|

市场调查报告书

商品编码

1851639

磁感测器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Magnetic Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

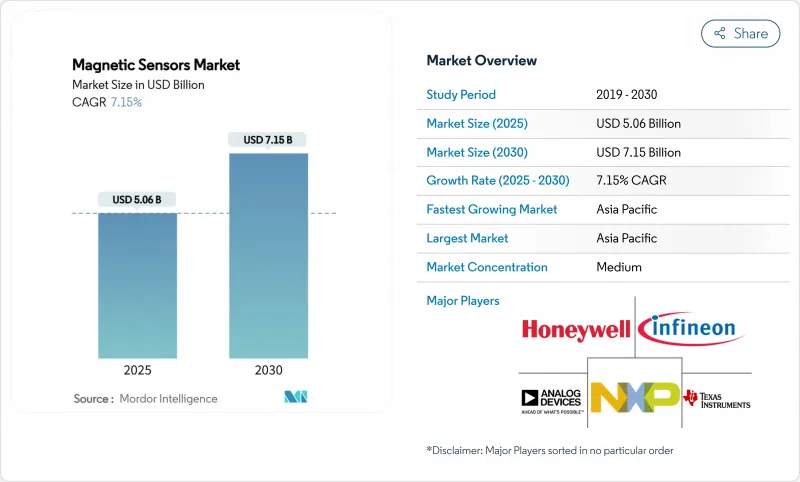

预计到 2025 年,磁感测器市场规模将达到 50.6 亿美元,到 2030 年将达到 71.5 亿美元,复合年增长率为 7.15%。

电动车动力系统的强制性要求、工业4.0生产线的进步以及三轴感测技术在消费性电子设备中的应用,共同支撑着这一稳步增长。汽车製造商正在指定更高精度的位置和电流感测器以满足功能安全目标,而智慧型手机和穿戴式装置品牌则正在整合微型隧道磁阻(TMR)晶粒,用于扩增实境和室内导航功能。资料中心营运商倾向于使用量子级TMR磁头来提高储存密度,这促使供应商转向高端、高灵敏度的设计。稀土磁铁的供应链风险依然高,迫使企业投资于回收、本地加工和替代材料。由于领先供应商专注于垂直整合、扩展TMR产品组合以及製定数位化输出蓝图以在霍尔效应驱动的价格环境下保护净利率,因此市场竞争较为温和。

全球磁感测器市场趋势与洞察

电动车动力系统的强制性电气化

欧盟和加州的电动车法规正在推动各种感测器的广泛应用,涵盖从转子位置和温度追踪到电池管理子系统等诸多领域。大陆集团的e-Motor转子温度感测器测量精度低至3°C,使设计人员能够在保证性能的同时减少稀土元素磁体的用量。如此高的精度既符合法规要求,也有助于电动车平台实现成本控制目标。

三轴磁感测技术在智慧型手机和穿戴式装置中已广泛应用。

行动电话厂商正在整合三维磁感测器,以实现扩增实境迭加和精准的室内导航。小型TMR晶粒满足角度精度和功耗要求,有助于跨产业需求的拓展。 TDK的Nivio™ xMR组件测量生物磁场的尺寸比实验室级SQUID更小,这显示其在医疗设备领域具有潜在的应用价值。

通用霍尔效应积体电路的价格已经下降

霍尔效应装置正面临来自中国低成本晶圆厂日益激烈的竞争。自2024年以来,钕的价格已下跌42%,这正在削弱高端供应商曾经拥有的材料成本优势,加剧了竞争压力。因此,供应商正将研发重心转向差异化的TMR和GMR产品线,并整合讯号处理模组以保持价格竞争力。

细分市场分析

TMR感测器正以8.80%的复合年增长率快速成长,是主要技术中成长最快的。霍尔效应解决方案在成熟的模具和极具吸引力的价格的推动下,预计到2024年仍将占据磁感测器市场48.0%的份额。然而,汽车安全系统和工业4.0机器人对-40°C至+150°C温度范围内亚度级角度精度的要求日益提高,而这正是TMR感测器的优势所在。 Allegro MicroSystems公司推出的XtremeSense™感测器,其灵敏度是霍尔效应感测器的10倍,电流消耗降低了50%。

GMR 是一款中阶产品,针对那些希望在不承担 TMR 过高成本的情况下获得更高灵敏度的客户;而 AMR 则是一款小众产品,适用于需要简单讯号链的工业线性编码器。磁通门和 SQUID 装置则应用于高阶实验室、国防和医疗设备。鑑于这种技术组合,霍尔效应元件很可能在对成本敏感的领域继续占据主导地位,但 TMR 将在磁感测器市场占据大部分增值份额。

到2024年,汽车产业将占据磁感测器市场规模的56.0%。虽然电动动力传动系统和ADAS的普及巩固了这个市场基础,但资料中心才是真正引人注目的成长点。用于HDD和SSD的量子级TMR磁头正帮助超大规模资料中心以9.60%的复合年增长率提升Terabyte储存密度。营运商还在配电单元中部署霍尔电流感测器,以优化机架级能耗,协助实现脱碳目标。在医疗保健领域,TDK的生物磁创新技术正推动非侵入式影像和植入监测技术的发展,开启新的应用前景。

磁感测器市场按技术(霍尔效应、AMR、GMR、TMR 及其他技术)、应用(汽车、消费性电子及其他)、终端用户产业(汽车OEM厂商和一级供应商、消费性电子OEM厂商及其他)、输出讯号(数位、类比)和地区进行细分。市场预测以美元计价。

区域分析

亚太地区将在2024年以42.0%的市占率引领磁感测器市场,年复合成长率将达到9.40%,这主要得益于中国半导体製造厂和日本精密感测器技术的强劲成长。中国稀土出口限制既是挑战也是机会。国内晶圆厂将获得稳定的磁铁供应,而出口型汽车製造商则将寻求替代来源。日本的TMR(三磁铁磁阻)蓝图将利用其在计量技术方面的优势推动感测器小型化,从而惠及汽车和医疗产业。韩国的储存设备巨头将增加对高密度TMR磁头的需求,而印度不断扩大的汽车生产也将扩大该地区的基本客群。

儘管原材料供应面临挑战,北美市场依然至关重要。 Allegro MicroSystems 预测,2024 财年销售额将达到 10.5 亿美元,年增 38%,主要得益于电动车领域的成长。像 Noveon Magnetics 在德克萨斯的工厂这样的计划,虽然得到了州政府对国内稀土加工的激励措施支持,但其产量在未来几年内仍将落后于亚洲。汽车製造商严重依赖当地的感测器设计中心来满足美国公路交通安全管理局 (NHTSA) 的软体更新要求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电动车动力系统的强制性电气化

- 智慧型手机和穿戴式装置中三轴磁感测技术的普及

- 汽车产业对ADAS和电动马达定位的需求日益增长

- 工厂自动化向工业4.0转型

- 车载直流快速充电电流监测

- 在资料中心的硬碟/固态硬碟磁头中采用量子级TMR技术

- 市场限制

- 通用霍尔效应积体电路的价格已经下降

- 稀土元素磁铁供应链的集中化

- 高速电气化平台的电磁干扰合规成本

- xMR感测器专利相关的智慧财产权诉讼风险

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过技术

- 霍尔效应

- 异性磁电阻(AMR)

- 巨磁电阻(GMR)

- 隧道磁阻(TMR)

- 其他技术

- 透过使用

- 车

- 消费性电子产品

- 工业自动化

- 医疗保健和医疗设备

- 航太/国防

- 资料中心和伺服器存储

- 其他用途

- 按最终用途行业划分

- 汽车OEM厂商和一级供应商

- 消费性电子产品OEM厂商

- 工业设备製造商

- 能源与公共产业

- 医疗保健原始设备製造商

- 航太与国防主控

- 透过输出讯号

- 数位式(IC/SPI、SENT、PSI5)

- 类比(线性电压/电流)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- ASEAN-5

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 土耳其

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Infineon Technologies AG

- Allegro MicroSystems LLC

- NXP Semiconductors NV

- TDK Corporation

- Honeywell International Inc.

- Analog Devices Inc.

- STMicroelectronics NV

- Murata Manufacturing Co. Ltd

- TE Connectivity Ltd

- Texas Instruments Inc.

- NVE Corporation

- Crocus Technology Inc.

- Omron Corporation

- Asahi Kasei Microdevices(AKM)

- Diodes Incorporated

- Melexis NV

- ams-OSRAM AG

- Sensitec GmbH

- TT Electronics plc

- Robert Bosch GmbH

- Lake Shore Cryotronics Inc.

第七章 市场机会与未来展望

The magnetic sensor market size is worth USD 5.06 billion in 2025 and is forecast to reach USD 7.15 billion by 2030, reflecting a 7.15% CAGR.

Rising electric-vehicle drivetrain mandates, the advance of Industry 4.0 production lines, and expanding 3-axis sensing in consumer devices underpin this steady growth. Automakers are specifying higher-accuracy position and current sensors to meet functional-safety targets, while smartphone and wearable brands integrate miniature tunnel-magnetoresistance (TMR) dies for augmented-reality and indoor-navigation functions. Data-center operators champion quantum-grade TMR heads to lift storage density, pushing suppliers toward premium, high-sensitivity designs. Supply-chain risk around rare-earth magnets remains an overhang, forcing companies to invest in recycling, local processing, and substitute materials. Competitive intensity is moderate as leading vendors focus on vertical integration, TMR portfolio expansion, and digital-output roadmaps to protect margins in an environment of Hall-effect price erosion.

Global Magnetic Sensors Market Trends and Insights

EV drivetrain electrification mandates

Electric-vehicle regulations in the European Union and California spur wider sensor deployment, stretching from rotor position and temperature tracking to battery-management subsystems. Continental's e-Motor Rotor Temperature Sensor trims measurement tolerance to 3 °C, allowing designers to cut rare-earth magnet content while protecting performance assemblymag.com. Such precision supports both compliance targets and cost-containment strategies across EV platforms.

Proliferation of 3-axis magnetic sensing in smartphones and wearables

Handset vendors embed 3-D magnetic sensors to deliver augmented-reality overlays and accurate indoor navigation. Miniature TMR dies meet the angular-accuracy and power requirements, stimulating cross-industry demand spillovers. TDK's Nivio(TM) xMR component measures biomagnetic fields in a footprint smaller than laboratory-grade SQUIDs, hinting at medical-device spill-over potential.

Price erosion in commoditised Hall-effect ICs

Hall-effect devices face rising competition from low-cost Chinese fabs. The 42% fall in neodymium prices since 2024 compounds pressure by eroding the material-cost moat once held by premium suppliers. Vendors therefore channel R&D into differentiated TMR and GMR lines or integrate signal-processing blocks to sustain pricing power.

Other drivers and restraints analyzed in the detailed report include:

- Growing ADAS and e-motor position needs in automotive

- Factory automation shift to Industry 4.0

- Supply-chain concentration in rare-earth magnetics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

TMR sensors are expanding at 8.80% CAGR, the fastest pace among major technologies. Hall-effect solutions still hold 48.0% of the magnetic sensor market share in 2024 due to mature tooling and attractive pricing. Yet automotive safety systems and Industry 4.0 robots now specify sub-degree angular accuracy across -40 °C to +150 °C ranges, a window where TMR excels. Allegro MicroSystems markets XtremeSense(TM) implementations with 10 X sensitivity and 50% lower current draw than Hall-effect peers.

GMR represents a middle path for customers demanding enhanced sensitivity without the cost premium of TMR, while AMR retains a niche in linear industrial encoders requiring simple signal chains. Fluxgate and SQUID devices serve high-end laboratory, defense, and medical equipment. The technology mix suggests Hall-effect incumbency in cost-sensitive lines will persist, but TMR will absorb most incremental value creation within the magnetic sensor market.

Automotive accounted for 56.0% of the magnetic sensor market size in 2024. The proliferation of electric powertrains and ADAS keeps that base stable, yet the standout growth story is data centers. Quantum-grade TMR heads for HDDs and SSDs help hyperscalers raise terabyte density at a 9.60% CAGR. Operators also deploy Hall-based current sensors in power-distribution units to optimize rack-level energy use amid decarbonization targets. Industrial automation contributes steady volume as factories digitize assembly lines, while healthcare opens nascent upside through non-invasive imaging and implant monitoring supported by TDK's biomagnetic innovations.

Magnetic Sensor Market is Segmented by Technology (Hall-Effect, AMR, GMR, TMR, Other Technologies), Application (Automotive, Consumer Electronics, and More), End-Use Industry (Automotive OEMs and Tier-1s, Consumer Electronics OEMs, and More), Output Signal (Digital, Analog), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the magnetic sensor market with 42.0% share in 2024 and is heading toward a 9.40% CAGR, powered by China's semiconductor fabs and Japan's precision sensor know-how. Chinese export curbs on rare-earths create both threat and windfall: domestic fabs gain a captive magnet supply, while export-oriented carmakers scramble for alternate sourcing. Japan's TMR roadmap leverages metrology depth to push sensor miniaturization that feeds both auto and medical verticals. South Korea's storage-device majors lift demand for high-density TMR heads, and India's expanding vehicle output widens the regional customer base.

North America remains pivotal despite material-supply pain points. Allegro MicroSystems booked USD 1.05 billion sales in fiscal 2024, up 38% in e-mobility-linked lines. State incentives for domestic rare-earth processing underpin projects such as Noveon Magnetics' Texas plant, though volumes will lag Asia for several years. Automakers rely heavily on local sensor design centers to meet National Highway Traffic Safety Administration software-update requirements.

- Infineon Technologies AG

- Allegro MicroSystems LLC

- NXP Semiconductors NV

- TDK Corporation

- Honeywell International Inc.

- Analog Devices Inc.

- STMicroelectronics NV

- Murata Manufacturing Co. Ltd

- TE Connectivity Ltd

- Texas Instruments Inc.

- NVE Corporation

- Crocus Technology Inc.

- Omron Corporation

- Asahi Kasei Microdevices (AKM)

- Diodes Incorporated

- Melexis NV

- ams-OSRAM AG

- Sensitec GmbH

- TT Electronics plc

- Robert Bosch GmbH

- Lake Shore Cryotronics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV drivetrain electrification mandates

- 4.2.2 Proliferation of 3-axis magnetic sensing in smartphones and wearables

- 4.2.3 Growing ADAS and e-motor position needs in automotive

- 4.2.4 Factory automation shift to Industry 4.0

- 4.2.5 On-board DC-fast-charging current monitoring

- 4.2.6 Quantum-grade TMR adoption in data-center HDD/SSD heads

- 4.3 Market Restraints

- 4.3.1 Price erosion in commoditised Hall-effect ICs

- 4.3.2 Supply-chain concentration in rare-earth magnetics

- 4.3.3 EMI compliance costs for high-speed electrification platforms

- 4.3.4 IP litigation risk around xMR sensor patents

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Hall-Effect

- 5.1.2 Anisotropic Magnetoresistance (AMR)

- 5.1.3 Giant Magnetoresistance (GMR)

- 5.1.4 Tunnel Magnetoresistance (TMR)

- 5.1.5 Other Technologies

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Consumer Electronics

- 5.2.3 Industrial Automation

- 5.2.4 Healthcare and Medical Devices

- 5.2.5 Aerospace and Defense

- 5.2.6 Data-Center and Server Storage

- 5.2.7 Other Applications

- 5.3 By End-Use Industry

- 5.3.1 Automotive OEMs and Tier-1s

- 5.3.2 Consumer Electronics OEMs

- 5.3.3 Industrial Equipment Manufacturers

- 5.3.4 Energy and Utilities

- 5.3.5 Healthcare OEMs

- 5.3.6 Aerospace and Defense Primes

- 5.4 By Output Signal

- 5.4.1 Digital (IC/SPI, SENT, PSI5)

- 5.4.2 Analog (Linear Voltage/Current)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN-5

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Turkey

- 5.5.5.2 Israel

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 UAE

- 5.5.5.5 South Africa

- 5.5.5.6 Nigeria

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Allegro MicroSystems LLC

- 6.4.3 NXP Semiconductors NV

- 6.4.4 TDK Corporation

- 6.4.5 Honeywell International Inc.

- 6.4.6 Analog Devices Inc.

- 6.4.7 STMicroelectronics NV

- 6.4.8 Murata Manufacturing Co. Ltd

- 6.4.9 TE Connectivity Ltd

- 6.4.10 Texas Instruments Inc.

- 6.4.11 NVE Corporation

- 6.4.12 Crocus Technology Inc.

- 6.4.13 Omron Corporation

- 6.4.14 Asahi Kasei Microdevices (AKM)

- 6.4.15 Diodes Incorporated

- 6.4.16 Melexis NV

- 6.4.17 ams-OSRAM AG

- 6.4.18 Sensitec GmbH

- 6.4.19 TT Electronics plc

- 6.4.20 Robert Bosch GmbH

- 6.4.21 Lake Shore Cryotronics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

旋转磁编码器市场报告:趋势、预测和竞争分析(至2035年)

旋转磁编码器市场报告:趋势、预测和竞争分析(至2035年) 2026-2030年全球磁感测器市场

2026-2030年全球磁感测器市场 磁阻感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、组件、最终用户、材质、功能、设备及解决方案划分

磁阻感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、组件、最终用户、材质、功能、设备及解决方案划分 全球奈米磁性元件市场规模、份额、趋势和成长分析报告(2026-2034)全球磁感测器市场:依技术、应用、终端用户产业、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年)磁性感测器市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)

全球奈米磁性元件市场规模、份额、趋势和成长分析报告(2026-2034)全球磁感测器市场:依技术、应用、终端用户产业、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年)磁性感测器市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034) 2026年全球汽车磁感测器市场报告2026年全球磁感测器市场报告

2026年全球汽车磁感测器市场报告2026年全球磁感测器市场报告 石油天然气磁测距市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年

石油天然气磁测距市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年 汽车磁感测器市场规模、份额和成长分析(按类型、磁密度、应用、最终用户和地区划分)—2026-2033年产业预测

汽车磁感测器市场规模、份额和成长分析(按类型、磁密度、应用、最终用户和地区划分)—2026-2033年产业预测