同期下降了6%,但售后服务收入却有所成长。中型机组(21-100kW)到2030年将以11%的复合年增长率成长,主要为通讯塔、工业和资料中心园区供电。开发人员倾向于选择符合IEC 61400-2认证标准的机型,这些机型整合了故障穿越和无功功率支援功能,无需单独的转换器即可併并联型。在60kW规模下,每千瓦单位的成本已降至2,300美元以下,缩小了与屋顶太阳能+储能係统的成本差距。

在电网收费包含需求费用的城市商业区,6-20千瓦小型风力发电机的市场规模正在稳定成长。冷冻负载高的农民选择15千瓦的涡轮机来抵销晚间用电高峰。以往的部署得益于安装人员的熟练操作,从而缩短了计划前置作业时间。中型供应商提供延保服务,保证97%的技术可用性,并从绿色银行获得低成本贷款。可互通的SCADA系统将风力发电输出与现场电池发行係统连接起来,优化自用率并避免併网限速。

小型风力发电机市场报告按轴类型(水平轴风力发电机、垂直轴风力发电机)、连接方式(离网、併网、混合)、安装位置(屋顶/建筑物集成、独立塔架)、应用(住宅、商业、其他地区(北美地区)和其他地区(北美地区)。

区域分析

2024年,亚太地区将占小型风力发电机市场48%的份额,年复合成长率达10%,主要得益于中国工业脱碳和印度通讯电气化的发展。中国正强制要求到2030年,40%的产品必须获得绿色认证,并鼓励经济特区在屋顶和庭院安装风力涡轮机。印度铁塔业者正积极采用可再生能源作为备用电源,混合能源竞标中指定使用5千瓦微型风力涡轮机,并搭配太阳能光电和锂电池组。日本在铁路沿线附近进行垂直轴风力涡轮机示范计画的同时,也严格执行声学法规。东协岛国正在建造社区微电网,越南製造商则向该地区的渔船出口10千瓦风力涡轮机。

欧洲仍然是一个成熟的平台,清晰的监管环境支持着稳定成长。可再生能源指令的修订缩短了50千瓦以下计划的授权时间,鼓励在都市区部署风电。德国在部分地区免除了10公尺以下风力涡轮机的规划许可,从而降低了25%的软成本。挪威海德鲁公司签署的为期29年、总装置容量235兆瓦的风电购电协议,展现了长期电力销售的可靠性。丹麦严格的39分贝噪音上限对出口到世界各地的产品的声学性能产生了影响。英国支持在岛屿地区扩大陆域风电项目,包括微型风力涡轮机,以期造福当地社区。

北美地区的政策正在提振市场需求。美国1.8亿美元的津贴将加速农场风电部署,而美国国家再生能源实验室(NREL)320万美元的竞争力基金将推动认证过程。加拿大对诺德克斯(Nordex)247兆瓦公用事业级风力涡轮机的订单激增,推动了零件的本地化生产。然而,由于屋顶太阳能的价格优势,住宅风电的普及速度有所放缓。纽约州等州正在试行针对小型风力涡轮机的上网电价补贴政策,而加州则在试办一项奖励多技术系统的微电网补贴政策。墨西哥农村电气化局已重新开放混合能源套件的竞标,其中包括用于离网诊所的1.5千瓦风力发电机组。

- Aeolos Wind Energy LtdBergey

- Windpower Co.

- City Windmills Holdings PLCWind

- Energy Solutions BVSD

- Wind Energy LtdUNITRON

- Energy Systems Pvt LtdNorthern

- Power Systems Inc.

- Shanghai Ghrepower Green EnergyTUGE

- Energia OURyse

- EnergyKingspan

- 集团有限公司(风能事业部)

- Eocycle Technologies Inc.

- XZERES Wind Corp.

- Fortis Wind Energy BVHY

- EnergyEndurance

- Wind Power Inc.

- Kliux Energies InternationalPika

- Energy(Generac)

- Envergate Energy AGSuzlon

- Energy Ltd( <=100千瓦段)

其他好处

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加勒比海偏远离岛快速通电

- 美国美国「农村能源促进美国」拨款计画推动了对5千瓦以下风力涡轮机的需求激增

- 中国的「零碳工业」强制要求园区内可再生能源。

- 欧盟屋顶可再生能源指令促进建筑物风力发电。

- 印度和东协的电信塔混合化议程

- Microwind在北欧资料中心丛集的企业购电协议数量增加

- 市场限制

- 欧洲都市区基于高度的区域划分法规

- 日本收紧声排放标准

- 北美地区10千瓦以下屋顶太阳能光电发电系统与高平准化能源成本的对比

- 非洲缺乏长期维运生态系统,导致融资能力有差距。

- 供应链分析

- 监理展望

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章 市场规模与成长预测

- 按轴类型

- 水平轴风力发电机(HAWT)(上风型、下风型)

- 垂直轴风力发电机(VAWT)(萨沃纽斯式、达里厄斯式、陀螺式)

- 按额定容量(千瓦)

- 0 至 5 千瓦(微型)

- 6至20千瓦(小型)

- 21-100千瓦(中)

- 连结性别

- 离网

- 併网

- 混合式(风力发电+电池/光伏)

- 按安装位置

- 屋顶/楼宇一体化型

- 独立式塔架(地面安装)

- 透过使用

- 住宅

- 商业(零售、办公、饭店)

- 工业和仓储业

- 农业和水产养殖

- 电信塔和远端监控站点

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 策略性倡议(併购、伙伴关係、购电协议)

- 市场占有率分析(主要企业的市场排名/份额)

- 公司简介

- Aeolos Wind Energy Ltd

- Bergey Windpower Co.

- City Windmills Holdings PLC

- Wind Energy Solutions BV

- SD Wind Energy Ltd

- UNITRON Energy Systems Pvt Ltd

- Northern Power Systems Inc.

- Shanghai Ghrepower Green Energy Co. Ltd

- TUGE Energia OU

- Ryse Energy

- Kingspan Group Plc(Wind Division)

- Eocycle Technologies Inc.

- XZERES Wind Corp.

- Fortis Wind Energy BV

- HY Energy Co. Ltd

- Endurance Wind Power Inc.

- Kliux Energies International

- Pika Energy(Generac)

- Envergate Energy AG

- Suzlon Energy Ltd

第七章 市场机会与未来展望

The Small Wind Turbine Market size is estimated at USD 2.31 billion in 2025, and is expected to reach USD 3.43 billion by 2030, at a CAGR of 8.20% during the forecast period (2025-2030).

Growth is driven by policy incentives, vertical-axis technology advances, and rising use in telecom, agricultural, and distributed energy systems. Public funding programs in North America, the European Union, and Asia accelerate deployments, while machine-learning-enabled turbine optimization reduces lifetime energy costs and improves reliability. Corporate power purchase agreements expand demand for on-grid projects, and hybrid wind-solar systems extend the addressable market in regions with variable wind resources. Cost rivalry with rooftop solar remains a restraint in the sub-10 kW segment, but efficiency gains and new siting rules narrow the gap.

Global Small Wind Turbine Market Trends and Insights

Rapid Electrification of Remote Islands across the Caribbean

Remote island utilities are replacing diesel systems with hybrid renewable microgrids, including small wind turbines. Governments and multilateral lenders have earmarked concessional finance that reduces upfront project costs and broadens developer participation. Turbine suppliers that offer corrosion-resistant coatings and modular logistics packages gain a competitive advantage in these markets. The average installed capacity per site remains below 50 kW, aligning with 0-20 kW product lines. Steady trade winds support capacity factors above 35%, improving payback periods relative to solar-only designs. Island electrification programs adopt performance-based tariffs that reward high availability, reinforcing the value of digital monitoring platforms integrated into new turbine models.

Sub-5 kW Turbine Demand Surge from USDA Rural Energy Grants

The USD 180 million Rural Energy for America Program allocation in 2025 prioritizes micro wind systems for farms and rural small businesses. Grants cover up to 50% of capital costs, enabling paybacks under six years in regions with mean wind speeds above 6 m/s. The National Renewable Energy Laboratory's Competitiveness Improvement Project funds prototype certification that unlocks third-party financing, addressing historical bankability gaps. More than 400 farms are targeted, driving an incremental 25 MW of cumulative micro-class installations by 2027. Coupling turbines with barn-roof solar arrays allows producers to offset peak daytime loads and evening irrigation demand. Manufacturers that complete UL 6141 certification under the program qualify for preference in federal procurement.

Height-Based Zoning Restrictions in Urban Europe

Municipal height limits constrain turbine hub height to 10 m or less in many historic districts, curbing energy yield. Variance requests often require shadow-flicker and visual assessments that lengthen project timelines. Noise measurement rules rely on modeled rather than empirical data, adding engineering costs. Fragmented jurisdiction means identical projects face divergent rules between adjacent municipalities, discouraging developers from citywide rollouts. EU Wind Power Package guidance seeks harmonization, but local cultural heritage bodies retain veto power. Suppliers respond with stub-mast vertical-axis designs that fit below parapets, though lower swept area reduces annual output.

Other drivers and restraints analyzed in the detailed report include:

- China's Zero-Carbon Industrial Parks Mandating On-Site Renewables

- EU Rooftop-Renewables Directive Boosting Building-Integrated Wind

- High Levelized Cost of Energy versus Rooftop Solar in Sub-10 kW Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Horizontal configurations retained 68% of 2024 revenue on proven aerodynamics and supply chain maturity. The segment dominated large-farm repowering and rural household replacements. Manufacturers standardize 2-20 kW models to meet USDA and Indian telecom bid specifications, leveraging volume economies. The small wind turbine market size for vertical axis units grew quickly from a lower base and is forecast to post 14% CAGR, outpacing horizontal units. Vertical turbines thrive in disrupted wind flows near rooftops and street-level poles, where omnidirectional blades capture multidirectional gusts. Genetic learning algorithms that modulate pitch through each rotation improve power coefficients by up to 0.45, close to Betz-limit benchmarks. Reduced moving parts allow ground-level gearboxes, cutting maintenance truck rolls by 30% and encouraging commercial fleet adopters.

Vertical axis suppliers partner with facade engineers to embed turbines into curtain walls, meeting EU innovative-technology quotas. Savonius and Darrieus hybrids with contra-rotating rotors minimize torque ripple, lowering the acoustic signature to within 35 dB at a 5 m distance. University of Tokyo field tests verify 15-year bearing life even under typhoon gusts, addressing durability perceptions. Developers structure leasing deals that bundle services and recycle obligations, satisfying circular economy rules in China and the EU. The narrative positions vertical turbines as complementary rather than disruptive, allowing mixed arrays that smooth site energy output.

Micro class 0-5 kW systems delivered 46% of the small wind turbine market share in 2024, supported by grant-funded installations on farms, cabins, and roadside sensors. Average selling price fell 6% year-on-year as electronics commoditized, yet post-installation service revenues rose. Medium 21-100 kW units expand at 11% CAGR through 2030, serving telecom towers, industrial parks, and data-center campuses. Developers favor IEC 61400-2-certified models that integrate fault ride-through and reactive power support, enabling grid connection without separate converters. At 60 kW size, unit cost per kW drops below USD 2,300, closing the gap to rooftop solar plus storage stacks.

The small wind turbine market size for 6-20 kW equipment grows steadily in peri-urban business estates where grid tariffs include demand charges. Farmers with high refrigeration loads choose 15 kW turbines to offset evening peaks. Historical adoption benefits from accumulated installer skillsets that shorten project lead times. Medium-class suppliers bundle extended warranties that guarantee 97% technical availability, unlocking low-cost debt from green banks. Interoperable SCADA links wind output to onsite battery dispatch, optimizing self-consumption and avoiding interconnection curtailments.

The Small Wind Turbine Market Report is Segmented by Axis Type (Horizontal Axis Wind Turbines and Vertical Axis Wind Turbines), Capacity Rating (0 To 5 KW, 6 To 20 KW, and 21-100 KW), Connectivity (Off-Grid, On-Grid, and Hybrid), Installation Location (Rooftop/Building-Integrated and Freestanding Tower), Application (Residential, Commercial, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More).

Geography Analysis

Asia-Pacific dominated the small wind turbine market with a 48% share in 2024 and is growing at a 10% CAGR on the back of Chinese industrial decarbonization and Indian telecom electrification. China's mandate for 40% certified green factory output by 2030 compels economic zones to install rooftop and courtyard turbines, while Jiangsu's recycling standards promote circular supply chains. India's tower operators commit to renewable energy for backup power, and hybrid tenders specify 5 kW microturbines alongside PV and lithium packs. Japan maintains stringent acoustic rules yet supports vertical-axis demonstrations near rail corridors. ASEAN island states deploy community microgrids, and Vietnamese manufacturers export 10 kW turbines to regional fishing fleets.

Europe remains a mature base where regulatory clarity supports incremental growth. The Renewables Directive revision cuts permitting delays for projects below 50 kW, boosting urban adoption. Germany exempts sub-10 m turbines from planning approval in selected Lander, cutting soft costs by 25%. Nordic data-center PPAs underpin a robust on-grid pipeline; Norsk Hydro's 29-year 235 MW wind PPA exemplifies confidence in long-dated offtake. Denmark's stringent 39 dB noise cap influences product acoustics exported worldwide. The United Kingdom supports island onshore wind expansions, including micro-turbines for community benefit shares.

North America's policy landscape rejuvenates demand. The USDA's USD 180 million grant pool accelerates farm deployments, and NREL's USD 3.2 million competitiveness fund advances certification pathways. Canada's 247 MW order boom for Nordex utility-scale turbines raises component localization that benefits small wind suppliers through shared transport links. However, residential adoption lags due to rooftop solar price advantage. States such as New York pilot feed-in tariffs specific to small wind, while California trials microgrid tariffs that reward multi-technology systems. Mexico's rural electrification agency reopens tenders for a hybrid kit, including 1.5 kW wind units for off-grid clinics.

- Aeolos Wind Energy Ltd

- Bergey Windpower Co.

- City Windmills Holdings PLC

- Wind Energy Solutions BV

- SD Wind Energy Ltd

- UNITRON Energy Systems Pvt Ltd

- Northern Power Systems Inc.

- Shanghai Ghrepower Green Energy Co. Ltd

- TUGE Energia OU

- Ryse Energy

- Kingspan Group Plc (Wind Division)

- Eocycle Technologies Inc.

- XZERES Wind Corp.

- Fortis Wind Energy BV

- HY Energy Co. Ltd

- Endurance Wind Power Inc.

- Kliux Energies International

- Pika Energy (Generac)

- Envergate Energy AG

- Suzlon Energy Ltd (<=100 kW segment)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Electrification of Remote Islands across the Caribbean

- 4.2.2 Sub-5 kW Turbine Demand Surge from U.S. USDA "Rural Energy for America" Grants

- 4.2.3 China's "Zero-Carbon Industrial Parks" Mandating On-site Renewables

- 4.2.4 EU Rooftop-Renewables Directive Boosting Building-Integrated Wind

- 4.2.5 Telecom Tower Hybridization Agenda in India & ASEAN

- 4.2.6 Increasing Corporate PPAs for Micro-Wind in Nordics' Data-Center Cluster

- 4.3 Market Restraints

- 4.3.1 Height-Based Zoning Restrictions in Urban Europe

- 4.3.2 Acoustic-Emission Standards Tightening in Japan

- 4.3.3 High LCOE versus Rooftop PV in North America <10 kW segment

- 4.3.4 Bankability Gaps due to Absence of Long-Term O&M Ecosystem in Africa

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Axis Type

- 5.1.1 Horizontal Axis Wind Turbines (HAWT) (Upwind, and Downwind)

- 5.1.2 Vertical Axis Wind Turbines (VAWT) (Savonius, Darrieus and Giromill)

- 5.2 By Capacity Rating (kW)

- 5.2.1 0 to 5 kW (Micro)

- 5.2.2 6 to 20 kW (Small)

- 5.2.3 21 to 100 kW (Medium)

- 5.3 By Connectivity

- 5.3.1 Off-Grid

- 5.3.2 On-Grid

- 5.3.3 Hybrid (Wind + Battery/PV)

- 5.4 By Installation Location

- 5.4.1 Rooftop/Building-Integrated

- 5.4.2 Freestanding Tower (Ground-Mounted)

- 5.5 By Application

- 5.5.1 Residential

- 5.5.2 Commercial (Retail, Offices, Hotels)

- 5.5.3 Industrial and Warehousing

- 5.5.4 Agricultural and Aquaculture

- 5.5.5 Telecom Towers and Remote Monitoring Sites

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Nordic Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Australia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves (M&A, Partnerships, PPAs)

- 6.2 Market Share Analysis (Market Rank/Share for key companies)

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Aeolos Wind Energy Ltd

- 6.3.2 Bergey Windpower Co.

- 6.3.3 City Windmills Holdings PLC

- 6.3.4 Wind Energy Solutions BV

- 6.3.5 SD Wind Energy Ltd

- 6.3.6 UNITRON Energy Systems Pvt Ltd

- 6.3.7 Northern Power Systems Inc.

- 6.3.8 Shanghai Ghrepower Green Energy Co. Ltd

- 6.3.9 TUGE Energia OU

- 6.3.10 Ryse Energy

- 6.3.11 Kingspan Group Plc (Wind Division)

- 6.3.12 Eocycle Technologies Inc.

- 6.3.13 XZERES Wind Corp.

- 6.3.14 Fortis Wind Energy BV

- 6.3.15 HY Energy Co. Ltd

- 6.3.16 Endurance Wind Power Inc.

- 6.3.17 Kliux Energies International

- 6.3.18 Pika Energy (Generac)

- 6.3.19 Envergate Energy AG

- 6.3.20 Suzlon Energy Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment